Many space systems are reaching maturity in terms of performance at a time when their capacities are needed to deal with pressing global challenges – from accelerating climate change impacts to natural resource depletion. This chapter explores overarching trends in space innovation and funding for space programmes and activities. It also reviews how the space economy has fared in recent crises and identifies possible game changers for the coming years.

The Space Economy in Figures

Responding to Global Challenges

Abstract

This chapter explores overarching trends in space innovation and funding for space programmes and activities. It reviews how the space economy has fared in recent crises and identifies possible game changers for the coming years and provides multiple pointers for policy action.

The digitalisation of society and rising geopolitical tensions worldwide highlight the importance of space infrastructure, including space-based systems and their supporting ground segments (Undseth and Jolly, 2022[1]).

Satellite networks are increasingly recognised as integral parts of the economic infrastructure for information technologies and communications, while space launch facilities are becoming critical parts of overall transportation infrastructure (Van de Ven, 2021[2]). An important aspect of space infrastructure is how it has become essential in supporting other critical infrastructures and activities, such as the energy and finance infrastructures, public safety, transportation (e.g. air traffic management), and food supply. For example, energy grid systems rely on high-precision timing signals from navigation satellites to synchronise electrical waves and detect potential problems and faults in the transmission infrastructure. OECD (2019[3]) tracks the expansion of satellite navigation constellations and associated augmentation systems worldwide.

Number of countries per designated sector

1. Space sector infrastructures encompass all space systems, whether public or private, that can be used to deliver space-based services, both space-based (e.g. orbital spacecraft) and terrestrial (e.g. launch facilities, ground stations, mission control centres).

Source: Undseth and Jolly (2022[1]), "A new landscape for space applications”, OECD Science, Technology and Industry Policy Papers, No. 137, https://doi.org/10.1787/866856be-en.

As shown in Table 1.1, space technologies support more than half of the 16 most frequently designated critical infrastructures in OECD countries. Several OECD countries (Belgium, France, Spain, United Kingdom) designate the space sector itself as “critical”, and many more countries include space activities in other categories – satellite telecommunications are typically included in “ICT (Information and Communication Technology)” and space manufacturing in “critical manufacturing” and/or “defence industry” (OECD, 2019[4]). It is worth noting that the designation as a “critical” infrastructure can be accompanied by a higher administrative burden. The US Aerospace Industries Association is taking a stance against designating the “space sector” as critical infrastructure because several space activities are already implicitly designated as such – as part of communications, critical manufacturing, transportation, etc. – and such an indiscriminate approach may put undue regulatory and economic pressure on small businesses, for example (AIA, 2023[5]).

The growing supply and quality of space-based data and signals (much of which is open access), combined with improved capabilities of data processing and analysis, may finally be unleashing the full potential of space technologies. Recent illustrations include the responses to the Russian Federation’s [hereafter ‘Russia’] war of aggression against Ukraine, where satellite signals and imagery have made important contributions to Ukraine’s war efforts and supported an unprecedented near-real-time media coverage of events (Undseth and Jolly, 2022[1]). Importantly, this also demonstrated the strategic importance of robust space-based broadband infrastructure, provided today by commercial operators such as SpaceX. There are several plans underway for many national and commercial broadband constellations, including the GuoWang project of the People’s Republic of China [hereafter ‘China’] and the European Union’s IRIS2 constellation.

Furthermore, during the COVID-19 crisis, space infrastructure provided high-speed connectivity to remote locations (e.g. establishing links to remote hospitals, residential and small business customers, and deployment of online solutions schooling) as well as earth observation imagery for industry intelligence and monitoring of remotely located installations (OECD, 2020[6]).

As for tackling the accelerating crisis linked to climate change and its policy responses, in 2022 newly launched satellites detected more than 1 000 human-induced methane super-emitter events landfills (Carrington, 2023[7]), demonstrating the global and continuous reach of space-based earth observation feeding data in assessing the sources of carbon emissions around the world (more on this in Chapter 2).

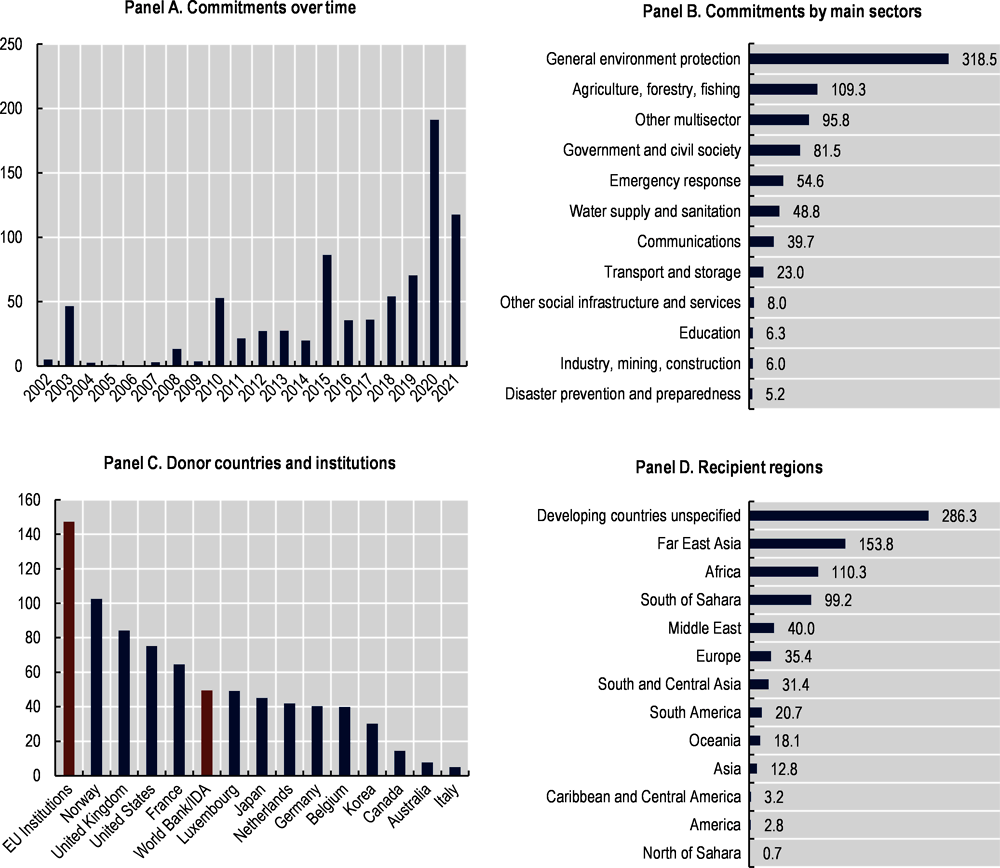

Space technologies are also increasingly used in official development assistance, as shown in Figure 1.1, with a notable growth in commitments over 2002-21, reaching more than 700 million inflation-adjusted USD in total over the period. Key applications include the monitoring of the environment and forests; information services to food producers; disaster prevention and emergency response; and different types of communication services via satellite TV and radio. This growth reflects targeted efforts and projects of several OECD countries, including the US SERVIR partnership programme between the US National Aeronautics and Space Administration (NASA) and the US Agency for International Development (USAID); the International Partnership Programme in the United Kingdom; the Geodata for Agriculture and Water (G4AW) project in the Netherlands; and the Satellite Data Programme of Norway’s International Climate and Forest Initiative (NICFI). At the international level, the European Space Agency has teamed up with the International Development Association (IDA) and the Asian Development Bank to create the Space for International Development Assistance (ESA) programme, which aims to improve the uptake and understanding of earth observation data in development projects. Finally, the Global Monitoring for Environment and Security and Africa (GMES & Africa) initiative, co-funded by the European Commission and the African Union Commission, applies data and services from the European earth observation Copernicus programme to the African context.

