The Digital Supply and Use Tables (SUTs) extend the industry dimension of conventional SUTs by classifying based on how the producers are using digitalization to interact with consumers. The framework defines seven new digital industries, beyond those in existing formal classification structures, allowing for new aggregations of output, gross value added to be created.

OECD Handbook on Compiling Digital Supply and Use Tables

5. Digital industries (the “who”)

Abstract

Introduction

Chapter 1 notes that digitalisation has affected every industry within the supply and use framework, from the inputs used in production, to the way that the products are marketed and sold. It is for this reason that the Digital Supply and Use Tables (SUTs) framework presented in Chapter 2 includes the transaction and product perspectives (the “how” and the “what”) in addition to the activity or industry perspective (the “who”) discussed in this chapter. The transaction split (Chapter 3) can provide an insight into the level of digital ordering and delivery within a conventional industry, while the product perspective (Chapter 4) sheds light on the growth in Information and Communication Technology (ICT) goods and digital services consumed by businesses and households.

This chapter presents the seven new “digital industries” that are separately identified in the Digital SUT framework. These industries are not shown separately in the International Standard Industrial Classification (ISIC), but the economic units (companies etc.) that belong to them are included within established ISIC industry categories, and they are part of the conventional SUTs and related indicators. The Digital SUT framework clusters economic units in a way that is designed to highlight their role in digitalisation. This allows for traditional industry-based macroeconomic indicators such as output, gross value added (and its components such as gross operating surplus and compensation of employees) to be produced from a digitalisation perspective rather than with traditional economic activity breakdowns.

The chapter first provides detail on the definition and characteristics of each of the seven digital industries within the Digital SUT framework. For each digital industry, it also explains the benefits of separately identifying it. The chapter then reviews some of the early work that countries have undertaken to estimate the high priority indicators associated with the digital industries. It also discusses how the changes to the ISIC (from Revision 4 or “Rev. 4” to Revision 5 or “Rev. 5”) will affect the compilation of the Digital SUT industries.1

As digitalisation plays a bigger role in the economy, policy makers need information on the level of valued added and its contribution to economic growth coming from “digital” businesses. The digital industries presented in this chapter are considered significant enough to measure and to be of interest to policy makers. However, this may change over time as the digital economy continues to evolve. Changes may be made in the future either to remove from the Digital SUT framework industries that do not provide analytical interest to users; or to include additional industries that become fundamental to the digital economy.

The seven digital industries discussed in the next section of this chapter are included as additional columns in both the supply and use tables. They are:

1. The digitally enabling industry.

2. Digital intermediation platforms (DIPs) charging a fee.

3. Data- and advertising-driven digital platforms.

4. Producers dependent on DIPs.

5. E-tailers.

6. Financial service providers predominantly operating digitally.

7. Other producers only operating digitally.

The seven digital industries – concepts and definitions

1. The digitally enabling industry

The digitally enabling industry is made up of units that produce goods and services that enable the digital transformation to occur, such as IT equipment and software. In discussions with the Informal Advisory Group (IAG) on Measuring GDP in a Digitalised Economy, there has been a consistent desire to identify such facilitators of the digital transformation. For example, the “tiered” structure of the digital economy proposed in the G20 Roadmap toward a Common Framework for Measuring the Digital Economy (OECD, 2020[6]) included a “core measure”, made up of producers of ICT goods and services. As digitalisation spreads, the production associated with facilitating and enabling digitalisation is considered key for understanding its impact and analysing future trends.

This group is different from the other digital industries in that units are assigned to this industry based on the activity they are undertaking (and the good and service they are producing) rather than how they leverage the digital transformation.

Within the Digital SUT framework, the digitally enabling industry consists of producers for which their primary production is facilitating digitalisation. This definition builds on that of the ICT sector in ISIC Rev. 4, which is: “The production ([of] goods and services) of a candidate industry must primarily be intended to fulfill or enable the function of information processing and communication by electronic means, including transmission and display”. (UNSD, 2008[24])

For simplicity, it was decided to align the digitally enabling industry with the ICT sector in ISIC Rev. 4, as many statistical offices already have surveys and outputs in place consistent with this this definition (Eurostat, 2022[32]). This should make compilation of estimates straightforward.

The list of ISIC Rev. 4 categories (Table 5.1) spans a wide range of activities, from the manufacture of ICT goods to the delivery of telecommunication and information technology services. It was initially constructed in 2007 by the OECD Working Party on Indicators for the Information Society (OECD, 2007[89]) as a way of defining the digital economy. It is now considered too narrow as a definition of the digital economy,2 but it is useful for measuring the digitally enabling industry.

2. DIPs charging a fee

The emergence of digital intermediation platforms (DIPs) for buying and selling products is one of the most visible changes brought on by the digital transformation. DIPs provide an avenue for producers to interact with a larger number of potential consumers (including those in other geographical locations) at relatively low cost, lowering the barriers to entry and bringing in producers previously excluded from the market. At the same time, DIPs act as a form of commission agent for many producers, give consumers far greater ability to compare prices and quality of products and services and collect large amounts of information. In short, they match supply with demand, facilitating and structuring online transactions” (OECD, 2019[90]). Some well-known examples of DIPs are auction sites and independent booking sites for travel. Although platforms facilitating peer-to-peer (P2P) lending transactions and crowd funding share some similarities with DIPs (e.g. limited financial risk, charging a fee for a service), it was considered more appropriate to place these types of platforms in “financial service providers predominantly operating digitally” rather than DIPs charging a fee.

