Sustainable development and green growth are high on Costa Rica’s agenda. The country has a long-standing environmental policy, a comprehensive legal framework and well-developed mechanisms of environmental democracy. However, institutional capacity and financial resource constraints have hampered effective implementation. The sheer scale of investment needed to achieve the Sustainable Development Goals calls for improving the efficiency of public spending, mobilising private finance, strictly enforcing regulations and providing adequate incentives. This chapter assesses the environmental effectiveness and economic efficiency of the environmental governance and policy mix, including regulatory, fiscal and economic instruments. It also looks at efforts to increase investment in environment-related infrastructure and services and encourage green business practices.

OECD Environmental Performance Reviews: Costa Rica 2023

Chapter 2. Towards a green and inclusive growth

Abstract

2.1. Introduction

Costa Rica is the oldest democracy in Central America whose solid institutions have ensured stability over the years. The country has shown continued commitment to aligning its legislation, policies and practices with OECD standards. The Sustainable Development Goals (SDGs) are high on Costa Rica’s political agenda. However, despite an extensive suite of policies addressing the SDGs, it needs to further strengthen policy coherence to achieve them cost effectively by 2030.

Costa Rica is a middle-income and open economy that has made considerable economic, social and environmental progress in the last 20 years. However, additional effort is required to pursue many of the environment-related SDGs (Chapter 1). The scale of the investment needed is remarkable, while the government is facing severe fiscal constraints that are expected to persist. With a high public debt, maintaining fiscal prudence is critical for macroeconomic sustainability (OECD, 2023[1]). It is, therefore, essential to improve the quality and efficiency of public management and spending, as well as to mobilise private finance for investment in basic infrastructure, environmental protection, climate change mitigation and resilience. There is also a need to further encourage households and businesses to make sustainable consumption and production choices. To that end, Costa Rica should promote compliance with environmental regulations, provide stronger price signals and remove harmful subsidies, while supporting vulnerable groups in getting out of poverty and informal jobs.

2.2. Ensuring sound governance for sustainable development

2.2.1. Strategic framework for achieving the SDGs

Costa Rica is strongly committed to meeting the 17 SDGs. In 2016, representatives of the parliament, government and judiciary, local governments and various social stakeholders signed the “Social Pact for the Implementation of the SDGs”, the first such agreement in the world. In 2020, the government submitted its second SDG voluntary national review to the United Nations (UN) High-level Political Forum on Sustainable Development. The government has actively used the SDGs as guidelines for its main national policies, including public investment plans (Section 2.6). Its strategy prioritises SDGs related to poverty and inequality, sustainable production and consumption, and resilient infrastructure and sustainable communities; these are considered instrumental to achieve all other goals.

Costa Rica has adopted a wide range of strategic policies and plans, which are broadly aligned with the SDGs. Among the key documents are the National Decarbonisation Plan (PND) 2018-50, the National Climate Change Adaptation Policy 2020-30, the National Policy for Sustainable Production and Consumption 2018-30 and the National Biodiversity Strategy 2016-25 (Chapters 1 and 3). The National Development and Public Investment Plan (PNDIP) 2023-26 is the second multiannual investment plan to link investment projects to the SDGs they contribute to achieve. The government regards the PNDIP as a key instrument to achieve the SDGs. Several other sectoral and cross-sectoral strategies and programmes have been adopted over the years. However, many policy goals and objectives do not translate into concrete measures and adequate financing (CONARE, 2022[2]).

Progress has been made towards all SDGs. However, Costa Rica has achieved only 17 of 112 SDG‑related targets, most of them linked to the coverage of basic needs and adoption of policy tools and frameworks recommended by UN Agenda 2030. It is expected to meet seven additional targets by 2030, mostly related to health (OECD, 2022[3]). It has nearly achieved SDG 7 (Affordable and clean energy), especially regarding access to electricity and share of renewable energy. However, further efforts are needed to achieve most of the SDGs related to waste, water, oceans, terrestrial biodiversity and climate, as well as to reduce informality in the job market, and tackle poverty and inequality (Chapters 1 and 3).

2.2.2. Institutional framework

The institutional framework for environmental management and sustainable development is complex. As in many countries, several ministries share responsibilities for sustainable development and environmental policies. The Ministry of Environment and Energy (MINAE) is the main government entity in charge of environmental matters. Other ministries with environmental responsibilities include health (MINSA), agriculture and livestock (MAG), and public works and transport (MOPT). MINAE, its subsidiary bodies and other institutions with environmental competences, form the Environment and Energy Sector (Box 2.1). There are also autonomous institutions with environment-related competencies that lie outside the Environment and Energy Sector.1 Overall, environmental governance comprises over 35 subsidiary bodies of different government ministries and other decentralised institutions, with varying degrees of autonomy and with limited steering and accountability mechanisms. This is a common feature of Costa Rica’s public administration (OECD, 2021[4]).

The environmental legislation establishes several inter-ministerial bodies to ensure co‑ordination at the political, technical and operational levels. These include the National Environmental Council, chaired by the President of the Republic and comprising the MINAE minister and several other ministers.2 The Sectoral Council on Environment and Energy co‑ordinates activities of the institutions within the Environment and Energy Sector (Box 2.1). Several entities were created to promote environmental considerations in sectoral policies, such as the Commission on Sustainable Production and Consumption, the Technical Inter-ministerial Committee on Climate Change and the Technical Commission on the Circular Economy.

In addition, a governance system is in place for implementation of the 17 SDGs. The President of the Republic chairs the High-Level Council for the SDGs, which oversees the design, funding and implementation of the policies to fulfil the goals. The High-Level Council also comprises the MINAE minister, the ministers responsible for economic planning and foreign affairs, and the Chief Executive of the Joint Social Welfare Institute. Its composition and functions partly coincide with those of the National Environmental Council. The Technical Secretariat for the SDGs, within the Ministry of National Planning and Economic Policy (MIDEPLAN), is tasked with day-to-day co‑ordination of the SDGs across line ministries. The National Institute of Statistics and Census manages the system of indicators to monitor progress towards the SDGs.

As repeatedly noted by the Office of the Comptroller General, the multitude of subsidiary bodies, decentralised institutions and inter-institutional councils and committees generates overlap and fragmentation, while dispersing spending. This hinders policy coherence and implementation effectiveness (CGR, 2022[5]). Costa Rica launched some reforms to address institutional fragmentation. These include a 2022 legislative proposal to consolidate MINAE and reduce the number of its subsidiary bodies. The country could build on this proposal to redesign and merge environmental institutions (subsidiary and autonomous entities), as well as to streamline activities of the various councils and committees engaged in horizontal co‑ordination and multi-level governance. This rationalisation should be based on transparent criteria for maintaining or establishing institutional entities, a clear definition of their responsibilities and mechanisms to monitor their performance.

2.2.3. Multi-level governance

MIDEPLAN oversees implementation of national policies at the local level, including policies relevant to the environment. Costa Rica is divided into 90 local governments (82 cantons or municipalities and 8 district municipal councils) that have administrative powers. The Cantonal Inter-institutional Co‑ordination Councils (CCCI) co‑ordinate the design, execution and oversight of public policies at local level. As of 2021, 60 municipalities had a working CCCI (OECD, 2021[4]).

Box 2.1. The Environment and Energy Sector

Entities under the aegis of Ministry of Environment and Energy (MINAE)

The National Environmental Technical Secretariat (SETENA) manages environmental impact assessment and permitting, and monitors compliance with environmental regulations.

The Environmental Administrative Tribunal (TAA) arbitrates complaints and referrals for violations of the environmental legislation. It can impose administrative sanctions.

The Environmental Comptroller supervises compliance with environmental legislation, investigates environmental complaints and reports violations to the judiciary and/or the TAA.

The National Meteorological Institute (IMN) co‑ordinates the meteorological and climatologic activities of the country. It produces the emission inventories of air pollutants and greenhouse gases.

The National Biodiversity Management Commission (CONAGEBIO) formulates policies for the conservation and sustainable use of biodiversity, as well as access to genetic resources. It oversees the implementation and monitoring of the national biodiversity policy and strategy.

The National System of Conservation Areas (SINAC) oversees the protected area network. It is also tasked with the integrated management of natural resources (forest, wildlife, water) within and outside protected areas.

The National Forestry Financing Fund (FONAFIFO) finances afforestation and reforestation activities led by small and medium-sized producers. It manages the Programme of Payments for Environmental Services.

Other entities: the Commission for the Management of the Upper Reventazón River Basin; the Board of Directors of San Lucas Island National Park; the Board of Directors for the Manuel Antonio National Park Trust; and the Pacific Marine Park.

Autonomous institutions

The Costa Rican Institute of Aqueducts and Sewers (AyA) plans, regulates and manages drinking water supply and wastewater collection and disposal, partly through the community water associations.

The Public Services Regulatory Authority (ARESEP) sets service tariffs and monitors the quality and reliability of electricity and fuel supply, water and wastewater services, and public transport.

The National Emergency Commission (CNE) co‑ordinates activities to prevent and respond to natural disasters, including the National Emergency Prevention and Response System.

The Costa Rican Institute of Electricity (ICE), the state-owned electricity transmission system operator, manages the electricity grids and is the main electricity supplier.

The Costa Rican Petroleum Refining Company (RECOPE) is the state-owned company that imports, refines and distributes oil and oil products under a monopoly regime. It also develops and manages the related infrastructure.