More granular data on space-related official development assistance can be found in this publication’s country profiles, featuring space programmes of OECD Space Forum members. Furthermore, a forthcoming OECD working paper will study space-related official development assistance in greater detail, looking at the type of projects and main channels of assistance.

Commitments in constant USD million (base year = 2021)

Notes: EU: European Union; IDA: International Development Association.

Source: Analysis based on OECD (2023[8]), “Creditor Reporting System (CRS)", OECD.stat (database), https://stats.oecd.org/Index.aspx?DataSetCode=CRS1 (accessed on 24 April 2023).

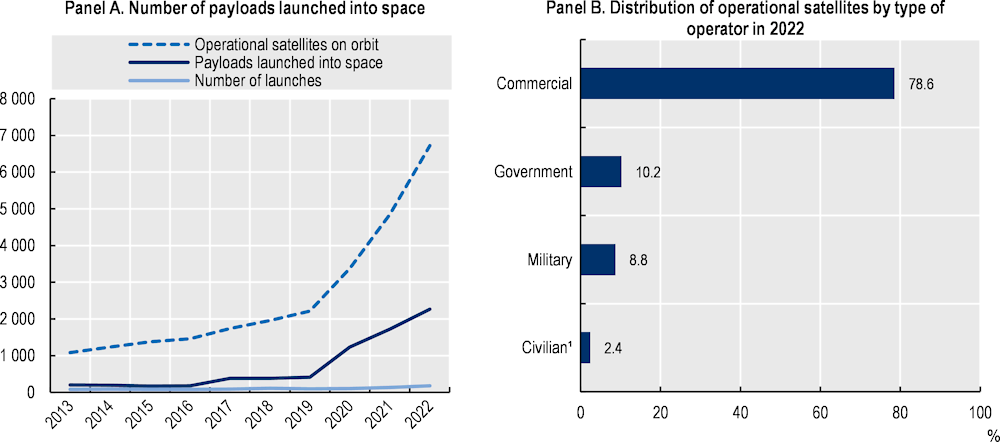

There have never been so many active satellites in orbit. More satellites in orbit means in principle a growing availability of useful space services, but this comes also with its challenges. The number of satellites launched in the last 15 years has dramatically increased, as shown in Figure 1.2. After several active decades of space system deployment in the 1970s and 80s, launch activity had decelerated at the turn of the 21st century with some 80-110 objects (or payloads) launched yearly. This changed in 2013, which saw almost a doubling in launched objects. Since 2019, this number has been well above 1 000 per year and rising, with no end in sight.

As a result, orbits are getting more crowded. By the end of 2022, there were some 6 700 operational satellites in orbit (in addition to many more defunct satellites and other debris objects), twice the number recorded by the end of 2020 (Union of Concerned Scientists, 2023[9]). Active satellites are mainly operated by commercial actors (78.6%), followed by non-military government and military actors (10.2% and 8.8%, respectively), as shown in Figure 1.2. Chapter 3 looks more closely at these launch trends and at the ensuing “race” to occupy orbital space and resources such as the electromagnetic spectrum needed for operations and transmitting data and signals to Earth, as well as the effects of growing competition on the space sector itself.

It is worth noting that active satellites account for only 25% of (unclassified) space objects tracked by the US Space Force (2023[10]). Satellites in the orbits closest to Earth clear their orbits fairly quickly by natural processes, but satellites at higher altitudes may stay in orbit for decades or even centuries (or forever, as in the geostationary orbit) unless they are intentionally cleared from orbit. In addition, there are other types of debris, such as abandoned rocket stages or fragments from collisions or explosions. As a result, the orbital environment still carries traces of human activity dating back to the beginning of the space age in the late 1950s. The effects of this pollution on the orbital environment and society more broadly are treated in Chapter 4.

1. Civilian operators typically include universities and radio amateurs.

Note: Each category of actors also includes partnerships and dual-use missions (e.g. public-private, military-commercial).

Sources: US Space Force (2023[10]), space-track.org website, https://www.space-track.org, data extracted 16 December; and Union of Concerned Scientists (2023[9]), UCS Satellite Database, 1 January 2023 version, data extracted 27 July 2023, https://www.ucsusa.org/resources/satellite-database.

The overall short-term outlook for space activities is positive despite recent economic shocks, with sustained and (in some cases expected growing) government demand for space products and services, as well as increased commercial activity in certain domains. However, although many indicators of the space sector’s expansion look positive – the growing number of countries, players, launches, satellites, a growing role in infrastructures etc., they do not necessarily translate into growth in revenues. The following sections look more closely at this apparent contradiction.

The optimism of numerous industry forecasts for the coming decade is not borne out by the historic record: only a limited number of activities have demonstratively grown between 2008 and 2021, as shown by data collected on behalf of the US Satellite Industry Association (BryceTech, 2022[11]). The manufacturing of positioning, navigation and timing (PNT)-related user (“ground”) equipment, such as receivers and chipsets, is the only space industry segment that has experienced notable growth in real terms since 2008, with a compound average growth rate of 7% for the 2008-21 period. The other industry segments have, on average, performed more modestly: 0.8% compound average growth for space manufacturing, 1.3% and 1.5% for satellite services and launch, respectively.

These trends, based on data from industry surveys, are also reflected in the estimates by the Bureau of Economic Analysis (BEA) for the US space economy, which indicate that the average annual growth rate for the 2012-19 period of 1.6% was below the overall US growth rate (Highfill, Jouard and Franks, 2022[12]). The BEA’s estimates come from the US Space Economy Satellite Account (SESA), and as such, they provide robust trends for more space industry segments integrated into US national statistical accounts.

Given such modest historical growth rates, it is hard to believe that the sector will become a “1 trillion economy” by 2040, as previously estimated by several investment banks (OECD, 2019[13]). Such projections lack in most cases the precision and granularity needed to adequately assess the health and growth potential of individual industry segments. Although this is an ongoing challenge, notable statistical efforts over the last years (e.g. the work to create statistical thematic (or “satellite”) accounts in the United States and Europe) are strengthening the ability to identify and measure the space economy and its components and making them more comparable with other sectors in the global economy (OECD, 2022[14]).

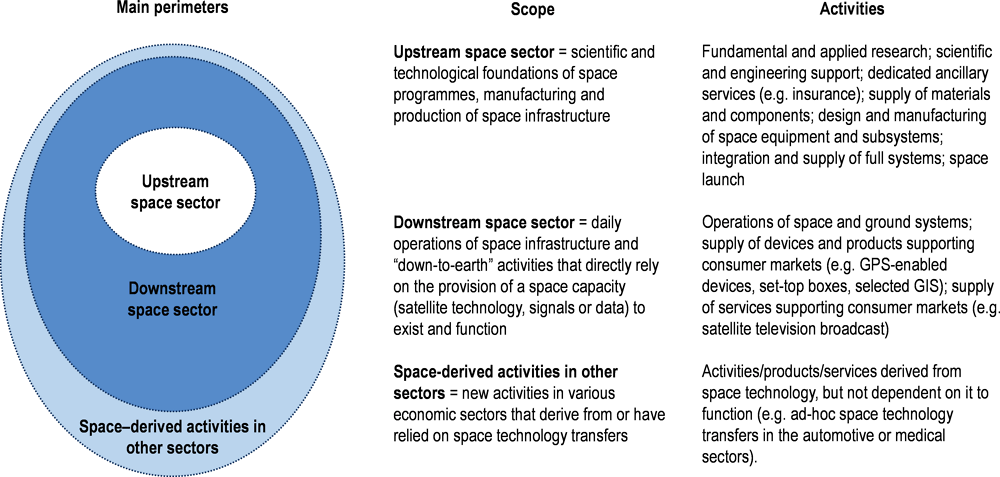

To better understand the industry dynamics, one needs to take a closer look at the distinct parts of the space economy. Indeed, the sector is deeply heterogeneous in terms of customer base, nature of activity and dependency on trade, and the different industry segments have fared very differently in the 2020-22 period The OECD Handbook on Measuring the Space Economy (2022[14]) defines three perimeters of activities: upstream, downstream and space-derived activities (Box 1.1).