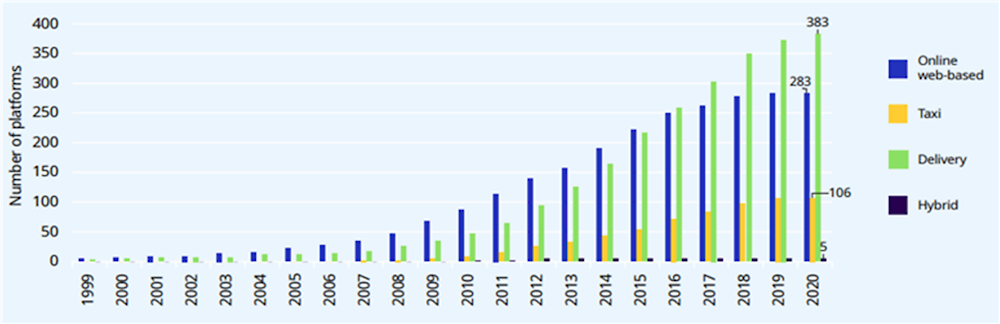

When a transaction goes through a DIP, both sides of the transaction derive economic benefits despite the fee charged for the intermediation service by the DIP. This is one of the main reasons that DIPs are now so popular, facilitating the buying and selling of all kinds of products and services. Evidence of this is shown by an ILO study of a subset of DIPs known as “digital labour platforms” (ILO, 2021[91]).3 The number of such platforms increased by around 400% between 2010 and 2020 (Crunchbase database, as cited by ILO, 2021[92]). Figure 5.1 shows the main types of digital labour platforms and their increase over this period.

Figure 5.1. Number of active digital labour platforms globally 1999-2020, selected categories

Note: Only currently active platforms are included.

DIPs are defined by the IAG on Measuring GDP in a Digitalised Economy as:

Business that operate online interfaces that facilitate, for a fee, the direct interaction between multiple buyers and multiple sellers, without the platform taking economic ownership of the goods or rendering the services that are being sold (intermediated).

This definition focuses on two important components that separate out DIPs from other online platforms as well as from traditional retail and wholesale activity. These are:

The charging of a fee for facilitating a transaction.

The absence of economic ownership of the product or service by the business facilitating the transaction.

The first point separates DIPs from the broader group of online platforms. DIPs do not include social media and platforms that provide services free of charge.

In 2019, the OECD, after extensive consultation, proposed a broad definition of online platforms as “a digital service that facilitates interactions between two or more distinct but interdependent sets of users (whether firms or individuals) who interact through the service via the Internet” (OECD, 2019[90]).4 However, this definition is for all digital platforms including those that are beyond the scope of DIPs. An “interaction” might simply be communication between two parties or an exchange of information. What separates DIPs from the broader group of online platforms is the charging of an explicit fee in exchange for facilitating a “transaction” as defined by the System of National Accounts (SNA).5 The charging of a fee creates a transaction in itself, and it also confirms that there is a transaction between the producer and the consumer.

Online platforms that do not facilitate an interaction that creates value added or do so but do not charge a fee to the producer or consumer must be generating revenue via other means. This is most likely from selling advertising space on their platform or selling analysis based on the data they produce from the interactions on the platform. Within the Digital SUT framework, the units that operate these platforms should be classified to data- and advertising-driven digital platforms.

The second point confirms that the DIP is not acting as a retailer or sub-contractor. Since the good or service that is exchanged as part of this transaction is not produced or owned by the DIP, the output and associated value added of the underlying product remain with the producer. The DIP’s role is to match the producer with the consumer, which is done in exchange for the fee, usually paid for by the producer and recorded as intermediate consumption.6

A global consultation on DIPs undertaken as part of the update to the 2008 SNA confirmed these two characteristics as being fundamental to the definition of a DIP7 (ISWGNA, 2022[87]). Descriptions of similar characteristics such as “leaving control rights with the supplier” and the ability to “adapt their price structures by levying different membership and usage fees on each side of the market” have also been discussed previously in different contexts (OECD, 2018[93]), (OECD, 2019[94]).

A final consideration on these two defining characteristics is that this appears to be how DIPs view themselves. Lyft, one of the largest rideshare platforms, described their business model in their 2021 annual report in the following terms:

We facilitate the provision of a transportation service by a driver to a rider (the driver’s customer) in order for the driver to fulfil their contractual promise to the rider. The driver fulfils their promise to provide a transportation service to their customer through use of the Lyft Platform. While we facilitate setting the price for transportation services, the drivers and riders have the discretion in accepting the transaction price through the platform. We do not control the transportation services being provided to the rider nor do we have inventory risk related to the transportation services. As a result, we act as an agent in facilitating the ability for a driver to provide a transportation service to a rider. (LYFT, 2021[95])

This clearly shows that Lyft does not consider itself as taking ownership of the services provided. It sees itself as facilitating the transaction by acting as an agent.

It is worth noting that production from DIPs is already included in GDP. The concern for users is the lack of visibility of this contribution. This is partly due to two classification challenges affecting the measurement of DIPs.

The first of these challenges regards the product that these units are producing. This is because the current version of the CPC only addresses certain aspects of intermediation services (see Chapter 4).

The second challenge is a lack of consistency regarding where the activities of DIPs are currently classified. Recommendations on the classification of DIPs (‘intermediaries’ in the recommendations) were released in September 2017, as temporary guidance to supplement ISIC Rev. 4. The guidance said that if an appropriate support or agency class exists, the unit “is classified to the industry of the specific activity (e.g. travel agent, reservation service)”. If such a support or agency class does not exist, then it should be classified to “the industry of the principal [good or service they are intermediating] (e.g. telecommunications for selling telecommunication services on a commission or fee basis)” (Murphy, 2017[96]).

Since these recommendations were not part of a full update of the ISIC, it is unclear how much they have been implemented. Additionally, since most countries do not publish SUTs below the ISIC Division level, the specific output and value added from these DIPs are likely to be invisible within the national account aggregates as they make up only part of the Division. However, as discussed later in the chapter, ISIC Rev. 5, which was endorsed in early 2023, provides greater clarity to countries on how to classify DIPs in the future.