The National Forestry Office manages forestry resources and promotes investment in the forestry sector.

Other autonomous bodies: the National Company of Energy and Light, the Public Services Enterprise of Heredia, and the Administrative Board of the Municipal Electric Service of Cartago.

Source: Country’s submission.

The country is divided geographically for various purposes. Several institutions for multi-level governance have different objectives, such as the Regional and Local Councils of Conservation Areas (Chapter 3), the Watershed Committees and the Regional Development Councils. This creates an overly complex, expensive and fragmented system (OECD, 2021[4]).Two national associations of municipalities represent the interests of local governments in relation to central authorities.3 However, unlike many OECD countries, Costa Rica has no institutionalised mechanisms to co-ordinate national policy decisions with local government associations (OECD, 2021[4]).

As in many countries, local governments handle a wide range of environment-related matters, including urban planning, housing and waste collection. In 2019, they accounted for 57% of spending on environmental protection (Section 2.6). The 2001 constitutional reform formally allocated more powers and budget to subnational governments. According to the reform, municipalities should receive at least 10% of the central government’s budget to finance the delegated functions. However, the reform has suffered severe delays and is far from complete. This implies that subnational authorities have still limited budget and implementation capacity (OECD, 2021[4]). Most local governments struggle to collect taxes and service fees, including fees for waste management, street cleaning, lighting and commercial allotments. Revenue from these taxes and fees barely covers human resource costs.

The quality and delivery of environment-related services vary greatly across municipalities and regions. In addition to accelerating implementation of the constitutional reform, Costa Rica could consider establishing a system to redistribute fiscal resources across regions to reduce these disparities (OECD, 2021[4]). Eleven federations of local governments provide technical support to the associated municipalities. There are also examples of co-operation between local governments and stakeholders such as businesses and non-governmental organisations to improve service delivery. However, there is a need to provide nationwide guidance, support and training to local governments to improve their capacity to carry out their environment-related responsibilities.

Costa Rica’s legislation does not allow municipalities to create inter-municipal structures or shared service arrangements to pool resources and provide services to a wider population. Such legislative barriers should be removed. The experience of other OECD countries shows that sharing arrangements allow better services at lower costs through economies of scale (OECD, 2019[6]). For example, French municipalities can create a “community” and delegate to it certain responsibilities or services. A similar experience in Chile has helped improve the quality of waste collection and treatment services in a province (Box 2.2).

Costa Rica’s only example of inter-municipal association is the Metropolitan Federation of Municipalities of San José, which promotes co‑operation for spatial planning among the capital of San José and its nine neighbouring municipalities. The Greater Metropolitan Area (GAM) around San José comprises 31 municipalities, including the country’s four largest cities (San José, Alajuela, Cartago and Heredia). It is home to 73% of the country’s population. The GAM is a geographical designation used for spatial planning, but there is no metropolitan structure to co‑ordinate management of public urban services such as public transport and waste management (Chapter 1).

2.2.4. Public participation in environmental decision making

Costa Rica has made remarkable progress in implementing the open government principles of transparency, accountability and participation. Its legal and institutional frameworks for open government are on par with OECD standards (OECD, 2021[4]). The National Constitution grants rights to participation, petition and access to information of public interest.

Box 2.2. A consortium of municipalities for managing waste in Chile

The Association of Municipalities of the Province of Llanquihue for Sustainable Waste Management and Environmental Management conglomerates all the municipalities of Llanquihue to jointly manage solid waste while optimising use of resources. An executive secretary and technical unit are in charge of administration. A technical committee gathers professionals from participating municipalities to co‑ordinate and carry out waste management activities.

The association helped overcome decades of poor waste management by individual municipalities working separately. Municipalities did not have the appropriate resources or capacity to manage waste efficiently, from collection to disposal. The association has subsequently expanded its activities into recycling and capacity.

The association has been operating since 2016. Despite its effectiveness in managing waste, the association depends on the fees paid by participating municipalities – and thus on political will. This makes its financing unstable and jeopardises the quality of the service.

Source: OECD (2017), Making Decentralisation Work in Chile: Towards Stronger Municipalities, OECD Multi-level Governance Studies, OECD Publishing, Paris, https://doi.org/10.1787/9789264279049-en.

Public participation and consultation of Indigenous Peoples are required by law for the formulation of several public policies and environmental decision-making processes. These include the environmental impact assessment (EIA) procedures of projects and activities, as well as, to a lesser extent, for strategic environmental assessment (SEA) of land-use plans (Section 2.3.2). Several mechanisms for public participation are in place. These range from making documents open to public for comments to organising public hearings or establishing special bodies to ensure public engagement. For example, the National Biodiversity Management Commission (Box 2.1) set up a plenary committee to promote participation of stakeholders in policy formulation and implementation.4 Another example is the Citizen Advisory Council on Climate Change, which was established in 2017 to inform the design, application and evaluation of climate policies.

The government has made efforts to better involve indigenous communities in the policy process. Government institutions are required to consult Indigenous Peoples before implementing policies, measures and projects that can potentially affect their communities. In 2018, the government introduced the General Mechanism for Consultation of Indigenous Peoples to implement its obligation to consult. The mechanism was used to update the National Water Policy and the National Plan for the Integrated Management of Water Resources, among others. The Network of the Indigenous Bribri-Cabecar Communities was founded in 2005 to strengthen the participation of these communities, improving their living conditions and their institutional leverage. The network has also been useful to encourage Indigenous Peoples to fight for their right to land use, while respecting their traditions (OECD, 2021[4]).

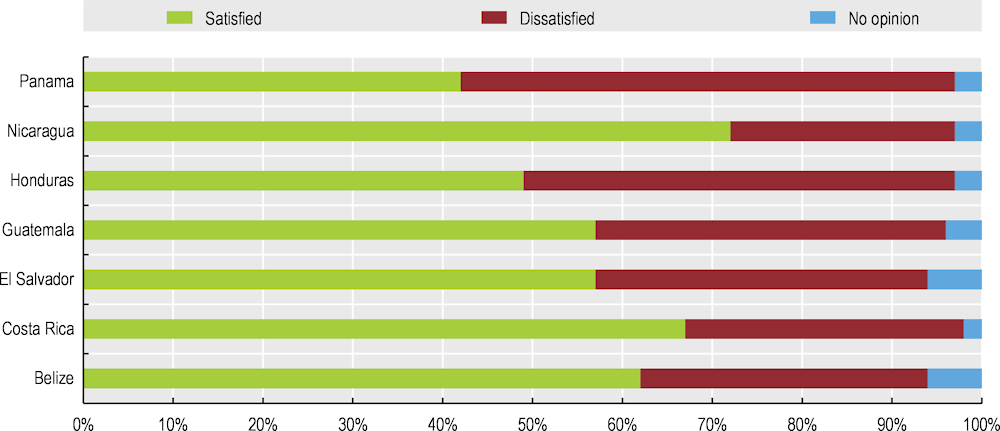

Despite an advanced framework for encouraging public participation in policy making, active engagement of citizens and civil society organisations remains limited and trust in government is relatively low (OECD, 2023[1]; OECD, 2021[4]). Nonetheless, citizens’ support for environmental policies has remained above 50% since 2010 (Gallup, 2022[7]). The population shows a high degree of satisfaction (67%) with the country’s efforts in protecting the environment – the second highest level in Central America (Figure 2.1). In a 2019 opinion poll, respondents identified insufficient public transport and inadequate waste management as the top two obstacles on Costa Rica’s decarbonisation path. These are followed by traffic congestion and pollution, insufficient incentives for the clean energy transition, and inadequate land management and deforestation (Ministerio de Comunicaciones, 2019[8]).

Figure 2.1. Most people in Costa Rica are satisfied with its environmental protection efforts

Note: Question: “In this country, are you satisfied or dissatisfied with efforts to preserve the environment?”

Source: (Gallup, 2022[7]).

Costa Rica has taken important steps in improving availability of environmental information. The National Environmental Information System (SINIA) was established in 2013 to co‑ordinate the collection of environmental statistics and disseminate them through a single web repository. The National System of Climate Change Metrics (SINAMECC), established in 2018, is a parallel platform for information related to climate change. Both systems are led by MINAE and are part of the National Statistics System. The Central Bank of Costa Rica (BCCR) produces the environmental accounts of water, forests, materials and energy, and surveys environmental spending of businesses (Section 2.7). More work is needed to extend the coverage of SINIA, as much information is still scattered across ministries, their subsidiary entities and other autonomous bodies. In addition to government institutions, the National Council of Rectors (CONARE), a consortium of the country’s five public universities, maintains publicly available databases. It releases annual reports as part of its research initiative on sustainable human development (Programa Estado de la Nación).

However, many data are not produced systematically and are outdated. The first and last state of the environment report was released in 2017. Work is progressing to update the report, as well as to implement a pollution release and transfer registry. Important information gaps persist, including on greenhouse gas (GHG) emissions, air and water quality, and waste (Chapter 1), as well as the oceans (Chapter 3). These gaps impede evidence-based decision making and informed citizen engagement. Increased funding, deployment of Earth observation technologies and enhanced collaboration with the scientific community would help improve production, collection and dissemination of environmental statistics as part of the SINIA.