For measurement purposes; the OECD Handbook on Measuring the Space Economy (2022[14]) defines three perimeters of activities in the space economy (Figure 1.3): the upstream space segment, comprising fundamental space activities such as space manufacturing and launch; the downstream segment, including activities that depend on the exploitation of space data and signals (e.g. satellite television) as well as the manufacturing of associated equipment; and finally, “space-derived activities”, which are derived from space technologies but not dependent on them to function.

Source: OECD (2022[14]), Handbook on Measuring the Space Economy, 2nd Edition, http://doi.org/10.1787/8bfef437-en.

Recent estimates of the size of the global space economy, when excluding government procurement, range from some USD 200 to 350 billion depending on the definition and measurement method, with the upper-range estimates also including revenues from location-based services (e.g. mobility apps on mobile phones) enabled by navigation satellite services (GNSS) (see for instance the Market Report of the European Space Agency (EuSPA, 2022[15])). Upstream segment revenues are dwarfed by those of downstream segments, typically satellite television and, increasingly, revenues generated by PNT services and equipment. Overall space economy revenues are strongly affected by developments in the satellite television market, which is declining faced with the rollout of fixed broadband and consumers’ growing preference for streaming platforms over linear television.

The space economy has been further affected by the impacts of COVID-19 and other economic shocks.

The degree of exposure of the space sector to the COVID-19 crisis has varied by industry segment, company size and company age. In general, upstream activities, comprising “core” industry segments such as manufacturing and space launch (see Figure 1.3), seem to have weathered the global pandemic relatively well, bolstered by government contracts, support measures and their ability to continue operations during lockdown, although also suffering considerable supply chain delays (OECD, 2020[6]).

But messages are mixed.

In the United Kingdom, in a retrospective 2022 survey, less than half of respondents reported negative impacts of COVID-19 (on workforce and income, on demand, and from suppliers), with a notable share (15%) signalling positive effects on demand (know.space, 2023[16]).

In Canada, a similar survey shows that the majority of respondents experienced negative effects on revenues, demand and supply chains (CSA, 2023[17]).

Finally, a German survey conducted among space start-ups at a relatively early stage of the pandemic found that almost 40% of respondents reported “dramatic” negative impacts that threatened the existence of their firm, with a large majority finding government measures insufficient (BDI, 2020[18]).

The strongest immediate impacts were probably in the downstream segment. Businesses catering to the transportation and extractive industries (e.g. inflight broadband) were the hardest hit, while broadband providers saw an increase in demand, enabling broadband connectivity from remote locations without appropriate terrestrial telecommunications infrastructure. Earth observation actors also observed increased demand for industry intelligence and remote monitoring applications.

Russia’s war of aggression against Ukraine has dealt an additional blow to space industry supply chains (Undseth and Jolly, 2022[1]). In this niche market, Russia and Ukraine have long been notable international providers of specialised components, space systems and launch services. For instance, several US and European launchers have until recently relied on Russian- and Ukrainian-built engines (CNES, 2022[19]). In 2022, The European Space Agency stopped using the Russian Soyuz launcher, which since 2011 had launched satellites from the Kourou Space Centre in French Guiana, including European Union earth observation and satellite navigation satellites. The same year, the UK operator OneWeb suspended launch activities at the Russian-operated Baïkonur spaceport in Kazakhstan and left behind 36 broadband satellites, which have not been returned (OneWeb, 2022[20]).

It is worth noting that a too-narrow focus on commercial revenues may not fully capture the critical changes that are taking place in the sector, such as in the composition of investors and industrial actors, the volume of investments, and the maturing of disruptive technologies and services.

In the last 15 years, “new space” actors have provided disruptive new offerings in launch services, space manufacturing and operations, as well as in specific applications such as earth observation and satellite communications. This, combined with significant advances in data processing and computing, has lowered the cost of access to space and expanded the range of space applications, paving the way for new entrants into the sector and boosting further interest in space activities.

The term “new space” was coined in the early 2000s to distinguish a new type of commercial activities and actors from incumbents in the space sector. “Old space” actors were often affiliated with defence and aerospace industries, closely linked with government agencies on year-long projects and reliant on government procurement and R&D support.

In contrast, “new space” actors, big and small, brought with them funding and innovation strategies from other industries and typically still have one or several of the following characteristics:

having a high dependence on private capital (third-party or otherwise), including equity finance in many cases, with some of the proponents of “new space” being digital economy billionaires

making maximal use of lean production processes (standardisation, using off-the-shelf components, additive manufacturing) and digital business models (“space-as-a-service”, etc.)

putting on the market new products and services born from the convergence of digital and space technologies: miniaturised satellites, satellite constellations, data analytics combining location-based and satellite data.

“New space” activities have benefited from the favourable conjunction of technological developments, policy decisions and macro-economic events in the early 2000s. This includes a radical reduction in the size of space systems and instruments and innovative solutions for launching multiple satellites into orbit, as well as advances in storage, processing, and analysis of data (OECD, 2019[13]); new sources of funding from equity finance; and strategic policy decisions creating new markets and improving access to new types of actors, such as a shift to service buys in the United States and widespread promotion of commercial activities among both established and newer space actors (e.g. India, China, Korea) (OECD, 2023[21]). Some of the most important impacts of “new space” activities are listed below:

disruption of the launch market with more affordable and reusable launch services

disruptive and new applications from micro- and nanosatellite constellations (weighing less than 100kg and 10kg, respectively, see Box 1.2) in the low-earth orbit, for geospatial and signal intelligence (e.g. imagery, radio-frequency monitoring), weather and emissions monitoring, Internet-of-Things, etc.

deployment of constellations with thousands of satellites for satellite broadband in the low-earth orbit (with satellites weighing some 150-200kg, which is still “small” compared to traditional satellite design).

Several developments in both the upstream and downstream segments could further shake up the status quo.

The use of space is closely related to the cost of access, and the popularisation of cubesats (cube-shaped miniature satellites originally developed for university projects) and other miniaturised satellites, has been a major enabler.

Satellites come in all shapes and sizes. The biggest telecommunications satellites in geostationary orbit weigh several metric tonnes, but it is increasingly possible to squeeze technology into smaller vessels, which may be interesting from a production and launch cost perspective, although it also may shorten mission life. For example, there have been several demonstration flights of prototype “chipsats”, weighing less than 10 grammes.