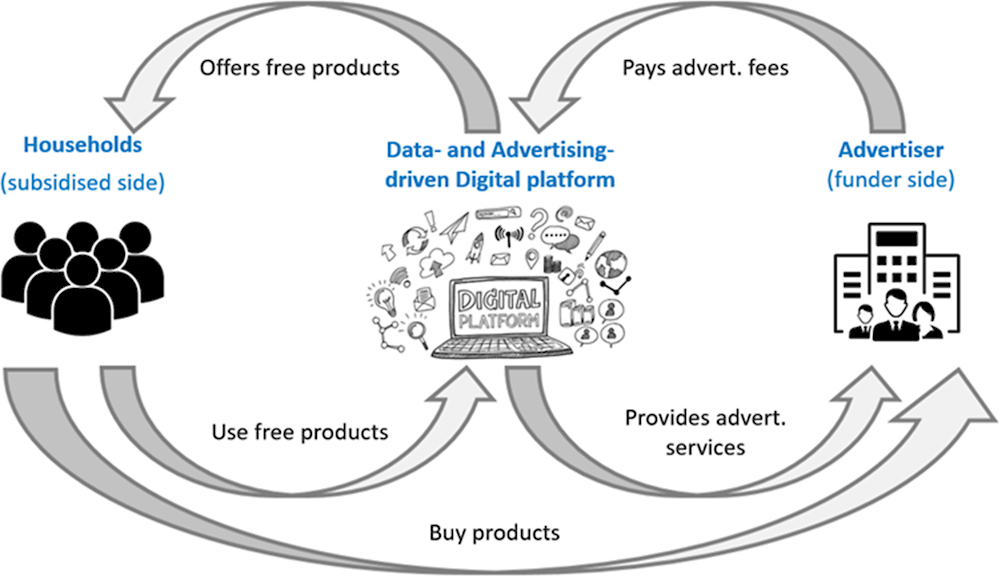

3. Data- and advertising-driven digital platforms

The data- and advertising-driven digital platforms industry includes all units operating exclusively as digital platforms whose main source of revenue is either the sale of data produced using information collected from the platform and/or the sale of advertising services using the platform for advertising.

To generate both eyeballs for advertising8 and information for data, platforms must produce digital services to attract people. These digital services are provided to users free of charge, so the business model of this digital industry differs from the standard producer-consumer paradigm.9 If a business is charging the consumer for the service they are providing, they do not meet the definition of data- and advertising-driven digital platforms.

Figure 5.2 shows how this business model revolves around revenue from sales in (usually) advertising or data analytics to third parties cross subsidising the cost of providing the free service. The better the free services, the more the likely the platform is to attract advertising and increase data services sold. This business model and how it is represented in the national accounts are described in detail in the SNA guidance note covering the treatment of free digital products (ISWGNA, 2022[97]).

Figure 5.2. Cross-subsidisation of data- and advertising- driven platforms

Note: Advertising can be purchased by the Government or non-profit institution serving households (NPISH) sectors in the national accounts, which generate revenue in ways that may not include buying products.

Source: (Eurostat, 2023[98]) – adapted.

Examples of data- and advertising-driven digital platforms include search engines, web mapping platforms, public transport applications, mobile wallets, information sharing (e.g. sport results) applications, social media and social networking sites. Such platforms offer a huge range of services to consumers, and since they are likely classified with other units that undertake similar activities (but charge for the service) rather than with the activity from which they derive revenue, they are likely to be classified across a range of conventional industry classifications.10

Cross-subsidisation business models have previously been used for other types of published content such as newspapers and TV. However, the proliferation of platforms operating like this means that there is now a large amount of labour and capital investment associated with producing content consumed by households as free digital services. This is not recorded as part of household consumption in the national accounts. Also, while the output produced by this labour and capital investment is still recorded as consumed by entities (intermediate consumption as input into other production), generating an estimate of the specific inputs contributing to this consumption of free digital services would be of interest for productivity measurement.

The extension of the Digital SUTs into a fuller Digital Economy Satellite Account (see Chapter 1) may involve estimating the value of these free products. A guidance note produced as part of the process of updating the 2008 SNA summarises options for recording and valuing cross-subsidised digital products and services in a satellite account (ISWGNA, 2022[97]). It concludes that it would be useful to identify the units that provide mainly free digital services and develop estimates of such services.

4. Producers dependent on DIPs

Producers dependent on DIPs are units that sell most of their goods or services via intermediation platforms. For the Digital SUTs, these units will be placed in this industry regardless of the good or service they are producing. They will be re-allocated from the activity-based classification in the ISIC if most of the demand for their products comes from a DIP. This industry may include both commercial enterprises (firms) and individuals (independent contractors or workers).

Whereas the output and the value added of the DIP industry consists of only the intermediation service product (see Chapter 4) associated with facilitating the transaction, for “producers dependent on DIPs”, the output and value added of the industry comes from the amounts they make via DIPs.

Individual workers or independent contractors in this industry usually source their business from DIPs that focus on types of products that can be produced by a single person. The International Labour Organization (ILO) refers to these DIPs as “digital labour platforms” (see DIPs charging a fee). While the platforms themselves would be classified in the DIP industry, the people who work with them should be classified in the industry “producers dependent on DIPs”.