2.3. Setting sound environmental requirements and ensuring their fulfilment

2.3.1. Environmental policy and legal framework

Costa Rica has a long-standing environmental policy framework based on its 1949 National Constitution and an extensive legislation. Article 50 of the Constitution recognises citizens’ right to a healthy and ecologically balanced environment. In 2020, Article 50 was reformed to define access to safe drinking water as a basic and inalienable human right. Costa Rica’s environmental legislation includes one overarching law (the 1995 Organic Law on the Environment) and several thematic laws, resulting in more than 275 environmental laws. The Organic Law on the Environment aims to prevent and minimise adverse environmental impacts and sets the framework for environmental permitting, including EIA and compliance assurance (Sections 2.3.2 and 2.3.3).

Costa Rica’s environmental legal framework is largely in line with requirements set by OECD legal instruments in the environmental field (OECD, 2019[9]). It has continued to evolve in recent years. Indeed, in 2021 and 2022, 153 new environmental provisions were approved, more than the average of the five previous years. Most of the new environmental regulations were dedicated to biodiversity and protected areas and needed to implement previously adopted provisions. As of June 2021, Costa Rica had signed and ratified over 51 international environmental agreements. However, many policy goals and objectives do not translate into concrete measures and adequate financing (CONARE, 2022[2]). Many regulations lack adequate implementation and enforcement.

2.3.2. Environmental impact assessment and permitting

In line with OECD standards, an EIA is required for any activity, work or project that entails risks of adverse impacts on the environment. The National Environmental Technical Secretariat (SETENA) manages the EIA procedure and issues the corresponding Environmental Viability or Licence (Viabilidad (Licencia) Ambiental, VLA). A VLA is a pre-condition for obtaining construction, operating and several sector-specific permits. These include a wastewater discharge permit from the Water Directorate of MINAE and a Sanitary Operating Permit (PSF) from MINSA.5 Since 2006, land-use plans (including Cantonal Regulatory Plans) are subject to an SEA with a view to obtaining a VLA.

The EIA process differs according to the potential impact of the activity, with stricter requirements for activities with a potentially high or moderate-high environmental impact (Box 2.3). Following the EIA, and depending on its results, SETENA issues the VLA. The VLA sets out environmental requirements for activities or projects. However, these conditions could better reflect the implementation of Best Available Techniques (BAT).6 All documents produced as part of the EIA process are open to the public, and the public has the possibility of being actively involved in the process (Box 2.3). Municipalities can conduct public hearings for the environmental assessment of land-use plans.

In line with good international practice, a financial mechanism is in place to guarantee that the conditions set in the VLA are met (Box 2.3). However, evidence suggests that financial deposits are often returned to developers even when their mitigation and compensatory actions did not offset the potential environmental loss (Bonilla-Murillo et al., 2022[10]). These financial guarantees could be used more effectively to ensure compliance of activities with the VLA requirements, as well as the execution of compensatory measures that respect the ecological equivalence principle. As in other countries, the overall effectiveness of the assessment process can be strengthened. Some weaknesses in SETENA’s governance and procedures negatively affect the quality of its EIA (CGR, 2022[11]). A 2023 regulation aims to streamline the EIA and VLA issuance processes and make them more efficient.

In 2022, Costa Rica launched a comprehensive reform to streamline the now cumbersome system of government approvals and reduce the regulatory burden on businesses. Integrated environmental permits will be part of the “Single Window of Investment” (Ventanilla unica de inversion, VUI), a paperless one-stop shop for permits. This reform is based on the concept of regulatory differentiation, whereby activities with a low level of environmental risk warrant simpler applications. Environmental inspections will also be integrated. This would align Costa Rica with the OECD standards on integrated pollution prevention and control.

Box 2.3. The Environmental Impact Assessment process in Costa Rica

The EIA process starts with a preliminary assessment, during which activities with a potentially high or moderate-high environmental impact are subject to a formal scoring process. Conversely, activities with a potentially moderate-low and low impact need only submit a simplified application (the classification of activities according to their potential environmental impact is contained in a 2004 executive decree). The formal scoring reflects the size of potential impact and determines the type of document the developer would have to submit: a declaration or a full environmental impact study with an environmental management plan. The environmental impact study must also include an analysis of alternatives. SETENA may conduct on-site inspections prior to EIA approval.

Anyone can consult the documents produced as part of the EIA process, either at the offices of SETENA or on its website. The developer must engage with the local population if the activity is likely to generate social tensions or affect indigenous communities. The public can request to be a party to the EIA procedure (and be notified of its every step) and comment on the developer’s submissions in writing, in a meeting with SETENA technical staff or in a public hearing. Any natural or legal person can initiate a public hearing, but SETENA decides whether to proceed. It bases its decision on several criteria: perceived information gaps regarding the project, its high environmental impact or social implications, or lack of appropriate public consultation by other means. Public hearings are uncommon, primarily because they are seldom requested.

Upon receiving a VLA, the project developer must deposit a financial environmental guarantee of up to 1% of the amount of project investment (the guarantee is higher for mining and hydropower projects). SETENA can use the guarantee to recover remediation costs in case of environmental damage. To get the deposit back, the developer must implement the measures prescribed in the VLA to mitigate or compensate for environmental impacts and request the closure of the project.

Source: Country’s submission.

2.3.3. Compliance monitoring and enforcement

The Environmental Comptroller within MINAE has broad supervisory functions over compliance with environmental legislation (Box 2.1). Each authority (SETENA, MINSA, SINAC, municipalities and others) inspects compliance with the laws, decrees and permits under its competence.7 However, in practice, most on-site inspections react to incidents or public complaints to the competent authority.

Costa Rica has encouraged citizens to help monitor compliance. The Environmental Comptroller operates the Integrated System of Procedures and Consideration of Environmental Complaints for receiving and handling signals on non-compliance from the public (Box 2.4). It also maintains the registry of the Natural Resources Surveillance Committees (COVIRENAs). Defined by a 2016 decree, COVIRENAs are civil society organisations of volunteer environmental inspectors. They collaborate with public employees to enforce environmental legislation and protection of natural resources. In 2021, there were 40 registered committees and 294 volunteer inspectors.

Box 2.4. An integrated system to submit and handle environmental complaints

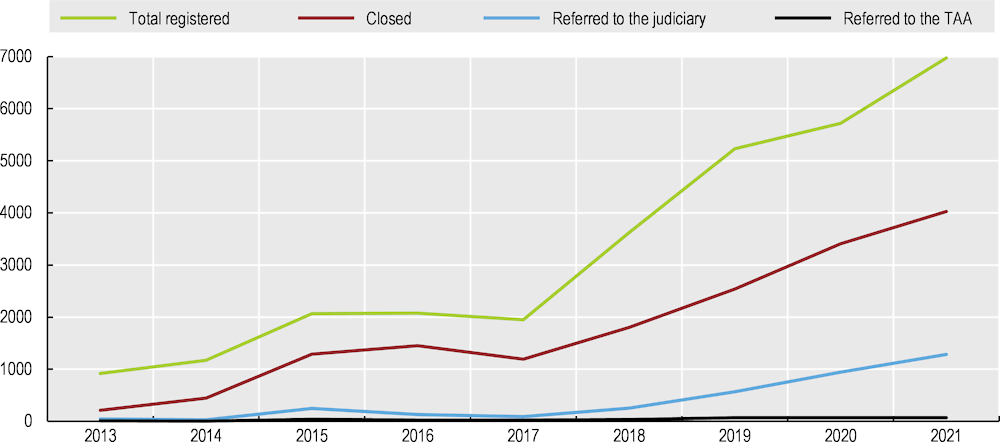

The Integrated System of Procedures and Consideration of Environmental Complaints (SITADA) is the official system to submit a complaint against suspected environmental non-compliance and to follow up the complaint as it moves through the system. Every citizen can access the system. The Environmental Comptroller issues an annual report based on the SITADA data, which it disseminates to the press and publishes on its website. In 2021, SITADA received 6 977 complaints, more than three times the number from 2017 (Figure 2.2). In 2021, almost half of the complaints concerned forests, followed by those related to biodiversity loss and water pollution. Over 30% related to illegal logging and/or harvesting, followed by referrals of wild animals in danger, encroachment on protected water bodies and illegal possession of wild animals.

When an environmental complaint or referral is entered into the system, the competent agency is required to follow up through on-site inspections and an investigation report. Over the years, SINAC has handled the most complaints of any government agency; indeed, in 2021, it handled more than 5 000 complaints, or more than 70% of all referred cases in SITADA. The competent authority verifies compliance with environmental regulations for each complaint. When non-compliance is detected, the complaint is referred to the judiciary, the Environmental Administration Tribunal (TAA), the National Mining Registry or the Plenary of SETENA. In 2021, 58% of complaints were closed without consequences, 18% were brought before the judiciary and 1% went before the TAA (Figure 2.2).

Source: MINAE (2021), Sistema Integrado de Trámite y Atención de Denuncias Ambientales (SITADA), Estadísticas 2021, MINAE Contraloría Ambiental, San José, https://contraloriaambiental.go.cr/doc_/doc_1644441660.pdf.

Implementing risk-based planning for environmental inspections would make compliance monitoring more efficient and reduce its reliance on environmental complaints. Complaints have increased steadily since 2017, but most of them are closed without consequences (Figure 2.2). This raises the concern that many complaints may be unsubstantiated but still require authorities to investigate. This, coupled with a general understaffing of competent authorities, may lead to clogging the environmental enforcement system. More generally, there is room to better support the regulated community fulfil its environmental requirements by providing technical assistance and information on best practices. Similar compliance promotion activities would help reduce the compliance monitoring workload on authorities, while improving the environmental conformity of regulated activities.

