This chapter takes stock of policies and practices underpinning the remuneration of executive managers of SOEs across countries. It takes stock of executive remuneration levels and pay packages, and explores the extent to which the state as an owner influences the board of directors’ autonomy to decide on managerial remuneration and incentives. The chapter also presents good transparency and disclosure practices.

Remuneration of Boards of Directors and Executive Management in State-Owned Enterprises

3. Remuneration schemes applicable to executive management of SOEs

Abstract

3.1. Introduction

Managerial remuneration in SOEs straddles the spheres of corporate and public sector governance. On one hand, adequate remuneration levels are crucial for attracting competent executive managers in SOEs and to incentivise them in accordance with the interests of the owners. On the other hand, for political and societal reasons care must be taken to avoid setting these at a level perceived by the general public as being too high. The SOE Guidelines imply that care should be taken to ensure that the state owners do not infringe on the boards’ role in determining managerial salaries. If the state wishes to influence this, general rules should be established and/or owners’ expectations regarding remuneration should be communicated to the boards through the usual channels of control.

Main findings

Remuneration levels, policies and practices

Practices regarding executive remuneration vary significantly across countries. In countries facing specific political or fiscal constraints, remuneration is generally prescribed by law or by separate government decision, with levels standing (sometimes significantly) below the average of SOEs in other countries, as well as lower than market levels in the domestic economy. On the other hand, in countries where remuneration is set at the full discretion of the board, levels are generally higher – sometimes explicitly based on private sector benchmarks.

Regardless of the way in which remuneration policies are established, average CEO remuneration is twice as high in commercially oriented SOEs as in public policy-oriented SOEs, except in countries where levels are set by law. In many countries, the disparity between remuneration levels of CEOs of large SOEs and small SOEs is also significant. Some outliers exist in some sectors, for instance the air transport sector, where caps may have been derogated in order to accommodate generally high sectoral pay levels. Unsurprisingly, the remuneration of the CEO is generally higher than the remuneration of other executive managers. In some cases, the differences actually seem to be smaller than might have been expected in the private sector.

The majority of countries hire executive managers on fixed-term contracts, while only eight countries exclusively hire executive managers – including both the CEO and other members of the management board – on continuous contracts with terms for termination, like in the private sector. In these countries, the boards also set remuneration levels at their full discretion, similar to private sector practices. In six countries, both contractual relationships are possible.

Remuneration components

Pay packages of executive managers usually include an annual fixed salary (which can be based on the consumer price index or set as a multiple of the average nominal wage), allowances, fringe benefits and payments to the pension plan, and can also include severance payments. Stock options are not allowed in all but two countries.

In all but five of the surveyed countries, executive managers’ pay packages also include a performance‑based component, which is capped by the government owner in more than half of surveyed countries, either at the absolute level (in around one‑fifth of countries), or at a percentage of the fixed remuneration component (in around four‑fifths of countries).

While limited information is available regarding how performance is benchmarked since these key performance indicators are mostly set at the full discretion of the board (sometimes upon recommendations of the remuneration committee) and not by government – and thus vary across companies, many countries mention that performance is benchmarked against profitability relative to other companies and compared to the previous year. In many countries, performance of the CEO is also benchmarked against both corporate (SOE‑level) and individual performance indicators. Financial and non-financial indicators can be both qualitative and quantitative.

Transparency and disclosure practices

In all but two countries, SOEs are required to disclose information on the remuneration levels of executive managers to the general public, along with the remuneration policy including details of the bonus schemes in many countries. In some countries, disclosure requirements apply only for the remuneration of the CEO and/or only in the case of listed companies. In some countries, some SOEs also disclose disaggregated information on the fixed and variable remuneration components. While SOEs are mainly required to disclose this information in their annual reports or websites, a separate remuneration report is required to be prepared by the company or the remuneration committee in two countries.

By contrast, the state or ownership entity does not disclose information on executive remuneration in almost half of the surveyed countries, mainly because individual SOEs are already required to do so. In the 15 countries where the government does disclose granular information, this is mainly done through a central government portal, or the government or ownership entity’s annual report on SOEs.