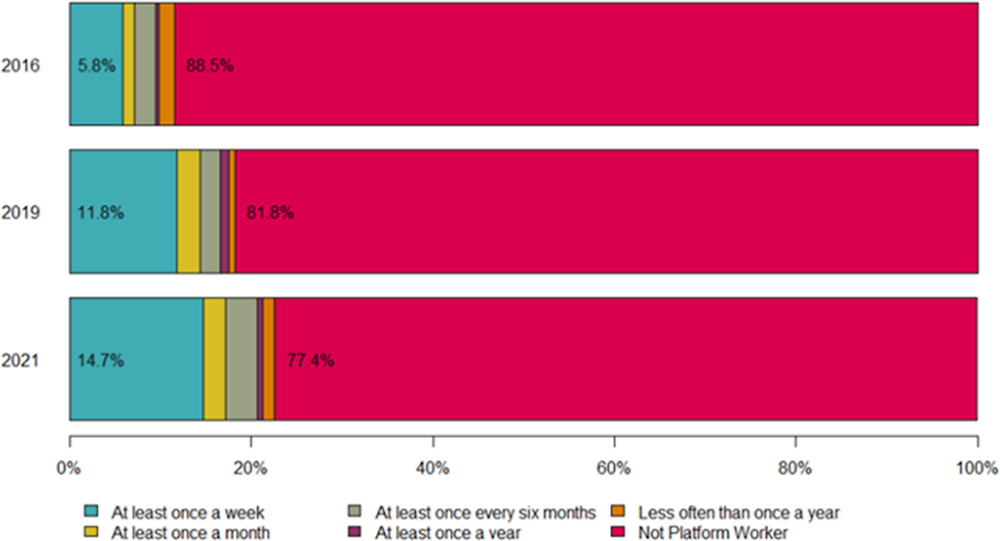

DIPs simplify the process of entering the workforce and provide opportunities for workers and firms to broaden their markets, potentially leading to increases in workforce participation and better outcomes for workers and the clients who engage them. Such benefits have seen a rapid expansion in those generating work via online platforms. For example, in England and Wales, the percentage of the working population who found work via a platform at least once a week has increased from 5.8% in 2016 to 14.7% in 2021 (Figure 5.3). However, as pointed out by the ILO, this rapid change also creates challenges and specific concerns, such as regularity of work and income, working conditions and social protection (ILO, 2021[91]). As the contribution of this sector to the economy increases, there will also be a need for policy interventions including regulation. For example, a review undertaken by the Conference of European Statisticians (CES) in 2022 found “that there is strong interest among policy makers and researchers across the CES region for data on new forms of employment, particularly digital platform employment” (UNECE, 2022[99]). Therefore, the compilation of accurate and visible estimates for this sector is important.

Digital labour platforms can be further broken down into two different types (ILO, 2021[91]):

Online web-based platforms, where tasks or work assignments are performed online or remotely by workers, before being (digitally or physically) delivered to the client (the user of the digital platform).

Location-based platforms, where tasks or work assignments are carried out in person in specified physical locations by workers.

Although this breakdown is not part of the Digital SUT framework, countries may also decide to include these two categories in their Digital SUTs.

Figure 5.3. Proportion of people who did work found via an online platform in England and Wales, 2016-2021

Source: (Spencer and Huws, 2021[100]).

5. E-tailers

E-tailers is defined as traders engaged in purchasing and reselling goods who receive most of their orders digitally.11 This industry has the same characteristics and definitions as the traditional ISIC Rev. 4 category of “retailers and wholesalers”, except for the digital ordering element.

Online shopping developed early in the digital transformation. Consumers who previously had to be in the same physical location as the retailers were able to browse and purchase goods from anywhere in the world. From the retailer’s point of view, online retailing reduces costs due to the absence of physical locations and opens additional markets. Because of these benefits, many traditional retail businesses that were buying products wholesale and reselling them physically to final consumers now do so entirely online. Others have developed as online-only retailers.

Separating out the units based on the method of ordering, even when they are undertaking the same fundamental activity, will provide insight into policy questions. While some research has shown that there is a limited difference between the price of products sold online and in store (Cavello, 2017[101]), the production and business models of online and in store retailers are different. For that reason, there is a clear user interest to see results separately, obtaining insights into how the specific business models may affect important indicators such as retail margins, operating surplus and the output-to-intermediate consumption ratio.

Almost all retailers in high income countries offer some form of e-tailing option. However, moving all units that offer this service to the new digital industry would mean just replacing the existing retail industry. At the same time, the IAG on Measuring GDP in a Digital Economy did not believe it was helpful to limit the definition of the e-tailers to units operating exclusively online. The IAG decided instead to define e-tailers as those units for which a majority of orders, in terms of value, are being received digitally. Such a definition will need to be approached with common sense and pragmatism, in the same way as units that undertake multiple activities are classified currently. It would be counterintuitive if units were to move back and forth between the proposed e-tailer classification and the existing retail industry depending on whether they were just over or just under the 50% value threshold. Additionally, materiality and resource availability will also dictate when such a move is made. It may not be practical for compilers to check all units within the retail industry every year to ensure that they are classified correctly, but this may not be necessary if the retailer contributes a very small amount to the industry. Rather, it is envisioned that compilers would move units into the e-tailer classification once this method of transaction becomes the predominant source of demand, with perhaps a higher bar considered if the unit is a particularly large contributor.

6. Financial service providers predominantly operating digitally

This industry contains financial service providers, including insurance, reinsurance and pension schemes/funds, which are operating predominantly online, with limited or no avenues to interact with consumers physically. It also includes financial platforms that facilitate digital peer-to-peer (P2P) lending and crowd funding.

In the national accounts, financial service providers belong to the Financial Corporations sector. In the ISIC Rev. 4, they are classified in Section K: Financial and insurance activities. For the Digital SUTs, financial service providers are part of the industry known as “financial service providers predominantly operating digitally” if they predominantly transact with consumers via digital channels.

Although consumers may be able to order a specific service directly from the producer, often within this industry the services are provided without direct contact between the producer and the consumer. Interactions with the service provider can take varied forms such as, for banking: using a credit card, an ATM (cash machine), an in-person consultation, making and receiving automatic transfers; for insurance: purchase of an insurance policy on an insurer’s website; or for asset management: selecting and buying funds on a platform provided by the asset manager.

In some cases, institutional units within this industry are exclusively digital. Many such units are associated with “Fintech”, a concept which is generally understood to be about financial services involving innovative new (digital) technologies.12 Examples of Fintech are robo-financial activities, online asset management platforms, P2P lending, crowdfunding, payment services, digital-only banks, InsurTech and PensionTech.

On the other hand, many units in the Financial Corporations sector of the national accounts engage in both physical and digital supply of services. Most banks, for example, still have high-street branches, even though much of their business nowadays is conducted online. For some banking activities there is no explicit charge to the consumer at the time of the service, leading to output being measured implicitly. If compilers cannot calculate a defined percentage of digital ordering that would result in a unit being considered digital, the decision on whether to include the unit in this industry should be based on determining whether the predominant way that the unit transacts with consumers is digital.

The IAG discussed the option of making the definition of this industry exclusively (rather than predominantly) digital. However, it was considered that such a narrow definition may exclude units which for all intents and purposes are operating digitally, including those providing insurance and pensions.