When non-compliance is detected, complaints or referrals from inspecting authorities are transmitted to the Environmental Administrative Tribunal (TAA) and/or the judiciary for criminal enforcement. The TAA can prescribe precautionary measures and issue compliance orders. It can impose administrative sanctions, including temporary or permanent cancellation of permits, closure of premises and companies, fines and compensation for environmental damage. If a compliance order is not implemented in a specified timeframe, the TAA may refer the case to the Environmental Prosecutor’s Office for criminal enforcement. The administrative and criminal enforcement processes can run in parallel.

Environmental damage is assessed by competent authorities such as the Directorate of Geology and Mines or the MINAE Water Directorate, MINSA or municipalities, with results presented to the TAA. Compensatory payments are channelled to the treasury and do not contribute directly to remediation of environmental damage. The same authorities calculate fines in relation to the estimated value of environmental damage but not to the benefits of the operator from non-compliance. There are no levels or intervals for administrative fines defined in the legislation. According to international best practices, fines should reflect the gravity of the offence to be an effective deterrent. Moreover, fines should recover the economic benefits to the operator from non-compliance. Revenues from fines are channelled to MINSA or to the municipality where the offence occurred rather than the general state budget. This, however, can generate perverse incentives and conflicts of interest.

Figure 2.2. The number of environmental complaints has increased

Source: MINAE (2021), Sistema Integrado de Trámite y Atención de Denuncias Ambientales (SITADA), Estadísticas 2021, MINAE Contraloría Ambiental, San José, https://contraloriaambiental.go.cr/doc_/doc_1644441660.pdf.

The number of TAA staff is largely insufficient to cope with the increasing number and complexity of complaints. A backlog of cases has accumulated over time. As of 2011, each of the 11 lawyers of the tribunal was responsible for about 455 cases. As a result, the time to conclude each case has grown well over one year.

2.3.4. Access to justice in environmental matters

Every person has legal standing to denounce any acts that may violate the constitutional right to a healthy and ecologically balanced environment and to safe drinking water. Every citizen can file a complaint for suspected non-compliance with environmental provisions and claim compensation for the resulting damage (Box 2.4).

Access to remedy for environmental impacts can also be sought through the country’s Ombudsperson (Defensoría de los Habitantes de la República or DHR). The DHR can investigate actions and omissions by public entities, as well as by public and private companies providing public services, that contravene environmental laws. It can then issue recommendations with a view to protecting environmental rights effectively. For example, the DHR monitors the inter-institutional process for improving the registration of agrochemicals. It also monitors government measures to eliminate the use of mercury in artisanal and small-scale gold mining activities in compliance with the Minamata Convention. The DHR has often intervened to require both the Costa Rican Institute of Aqueducts and Sewers (Box 2.1) and the municipal aqueducts to upgrade and extend water infrastructure to improve access to safe water and sanitation (DHR, 2022[12]) (Chapter 1).

In line with its environmental democracy tradition, Costa Rica was one of the promoters of the Regional Agreement on Access to Information, Public Participation and Justice in Environmental Matters in Latin America and the Caribbean (Escazú Agreement). The agreement is modelled after the Aarhus Convention of the United Nations Economic Commission for Europe. It is the first international agreement that includes binding provisions on protecting human rights defenders in environmental matters. The agreement entered into force in April 2021; at the time of writing, 14 of 25 signatory countries had ratified the agreement.

Costa Rica has taken several measures to protect environmental human right defenders and Indigenous Peoples but has not ratified the Escazú Agreement. As recommended by OECD (2023[13]), “Costa Rica could consider the possibility of taking steps towards the ratification of the Escazú Agreement”. This ratification would further consolidate the country’s significant efforts to build an advanced legal framework to manage the environment and guarantee environmental democracy.

2.4. Greening the system of taxes and charges

2.4.1. Towards a green tax reform

Costa Rica’s level of taxation is in line with regional peers but lower than in most OECD countries. This is due to a large share of informal employment, high tax evasion, narrow tax bases and various tax expenditures. Total tax revenues were about 23% of GDP in 2020, compared to the OECD average of 33%. The tax system has a weak redistributive performance and relies on high social security contributions, which favour informality (OECD, 2023[1]).

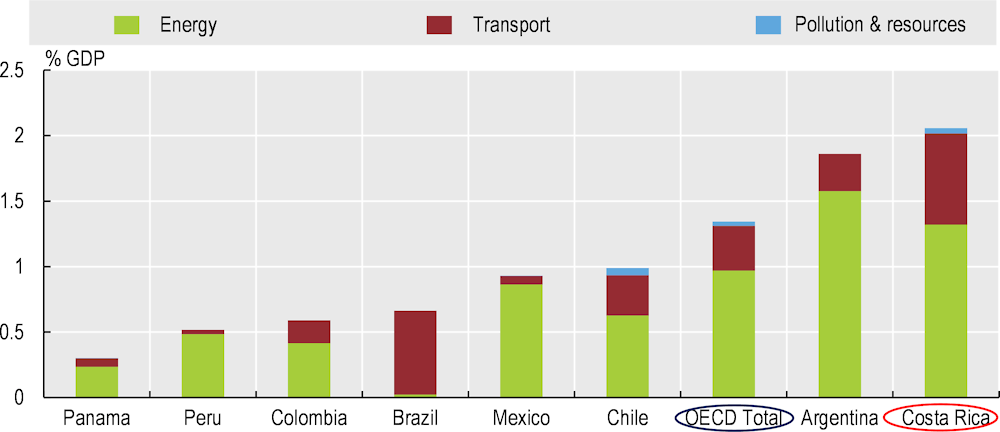

Environment-related taxes are an important source of fiscal revenue in Costa Rica. On average, they accounted for about 10% of total tax revenue and 2.3% of GDP in 2010-21, above the 2010-21 averages in the OECD (6.8% and 2.2%). These shares were also higher than in other major Latin American countries (Figure 2.3). Most receipts come from the excise duty on fuels and, to a lesser extent, from vehicle taxes. Taxes on pollution and resource management mainly apply to wastewater discharges and water use (Chapter 1) and generate limited revenue (Figure 2.3).

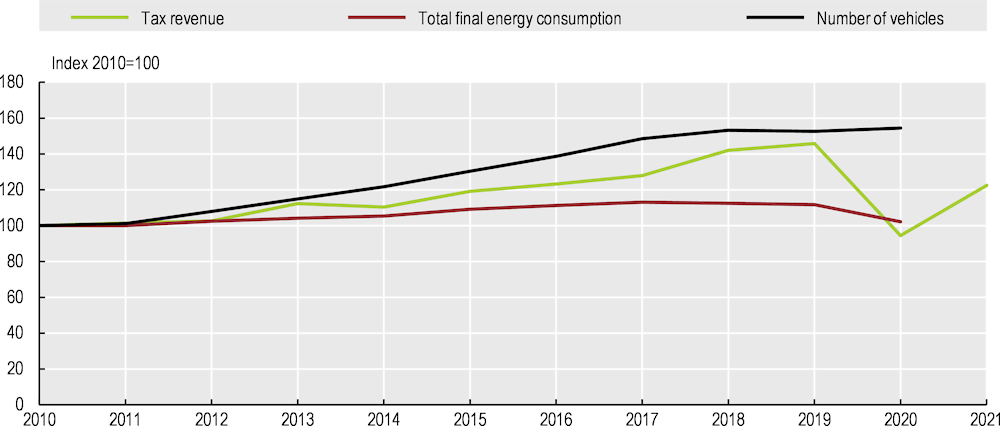

Revenue increased steadily and strongly (by over 30% in real terms) between 2010 and 2021. This increase was in line with a rising number of vehicles on the roads and higher fuel consumption (except in 2020, at the peak of the COVID-19 pandemic) (Figure 2.4). Proceeds from environment-related taxes are partly earmarked for environmental purposes. In particular, 3.5% of the fuel excise duty revenue is allocated to the National Forestry Financing Fund for the Programme of Payments for Environmental Services (PPSA) and represents 90% of the PPSA funding. A quarter of the proceeds from the Water Utilisation Levy are earmarked for the PPSA and another 25% is allocated to SINAC (Chapter 3).

When considering the value added tax (VAT) and custom duties on vehicles and VAT on fuels, the tax revenue linked to vehicle ownership and use reaches 20% of total tax revenue, according to Ministry of Finance estimates. These revenues are expected to decline by, on average, 0.4% of GDP per year in 2023-50. This is in keeping with implementation of the PND 2018-50, which anticipates the electrification of vehicles and a shift to public transport and active mobility (Chapter 1). A tax reform should become operative by 2030 to eliminate the fiscal impact of transport decarbonisation, if PND plans proceed (Victor‑Gallardo et al., 2022[14]). The expected decline in fuel tax revenue will also reduce funds available for environmental activities, and primarily for implementation of the PPSA. It is, therefore, urgent to delink the PPSA from fuel tax revenue (Chapter 3).

Figure 2.3. Environment-related taxes are an important source of fiscal revenue in Costa Rica

Note: OECD weighted average in 2020.

Source: OECD (2022), “Environmental Policy: Environmentally related tax revenue”, OECD Environment Statistics (database).

Figure 2.4. Revenue from environment-related taxes grew in line with fuel use and vehicle fleet

Note: The number of vehicles corresponds to those paying the right of circulation in the country.