3.2. Actual remuneration levels of executive managers according to SOE corporate characteristics

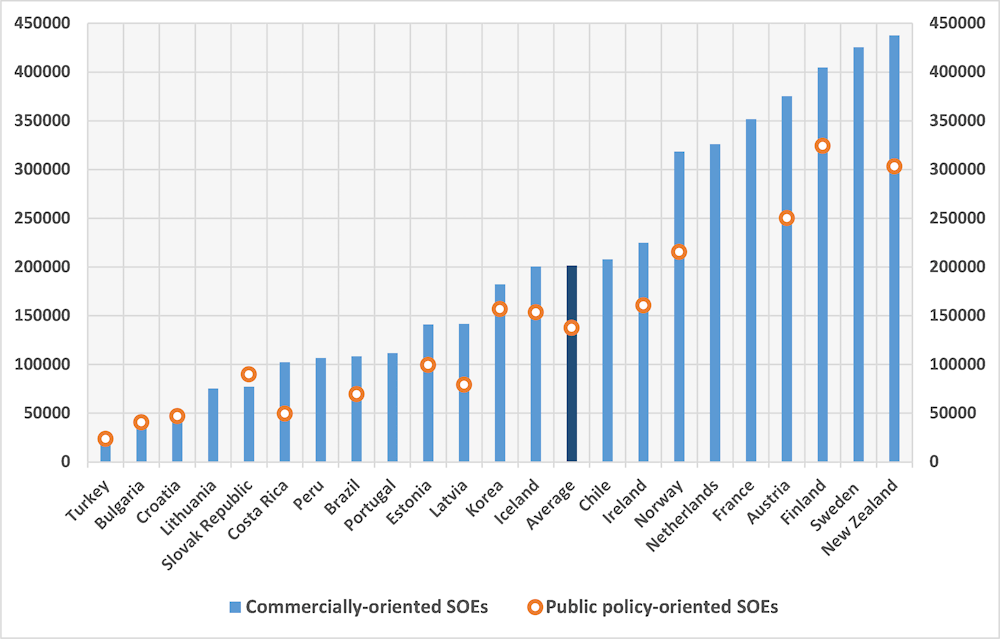

Similar to trends regarding board remuneration, CEOs of public policy-oriented SOEs receive lower annual nominal compensation (USD 137 452 on average, representing approximately 5 times the amount of average annual national wages of production workers) than CEOs of commercially oriented SOEs (USD 201 635 on average, representing almost seven times the amount of the average annual national wages of production workers). Croatia and Turkey stand as exceptions, as remuneration levels are prescribed by law (Figure 3.1). The three countries which set the highest annual nominal wages for CEOs of commercially oriented SOEs in absolute terms (New Zealand, Sweden, Finland) also remain above average when remuneration levels are captured as a multiple of average annual national wages (Figure 3.2).

Relatively high remuneration levels in New Zealand can be explained by the fact that unlike other countries in the figure, data includes both fixed and variable remuneration components, in addition to the fact that bonuses granted to executive managers of commercially oriented SOEs are not capped, and defined at the full discretion of the board. In Sweden, although remuneration levels are relatively high compared to other countries, evidence suggests that levels are above medium market levels for small SOEs but below market levels for large SOEs (Swedish Government, 2021[1]). This may be due to the fact that pay packages of executive managers do not include a performance‑related component. Anecdotal evidence also suggests that this has hampered recruitment, with CEO prospects turning down offers in some instances.

Figure 3.1. Average annual remuneration of CEOs of SOEs (fixed remuneration only, in USD as of 2020)

Note: Data covers executive remuneration of SOEs with a state shareholding of at least 50%, which are not listed on the stock exchange, except for Chile where data includes one listed SOE (ZOFRI), albeit with remuneration levels similar to those of non-listed SOEs. Data includes fixed remuneration only, except for Brazil, Estonia, Finland, Latvia, the Netherlands and New Zealand where both fixed and variable remuneration are included. In Chile, France, the Netherlands, Peru, Portugal and Sweden, all SOEs are classified as commercially oriented. See Annex C for details.

Source: Author, based on questionnaire responses, and calculations using the OECD database (https://data.oecd.org/earnwage/average‑wages.htm) and ILOSTAT database (https://ilostat.ilo.org/topics/wages/).

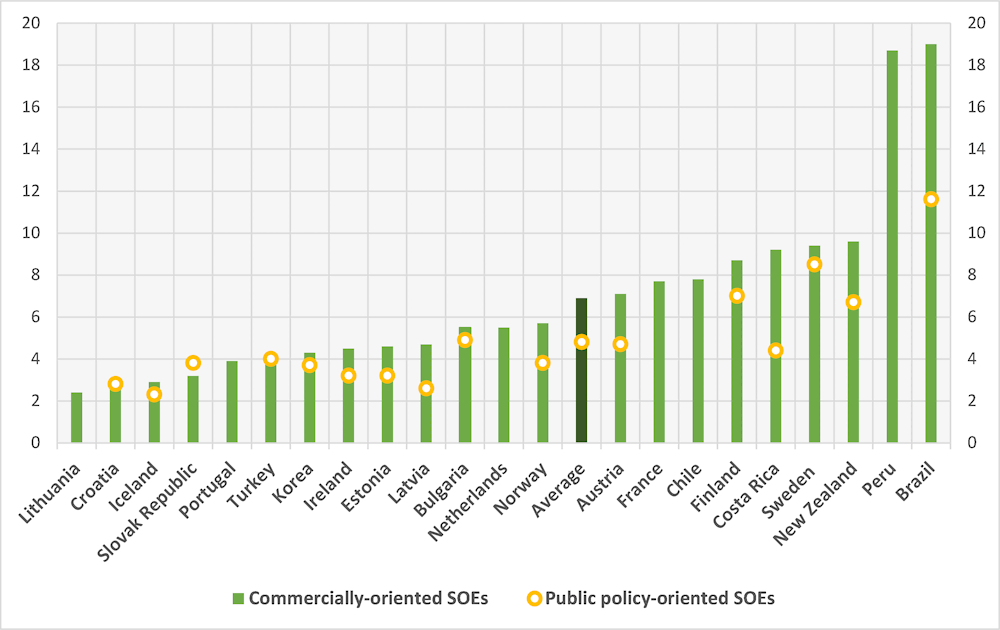

Similar to trends on board remuneration, high executive remuneration levels displayed as a percentage of average annual national wages in Brazil and Peru can likely be explained by low average nominal wages in these countries and the need to set remuneration levels at a high threshold in order for them to remain competitive with private sector peers. Besides, in Brazil, unlike other countries in the figure, data includes both the fixed and variable remuneration components. The latter can vary from 16% to 100% of the fixed remuneration depending on the company size and sector of operation.

