In terms of the Financial Account information collected and sent by Belize, it was found to include a much lower proportion of Tax Identification Numbers with respect to the individuals associated with the accounts when compared to most other jurisdictions. Furthermore, while the collection and reporting of dates of birth is generally higher across jurisdictions, Belize nevertheless reported a much lower rate of collection of dates of birth when compared to other jurisdictions. These are key data points for exchange partners to effectively utilise the information. Follow-up discussions confirmed that Belize is aware of these issues and is taking steps to address them. Belize confirmed that no undocumented accounts were reported by Reporting Financial Institutions.

Feedback was also received from Belize’s exchange partners indicating that, compared to what they generally experience in relation to the information received from all of their exchange partners, they achieved a relatively lower level of success when seeking to match information received from Belize with their taxpayer database.

Based on these findings it was concluded that Belize is not meeting expectations in ensuring that Reporting Financial Institutions correctly conduct the due diligence and reporting procedures, including by having in place the required administrative compliance framework and related procedures. More specifically, fundamental issues have been identified, including with respect to implementing a comprehensive compliance strategy in order to address issues of non-compliance by Reporting Financial Institutions and carrying out verification and enforcement activities. Belize should therefore continue its implementation process accordingly, including by addressing the recommendations made.

Recommendations:

Belize should further develop and implement its overarching compliance plan to underpin its compliance activities, including by ensuring it is informed by a risk assessment that takes into account a wide range of relevant information sources and that it includes monitoring the interaction of its CRS and AML frameworks to ensure the identification of Controlling Persons is always in accordance with the AEOI Standard.

Belize should develop and implement effective procedures to identify its population of Reporting Financial Institutions, specifically including non-regulated entities that are Financial Institutions for the purposes of the AEOI Standard.

Belize should implement effective verification mechanisms, including the inspection of the records maintained by Reporting Financial Institutions, to ensure they are effectively implementing the due diligence and reporting obligations. Reference is made to the recommendations made when assessing Belize’s legal framework implementing the AEOI Standard.

Belize should ensure it has effective enforcement mechanisms to address non-compliance by Reporting Financial Institutions, including appropriate penalties and sanctions applicable to non-compliance with any of the obligations (e.g. due diligence, reporting, record keeping).

Belize should establish and implement a clearly defined procedure to monitor and verify whether self-certifications have been obtained as required. Reference is made to the recommendations made when assessing Belize’s legal framework implementing the AEOI Standard.

Belize should implement systems to collect and monitor information on the reporting of undocumented accounts to inform its compliance strategy.

Belize should put in place a clearly defined policy that, where circumvention is identified, action is taken to address it.

SR 1.6 Jurisdictions should collaborate on compliance and enforcement. This requires jurisdictions to:

use all appropriate measures available under the jurisdiction’s domestic law to address errors or non-compliance notified to the jurisdiction by an exchange partner; and

have in place effective procedures to notify an exchange partner of errors that may have led to incomplete or incorrect information reporting or non-compliance with the due diligence or reporting procedures by a Reporting Financial Institution in the jurisdiction of the exchange partner.

It should be noted that, as Belize exchanges information on a non-reciprocal basis and does not therefore receive information, it is not required to have in place procedures to notify its exchange partners. SR 1.6 b) has therefore not been assessed in this case.

Findings:

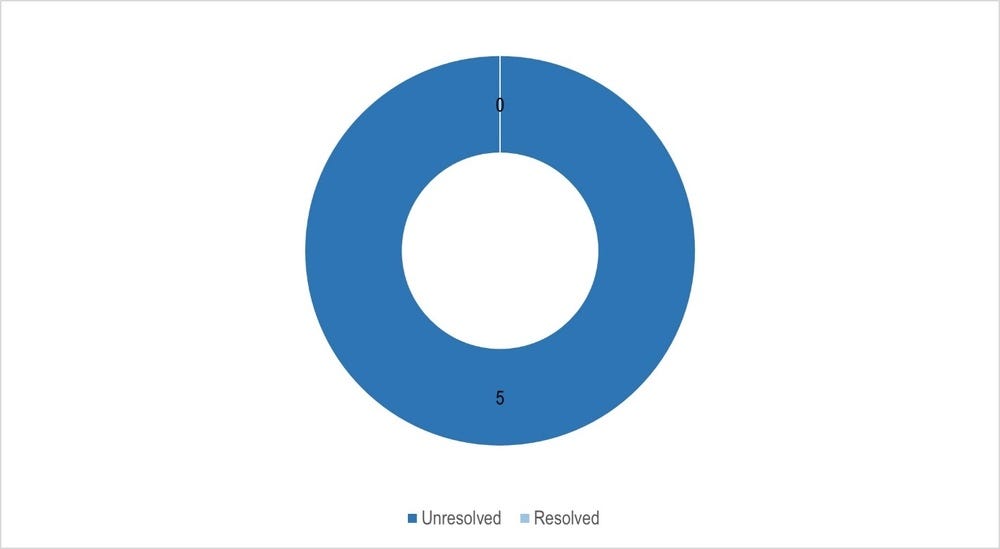

Belize has an understanding of its obligation to collaborate on compliance and enforcement in relation to issues notified to them (i.e. under Section 4 of the MCAA or equivalent). While no such notifications have yet been received, it has also not yet developed the necessary systems and procedures to be ready to process them as required.

Based on these findings it was concluded that Belize is partially meeting expectations in relation to collaborating with its exchange partners to ensure that Reporting Financial Institutions correctly conduct the due diligence and reporting procedures. More specifically, significant issues have been identified, including with respect to a lack of a documented procedure in cases where notifications are received from an exchange partner. Belize should therefore continue its implementation process accordingly, including by addressing the recommendation made.

Recommendations:

Belize should put in place documented procedures to address errors or non-compliance notified by an exchange partner.