This compilation guide summarises the main steps to derive ERTR accounts in practice. The compilation guide covers the most important aspects of the OECD guidelines, and compilers are encouraged to consult the main document for a detailed description of the underlying concepts, definitions and principles. This practical compilation guide incorporates the insights gained during a feasibility study documenting the implementation of the guidelines [ENV/EPOC/WPEI(2018)6/REV1/ADD], and two rounds of data collection from OECD and interested non-OECD countries.

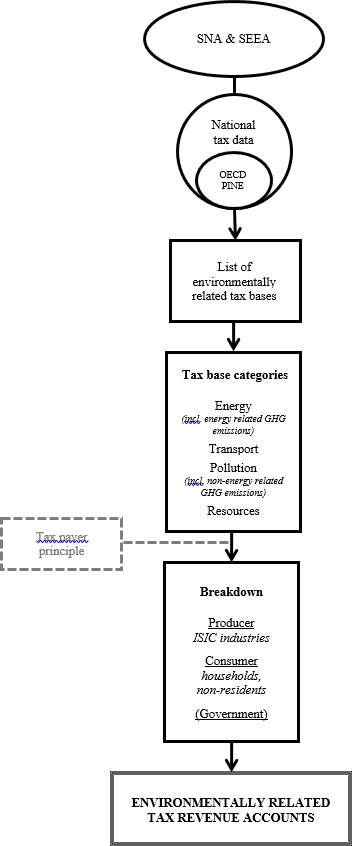

Figure B.1. illustrates the process underlying the compilation of ERTR accounts described in these guidelines. The ERTR accounts are broken down by industries using ISIC classifications, households, non‑residents and – optionally – the levels of government. The ERTR accounts apply the “tax payer” principle. At the same time, the ERTR accounts are also classified according to four tax base categories (energy, transport, pollution and resources) as well as two sub-categories (energy and non-energy related GHG emissions).

Compiling ERTR accounts according to these guidelines can be described chronologically as follows.

1. Compiling a general tax list:

Compile a general list of taxes that is consistent with the definition described in the SNA (see Section 2.1 for details). Such detailed tax lists will serve as a starting point to identify environmentally related taxes.

This exercise should be repeated every time the accounts are updated to ensure relevant changes are included.

Potential data sources: Use existing information on tax revenues reported in the national accounts, national tax lists from the Ministry of Finance, or information reported in the OECD Revenue Statistics.

2. Identifying environmentally related taxes:

Drawing on the general tax list and the list of environmentally related tax bases (see Table 1) identify taxes that are environmentally related and exclude all other taxes. All revenue from taxes levied on environmentally related tax bases should be reported as ERTR in the accounts.

Additionally, collect ERTR for certain land taxes, extraction taxes on oil and natural gas, resource rent taxes and elevated VAT, as described in Section 2.9.

For all taxes identified as environmentally related, include the detailed information at the tax base level, including tax rates, tax revenue, exemptions and the physical volumes underlying the ERTR.

Potential data sources: The identification of environmentally related taxes is likely to require additional information on the exact tax base, such as the tax legislation, detailed information from the Ministry of Finance or sub-national agencies. This information is necessary to distinguish whether (or not) specific taxes are levied on environmentally related tax bases. Additionally, information reported in the OECD PINE database could be consulted.

3. Allocating ERTR to tax base categories:

Based on tax-specific information, classify ERTR according to four base tax categories (energy, transport, pollution, and resources) and the two sub-categories (energy and non-energy related GHG emissions) (see Table 1 for details).

If an ERTR spans across several tax base categories, the ERTR should be split according to an allocation key reflecting the relative contribution of each tax base category to the total ERTR of the categories involved in the split. If such split is not possible, the allocation could be done according to the category most aligned with the tax.

Potential data sources: For this step, tax-specific information on the tax base could be used, similar to the previous step. Once the exact tax base is identified, the allocation to the four tax base categories and the two sub-categories can directly be made in line with Table 1.

4. Allocating ERTR to industries, households and non-residents:

Using tax-specific information on the tax bases, allocate ERTR to ISIC industries, households and non-residents.

Generally, the allocation to industries, households and non-residents is based on the “tax payer” principle, i.e. the final user of the tax base (Sections 2.4 and 2.5).

Potential data sources: This step is likely to be country and tax-specific. Nevertheless, supply-use tables in the national accounts that allow identifying the use of the exact tax base or firm-level data on the use of the tax base can support the allocation of ERTR to ISIC industries, households and non-residents. Similarly, vehicle registries, fuel purchases, VAT registers, among others, could be used for individual taxes. Sometimes detailed firm-level data (e.g., data from government bodies collecting the tax) are available to support the allocation, in particular when a tax base is used by multiple industries. The identification of the final user of energy-related tax bases could be based on information provided by energy flow accounts and statistics on gross fixed capital formation and household final consumption expenditure on vehicles from the national accounts for transport taxes. For non-resident ERTR from fuel taxes, for instance, ratios between resident/non-resident breakdown of physical consumption from the energy account could be used. For products subject to ERT, these ratios are used to split the original fuel excise tax estimate between resident and non-resident liabilities.

5. Allocating ERTR across calendar years:

Allocate ERTR to the calendar year in which the liability for these taxes arises, i.e. applying the accrual principle (Section 2.7). In case it is not possible to apply the accrual principle, countries can report on a cash basis. However, this should be made explicit in the ERTR accounts.

Potential data sources: Since the tax revenue recorded in the national accounts should already follow the accrual principle, the allocation of ERTR across years can – in most cases – be done by directly using the information provided in national accounts. For the more challenging cases related to emission permits, additional data sources for firm-level activities might be required.

6. Optional: Allocating ERTR to levels of government:

Split the ERTR according to three levels of government whose budget is replenished by environmentally related taxes (Section 2.8), namely (i) central, (ii) state, (iii) and local.

Potential data sources: Existing data reported in the OECD Revenue Statistics could be an adequate starting point for making the distinction between different levels of government. Additionally, information provided by the finance ministry or sub-national agencies could be used.