Source: CONARE (2021), Programa Estado de la Nación (database); IEA (2023), "World energy statistics", IEA World Energy Statistics and Balances (database). OECD (2022), “Environmental Policy: Environmentally related tax revenue”, OECD Environment Statistics (database).

The PND mandates the Ministry of Finance, in collaboration with MINAE, to design a green tax reform to find alternative sources of tax proceeds to offset the revenue loss from vehicle and fuel taxes. The PND foresees progressive elimination of fossil fuel subsidies and introduction of a carbon pricing scheme. These intentions are welcome. As discussed in the following sections, the fuel and vehicle taxes should be redesigned to encourage a shift towards cleaner vehicles, public transport and active mobility. In the longer term, a shift from taxation of energy use to the taxation of road use will be needed to ensure a sustained revenue stream (van Dender, 2019[15]). There is also room to introduce taxes on resource use and pollution. These taxes could target chemical fertilisers and pesticides, which are intensively used (Chapter 3), as well as landfilled waste and plastic bags or other plastic products, with a view to improving waste management and reduce plastic pollution (Chapter 1).

The green tax reform should also aim to reduce tax avoidance and make the tax mix more progressive and conducive to creating jobs and moving towards a more formal economy by, for example, reducing social security contributions. Gradually introducing a comprehensive package of tax measures will help smooth the costs of reform across sectors and over time. The package should include relatively low tax hikes but spread across several taxed products such as fuel, vehicles and electricity (Victor‑Gallardo et al., 2022[14]). Part of the revenues from new or increased environment-related taxes and subsidy removal should be used in a well-targeted way to reduce the impact on low-income households and most affected economic sectors. This would improve social acceptability of the reforms. Part of the revenue could also be used to finance low-carbon investment and other environment-related actions, such as the PPSA. As revenue earmarking can reduce efficiency of public spending, such arrangements should be clearly communicated and periodically reassessed in a transparent way (Marten and van Dender, 2019[16]).

2.4.2. Energy taxes and carbon pricing

Since 2001, Costa Rica has applied an excise duty on fuels (the Single Tax on Fuels or IUSC) and electricity. The rates vary with fuel products, irrespective of the energy or carbon content of the fuels. They are updated quarterly to the consumer price index (CPI) with a maximum 3% increase per quarter.

Road fuel prices and taxes do not fully reflect the social costs of fuel use, including costs associated with emissions of GHGs and local air pollutants, accidents and congestion (Parry, Black and Vernon, 2021[17]). The energy tax on diesel is 57% that on petrol, despite the higher carbon content per litre of diesel and higher emissions of local pollutants from diesel vehicles. This diesel tax discount is common to most other OECD and Latin American countries but remains unjustified on environmental grounds (OECD, 2022[18]). Gradually increasing the IUSC rate on diesel to at least match that on petrol would encourage a shift towards cleaner vehicles, especially in the freight sector where diesel is most used. Some types of fuels and some sectors benefit from preferential tax treatments and other forms of price support that reduce the incentive for energy savings (Section 2.5.2).

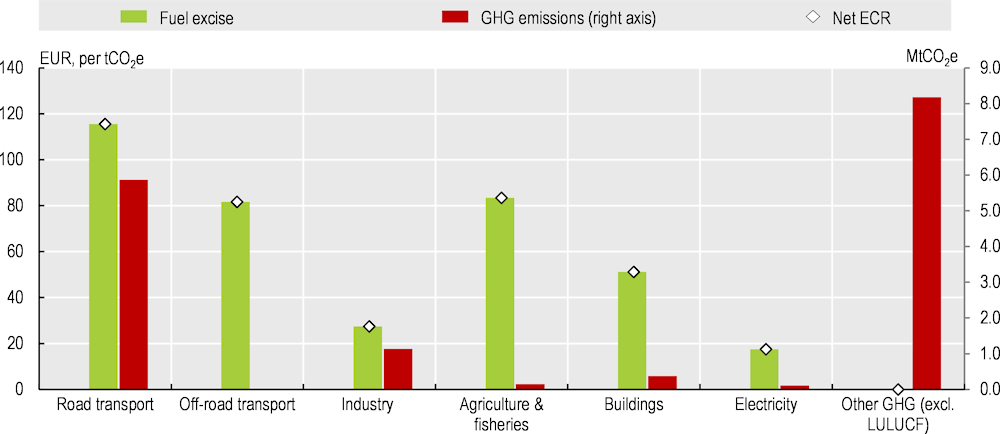

Fuel excise taxes are the only way GHG emissions are priced in Costa Rica. There is no carbon tax or emissions trading system in place. Therefore, in 2021, the net effective carbon rates (ECR) coincided with the fuel excise taxes net of pre-tax fossil fuel subsidies.8 Costa Rica priced 46% of its GHG emissions. While this is below the OECD average of 68%, it is among the highest shares in Latin America and the Caribbean (LAC) (Figure 7 in Assessment and recommendations). Nearly 40% of the country’s GHG emissions are priced at a net ECR above EUR 60 per tonnes of carbon dioxide (CO2), which is the midpoint estimate of climate damage caused by each tonne of CO2 emitted in 2020. This is a higher share than in the OECD and most LAC countries (Figure 7 in Assessment and recommendations).

In 2021, the economy-wide net ECR was nearly EUR 47 tCO2, or three-quarters the OECD average. As in all countries, net ECRs vary by sector and by fuels (Figure 2.5). In 2021, the average net ECR in the non‑road transport sectors was aligned with the OECD average. Meanwhile, the average net ECR on road transport fuels was nearly EUR 116 tCO2 or just two-thirds the OECD average. Nonetheless, net ECRs on road fuels are the highest among the major LAC economies. Virtually all CO2 emissions from road transport are priced above the EUR 60 benchmark in Costa Rica, as well as all emissions from off‑road transport and most CO2 emissions from energy use in agriculture. However, all emissions of GHGs other than CO2 (mostly methane and nitrous oxide) are not priced at all (Figure 2.5). No emissions are priced at or above EUR 120 tCO2, a midrange estimate of carbon costs in 2030 (OECD, 2022[18]).

Figure 2.5. Carbon prices are highest for road transport and zero on non-energy-related emissions

Note: In Costa Rica, the Effective Carbon Rate (ECR) coincides with fuel excise taxes. The Net ECR is the ECR minus fossil fuel subsidies that decrease pre-tax fossil fuel prices.

Source: OECD (2022), Pricing Greenhouse Gas Emissions: Turning Climate Targets into Climate Action, OECD Series on Carbon Pricing and Energy Taxation, OECD Publishing, Paris.

Costa Rica should follow through with a carbon pricing scheme as foreseen by the PND 2018-50. This could take the form of a carbon tax element of the fuel excise levy. Its rate could be set at a low level and gradually raised according to a pre-determined schedule. A credible path of future carbon prices would provide an incentive for low-carbon consumption and investment without immediately imposing the burden on households and firms at times of high cost of living. OECD (2022[18]) estimates that introducing a carbon tax of EUR 120 tCO2 would yield revenue equal to 0.3% of GDP. This compares with the expected revenue decline due to transport decarbonisation of 0.4% of GDP in Victor-Gallardo (2022[14]) (Section 2.4.1). Even if the carbon tax revenue will decrease over time with decarbonisation of the economy, it can help finance the adjustment costs at the start of the transition. Part of the carbon tax revenue should be used to alleviate the impact of higher energy prices on low-income households. In many countries, transferring a third of the additional revenues to poor households through means-tested benefits is sufficient to mitigate energy affordability risk (Flues and van Dender, 2017[19]). Compensation through preferential tax rates should be avoided as it undermines the incentive of carbon pricing.

2.4.3. Vehicle taxes and road charging

There is scope to improve the design of vehicle taxes to encourage a shift to more energy-efficient and less polluting vehicles. The annual vehicle tax applies the same rate, regardless of fuel consumption capacity or emission levels. It is levied as a percentage on the fiscal value of vehicles, with the rate depending on the model of the vehicle. The fiscal value is adjusted annually for inflation but reduced by 10% for depreciation every year. Inflation has been consistently below 10% since 2009, which implies that the tax amount declines with the vehicle age (Rodríguez-Garro, 2020[20]). This system favours old and potentially less safe and more polluting vehicles. This distortion needs to be eliminated. At a minimum, the annual depreciation rate should be reduced and adjusted to the average useful life of vehicles, which is above ten years (Rodríguez-Garro, 2020[20]).

Electric vehicles (EVs) and their spare parts benefit from several tax exemptions (general sales tax, selective consumption tax and customs value tax). In 2020, these exemptions amounted to CRC 365 million (about USD 650 000) (Ministerio de Hacienda, 2021[21]). EVs also benefit from other incentives such as green plates and free parking spaces. These incentives have encouraged a rapid increase in EV sales in the last few years (Figure 4 in Assessment and Recommendations). However, the number of EVs still represented 0.5% of the vehicle fleet in 2021. The PND 2018-50 aims to achieve 30% of EVs in the light vehicle fleet (including cars) by 2035 (Chapter 1).

As the country’s EV market matures, purchase subsidies should be phased out (IEA, 2022[22]). These subsidies should be accompanied and progressively replaced by higher taxation of internal combustion engine vehicles (ICEVs). This should aim to reduce the difference in purchase price or lifetime cost between EVs and ICEVs. Costa Rica should revise vehicle taxes and modulate them according to the vehicles’ fuel efficiency and levels of local pollutant emissions. Adding a weight element would help address road wear and associated particulate pollution. Vehicle taxes should be combined with more stringent emission standards (Chapter 1). The government should reconsider its decision of delaying from 2023 to 2027 the entry into force of Euro 6 or Tier 3 standards.9 This postponement aimed to contain rising energy prices, as the stricter vehicle standards would entail the import of more expensive fuels (Section 2.5.2).