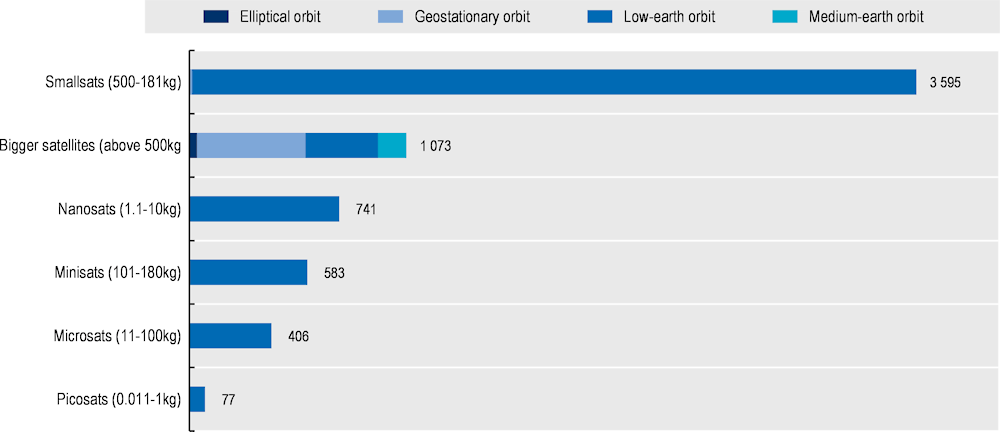

Satellites with a mass equal to or below 500 kilograms are generally considered “small”, and the US National Aeronautics and Space Administration (2015[22]) uses the following breakdown for even smaller satellites:

Minisatellite, 100-180 kilograms

Microsatellite, 10-100 kilograms

Nanosatellite, 1-10 kilograms

Picosatellite, 0.01-1 kilograms

Femtosatellite, 0.001-0.01 kilograms

Cubesats belong to the class of nanosatellites and use a standard size and form factor. A standard cubesat measures 10x10x10 centimetres (1U), and is extendable to larger sizes, 1.5U, 2U etc. They provide an attractive platform for a range of applications either alone or in constellations, including commercial operations.

Among the population of operational satellites, bigger satellites are outnumbered by smaller ones, the most common of which are smallsats and nanosats (Figure 1.4).

Number of satellites, data as of 31.12.2022

Notes: The mass calculated is mass at launch. The sample excludes 243 blank entries.

Source: Adapted from Union of Concerned Scientists (2023[9]), UCS Satellite Database, 1 January 2023 version, data extracted 27 July 2023.

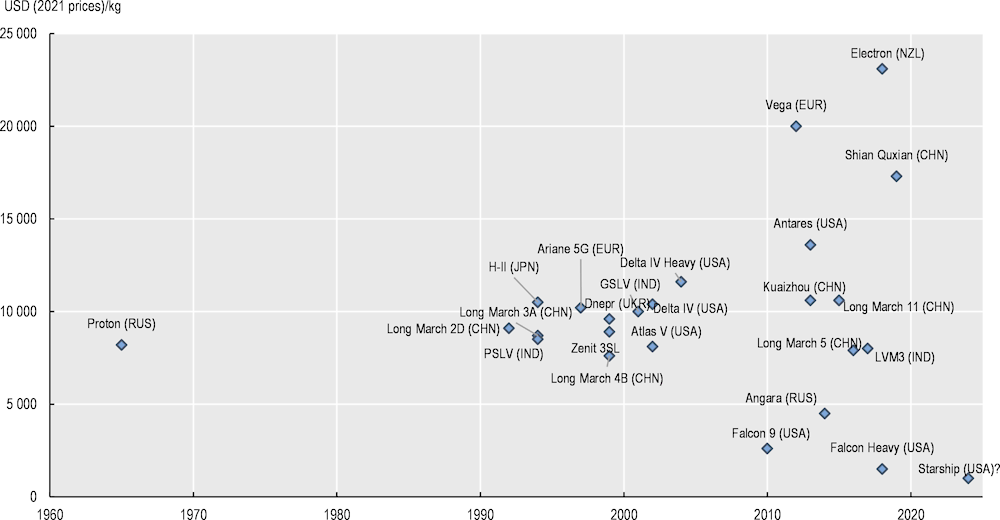

Launch options are becoming more numerous, diversified and cheap, with new opportunities closer to government, commercial and academic clients in Asia, North America and Europe (Figure 1.5), although Europe has for now no dedicated operational heavy launcher available. Lower prices, combined with more regular launches, could potentially create new commercial opportunities (e.g. for microgravity pharmaceutics, point-to-point space transportation), although launch represents just one of several cost drivers (Hollinger, 2023[23]). It could furthermore open new opportunities for government space programmes.

Furthermore, new commercial heavy-lift launchers (e.g. the US Falcon Heavy) are driving down prices to unprecedented levels. It is worth noting that launch prices are often not disclosed (e.g. for military launches) or not directly comparable due to heavy rocket customisation. The fully reusable super heavy-lift launcher Starship had a second failed orbital launch attempt in November 2023 but has several other prototypes in various stages of assembly. There is limited information about Starship’s pricing. It is expected to go lower than existing offerings, but it would be competing against other launchers from the same company. There is also the question of availability, as SpaceX needs considerable launch capability to deploy its own missions, including the ultimate objective of colonising Mars. The development of new launchers is further described in Chapter 3.

Estimated price per kilogramme, in USD (2021 prices)

Note: The figure includes small, medium and heavy-lift launchers that were operational in early 2023. Several of these launchers were set to retire by the end of 2023, e.g. Ariane 5 and Delta IV. Price per kilogramme is generally lower on heavy-lift vehicles. Deflators and currency exchange rates are the author’s own.

Source: Adapted from Roberts (2022[24]), “Space Launch to Low Earth Orbit: How Much Does It Cost?”https://aerospace.csis.org/data/space-launch-to-low-earth-orbit-how-much-does-it-cost/.

Despite considerable progress in the last decade, hundreds of millions of people in both high- and lower-income countries still have no access to a fast and reliable fixed Internet connection. In this context, satellite systems certainly have a role to play, despite technical limitations compared with terrestrial alternatives. The most performant low-earth orbit constellations under development/deployment (e.g. OneWeb, Starlink, Kuiper Systems), could offer a total capacity of around tens of terabytes per second, compared to terrestrial networks which move around thousands of terabytes per second (Pachler et al., 2021[25]). There are also other issues, such as sensitivity to weather conditions and the need for clear sight of the sky and horizon. Finally, there is the question of pricing of services, with operators providing limited information about how they intend to make their activities profitable. Satellite systems would therefore be most usefully deployed as a complement to terrestrial networks, by:

filling the coverage gap to deliver fixed broadband services to residential and business users in remote and isolated geographic areas by offering ubiquitous and easy-to-deploy solutions

providing backhaul or backbone network interconnection to the global Internet for terrestrial fixed or mobile telecommunication network service providers

expanding the market for satellite broadband to deliver connectivity to lower-density areas, closely adjoining urban areas (OECD, 2017[26]; 2019[13]).

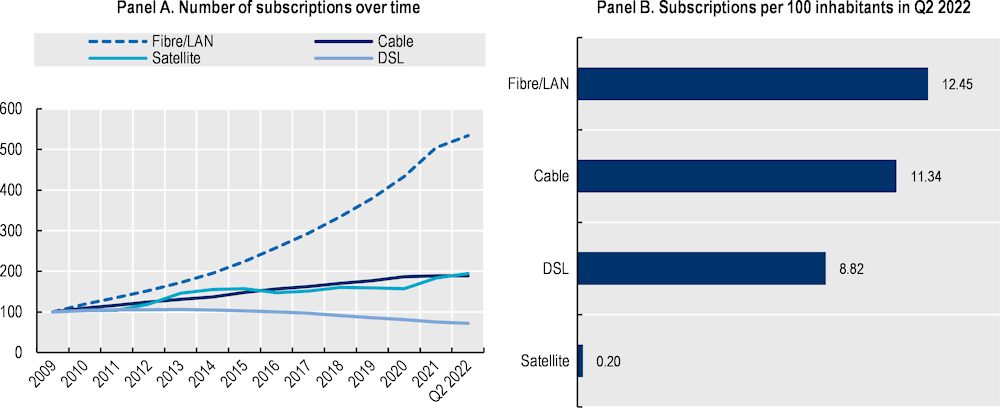

Satellite broadband is still much less used than other technologies (only 0.2 fixed broadband subscriptions per 100 inhabitants in the OECD area ( (OECD, 2022[27])), as shown in Figure 1.6. However, this could change with the rollout of new consumer services. More than ten broadband satellite constellations are in different stages of development, with two companies (SpaceX and OneWeb) having already launched satellites. The US operator SpaceX is by far the most advanced, with new satellites launched every two weeks or so and comprising more than 3 000 operational satellites by the end of 2022. Indeed, Figure 1.6 shows a notable rise in the number of subscriptions from 2020 onwards.