As in the case of e-tailers, the recommendation to use the “predominance” principle implies some subjectivity on the part of compilers; but this is not unusual in national accounts classification decisions. As more countries produce outputs associated with this industry, the feasibility of its compilation and comparability across countries will be able to be tested, as will the analytical usefulness of the estimates in relation to emerging policy requirements and user needs. In the future, inclusion in this industry may be based on some other characteristic of digitalisation beyond digital ordering or delivery. Additional changes, if required, can be made at this time.

7. Other producers only operating digitally

This industry is made up of units operating exclusively online that are not included in one of the previous six digital industries. It includes businesses that produce their own goods and services and interact with consumers in an exclusively digital manner. All ordering within this industry would be considered as digitally ordered, and all services within this industry would be considered digitally delivered.13 This industry is defined as exclusively digital in order to maintain its analytical usefulness and interpretability. While many producers have a significant digital component in their interactions with consumers,14 it was considered more useful to users to limit this industry to so called “digital natives” whose business model is based on digitalisation.

This industry may include any unit producing a service that is considered digitally deliverable (see Chapter 3). Examples include producers providing digital content on a subscription basis (such as digital newspaper subscriptions and audio or visual content subscriptions), online gaming and gambling services, as well as more traditional services (such as legal or accounting services) that only have a presence online.

However, the industry should exclude units that interact with consumers digitally as well as physically. For example, it would include universities and other tertiary education providers that interact with students entirely online, where students do not have the option to attend physically and must receive their education service digitally; but it would exclude education providers that offer online courses in addition to physically attended courses.

Similarly, it should exclude newspaper publishers that sell newspapers through physical outlets such as shops and newspaper stands as well as selling via digital newspaper subscriptions, since the publisher is interacting with consumers both digitally and physically. However, if a newspaper only sells its product via digital subscriptions, it should be included in this industry even if the newspaper is delivered to the home or office of the online subscriber.

In many ways, these businesses are like the data- and advertising-driven platforms, in that they are providing a wide variety of services to the consumer in a digital manner. The difference is the business model, in that the data- and advertising-driven platforms are subsidised by revenue from other sources, whereas the units contained within “other producers only operating digitally” are explicitly charging the consumer for the service provided.

In some cases, this may be thought of as a residual class, ensuring that all businesses operating exclusively in a digital manner are captured in one of the digital industries.15 For example, most producers only operating digitally are likely to be collecting data. If this is a by-product of their main activity, they should be in the “other producers only operating digitally” industry, rather than in the data- and advertising-driven platforms industry.

Methods and sources used by countries to estimate outputs associated with digital industries

Undertaking compilation of industry outputs

The Digital SUTs are about reallocating production that is already contained in the national accounts and conventional SUTs in a way that provides insights into the digital economy. Output and the components of value added (compensation of employees, gross operating surplus and mixed income) for each of the seven digital industries need to be reallocated from the industry aggregates of the conventional SUTs. It should be noted that the coverage of the conventional SUTs includes informal units such as undocumented workers and businesses not formally reporting their income from certain productive activities. Such units are included within the SNA production boundary, so the output of these units may also be reallocated alongside the formal units. In some cases, estimates representing the informal sector may require updating due to the increasing role of digitalisation in the economy.

As outlined in Chapter 2, in the initial stages of the development of the Digital SUTs, the high priority indicators associated with the digital industries are: output, gross value added (GVA) and the components of GVA: compensation of employees, gross operating surplus and mixed income. In time, additional estimates connected to labour (i.e. number of employees and/or hours worked) and capital formation may be introduced. The ease with which additions can be made may depend on the compilation (or re-allocation) strategy implemented.

Based on the initial attempts to produce estimates, the compilation methods for deriving the high priority indicators associated with digital industries fall into two categories. Within the handbook these are referred to as:

Reallocation of specific units: where specific units are identified as matching the criteria of the new digital industry and estimates of output, intermediate consumption and value added associated with these units are moved to the new industry.

Aggregate reallocation based on indicators: where specific units cannot be identified, aggregated estimates associated with the production of these units is calculated using alternative indicators. The aggregate amounts can then be deducted from existing industry classes and moved to the new industry.

Based on a review of early compilation attempts, it appears that the digitally enabling industry and DIPs charging a fee favour compilation by reallocation of specific units across industries, while e-tailers and producers dependent on DIPs are more easily compiled using the indicator method. However, no choice is correct or incorrect and the choice of method (including any other method not yet documented) applied by countries should be undertaken based on a range of reasons, including statistical infrastructure, available resources and source data availability.

Compilation of digital industries based on reallocation of specific units

To reallocate specific units, first it is necessary to identify the units. If the businesses that meet the characteristics of the new digital industry are already in the business register or other sampling frames and already being surveyed as part of traditional surveys, it should be straightforward to identify the units that should be reallocated. However, this may be a non-trivial task where the registers are large and complex. The sampling strategy of the surveys used to produce the estimates may also need to be re-designed to provide sufficiently robust estimates for the new industries (and of the existing ones after removing the reallocated units).