As EVs become widespread, Costa Rica will eventually need comprehensive road use charging to internalise costs of car use and substitute transport fuel tax revenues (van Dender, 2019[15]). Road tolls finance road developments but have not been updated since 2002. As a first step, as suggested by OECD (2023[1]), the government should raise road tolls to reflect the cost of road use as soon as inflationary pressures abate. Looking ahead, Costa Rica would benefit from developing a distance-based road pricing system. This would apply different rates depending on the location and time of the driving and the emission performance of vehicles. This, in turn, would allow to reflect the different externalities (air pollution, road wear and tear, accidents, etc.) of driving.

Costa Rica could explore the introduction of congestion charges, potentially in combination with low-emission zones, to address congestion and air pollution in urban areas. In 2017, the social costs of transport in the GAM were estimated at USD 3.1 billion (or about 5% of GDP), more than 90% of which linked to accidents and road congestion (CONARE, 2018[23]). Driving restrictions based on licence plates have long been in place to manage entry of cars and vans into San José city centre during weekdays from 6:00 am to 7:00 pm.10 Cars with four travellers and EVs are exempted, as are heavy goods vehicles. This measure has largely been ineffective because many households own more than one car, which allows them to circumvent the restriction. The experience of other countries shows this kind of traffic regulation can also have perverse effects, such as shifting congestion outside the restricted areas and hours and stimulating the purchase of second-hand vehicles (Blackman, Li and Liu, 2018[24]).

Implementing congestion charges would help curb peak-time congestion in a cost-effective and socially fair manner. As in other middle-income countries, cars are used by the most affluent people while low-income households tend to use public transport (CONARE, 2020[25]). By increasing driving costs, congestion charges discourage trips that are less necessary or that can be made at less congested periods, thereby reducing traffic. Travel conditions improve for drivers that pay the charge, as well as for buses. Revenue from the charges could fund a much-needed integrated public transport system in the GAM, together with walking and cycling infrastructure (Chapter 1). The GAM could consider the example of Bogotá, which added a charge to its long-standing plate-based traffic restriction (Pico y Placa).11 A pilot charging system and effective communication campaigns could help showcase the benefits of the system and gain citizens’ support (OECD, 2021[26]).

2.5. Removing subsidies with potentially negative environmental consequences

2.5.1. A stocktaking of environmentally harmful support

In 2021, the Ministry of Finance categorised tax expenditures (i.e. tax revenue forgone due to exemptions, discounts and other forms of preferential tax treatment) according to their environmental impact. It estimated that environmentally harmful tax expenditure amounted to nearly CRC 88 billion (USD 150.45 million) or 0.24% of GDP in 2020. More than 70% of this revenue loss was for tax discounts and exemptions on machinery and other inputs for agriculture and fishing (Chapter 3). Agricultural inputs, such as fertilisers and pesticides, have long benefited from a total sales tax exemption. In 2018, this was replaced by a reduced VAT rate of 1% (compared to the standard rate of 13%). The remaining part of environmentally harmful tax expenditure was linked to fossil fuel support, which also includes direct transfers (Section 2.5.2). In comparison, tax expenditures with positive environmental impact were negligible, amounting to about CRC 3 billion (USD 5.13 million) (Ministerio de Hacienda, 2021[21]).

Costa Rica should build on the Ministry of Finance’s stocktaking of tax expenditure to develop a plan to phase out environmentally harmful subsidies, including support to energy use and agriculture (Chapter 3). The stocktaking should be completed with the identification of direct subsidies, in addition to tax expenditure, and an evaluation of the economic, social and environmental effects of support measures. Such evaluation is key to prioritise the support measures that need reform.

Any subsidy reform plan should also assess its distributional implications. It should propose alternative measures to achieve the same policy objectives more cost effectively and with better environmental or social outcomes (Elgouacem, 2020[27]). Alternative policies include means-tested cash transfers, investment in public services or general support for the competitiveness and innovation of the affected economic sectors. Such an approach would help minimise adverse impacts of subsidy reform and, in turn, reduce the risk of political backlash and backtracking.

2.5.2. Fossil fuel subsidies

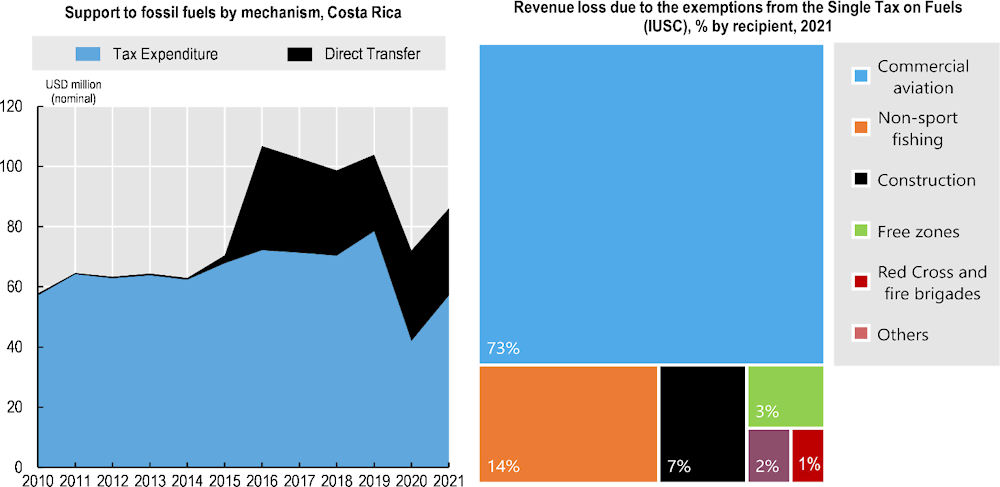

Fossil fuel support amounted to USD 86 million, or about 0.13% of GDP in 2021 (OECD, 2023[28]). This is a lower amount than in regional peers and many other OECD countries. That said, international comparisons are only indicative due to the estimation methodology and data collection. Support is nearly exclusively linked to the use of petroleum products. Two-thirds of support is provided through tax expenditure (Figure 2.6). Exemptions from the IUSC excise duty is the main form of support, accounting for 65% of all support to fossil fuels in 2021. These exemptions benefit mainly fuels used in commercial aviation and the fishing fleet (Figure 2.6). A price discount on liquefied petroleum gas (LPG) is the second largest form of support, accounting for 26% of support to fossil fuels. The cost of the LPG price discount is recovered through the prices of other fuels, mainly petrol and diesel. This mechanism was introduced in 2016 and led to a hike in budgetary transfers to fossil fuels that year and in the following years. Revenue loss due to tax relief increased in the last decade in line with increased fuel use in aviation, except for the pandemic-related drop in 2020 (Figure 2.6). Nearly all forms of support benefit end-users of fuels.

In 2022, in response to rising energy prices and inflation, the government introduced some measures to contain the energy price hikes. These measures will likely translate into higher fossil fuel support. In particular, the government more than halved the IUSC tax rate on LPG for six years, thereby lowering its price by 7.5%. This measure targets low-income households, who are the main users of LPG for cooking and heating. It also aims to support the recovery of the pandemic-stricken services sector, in particular tourism and leisure-related activities. The government took measures also on other fuels: it froze the quarterly adjustment of the IUSC to the CPI for six months; it introduced a temporary cross-subsidy benefiting diesel, which is mostly used in freight, agriculture and shipping; and ended a cross-subsidy for bitumen. As this subsidy was paid for by higher taxes on petrol and diesel, its elimination helped contain the prices of road fuels. Overall, these measures reduced the prices of diesel and petrol by less than 1%. They were less costly and less regressive than in regional peers, with a fiscal cost of only 0.02% of GDP (Garcimartín and Roca, 2022[29]). Nonetheless, measures to cap energy prices tend to discourage energy savings.

Figure 2.6. Government support to fossil fuels grew in the last decade

Note: Fossil fuel support figures are provided on a “best estimate” basis, as several subsidies and broader support measures may not be completely quantified or the complete set of fossil fuel support measures may not have been exhaustively identified.

Source: Ministerio de Hacienda de Costa Rica; OECD (2022), Inventory of Fossil Fuel Support Measures (database).

The government also introduced a temporary subsidy targeted at low-income households that receive other social benefits (Bono inflación). Increasing this temporary allowance is a more cost-effective and equitable way to shield the population most affected by rising prices (OECD, 2023[1]). More generally, as indicated by the PND 2018-20, Costa Rica should progressively eliminate fossil fuel subsidies, which run counter to energy efficiency and GHG emission mitigation objectives.