The satellite mobile broadband market is also evolving rapidly. Existing services, typically catering to military, remotely located and maritime/offshore clients, require dedicated devices such as antennas and handheld equipment, but emerging projects are exploring different types of satellite connectivity on normal consumer mobile phones.

In 2023, technology company Apple and satellite operator GlobalStar started offering emergency SOS text messaging via satellite on iPhone 14 models.

Several satellite and mobile operators have announced partnerships to develop satellite-to-mobile services, including SpaceX and T-mobile Amazon Kuiper and Verizon, respectively.

Start-ups are developing constellations for satellite-to-mobile connectivity, including US companies Lynk and AST SpaceMobile. The latter launched a test satellite in 2022 (which has raised concerns in the astronomy community because of its brightness, more on this in Chapter 4).

Notes: DSL: Digital subscriber line; LAN: Local area network.

Source: OECD (2022[27]), "Broadband database (Edition 2022)", OECD Telecommunications and Internet Statistics (database), https://doi.org/10.1787/dc2d97f8-en (accessed on 25 May 2023).

The lowering of launch costs and the growing number of orbital clients is making the emergence of a viable “in-orbit” economy more credible, comprising activities such as in-orbit servicing, connectivity relay and debris removal, or even resource generation and extraction, designed to serve terrestrial needs and/or support further space habitation and exploitation. Large parts of this in-orbit economy would certainly be fuelled first by heavy public R&D investments.

For instance, several connectivity relay constellations are under deployment, aiming to provide high-speed data transfer services via laser or radio-frequency links for satellites in low-earth orbit that are out of reach of terrestrial ground stations (Werner, 2022[28]). Other activities are at a much earlier technological stage. In 2023, a solar power prototype from the US Caltech University demonstrated wireless energy transfer from space to Earth (Caltech, 2023[29]).

Still, accessing space is only one of several hurdles to clear, including a combination of technological, regulatory and economic challenges. For instance, in-orbit servicing and debris removal entail launching a dedicated spacecraft and agreements with operators to access proprietary technology. While service contracts typically envisage multiple servicing or multiple spacecraft, it remains costly for potential client operators. Asteroid mining companies attracted more than USD 50 million USD million in the 2010s until the bubble burst in 2019, because of investor scepticism about the technological feasibility and future customer base (Abrahamian, 2019[30]).

Governments play a pivotal role in industry segments such as space manufacturing and launch, as funders and procurers of R&D, products and services. In some OECD countries, sales to government customers account for a large share of revenues (e.g. close to 70% of upstream revenues in both Europe and Korea in 2021 (Eurospace, 2022[31]; Korean Ministry of Science and ICT, 2022[32])). However, private actors and venture capitalists have started to play a bigger role in recent years.

As a share of GDP (%)

1. Estimates, also including military activities, 2. Includes contributions to Eumetsat and the European Space Agency, 3. Includes AUT, BEL, EST, FIN, FRA, DEU, GRC, IRL, ITA, LUX, LVA, LTU, NLD, PRT, SVK, SVN and ESP, 4. Includes non-EU member contributions to selected EU programmes (e.g. Copernicus, Galileo).

Source: OECD calculations based on official government information.

Constant local currencies and USD (base year 2015)

Notes: United States data include civilian budgets for the National Aeronautics and Space Administration and space programmes in the Departments of Commerce, Transportation and the Interior. Data for France, Germany, Italy, Netherlands, Norway, Switzerland and the United Kingdom include contributions to the European Organisation for the Exploitation of Meteorological Satellites and the European Space Agency. Data for Norway, Switzerland and the United Kingdom also include subscriptions to selected European Union programmes (e.g. EGNOS/Galileo, Copernicus).

Source: OECD calculations based on official government information.

Public space budgets support a range of activities, including government services and operations (e.g. defence, disaster management, environmental protection); space science and exploration; and research and development (R&D), performed either in-house by government agencies or outsourced to external academic and commercial actors through grants and procurement. Over the last decades, the focus on economic growth, innovation and entrepreneurship has increased.

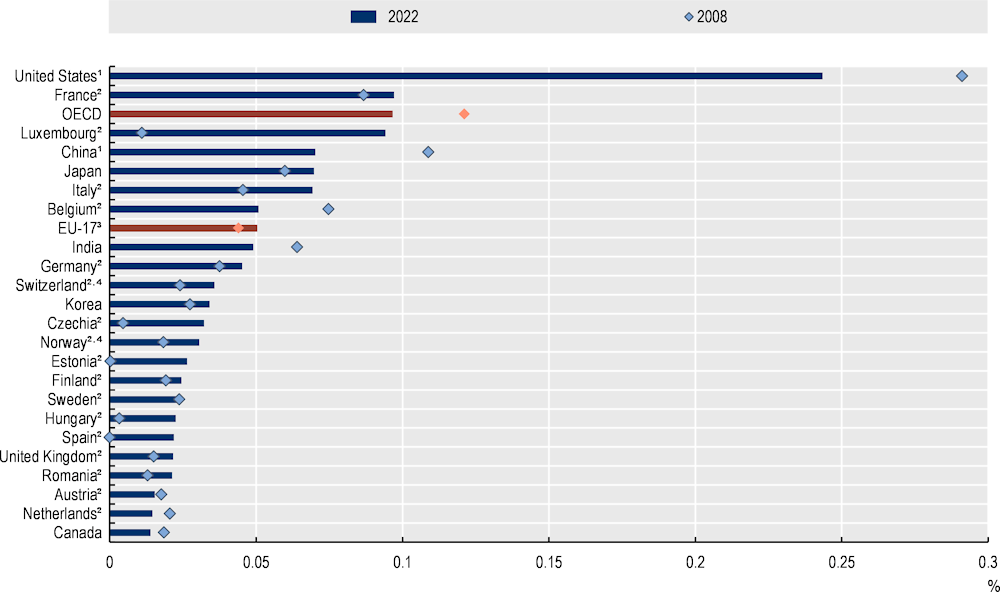

In 2022, government space budgets accounted for an estimated 0.10% of total OECD gross domestic product (GDP), compared to 0.12% in 2008 (Figure 1.7). Changes in the OECD average are dominated by developments in big and established space nations (e.g. United States, European Union countries, Japan) such as the retirement of the US space shuttle in 2011 or the introduction of European programmes Galileo (satellite navigation) in the early 2000s, and Copernicus (earth observation) in 2014.

Another part of the picture is the evolving role of smaller and emerging actors. Luxembourg, for instance, has significantly increased spending since 2018, its national programme includes support to new national facilities and an ambitious R&D support programme attracting start-ups. Korea started developing its space programme in the early 1990s and launched its first fully autonomously-built rocket in 2022. New Zealand has been proposing commercial launch services since 2017 and other small OECD countries are building spaceports (e.g. Canada, Norway, Sweden). Several countries in Eastern Europe have significantly increased their space budgets as they get more closely associated with European space programmes, both in the European Space Agency (ESA) and the European Union.