In many countries, the disparity between remuneration levels of CEOs of large SOEs and small SOEs is also significant. For instance, CEO remuneration of large SOEs is equal to 3.6 times the remuneration amount of CEOs of small SOEs in Austria, 5.2 times the amount in Latvia, and 5.6 times in the Netherlands. This may be due to outliers in the air transport sector. For instance, in New Zealand, the remuneration of the CEO of one large commercially oriented SOE amounts to NZD 4 500 000. Other countries report that higher remuneration tends to be offered to executives of SOEs operating in the financial sector (Brazil, Colombia, Iceland, Norway, United Kingdom), energy sector (Brazil, Colombia, the Czech Republic, Greece, New Zealand), water sector (Greece) and health sector (Portugal). These cases may be explained by the fact that caps may have been derogated in order to accommodate generally high sectoral pay levels.

While limited data is available on the remuneration levels of chief financial officers (CFOs) and chief operating officers (COOs) across countries, evidence suggests that the remuneration of CEOs is generally higher than the remuneration of other executive managers, albeit not significantly in most cases.

Figure 3.2. Average annual remuneration of CEOs of SOEs (fixed remuneration only, as a multiple of average annual national wages)

Note: Data covers executive remuneration of SOEs with a state shareholding of at least 50%, which are not listed on the stock exchange, except for Chile where data includes one listed SOE (ZOFRI), albeit with remuneration levels similar to those of non-listed SOEs. Data includes fixed remuneration only, except for Brazil, Estonia, Finland, Latvia, the Netherlands and New Zealand where both fixed and variable remuneration are included. In Chile, France, the Netherlands, Peru, Portugal and Sweden, all SOEs are classified as commercially oriented. See Annex C for details.

Source: Author, based on questionnaire responses, and calculations using the OECD database (https://data.oecd.org/earnwage/average‑wages.htm) and ILOSTAT database (https://ilostat.ilo.org/topics/wages/).

In terms of comparison with private sector levels, some countries report that the remuneration of executives is comparable to private sector peers, especially in countries where the board is responsible for setting remuneration levels – sometimes based on private sector benchmarks (Estonia, Finland, New Zealand, Norway, the Slovak Republic, United Kingdom), or where it is provided by cabinet decision that remuneration levels must correspond to the first quartile of the market (Chile). However, similar to the remuneration levels of board members, many countries also report that the remuneration of executive managers stands below market levels (Costa Rica, Croatia, France, Greece, Ireland, Israel, Latvia, Spain) especially for executives of medium-sized and small SOEs (Iceland, Lithuania).

While this is mainly due to government-imposed caps on remuneration, some countries report that these have hampered recruitment. For instance, in Costa Rica, freezes of chief executive wages and the establishment of remuneration caps have reportedly “degraded” the institutional salary scale in absolute terms and created “inverted” gaps between senior managers and the rest of the administration, while also hampering recruitment by preventing SOEs from using market research-based remuneration practices. In Greece, the lower remuneration levels of executives of SOEs subjected to remuneration caps implemented during the 2008 global financial crisis reportedly hampers recruitment. As such, differentiated remuneration rules for executives of “large” SOEs (with more than 3 000 employees and EUR 100 million of annual turnover) were introduced in 2015 in order to facilitate the recruitment of qualified professionals. In Belgium, it is reported that the cap on the basic remuneration of SOEs’ CEOs has led some executives to leave the company when it was introduced.

On the other hand, uncapped and “competitive” remuneration levels of executive managers can be perceived as being unreasonably high, and thus can spur public controversy. For instance, in Norway, media coverage of SOEs focuses on remuneration levels of executives being too high. In Lithuania, although remuneration levels of SOEs’ CEOs are moderate compared to market levels, the remuneration levels of senior civil servants are usually lower than those of the CEOs of large and medium-sized SOEs, which are thus perceived as excessively high. Likewise, in the United Kingdom, although remuneration is well below industry equivalents, senior pay is often very high compared to the average national wage, resulting in remuneration being often subject to public scrutiny and controversy, especially following the award of large bonuses.

3.3. Remuneration policies and practices

The SOE Guidelines state that the remuneration of both SOE boards and executive management should be aligned with the long-term interest of the enterprise. Concerning the executive management, the SOE Guidelines further offer that boards should “decide, subject to applicable rules established by the state, on the compensation of the CEO” (annotations to Chapter VII, point B).