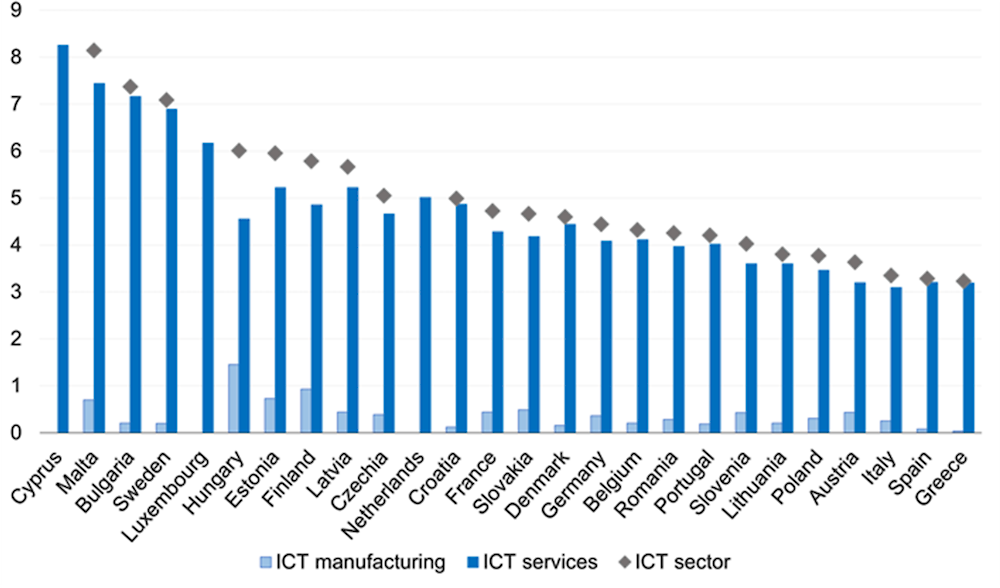

For the digitally enabling industry, the separation of the units has already been undertaken in many countries (Figure 5.4) because the definition of the new industry is aligned with the ICT sector in ISIC Rev. 4 (see the digitally enabling industry). While Figure 4 only covers Europe, estimates of value added for the ICT sector are also available for many other countries.

Figure 5.4. Value added for the ICT sector in the EU, 2020

Notes:

For Spain, data is for 2018; for Estonia and Italy, data is for 2019.

Data for Belgium, Germany, Greece and France is provisional.

The following results have been supressed to protect confidentiality: ICT manufacturing and ICT sector for Cyprus, Luxembourg and the Netherlands; all results for Ireland.

Source: (Eurostat, 2022[32]).

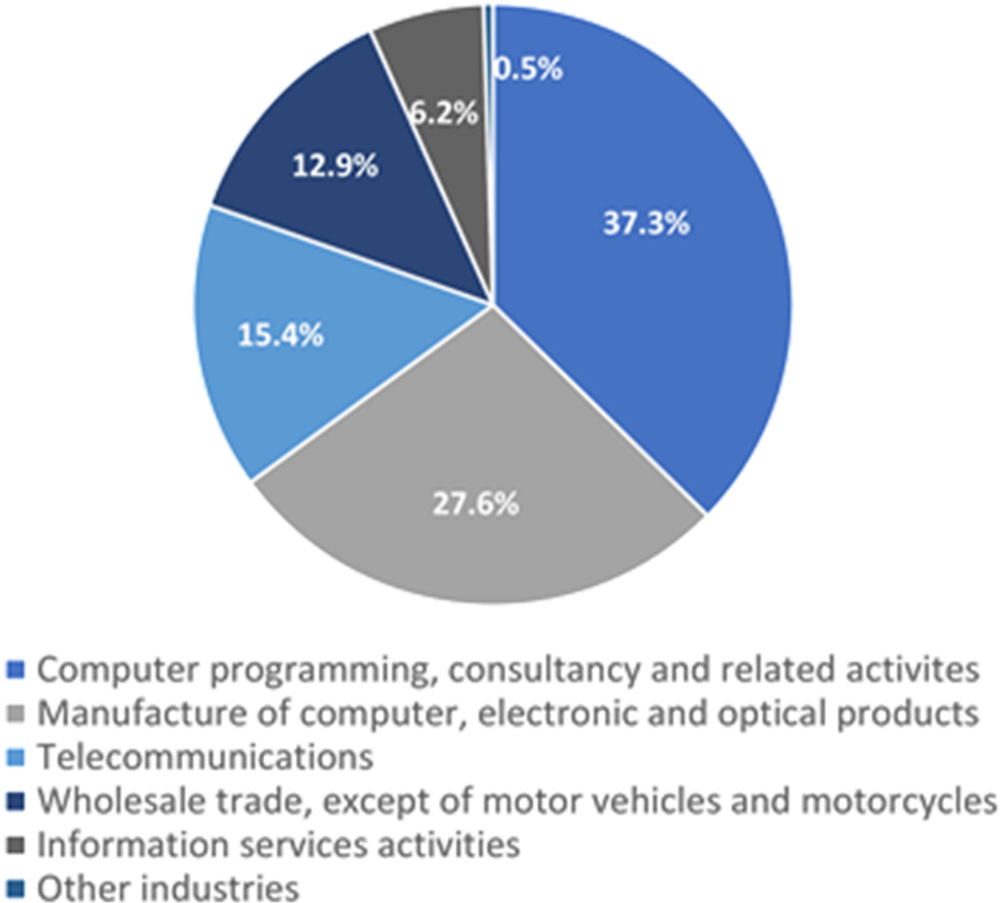

As these estimates come from different conventional industry columns, further breakdowns showing the composition of the digitally enabling industry are possible. Figure 5.5 shows that over one-third of the output of the digitally enabling industry in the Netherlands comes from a single NACE division: Computer programming, consultancy and related activities.

Figure 5.5. Composition of the output of the digitally enabling industry, Netherlands, 2018

Note: The numbers in the category descriptions (e.g. 61 Telecommunications) refer to divisions of NACE, the statistical classification of economic activities in the European Community.

Source: (Statistics Netherlands, 2021[43]).

Statistics Canada followed a similar approach for the estimation of e-tailers in their Digital SUTs publication. Their approach re-allocated to the e-tailer industry units that were classified to the NAICS category of 454110 “Electronic Shopping and Mail-Order Houses” (Statistics Canada, 2021[102]). NAICS defines this category as “establishments primarily engaged in retailing all types of merchandise using non-store means, such as catalogues, toll free telephone numbers, or electronic media, such as interactive television or the Internet” (NAICS, 2017[46]). This category is likely to contain many units that fit the characteristics of e-tailers, but it may also include establishments that still require non-digital ordering. Additionally, almost all retailers now offer some form of digital ordering option, so it is likely that other units not classified to NAICS 454110 would also fit the definition of e-tailers within the Digital SUT framework. Therefore, the approach to e-tailers taken by Statistics Canada is not fully aligned with the framework. Nevertheless, it has the advantage of being straightforward to do and transparent for users, who understand that units that were classified as X are now classified as Y. Such approaches are still welcome, if they are accompanied by explanations on what may or may not be included in the estimates.