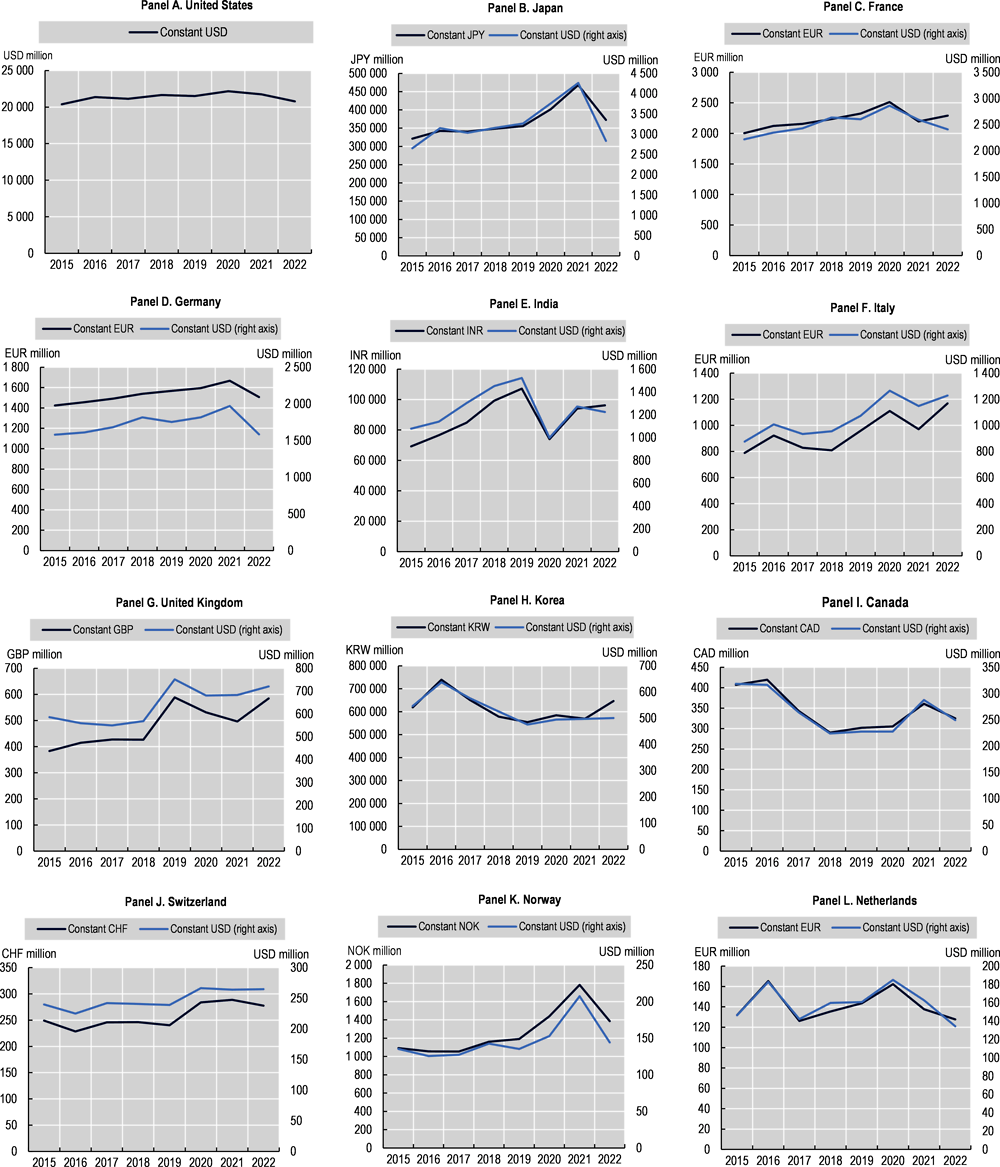

Figure 1.8 shows budgetary changes in greater detail over the 2015-22 period for selected OECD countries and other economies, generally revealing constant or increased levels of spending, but with inflation affecting purchasing power in 2022. COVID-19 has had limited short-term effects on space programmes. In several cases, it has led to an increase in spending through specific government plans and recovery packages (e.g. France, Italy). However, the future of civilian government space activities is uncertain.

There is growing interest in several OECD countries and beyond for military space activities, illustrated by a multiplication of military strategies and investments (e.g. the creation of the US Space Force, military strategies in France and, the United Kingdom). It is uncertain how this will affect civilian space activities. For the fiscal year 2023, the US Congress allocated more funding to the US Space Force (USD26.3 billion), three years after its creation in 2019, than to NASA (USD 25.4 billion). The ESA science programme's share of the total multi-annual budget has gradually decreased over the years (in an overall increasing budget) accounting for 24% of the 2002-06 budget compared to 19% of the allocations for 2023-27.

Strong inflation is also affecting purchasing power, effectively limiting options for launching new activities. For example, both ESA’s and NASA’s budgets saw a decrease in funding after the 2008-09 financial crisis, followed by a rebound (delayed in Europe due to the prolonged crisis) and then another inflation-induced dip in 2022, which brings current 2023 purchasing power of NASA close to or below 2008 levels in real terms.

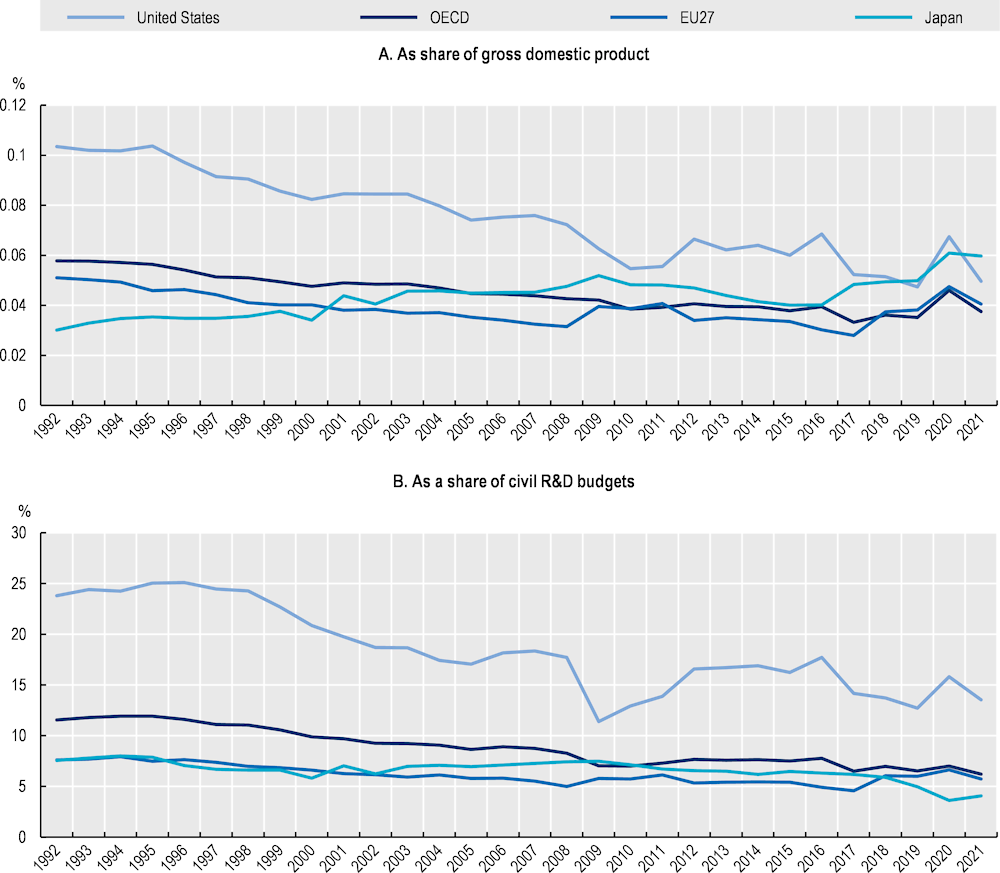

Figure 1.9 traces longer-term trends since the 1990s for Japan, EU27, the United States and the OECD area. The data show an overall decline in public R&D allocations since the 1990s, both as a share of GDP and of total civilian R&D budgets, coinciding with the end of the Cold War, the deregulation of certain downstream applications and the finalisation of the International Space Station (1998). It is worth noting that the negative trend is slowing down or even reversed towards the end of the period.