3.3.1. Remuneration models

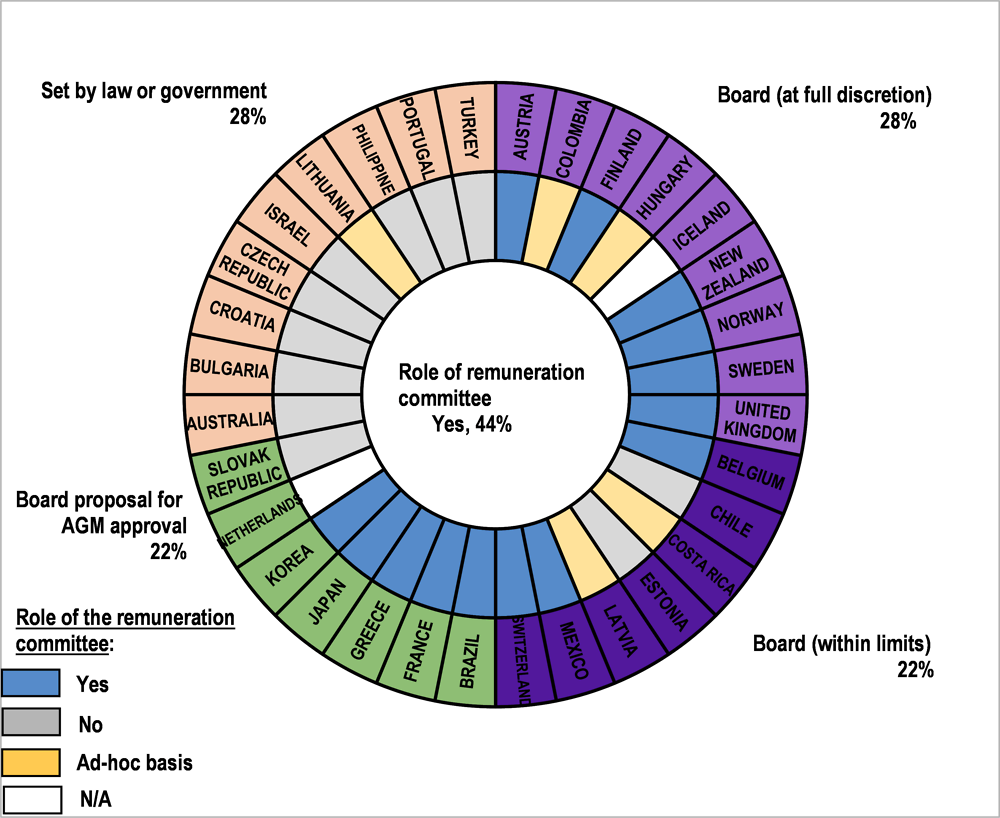

In 16 of the 34 surveyed countries with available information, remuneration policies and levels applicable to executive managers are set by the boards, either at their full discretion (in nine countries), or within overall limits set by government (in seven countries). In three of these countries, while the remuneration of the CEO is decided by the board, the remuneration levels of the rest of the executive managers are either decided by the CEO (Norway,1 Sweden), or decided by the board based on the CEO’s proposal (United Kingdom).

In another seven countries, remuneration is proposed by the boards and submitted to the AGM for approval on the limits. In some of these countries, after limits have been set, the supervisory board decides in a discretionary manner on the actual remuneration levels of the members of the executive board (France, Japan, the Netherlands). On the other hand, in nine of the surveyed countries, remuneration levels of executive managers are either set by law, or by the government against public sector wage grids (Figure 3.3). It should be noted that some countries fall into several categories, as different policies and practices apply to SOEs depending on their corporate form, share of state ownership and/or commercial and non-commercial orientation (Austria, Colombia, Costa Rica, Greece, Ireland, Switzerland). Detailed information on individual national practices is provided in Table 3.3.

Overall, the remuneration committee does systematically play, or can play, a role in setting the remuneration levels of executive managers in 14 of the surveyed countries, mainly including those where the remuneration levels are set by the board.

Figure 3.3. Remuneration policies and practices for executive managers of SOEs

Note: Data unavailable for Peru and Spain. In Germany and Ireland, processes respectively differ according to the corporate form of SOEs and their orientation. See Table 3.3 for details.

Source: Author, based on questionnaire responses and desk research.

3.3.2. Contractual relationships of executive managers

The majority of countries hire executive managers on fixed-term contracts, while only eight countries exclusively hire executive managers – including both the CEO and other members of the management board – on continuous contracts with terms for termination, like in the private sector. In these countries, the boards also set remuneration levels at their full discretion, similar to private sector practices. In six countries, both contractual relationships are possible. For instance, in Costa Rica, Ireland and the Slovak Republic, CEOs are hired on fixed-term contracts, but the rest of the executive managers are offered continuous contracts with terms for termination (Table 3.3).

3.3.3. Remuneration components

The SOE Guidelines state that boards “should ensure that the CEO’s remuneration is tied to performance and duly disclosed”. They further posit that “compensation packages for senior executives should be competitive, but care should be taken not to incentivise management in a way inconsistent with the long term interest of the enterprise and its owners. The introduction of malus and claw-back provisions is considered a good practice…” (annotations to Chapter VII, point B). This effectively recommends the inclusion of a performance‑related element in executive managers’ pay packages.

Overall, in almost all countries, the remuneration packages of SOE executive managers include a performance‑based component. While limited information is available regarding the other components of pay packages of executive managers, evidence suggests that pay packages usually include an annual fixed salary (which can be based on the consumer price index, such as in Israel, or as a multiple of the average nominal wage, such as in the Slovak Republic), allowances, fringe benefits and payments to the pension plan, and can also include severance payments. Stock options are usually not allowed, except in Switzerland, and for partially listed companies in New Zealand. In the Philippines, executive managers of SOEs are subject to the remuneration scheme applicable to National Government Agencies.

Variable remuneration

In almost all of the surveyed countries (85%), the remuneration packages of executive managers include a performance‑based component. In four of the five countries where it is not granted (Hungary, Iceland, Sweden, Turkey), other forms of benefits exist. In Ireland, performance‑related awards (PRAs) granted to CEOs of both commercial and non-commercial state bodies were suspended in 2009 in the context of the global economic downturn, and have not been reintroduced since.