It is not always so straightforward to identify the specific units to be reallocated to a new digital industry. The digitally enabling industry is the only digital industry that is defined by a specific set of ISIC/NACE/NAICS categories. For the other industries, units must be identified based on whether they meet the characteristics of the new industries. So far, compilers have tried both systematic approaches as well as those based more on compilers’ knowledge and research.

A systematic example was that undertaken by Statistics Netherlands to identify DIPs (See Box 5.1). The method involved training a machine learning algorithm to identify potential DIPs based on language used on their firms’ websites. This produced a register of DIPs that allowed Statistics Netherlands to run a DIP survey. The survey was designed first to confirm that the business did operate a DIP (as defined in the Digital SUT framework) and then to collect the specific information required for the high priority indicators for the DIP industry.

Box 5.1. Identification of online platforms by web scraping

Statistics Netherlands has derived a register of DIPs in a systematic way using web scraping. The first step was to identify key words that were likely to be present on a DIP website, such as: “register”, “login”, “platform”, “sign up”. The key words were found on websites of platforms that had already been manually identified by the staff of Statistics Netherlands. Using a list of companies from the country’s business register, the web scraping tool then scraped through websites of businesses with a “.nl” domain. This had the advantage of aligning the register of DIPs with the business register; but it also meant that any new platforms not yet included in the business register would be excluded from the DIP register.

Based on the prevalence of the words on the website, each website was given a score between 0 and 1 based on the possibility of the unit being a DIP. After reviewing over 600,000 websites, it was decided that those with a score of 0.8 or higher would be considered for inclusion in the DIPs survey. A manual review reduced the number of potential units by around half (Table 5.2). This component of the work was resource intense but improved the quality of the register. It should be noted that over the three years that the model has been run, it has produced relatively stable results.

Table 5.2. Identifying DIPs in Netherlands: refinement process

Importantly, this approach can be used for identifying other types of businesses, with promising results observed when for example asked to identify “innovative” companies, although a similar exercise for identifying companies using AI proved more problematic.

Source: (Statistics Netherlands, 2022[103]).

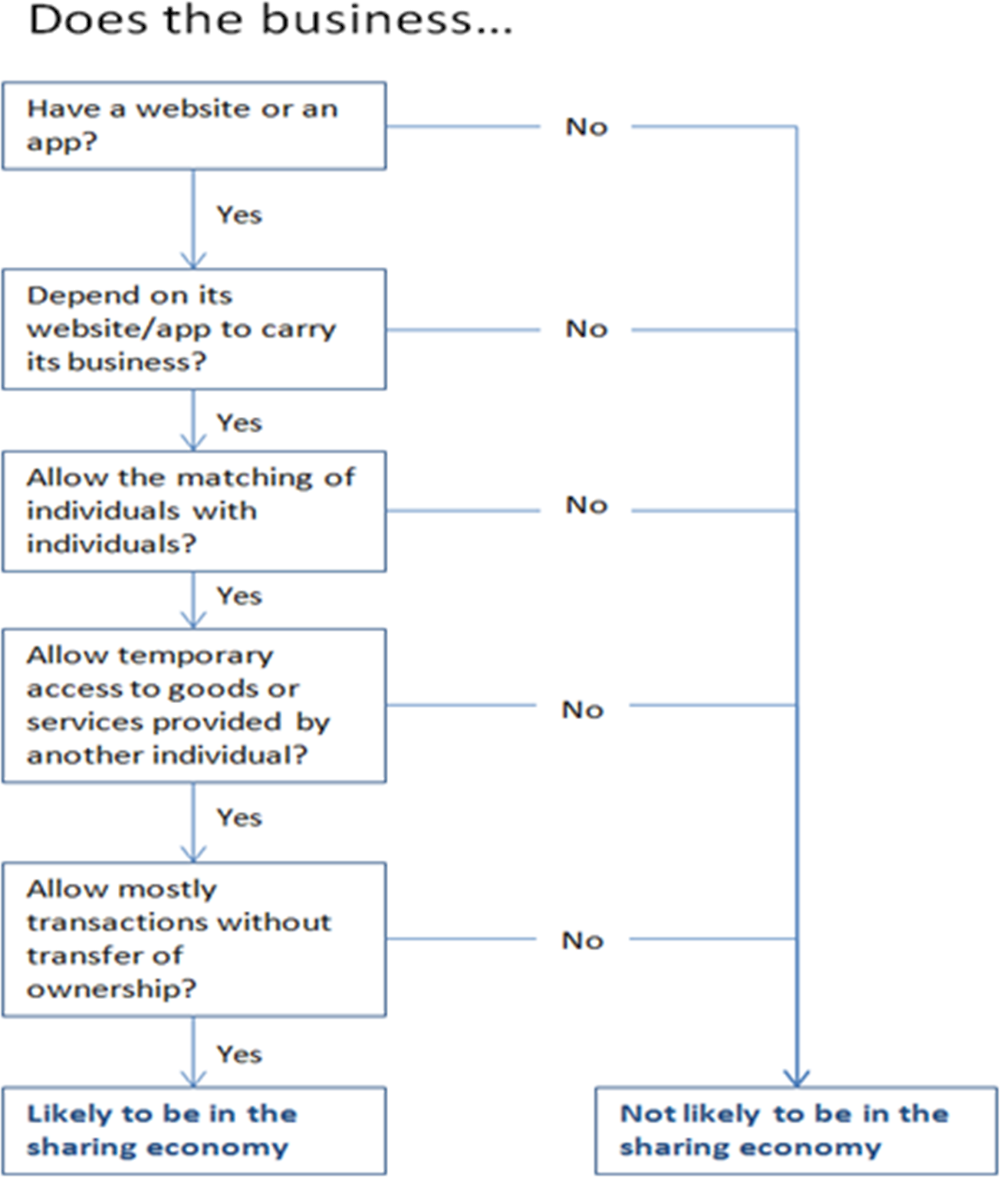

An alternative approach was undertaken by the UK Office for National Statistics (ONS) in response to concerns that elements of the “sharing economy” were not included in the country’s economic indicators. The sharing economy was defined by the ONS as “the sharing of under-used assets through completing peer-to-peer transactions that are only viable through digital intermediation, allowing parties to benefit from usage outside of the primary use of that asset” (ONS, 2017[104]). While this work focused on the topic of the sharing economy rather than DIPs as defined in the Digital SUT framework,16 the method and challenges faced in their work are similar to those faced by countries attempting to identify DIPs.