Note: Panel A illustrates how public civil space R&D allocations compare to the size of the overall economy (as a share of GDP) while panel B displays their order of priority in the overall public civil R&D portfolio (as a share of civilian R&D budget).

Source: OECD (2023[33]), "Main Science and Technology Indicators", OECD Science, Technology and R&D Statistics (database), https://doi.org/10.1787/data-00182-en (accessed on 15 May 2023).

In the meantime, access to private funding, including private third-party sources of equity, debt and acquisition finance, has significantly improved since 2008 and reached an all-time high in 2021 with some USD 15.4 billion in global investments, according to one industry observer ( (BryceTech, 2023[34]), before significantly dropping in 2022. The data indicate a strong increase in equity finance (seed, venture, private equity, initial public offerings) from 2016 onwards. Although initially benefiting a limited number of companies (e.g. SpaceX and OneWeb), the distribution of funding is becoming more diversified, also geographically.

However, rising levels of inflation and interest rates are also negatively affecting the overall supply of venture capital, for all domains and activities. As observed by the US Venture Capital Association, in early 2022 available venture funding supply exceeded demand by a ratio of 1.5-to-1, while by the end of the year demand for funding surpassed supply 2-to-1 (NVCA, 2023[35]).

This will most likely lead to reduced investment in the space sector in the coming years from equity finance; but the sector may still be more attractive to venture capitalists than in previous decades, because of the evolving composition of its actors with more fast-moving and digital start-ups; the lowering costs of access to space and stronger public reliance on space technologies.

Overall, the outlook for the space sector and the space economy is good, but there are also reasons for concern, such as the environmental sustainability of space activities, the continuity of important public missions, or the vitality of the space innovation ecosystem, that will require a targeted and long-term response from decision makers.

Stabilising the orbital environment and mitigating debris will require concerted action at both national and international levels as well as innovative policymaking. Furthermore, more evidence is needed on the externalities of space activities as well as the socio-economic effects, e.g. of space debris or orbital congestion.

The OECD has published several reports on the economics of space sustainability, identifying some of the shorter and longer-term costs associated with space debris (Undseth, Jolly and Olivari, 2020[36]; OECD, 2022[37]). The OECD Space Forum and its partnering space administrations have also launched an original project on the economics of space sustainability, collaborating with universities and research organisations to assess the costs of space debris and the value of space applications.

Public funding will continue to play a key role in the space sector to maintain critical programmes and infrastructure, and to support commercial activities through R&D subsidies and partnerships; procurement programmes; and debt finance. However, there is room for improvement in where and how to deploy these instruments for the best effect and value for money.

Governments need to align strategic objectives that do not necessarily pull in the same direction. For instance, the consolidation/verticalisation of the commercial manufacturing segment in many countries may make it more cost-efficient but a more concentrated supply chain may be more vulnerable to shocks.

Also, supporting innovation and entrepreneurship may eventually lead to more innovation, but relying on incumbents and tested technology could reduce economic and technological risks.

Public authorities therefore need to identify the industry segments with the highest risk profiles – least likely to attract third-party capital – and provide adequate demand-side/supply-side support following national objectives and procurement guidelines.

The size and stability of public markets for space products and services affect business firms’ incentives to invest. Some 18% of respondents to the 2013 US industrial base “deep dive” survey reported that the variability in US government space-related demand had somewhat or significant adverse effects on their willingness to stay in the sector, their solvency, their ability to retain skilled personnel, etc. (US Department of Commerce, 2013[38]). Evidence from other STI (Science, Technology and Innovation) domains indicates that it could positively affect their ability to raise third-party funds. OECD research on “clean-tech” industries has found a positive correlation between government deployment policies and higher levels of equity financing (OECD, 2014[39]).

The OECD Space Forum will contribute further to these efforts by providing definitions and guidelines on how to measure the space economy to encourage evidence-based policies and international comparability of results (see OECD (2022[14])), and by compiling space-related policy instruments in the STIP Compass for Space Policies to support analyst and policy makers.

Faced with mounting fiscal pressures and global challenges, governments are invited to build partnerships at both the national and international levels. Government agencies have a broad range of procurement mechanisms and instruments at their disposal to make use of private sector capabilities (Undseth, Jolly and Olivari, 2021[40]). With revamped public procurement practices and more service buys, new partnerships are being set up with the space industry throughout OECD countries and beyond. Space agencies and other procurement agencies will need to have adequate and sustained skills and resources to negotiate contracts and carry out oversight.

At the international level, space is already characterised by high levels of collaboration, as international organisations and committees co-ordinate activities in space exploration, space science, earth observation, space-based meteorological observations, space debris, radio frequencies, disaster management, space education, etc. Still, more efforts will be needed to muster the necessary economic, technological, and human resources to sustain and expand existing and new missions in earth and space exploration, or other challenging domains. In this regard, a useful addition is the European Centre for Space Economy and Commerce (ECSECO), founded in 2022, which serves as a platform for cross-border and interdisciplinary discussions and research on these matters. Several important lessons from managing the COVID-19 crisis for science, technology, and innovation communities (OECD, 2023[41]) are also applicable to future space developments and their sustainability challenges:

Decision makers need to recognise the role of research infrastructures as unique resources for training and capacity-building; as intermediaries and brokers vis-à-vis other disciplines and sectors; and in international collaboration, by sharing data and analysis. For space, they include physical and virtual space infrastructures, such as the internationally co-ordinated meteorological satellites and future joint space stations for example.

The pandemic further showed how only globally inclusive responses can provide the necessary level of protection. The same applies to efforts to address space debris, which is a truly global challenge. Establishing or better employing existing international funding mechanisms, trusted relationships and scientific networks could contribute to making society more resilient.

References

[30] Abrahamian, A. (2019), “How the asteroid-mining bubble burst”, MIT Technology Review, 26 June, https://www.technologyreview.com/2019/06/26/134510/asteroid-mining-bubble-burst-history/.

[5] AIA (2023), AIA Critical Infrastructure Letter, 19 September, US Aerospace Industries Association, https://www.aia-aerospace.org/publications/aia-critical-infrastructure-letter/.

[18] BDI (2020), Auswirkungen der Corona-Pandemie im New Space-Sektor, Federation of German Industries, https://www.slideshare.net/BDIndustrie/auswirkungen-der-coronapandemie-im-new-spacesektor.

[34] BryceTech (2023), Start-up space 2023: Update on investment in commercial space ventures, https://brycetech.com/reports.

[11] BryceTech (2022), State of the Satellite Industry Report 2022, Report commissioned by the Satellite Industry Association, https://brycetech.com/reports/report-documents/SIA_SSIR_2022.pdf.

[29] Caltech (2023), “In a First, Caltech’s Space Solar Power Demonstrator Wirelessly Transmits Power in Space”, News releases, 01 June, https://www.caltech.edu/about/news/in-a-first-caltechs-space-solar-power-demonstrator-wirelessly-transmits-power-in-space.