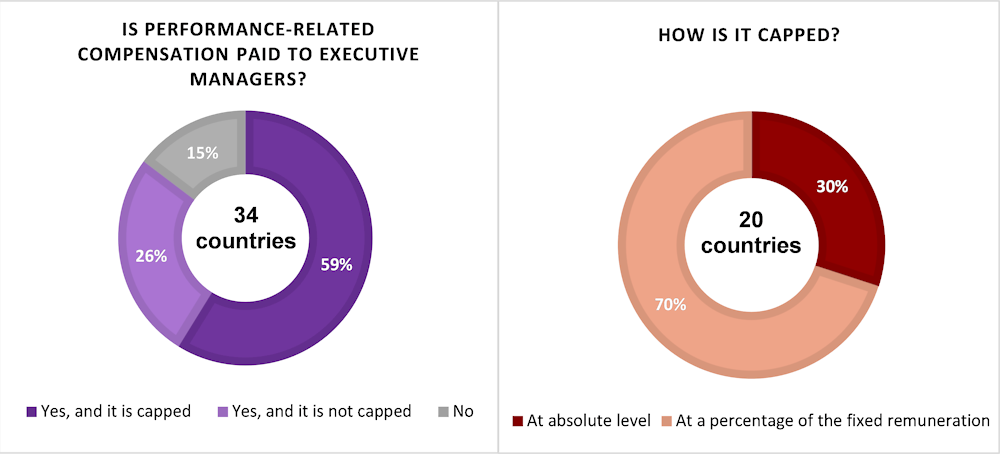

Among the 29 surveyed countries that grant performance‑related compensation to executive managers, this variable component is capped by the state owner in all but nine countries (Austria, Belgium, Costa Rica, Croatia, Japan, Mexico, New Zealand, Switzerland, United Kingdom). In Austria, while there are no formal caps, performance‑related compensation is determined by the chair of the board in co‑ordination with the shareholding ministry. In Belgium, no government caps exist, but variable remuneration can be capped at the SOEs’ discretion. In New Zealand, while there are not caps for commercially oriented SOEs – which are determined at the full discretion of the board – no discretionary bonuses are granted to CEOs of public policy-oriented SOEs. In Switzerland, while no caps on remuneration currently exist, the issue is a subject of ongoing debates in parliament.2 It should also be noted that in Costa Rica and Croatia, only two SOEs in each country pay performance‑related compensation to executives, as executive remuneration in these countries is subject to a unified salary system set by law.

Among the 20 countries that cap performance‑related compensation, one‑third cap it at the absolute level, while the remaining 70% cap it at a percentage of the fixed remuneration (Figure 3.4). Overall, different approaches exist across countries for capping performance‑based compensation (Table 3.1).

Figure 3.4. Performance‑related remuneration component of executive managers of SOE

Note: Information unavailable for Peru and Spain.

Source: Author, based on questionnaire responses.

Table 3.1. Selected approaches for capping performance‑related compensation of executives of SOEs

Source: Author, based on questionnaire responses.

While limited information is available regarding how performance is benchmarked since these key performance indicators (KPIs) are mostly set at the full discretion of the board (sometimes upon recommendations of the remuneration committee) and not by government – and thus vary across companies, many countries mention that performance is benchmarked against profitability relative to other companies and compared to the previous year. In many countries, performance of the CEO is also benchmarked against both corporate (SOE‑level) and individual performance indicators. Financial and non-financial indicators can be both qualitative and quantitative.

In some countries, KPIs are set by government or shareholding ministers. In New Zealand, for state‑owned enterprises and crown entities (falling under the respective legislative frameworks of the same names), performance is benchmarked against the targets set in the Statement of Corporate Intent and Statement of Performance Expectations (respectively). These are documents that comprise annual, publically accountable, key performance indicators and are approved by shareholding and responsible ministers before the start of each financial year. In Korea and the Philippines, guidance and criteria for eligibility to performance‑based remuneration are set by law (Box 3.1). In Switzerland, while the board is responsible for setting detailed KPIs, Article 8 of the ordonnance sur la rémuneration provides general guidance by stating that “bonuses are generally based on the average performance over at least two years and are increased or decreased accordingly. Both financial and qualitative criteria shall be applied as assessment criteria”.

Box 3.1. Criteria and methods for evaluating the performance of executive managers of SOEs in Korea and the Philippines

Korea

According to Article 48 of the Act on Management of Public Institutions, the criteria and methods for the evaluation of management performance should be prescribed by the Minister of Economy and Finance through deliberation and resolution by the Steering Committee, in such a manner that the following matters should be included in the evaluation of a public corporation or quasi-governmental institution:

1. The rationality and achievement level of management goals

2. The public nature and efficiency of major projects

3. The adequacy of organisational and personnel management, including types of employment of employees

4. Soundness in financial management and budget-saving efforts, including the implementation of the mid- and long-term financial management plan established under Article 39‑2

5. Results of the customer satisfaction survey conducted under Article 13 (2)

6. Operation of a rational performance‑based payment system

7. Other matters related to the management of the public corporation or quasi-governmental institution.

Financial and non-financial performance targets and indicators are newly determined each year by the consultation of the Ministry of Economy and Finance, the evaluation team for the management of public corporations and quasi-governmental institutions, and SOEs subject for evaluation.

According to Article 27 of the Enforcement Decree of the Act on the Management of Public Institutions, the Minister of Economy and Finance shall prepare a manual for the management performance evaluation before the beginning of each fiscal year, and may, after deliberation and resolution by the Steering Committee, take follow-up measures, such as making suggestions or demands concerning personnel or budgetary actions, or deciding on the piece rate.