2.6. Investing in the transition to a green and decarbonised economy

2.6.1. Public environment-related expenditure

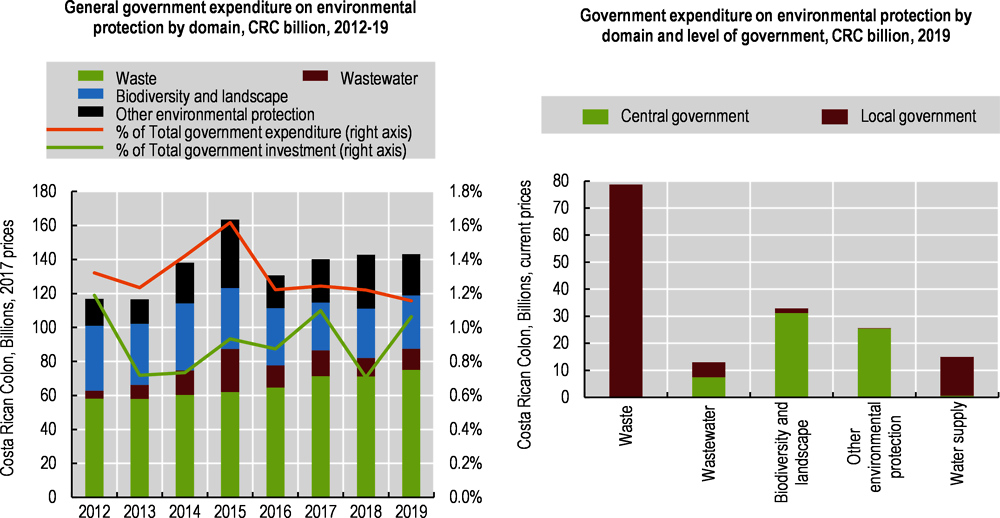

Public spending on environmental protection averaged 0.4% of GDP and 1.2% of general government expenditure in 2012-19 (Figure 2.7).12 Most spending went to waste management and, to a lesser extent, biodiversity. Spending on waste management increased during the period, accounting for more than half of government environmental spending in 2019. After a decline, expenditure for protecting biodiversity and landscape increased in 2017-19 to 22% of total public environmental spending. However, this was still 18% below the 2012 level. More than half of public environmental expenditure (57% in 2019) occurs at local level, largely for waste management. Local governments execute all capital spending in the waste and wastewater sectors, as well as in water supply infrastructure. Central government current and capital spending focuses on biodiversity and landscape protection (Figure 2.7).

Figure 2.7. Government spending for environmental protection focuses on waste and biodiversity

Note: Government expenditure on environmental protection includes current expenditure and capital investment devoted to activities to prevent, reduce and eliminate pollution and degradation of the environment, e.g. pollution abatement (air, water, soil and noise), waste and wastewater management, and biodiversity protection, as well as research and development, education and training.

Source OECD (2023), “General Government Accounts, SNA 2008 (or SNA 1993): Government expenditure by function”, OECD National Accounts Statistics (database).

About 95% of spending in environmental protection is current expenditure. Government investment in environmental protection hovered around 1% of total government investment in 2012-19 (Figure 2.7). Investment has been insufficient to provide adequate waste and wastewater infrastructure (Chapter 1). Similarly, transport infrastructure is of generally poor quality (OECD, 2023[1]), although it has absorbed most of the public infrastructure investment in the last decade (CONARE, 2022[2]). Transport investment has gone largely towards extending the road network, neglecting its maintenance, as well as public transport. Roads are mostly not safe for walking and cycling due to lack of sidewalks and bicycle lanes (Chapter 1).

Overall, deteriorating public finances have limited capital investment in Costa Rica in the last decade (CONARE, 2022[2]). There is a need to reallocate resources to address gaps in environment-related and low-carbon infrastructure, improve service delivery to a growing population and enhance resilience of infrastructure to climate change impacts. The PNDIP 2023-26 plans to invest in the GAM rapid passenger rail service, with the support of international donors. However, it also continues to focus on extending the road network and does not foresee investment in the EV charging network, or cycling and walking infrastructure. Limited investment is planned in energy efficiency, waste management or diversification of renewable energy sources.

The transition to a green and decarbonised economy requires large-scale investment. Financial needs for implementing the PND are estimated at USD 5 billion for 2021‑25 (7% of GDP), mostly for investment in the transport and waste sectors. Speeding up the PND investments would boost economic recovery and employment (Groves and et al., 2022[30]). At longer term, achieving a decarbonised and digital economy could create 135 000 net jobs by 2050 (equivalent to 5% of the 2021 labour force), mainly related to clean energy, sustainable transport and efficient use of natural resources (Quirós-Tortós et al., 2022[31]).

In addition to being scaled up, public environment-related investment should be made more efficient. Costa Rica’s well-developed National Public Investment System (SNIP) aims to improve and harmonise project selection across the public sector. However, the institutionally decentralised sector and the autonomous agencies have their own budget process (separate from the central government budget process). Consequently, only part of the public investment by autonomous institutions is reported to the SNIP. For that reason, less than half capital expenditure is estimated to be reported in the SNIP (OECD, 2021[4]). On average, only 30% of the budgeted capital spending is used (OECD, 2023[1]).

Further improving capacity to execute capital investment projects will require stronger accountability mechanisms, transparency and impact evaluation. MIDEPLAN issued regulations and guidelines to integrate climate mitigation and adaptation considerations into the SNIP. It has also started implementing a taxonomy of sustainable infrastructure. Costa Rica has defined standards for using cost-benefit analysis but in practice has made little progress in using them to select projects (OECD, 2020[32]). Implementing green budgeting practices would help the government align public expenditure, as well as revenue, with climate and other environmental goals.

2.6.2. Financing environment-related and low-carbon investment

Given the limited fiscal space, more private participation in infrastructure projects is needed. Concessions and public-private partnerships (PPP) can help in this respect. So far, most of the concession contracts have had long execution delays. Costa Rica’s PPP legal framework is aligned with OECD standards, but inefficiencies remain (OECD, 2021[4]). In 2014, the Ministry of Finance established a unit to oversee PPP contracts. The National Concessions Council, a subsidiary body of the Ministry of Public Works and Transport, manages concession contracts. The coexistence of two different authorities to manage concessions and PPPs, respectively, creates inefficiencies and reduces transparency (OECD, 2021[4]). There is also a need to improve the PPP implementation capacity of the administrations. Thorough assessment of projects, adequate specifications of the contracts and proper fiscal accounting are crucial to maximise value for money of PPPs and limit risks for public finances (OECD, 2023[1]).

Costa Rica’s long-standing environmental commitments place the country in a favourable position to access international green finance, including through green, social, sustainability and sustainability‑linked (GSSS) bonds.13 A successful issuance of green bonds (USD 504 million) by a Costa Rican state-owned bank in 2016 indicates this is a viable source of financing for the government (OECD, 2023[1]). This issuance brought Costa Rica among the ten largest LAC issuers of GSSS bonds on international markets (as measured by the cumulative bond value issued in 2014-22) (CBI, 2023[33]). The experience of Colombia shows that sovereign green bonds in local currency could help mobilise finance from private and institutional investors in the domestic market (OECD et al., 2022[34]). The country could also consider developing so-called catastrophe bonds to provide insurance against losses caused by natural disasters and finance investment in adaptation to climate change. Work is ongoing to develop official government guidance to access finance from the Green Climate Fund.

The General Superintendence of Financial Institutions developed a methodology to assess climate-related financial risks of the country’s banks and financial institutions. A systematic application of this assessment methodology would enhance transparency and provide incentives for redirecting finance towards cleaner activities. Costa Rica would benefit from joining other LAC countries, like Brazil and Colombia, in developing and harmonising GSSS bond standards, corporate sustainability standards and taxonomies that identify activities and investment that contribute effectively to the green transition (OECD et al., 2022[34]).

2.7. Encouraging green business practices

2.7.1. Environmental protection expenditure of private enterprises

According to a BCCR survey of 272 companies, businesses spent some CRC 40 billion (USD 68 million) or 0.1% of GDP in 2019 for preventing or mitigating pollution and environmental degradation (BCCR, 2022[35]). This compares with CRC 150 billion (USD 255.41 million) in government environmental protection expenditure in the same year. Business expenditure declined markedly in 2020 with the COVID‑19 pandemic. In 2018‑20, businesses spent less than 1% of their total expenditure on environmental activities. About half of spending went to managing waste. The other major spending categories include controlling air emissions (13%) and other environmental activities such as obtaining environmental certification (17%). On average, 83% of spending is for current expenditure. The limited investment focuses on curbing emissions of air pollutants and GHGs. Manufacturing companies are those that invest the most. About 1 000 people per year were employed to conduct environment-related activities in companies in 2018-20, especially in the manufacturing and services sectors (BCCR, 2022[35]).

2.7.2. Voluntary approaches

Costa Rica has developed several measures to encourage businesses to engage in environment-friendly activities and investment, in line with its 2018 National Policy for Sustainable Production and Consumption. These include voluntary agreements, environmental business certifications and product labels. Since 2018, MINAE has been implementing the Programme of Voluntary Agreements for Cleaner Production (AVP+L). As of 2022, four companies have entered these agreements with MINAE, all in the agro-food sector. As part of the programme, the ministry has also conducted environmental training, technical assistance and audits for several companies.

According to the BCCR survey, 65% of companies had some form of environmental certification in 2018‑20, mostly under the Country Programme for Carbon Neutrality (PPCN), the Ecological Blue Flag Programme (PBAE) and Essential Costa Rica (BCCR, 2022[35]). The PPCN certifies companies that voluntarily track, reduce and compensate their direct and indirect GHG emissions. The Institute of Technical Standards (INTECO) releases five levels of certification corresponding to the extent of the companies’ climate mitigation actions. As of end 2022, 120 companies had been certified “Carbon Neutral”. Overall, since 2012 more than 200 companies, 21 municipalities and 2 districts have engaged in the PPCN. The PBAE was launched in 1995 to recognise beaches that met certain ecological criteria. Its scope has been progressively extended to include a “climate change” category for industrial companies that reduce energy and water use, improve their water management and engage in reforestation (among other activities). In 2019, around 400 private organisations were granted the Ecological Blue Flag certification. Costa Rica’s country brand Essential Costa Rica, in operation since 2013, also includes an environmental component, among several others. Companies or products can use the brand following a licensing protocol. The dimensions associated with the environmental component include energy efficiency, air emissions, water use and waste management (OECD, 2023[13]).