[7] Carrington, D. (2023), “Revealed: 1,000 super-emitting methane leaks risk triggering climate tipping points”, The Guardian, 6 March, https://www.theguardian.com/environment/2023/mar/06/revealed-1000-super-emitting-methane-leaks-risk-triggering-climate-tipping-points.

[19] CNES (2022), “Conflict en Ukraine : impacts sur les relations spatiales russo-américaines”, 8 March, Centre national d’études spatiales, https://france-science.com/conflit-en-ukraine-impacts-sur-les-relations-spatiales-russo-americaines/ (accessed on 25 March 2022).

[17] CSA (2023), 2021 and 2022 State of the Canadian Space Sector Report, Canadian Space Agency, https://www.asc-csa.gc.ca/eng/publications/2021-2022-state-canadian-space-sector-facts-figures-2020-2021.asp.

[31] Eurospace (2022), Eurospace facts & figures: Key 2021 facts, https://eurospace.org/download/4176/.

[15] EuSPA (2022), EO and GNSS Market Report: 2022/Issue 1, European Space Agency, Publications Office of the European Union, https://www.euspa.europa.eu/sites/default/files/uploads/euspa_market_report_2022.pdf.

[12] Highfill, T., A. Jouard and C. Franks (2022), Updated and Revised Estimates of the US Space Economy, 2012-2019, US Bureau of Economic Analysis, https://www.bea.gov/system/files/2022-01/Space-Economy-2012-2019.pdf.

[23] Hollinger, P. (2023), Starship enterprise: the economics of Elon Musk’s bold bet, 26 April, https://www.ft.com/content/d6147eae-3493-4b70-bc5d-41610a680ebb.

[16] know.space (2023), Size and Health of the UK Space Industry 2022: Summary Report, Report commissioned by the UK Space Agency, https://www.gov.uk/government/publications/the-size-and-health-of-the-uk-space-industry-2022/size-health-of-the-uk-space-industry-2022#section4-6.

[32] Korean Ministry of Science and ICT (2022), Korea Space Industry Survey 2022, https://doc.msit.go.kr/SynapDocViewServer/viewer/doc.html?key=49048bc1634c402ab89bc3ae52958541&convType=html&convLocale=ko_KR&contextPath=/SynapDocViewServer/.

[22] NASA (2015), What are SmallSats ad CubeSats?, https://www.nasa.gov/content/what-are-smallsats-and-cubesats.

[35] NVCA (2023), NVCA Yearbook 2023, National Venture Capital Association, https://nvca.org/wp-content/uploads/2023/03/NVCA-2023-Yearbook_FINALFINAL.pdf.

[8] OECD (2023), Creditor Reporting System (CRS), OECD.stat (database), accessed on 24 April 2023, https://stats.oecd.org/Index.aspx?DataSetCode=CRS1.

[21] OECD (2023), Harnessing “New Space” for Sustainable Growth of the Space Economy, OECD Publishing, Paris, https://doi.org/10.1787/a67b1a1c-en.

[33] OECD (2023), “Main Science and Technology Indicators”, OECD Science, Technology and R&D Statistics (database), https://doi.org/10.1787/data-00182-en (accessed on 15 May 2023).

[41] OECD (2023), “Mobilising science in times of crisis: Lessons learned from COVID-19”, in OECD Science, Technology and Innovation Outlook 2023: Enabling Transitions in Times of Disruption, OECD Publishing, Paris, https://doi.org/10.1787/855c7889-en.

[27] OECD (2022), “Broadband database (Edition 2022)”, OECD Telecommunications and Internet Statistics (database), https://doi.org/10.1787/dc2d97f8-en (accessed on 25 May 2023).

[37] OECD (2022), Earth’s Orbits at Risk: The Economics of Space Sustainability, OECD Publishing, Paris, https://doi.org/10.1787/16543990-en.

[14] OECD (2022), OECD Handbook on Measuring the Space Economy, 2nd Edition, OECD Publishing, Paris, https://doi.org/10.1787/8bfef437-en.

[6] OECD (2020), The impacts of Covid-19 on the space industry, COVID-19 policy notes, Organisation for Economic Co-operation and Development, https://www.oecd.org/coronavirus/policy-responses/the-impacts-of-covid-19-on-the-space-industry-e727e36f/.

[3] OECD (2019), “Bringing space to earth with data-driven activities”, in The Space Economy in Figures: How Space Contributes to the Global Economy, OECD Publishing, Paris, https://doi.org/10.1787/07d50927-en.

[4] OECD (2019), Good Governance for Critical Infrastructure Resilience, OECD Reviews of Risk Management Policies, OECD Publishing, Paris, https://doi.org/10.1787/02f0e5a0-en.

[13] OECD (2019), The Space Economy in Figures: How Space Contributes to the Global Economy, OECD Publishing, Paris, https://doi.org/10.1787/c5996201-en.

[26] OECD (2017), “The evolving role of satellite networks in rural and remote broadband access”, OECD Digital Economy Papers, No. 264, OECD Publishing, Paris, https://doi.org/10.1787/7610090d-en.

[39] OECD (2014), “Intelligent Demand: Policy Rationale, Design and Potential Benefits”, OECD Science, Technology and Industry Policy Papers, No. 13, OECD Publishing, Paris, https://doi.org/10.1787/5jz8p4rk3944-en.

[20] OneWeb (2022), Annual report 2022, https://assets.oneweb.net/s3fs-public/2022-08/AnnualReport_2022.pdf.

[25] Pachler, N. et al. (2021), “An Updated Comparison of Four Low Earth Orbit Satellite Constellation Systems to Provide Global Broadband”, 2021 IEEE International Conference on Communications Workshops (ICC Workshops), https://doi.org/10.1109/iccworkshops50388.2021.9473799.

[24] Roberts, T. (2022), Space Launch to Low Earth Orbit: How Much Does It Cost?, 1 September, Center for Strategic and International Studies, https://aerospace.csis.org/data/space-launch-to-low-earth-orbit-how-much-does-it-cost/.

[1] Undseth, M. and C. Jolly (2022), “A new landscape for space applications: Illustrations from Russia’s war of aggression against Ukraine”, OECD Science, Technology and Industry Policy Papers, No. 137, OECD Publishing, Paris, https://doi.org/10.1787/866856be-en.

[40] Undseth, M., C. Jolly and M. Olivari (2021), “Evolving public-private relations in the space sector: Lessons learned for the post-COVID-19 era”, OECD Science, Technology and Industry Policy Papers, No. 114, OECD Publishing, Paris, https://doi.org/10.1787/b4eea6d7-en.

[36] Undseth, M., C. Jolly and M. Olivari (2020), “Space sustainability: The economics of space debris in perspective”, OECD Science, Technology and Industry Policy Papers, No. 87, OECD Publishing, Paris, https://doi.org/10.1787/a339de43-en.

[9] Union of Concerned Scientists (2023), UCS Satellite Database, 1 January 2023 version, data extracted 27 July 2023, https://www.ucsusa.org/resources/satellite-database.

[38] US Department of Commerce (2013), U.S. Space Industry ‘Deep Dive’: Final Dataset Findings, https://www.bis.doc.gov/index.php/space-deep-dive-results (accessed on 22 May 2017).

[10] US Space Force (2023), Space-track.org website, Data extracted 27 July, 18th Space Defense Squadron, https://www.space-track.org.

[2] Van de Ven, P. (2021), “Defining infrastructure”, OECD Statistics and Data Directorate, https://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=SDD/CSSP/WPNA(2021)1/REV1&docLanguage=En (accessed on 19 May 2022).

[28] Werner, D. (2022), “Competition is growing in the space-data-relay sector”, Space News, 13 September, https://spacenews.com/data-relay-networks/.