Philippines

Eligibility for the performance‑based bonus (PBB) is anchored on both the performance of the SOE and of the individual executive manager. Certain eligibility requirements are set by GCG M.C. No. 2019‑02, as detailed below:

Table 3.2. Eligibility criteria for performance‑based compensation in the Philippine

Source: Author, based on country responses to the OECD questionnaire.

Table 3.3. Remuneration policies and practices for executive managers of SOEs across 34 jurisdictions

Notes: Data unavailable for Peru and Spain. On role of board committees in setting remuneration levels:● = yes; ❍ = no; = ad-hoc basis. On contractual relationships of executive managers: ■ = fixed-term contracts; = open-ended contracts; ♦ = both possible.

1 In Australia, although board committees do not play a role, boards are consulted on an annual basis.

2 In Brazil, a “People Committee” was recently established in all SOEs to advise the board on human resources management issues, including executive remuneration.

3 In Greece, the remuneration committee plays a role in listed SOEs only.

4 In Ireland, the remuneration committee plays a role with regard to the remuneration of executive managers below CEO level in commercial state bodies only. In addition, while CEOs are hired on fixed-term contracts, other executive managers are usually hired on continuous contracts with terms for termination.

5 In Latvia, the role of the remuneration committee is mandatory for listed SOEs, but is not widespread practice for other SOEs.

6 In Lithuania, only three SOE boards have a remuneration committee.

7 In Mexico, fixed-term for PEMEC, open-ended for civil servants as executive manager (CFE).

Source: Author, based on questionnaire responses and desk research.

3.4. Transparency and disclosure practices

On the issue of transparency and disclosure, the SOE Guidelines observe that “[i]t is important that SOEs ensure high levels of transparency regarding the remuneration of board members and key executives. Failure to provide adequate information to the public could result in negative perceptions and fuel risks of a backlash against the ownership entity and individual SOEs. Information should relate to actual remuneration levels and the policies that underpin them” (annotations to Chapter VI, Point A). It indicates that it is considered in the interest of ownership entities to opt for maximum transparency, even at the risk of spurring public anger by disclosing pay levels that may be considered as excessive.

3.4.1. Disclosure practices by SOEs

In all but two countries (Turkey and Colombia)3, SOEs are required to disclose information on the remuneration levels of executive managers to the general public. In many countries, SOEs also disclose the remuneration policy applicable to executive managers, including some details of the bonus schemes and key performance indicators underpinning the calculation of the variable remuneration amount (e.g. Australia, Belgium, United Kingdom). In Latvia, while SOEs were previously only required to publish the principles of their remuneration policy, since January 2020, majority-owned SOEs are required to disclose remuneration levels of individual executive managers.

In some countries, different requirements apply depending on the legal form, share of state ownership, orientation and size of the company. For instance, in the Czech Republic, granular information on the remuneration of each executive manager is required to be disclosed by listed SOEs only, while non-listed SOEs are only required to disclose general information in their annual reports. In Israel, only listed and “non-profit” companies are required to disclose this information. In the Netherlands, while the Dutch Corporate Governance Code is only mandatory for listed companies, and prescribes that the remuneration of executive managers be published on the SOE’s websites, all SOEs comply. In Croatia, similar to provisions applicable to supervisory boards, listed SOEs are required to disclose the remuneration of individual executive managers and of the entire management board, in addition to the remuneration policy. Unlisted SOEs have not such obligation.

In New Zealand, while there are no legally binding disclosure requirements for SOEs, since 2019, the government expects commercially oriented SOEs to disclose the remuneration of the CEO and CFO, in an effort to align SOE practices with the provisions applicable to listed companies. In addition, according to Section 211 (1)(g) of the Companies Act 1993, all SOEs and listed companies are legally required to publicly disclose the number of employees which are paid more than NZD 100 000 (New Zealand dollars). Likewise, In the United Kingdom, while SOEs are required to disclose information on executives in their annual report, for those not classified as “public corporations” there is also a requirement to disclose the base remuneration of all employees earning a base salary of more than GBP 150k.

In Ireland, the Code of Practice for the Governance of State Bodies sets out that commercial state bodies, in addition to disclosing the aggregate pay bill and total number of employees, should publish details on the number of employees whose total employee benefits (excluding employer pension costs) for the reporting period fell within each band of EUR 25 000 from EUR 50 000 upwards and an overall figure for total employer pension contributions in their annual report and/or financial statements.

This information is most often required to be disclosed by SOEs in their annual reports or on their websites, but in some countries, a separate remuneration report is required. For instance, in Belgium, the remuneration committee is required by law to produce a report on the remuneration of the members of the executive committee, which is included in the annual report. In Sweden, SOEs have to prepare a remuneration report, like listed limited liability companies as per the Companies Act and Annual Accounts Act, disclosing the remuneration of executive managers and accounting how the government’s principles for remuneration and other terms of employment have been applied. A similar requirement to prepare a remuneration report has been imposed on non-small SOEs in Norway effective from 2023. Further, according to the Accounting Act, all companies that are not small shall report the aggregate salary provided to the CEO.

While SOEs are only required to disclose the remuneration of the CEO in some countries (Iceland, Lithuania), in other countries, disclosure is divided between CEO remuneration and remuneration of the rest of the management team on an aggregate basis (Australia, Belgium, Finland). In some countries, some SOEs also disclose disaggregated information on the fixed and variable remuneration components, and the weight of each part in the overall pay packages of the CEO and other executive managers (Estonia, Belgium).