In 2019, MINAE started implementing its environmental and energy labels for products and services. INTECO approves the requirements for obtaining the labels, which are aligned with international standards. Costa Rica aims to have the labels recognised by mutual approval agreements with other countries in the region. As of February 2023, only two products had received the MINAE environmental label (a bottled water and a beer). There are also sector-specific labels and certifications, such as the Good Agricultural Practices Label, the Pura Vida label for sustainably caught and processed fish and seafood, the Certification for Sustainable Tourism and the Distintivo ABS for products using the country’s genetic resources (Chapter 3). This multitude of business certification programmes and product labels risks creating confusion for customers and investors, and generating “greenwashing”. Costa Rica would benefit from strengthening and harmonising the criteria for certification of organisations and products.

2.7.3. Green public procurement

With large spending on public procurement (12.5% of GDP in 2018), expanding green public procurement (GPP) can greatly help raise demand for cleaner products and services, thereby stimulating entrepreneurship, innovation and job creation in green industries. For instance, GPP can foster the creation of markets for recovered and recycled materials (Chapter 1). In 2015, Costa Rica was the first LAC country to adopt a National Policy for Sustainable Public Procurement, followed by technical regulations setting environmental criteria for public purchases of several items and services. As of 2020, sustainability criteria also apply to building construction or renovation works procured by public institutions. GPP is part of each public institution’s mandatory environmental management programme.

However, results have been modest, largely because the overall public procurement system is still fragmented and inefficient. The use of the electronic public procurement system became mandatory in 2016, but its uptake remains incomplete (OECD, 2023[1]). The new law establishing that all public institutions must carry their purchases through the central procurement system is a welcome step. Its full implementation has the potential to boost the effectiveness of GPP.

References

[35] BCCR (2022), Cuenta Gasto en Protección Ambiental Sector Privado 2018-2020, [Private Sector Environmental Protection Spending Account 2018-2020], Banco Central de Costa Rica, San José, Costa Rica.

[24] Blackman, A., Z. Li and A. Liu (2018), “Efficacy of command-and-control and market-based environmental regulation in developing countries”, Annual Review of Resource Economics, Vol. 10, pp. 381-404, https://doi.org/10.1146/annurev-resource.

[10] Bonilla-Murillo, F. et al. (2022), “Environmental compensation actions in Costa Rica: Disparity between commitments and actions”, Open Journal of Ecology, Vol. 12/5, pp. 287-305, https://doi.org/10.4236/OJE.2022.125017.

[33] CBI (2023), “Interactive data platform”, webpage, https://www.climatebonds.net/market/data/ (accessed on 20 March 2023).

[11] CGR (2022), Informe de auditoría de carácter especial acerca de la gobernanza de los procesos de evaluación ambiental que ejecuta la Secretaría Técnica Nacional Ambiental, [Special audit report on the governance of the environmental evaluation processes conducted by the National Environmental Technical Secretariat], Contraloría General de la República, San José, https://cgrfiles.cgr.go.cr/publico/docs_cgr/2022/SIGYD_D/SIGYD_D_2022015871.pdf.

[5] CGR (2022), Memoria Anual 2021, [Annual Report 2021], Contraloría General de la República, https://cgrfiles.cgr.go.cr/publico/docsweb/documentos/publicaciones-cgr/memoria-anual/2021/ma2021.pdf.

[2] CONARE (2022), Informe Estado de la Nación 2022, [State of the Nation Report 2022], Programa Estado de la Nación, Consejo Naciónal des Rectores, http://www.estadonacion.or.cr.

[25] CONARE (2020), Informe Estado de la Nación 2020, Programa Estado de la Nación, Consejo Naciónal des Rectores, http://www.estadonacion.or.cr.

[23] CONARE (2018), Informe Estado de la Nación 2018, [State of the Nation Report 2018], Programa Estado de la Nación, Consejo Nacional de Rectores, http://www.estadonacion.or.cr/.

[12] DHR (2022), Informe anual 2020-2021, [Annual Report 2020-2021], Defensoría de los Habitantes de la República, https://www.dhr.go.cr/transparencia/informes_institucionales/informes/labores/documentos/if_2020_2021.pdf.

[27] Elgouacem, A. (2020), “Designing fossil fuel subsidy reforms in OECD and G20 countries: A robust sequential approach methodology”, OECD Environment Working Papers, No. 168, OECD Publishing, Paris, https://doi.org/10.1787/d888f461-en.

[19] Flues, F. and K. van Dender (2017), “The impact of energy taxes on the affordability of domestic energy”, OECD Taxation Working Papers, No. 30, OECD Publishing, Paris, https://doi.org/10.1787/08705547-en.

[7] Gallup (2022), Gallup World Poll, website, https://ga.gallup.com (accessed on 31 January 2023).

[29] Garcimartín, C. and J. Roca (2022), Impacto fiscal y distributivo de las medidas adoptadas para hacer frente a la crisis energética en Centroamérica, Panamá y República Dominicana, [Fiscal and Distributive Impact of the Measures Adopted to Face the Energy Crisis in Central America, Panama and the Dominican Republic], Inter-American Development Bank, Washington, DC, https://doi.org/10.18235/0004563.

[30] Groves, D. and et al. (2022), A Green Costa Rican COVID-19 Recovery. Aligning Costa Rica’s Decarbonization Investments with Economic Recovery, United Nations Development Programme – Costa Rica, San José, Costa Rica.

[22] IEA (2022), Global EV Outlook 2022, IEA, Paris, https://www.iea.org/reports/global-ev-outlook-2022.

[16] Marten, M. and K. van Dender (2019), “The use of revenues from carbon pricing”, OECD Taxation Working Papers, No. 43, OECD Publishing, Paris, https://doi.org/10.1787/3cb265e4-en.

[8] Ministerio de Comunicaciones (2019), Plan de Acción de Gobierno Abierto de Costa Rica 2019-2022, [Costa Rica Open Government Action Plan 2019-2022], Ministerio de Comunicaciones de Costa Rica, https://observatorioplanificacion.cepal.org/sites/default/files/plan/files/Costa-Rica_4to%20Plan%202019-2022.pdf.

[21] Ministerio de Hacienda (2021), Costa Rica: El Gasto Tributario (GT) 2020, Metodología y Estimación, [Costa Rica: The 2020 Tax Expenditure (GT), Methodology and Estimation], Ministerio de Hacienda, San José, Costa Rica.

[28] OECD (2023), “Fossil Fuel Support Data and Country Notes”, OECD Work on Support for Fossil Fuels, (database), https://www.oecd.org/fossil-fuels/countrydata/ (accessed on 31 January 2023).

[1] OECD (2023), OECD Economic Surveys: Costa Rica 2023, OECD Publishing, Paris, https://doi.org/10.1787/8e8171b0-en.

[13] OECD (2023), OECD Responsible Business Conduct Policy Reviews: Costa Rica, https://mneguidelines.oecd.org/oecd-responsible-business-conduct-policy-reviews-costa-rica.pdf.

[18] OECD (2022), Pricing Greenhouse Gas Emissions: Turning Climate Targets into Climate Action, OECD Series on Carbon Pricing and Energy Taxation, OECD Publishing, Paris, https://doi.org/10.1787/e9778969-en.

[3] OECD (2022), The Short and Winding Road to 2030: Measuring Distance to the SDG Targets, OECD Publishing, Paris, https://doi.org/10.1787/af4b630d-en.

[26] OECD (2021), OECD Environmental Performance Reviews: Ireland 2021, OECD Environmental Performance Reviews, OECD Publishing, Paris, https://doi.org/10.1787/9ef10b4f-en.

[4] OECD (2021), Public Governance in Costa Rica, OECD, Paris, https://www.oecd.org/governance/costa-rica-public-governance-evaluation-accession-review.pdf.

[36] OECD (2020), Best Available Techniques (BAT) for Preventing and Controlling Industrial Pollution, Activity 4: Guidance Document on Determining BAT, BAT-Associated Environmental Performance Levels and BAT-Based Permit Conditions, Environment, Health and Safety, Environment Directorate, OECD, https://www.oecd.org/chemicalsafety/risk-management/guidance-document-on-determining-best-available-techniques.pdf.

[32] OECD (2020), OECD Economic Surveys: Costa Rica 2020, OECD Publishing, Paris, https://doi.org/10.1787/2e0fea6c-en.

[6] OECD (2019), Making Decentralisation Work: A Handbook for Policy-Makers, OECD Multi-level Governance Studies, OECD Publishing, Paris, https://doi.org/10.1787/g2g9faa7-en.

[9] OECD (2019), OECD Accession Review of Costa Rica in the Fields of Environment and Waste Summary Report, OECD, Paris, https://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=ENV/EPOC%282019%2918/FINAL&docLanguage=En.

[34] OECD et al. (2022), Latin American Economic Outlook 2022: Towards a Green and Just Transition, OECD Publishing, Paris, https://doi.org/10.1787/3d5554fc-en.