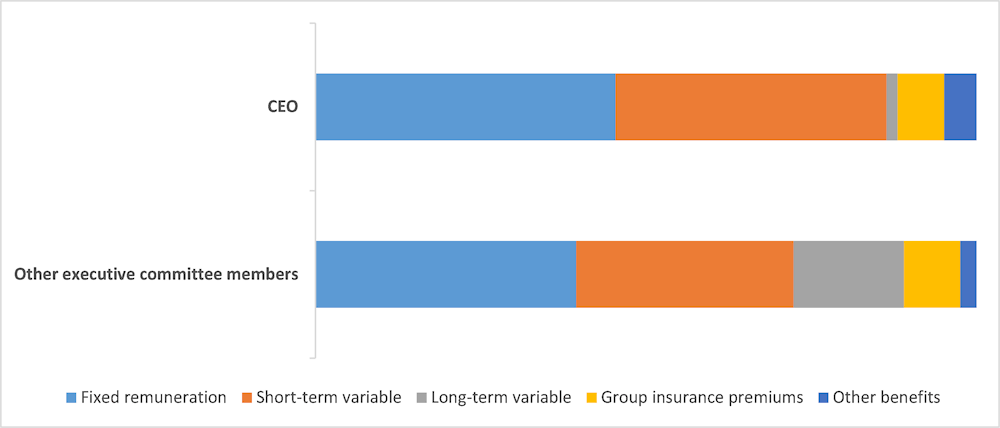

Box 3.2. Example of granular disclosure on executive remuneration by a Belgium SOE (Proximus)

In its integrated annual report, Proximus provides a general overview of the remuneration allocated to the members of the Executive Committee over the last five years, with disaggregated information on each remuneration component, split between pay packages of the CEO and the other members of the Executive Committee.

Table 3.4. Remuneration overview of the CEO

Source: Proximus Group (2020), Integrated Annual Report 2020, https://www.proximus.com/annualreport2020.html.

Table 3.5. Remuneration overview of the other members of the Executive Committee

Source: Proximus Group (2020), Integrated Annual Report 2020, https://www.proximus.com/annualreport2020.html.

Proximus also discloses the weight of each remuneration component in the overall pay packages of the CEO and rest of the executive committee in a given year.

Figure 3.5. Relative importance of the various components of the remuneration effectively allocated in 2020 before employer’s social contribution

Source: Proximus Group (2020), Integrated Annual Report 2020, https://www.proximus.com/annualreport2020.html.

In Colombia, while SOEs are not required to disclose information on the remuneration levels or policy, SOEs are encouraged by the ownership entity to disclose this information, especially for companies where the President appoints a public official as executive manager. In the Slovak Republic, only joint stock companies and state enterprises are required to disclose remuneration information on an aggregate basis. While the law provides for levels to be disclosed upon request, it is reported that in practice, SOEs rarely comply.

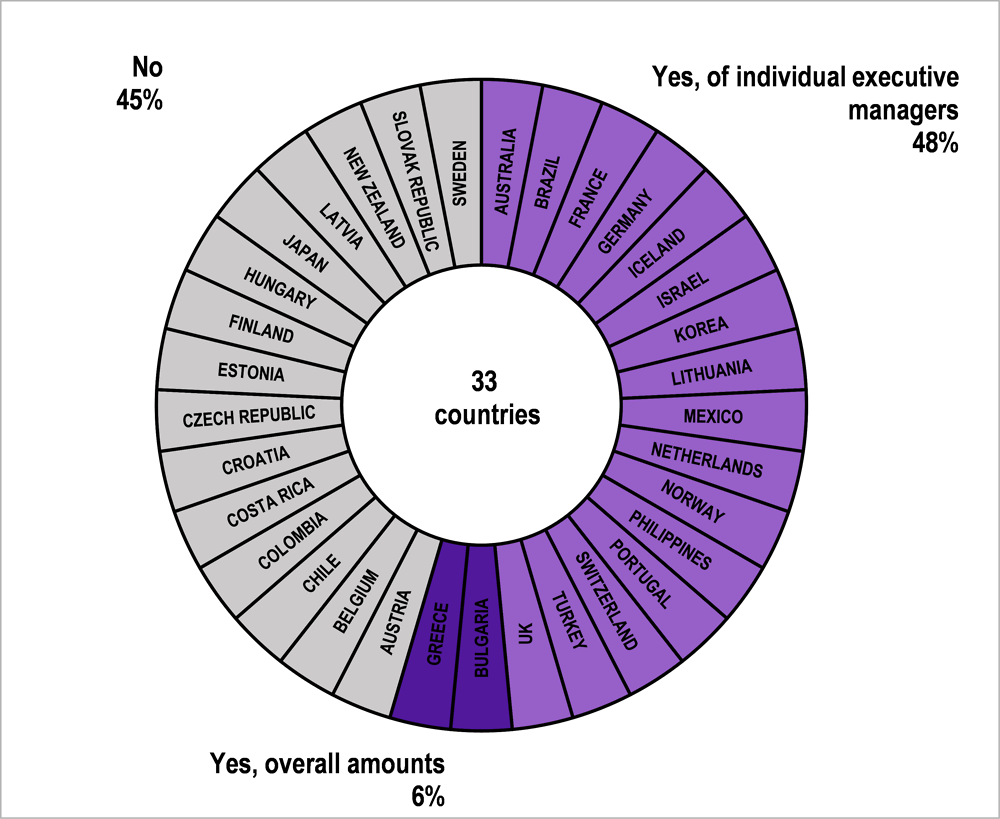

3.4.2. Disclosure practices by the state or ownership entity

In almost half of the surveyed countries with available information (15 out of 33), the state or ownership entity does not disclose information on the remuneration of executive managers, mainly because SOEs are already required to do so in their annual reports or on their websites (e.g. Austria, Belgium, Chile, Estonia, Finland, Japan, New Zealand), or because remuneration caps are set by law which is itself publicly available (e.g. Turkey). This may also be because in these countries, setting the remuneration of executive managers is the responsibility of the board and not the state.

In some of these countries, while executive remuneration is not disclosed on a systematic basis, SOEs are legally required to disclose the monthly remuneration of public officials appointed by the government as executive managers in SOEs (Colombia, Latvia). In Costa Rica, similar to boards, while information on remuneration is not actively disclosed by the ownership entity, the Presidential Advisory Unit on State Ownership does disclose whether specific SOEs are complying with their responsibility to publish the required board and management remuneration information, as part of the analysis included in the annual Aggregate Report on SOEs.

Out of the 16 countries where the government discloses granular information on remuneration of executive managers, in some instances this is mainly done through a central government portal aggregating all SOE websites, making this information easily accessible to the public (Australia, Korea, Portugal). In France, the Netherlands, Norway and Switzerland, information on executive remuneration is disclosed in the government or ownership entity’s annual report on SOEs, or by the Commission on Audit in the Philippines. In the United Kingdom, the state collates and discloses the salary of all employees who earn more than GBP 150k except those employed by ‘public corporations’.

In some countries, disclosure is limited to the remuneration of the CEO only (Iceland, Lithuania, Norway), or to the remuneration of executive managers of large SOEs only (Bulgaria). In Lithuania, since 2018 the Governance Co‑ordination Centre publishes detailed analysis on CEO remuneration, both disclosing the total amount and composition of the remuneration for each SOE in its portfolio.

Figure 3.6. Disclosure of remuneration levels of executive managers by the government or ownership entity

Note: Data unavailable for Ireland, Peru and Spain.

Source: Author, based on an analysis of questionnaire responses and desk research.

References

[3] European Commission (2016), State-Owned Enterprises in the EU: Lessons Learnt and Ways Forward in a Post-Crisis Context, https://ec.europa.eu/info/publications/economy-finance/state-owned-enterprises-eu-lessons-learnt-and-ways-forward-post-crisis-context_en.

[11] IBP (2014), Transparency of State-Owned Enterprises in South Korea, https://www.internationalbudget.org/wp-content/uploads/Hidden-Corners-South-Korea.pdf.

[4] IDB (2016), State-owned enterprise management: advantages of centralized models, https://publications.iadb.org/publications/english/document/State-owned-Enterprise-Management-Advantages-of-Centralized-Models.pdf.

[5] Keppeler, F. and U. Papenfuß (2021), Understanding vertical pay dispersion in the public sectir: the role of publicness for manager-to-worker pay ratios and interdisciplinary agenda for future research, Public Management Review, https://doi.org/10.1080/14719037.2021.1942531.

[8] OECD (2022), Monitoring the Performance of State-Owned Enterprises: Good Practice Guide for Annual Aggregate Reporting, https://www.oecd.org/corporate/ca/Monitoring-performance-state-owned-enterprises-good-practice-guide-annual-aggregate-reporting-2022.pdf.

[7] OECD (2021), Ownership and Governance of State-Owned Enterprises: A Compendium of National Practices, https://www.oecd.org/corporate/ownership-and-governance-of-state-owned-enterprises-a-compendium-of-national-practices.htm.

[12] OECD (2020), Implementing the OECD Guidelines on Corporate Governance of State-Owned Enterprises: Review of Recent Developments, OECD Publishing, Paris, https://doi.org/10.1787/4caa0c3b-en.

[9] OECD (2020), Transparency and Disclosure Practices of State-Owned Enterprises and their Owners, OECD Publishing, Paris, http://www.oecd.org/corporate/transparency-disclosure-practices-soes.

[10] OECD (2015), OECD Guidelines on Corporate Governance of State-Owned Enterprises, https://www.oecd.org/corporate/guidelines-corporate-governance-soes.htm.

[6] OECD (2011), Corporate Governance of State-Owned Enterprises: Change and Reform in OECD Countries since 2005, OECD Publishing, Paris, https://doi.org/10.1787/9789264119529-en.

[2] Proximus Group (2020), Integrated Annual Report 2020, https://www.proximus.com/annualreport2020.html.

[1] Swedish Government (2021), Annual report for state-owned enterprises 2020, https://www.government.se/4a8002/contentassets/cfc739c587744fefa6e117e0f20ae788/annual-report-for-state-owned-enterprises-2020-complete.pdf.

Notes

← 1. In Norway, it is worth noting that since 2022, most SOE boards are required to prepare a remuneration policy to be approved by the general meeting, and the remuneration of the CEO and other executive managers must be set within such policy. The remuneration policy will not include limits for the overall remuneration levels.

← 2. See for instance: 16.438 Entreprises fédérales et entreprises liées à la Confédération. Pour des rétributions appropriées et pour la fin des salaires excessifs ; 16.3377 Un plafond des salaires à 500000 francs.

← 3. The absence of such requirements in Turkey can be explained by the fact that this information is already publicly available as the limits are set by law. Likewise, in Colombia, when public officials serve as executives their remunerations are publicly disclosed.