By using the decision tree shown in Figure 5.6 to assess manually chosen businesses, the ONS identified an initial list of businesses involved in the sharing economy. This approach was time consuming and may have missed some businesses that should be included. Therefore, a more systematic approach was attempted using a key word search in the standard business register; but this still required a lot of manual checking and research.

Figure 5.6. ONS decision tree for identifying “sharing economy” businesses

Source: (ONS, 2017[104]).

The list of businesses produced by this decision tree was not intended to lead to a specific survey, but rather to ensure that existing surveys such as the Annual Business Survey could produce results for the sharing economy. The ONS then published indicators of how the sharing economy was impacted by the COVID pandemic (ONS, 2020[105]).

Although the ONS is now looking to update its definition of the sharing economy and is no longer using the specific decision tree shown in Figure 5.6, the approach is still an interesting one. It could be refined to produce indicators for DIPs as defined in the Digital SUT framework by including an additional question about the charging of fees.

A similar technique of identifying businesses that meet the definitions of digital industries in order to reallocate them to a new industry has been envisioned for other digital industries in the framework such as “financial service providers predominantly operating digitally” and “other producers only operating digitally”. In these industries, there are likely to be a small number of large firms that fulfill the predominantly or exclusively digital requirements, allowing for easier identification and classification using decision trees.

However, based on compilation attempts so far, some challenges have been uncovered. As pointed out by Statistics Netherlands, while “Many insurance and banking brands are promoted as online businesses, […] the brands or labels are owned and operated by a small number of very large business units that run both online and mixed models” (Statistics Netherlands, 2021[43]). This means that compilers will need to make decisions about including borderline cases in the “financial service providers predominantly operating digitally” industry or excluding them.

A similar concern was highlighted when Statistics Netherlands attempted to identify “producers only operating digitally“, where they concluded that “most providers of online content are not necessarily digital only, and that (online) distribution and production of content are in most cases integrated in a single statistical business unit” (Statistics Netherlands, 2021[43]). In this example, the focus was on the providers of online content. It needs to be further explored whether there are enough units meeting the definition of “other producers only operating digitally” to make this industry feasible to compile. Such learning experiences are important, not just to assist other countries hoping to undertake this kind of compilation, but also to continue to provide evidence on the feasibility of the current definitions for each of the industry.

While countries are still strongly encouraged to aim for estimates as consistent as possible with the agreed definition, it is possible that on occasions, some flexibility may be required. For instance, Statistics Canada in their outputs concluded that “for practical reasons, the units classified here [to other producers operating digitally] are not required to generate 100% of their revenues from online activities but rather a large majority of their revenues is deemed a sufficient condition” (Statistics Canada, 2021[102]). Therefore, while consistency with definitions and concepts is fundamental for meaningful international comparability, the ability for countries to actually produce estimates is equally important and as such, flexibility, accompanied by transparent metadata on how the estimates may differ from other countries, may greatly assist in the formation of initial outputs.

Box 5.2. The effect of ISIC Rev. 5 on the digital industries

In the ISIC and related classifications such as NACE for Europe and NAICS for North America, industry categories are designed around similarities in economic activity, not technology, as such a “distinction between modern and traditional production methods is not a criterion for ISIC, although that distinction may be useful in some statistics” (UNSD, 2008[24]). The final structure of the revised industry classification, known as ISIC Rev. 5, was endorsed in March 2023 at the annual meeting of the United Nations Statistical Commission (UNSC). ISIC Rev. 5 maintains this technology neutral perspective, whereby existing activities that are ordered or delivered via a new mechanism do not require a new classification (UNSC, 2022[51]).

However, new classifications are warranted where new technology has created new economic activities (or made previous activities large enough). This is the case for intermediation activities. Therefore ISIC Rev. 5 provides specialised classifications for activities associated with intermediation platforms. The final ISIC Rev. 5 structure includes 30 new classes or groups specifically created for the classification of units that facilitate “transactions between buyers and sellers for the ordering and/or delivering of goods and services for a fee or commission, without supplying and taking ownership of the goods and services that are intermediated” (UNSC, 2022[106]). These cover non-financial intermediation only.

Unlike the DIP industry within the Digital SUT framework, the change to non-financial intermediation in ISIC does not involve the aggregation of all intermediation platforms into a single category regardless of the product they are intermediating. Rather, the new classes are allocated to the division of the underlying economic activity being intermediated. Nevertheless, this change allows compilers to identify DIPs and aggregate the relevant outputs to compile estimates for the DIP industry in the Digital SUTs.

The source of revenue (e.g. explicit fee or advertising) does not come into consideration when classifying the unit for ISIC purposes. Therefore, when compiling the Digital SUTs, work will likely be required to separate the value added coming from DIPs (which facilitate a transaction as defined in the SNA and charge a fee to do so) from platforms that are providing the same intermediation service but deriving their revenue from data or advertising, making them part of the “data- and advertising-driven platform industry” in the Digital SUTs. Additionally, since the industry classification is agnostic to technology, the new classes may contain some traditional intermediation units undertaking the same activity (matching producers and consumers, for a fee) but without a digital platform. These units will need to be removed before compiling DIP estimates in the Digital SUT framework.

Other changes introduced in ISIC Rev. 5 may make it harder to compile estimates of digital industries. For example, in order to reflect the “new-normal” situation of most retail firms having both a physical and online mechanism for receiving orders (see Chapter 3), ISIC Rev. 5 has eliminated the distinction of retail trade activities according to the trade channel. This means that the distinction between “store” and “non-store” retailers (with the latter including a specific class for retail sale via mail order houses or via Internet) is no longer available. Compilers will either need additional steps to identify the relevant activities, or they will need to use indicators to apportion the aggregate retail estimates. However, the additional steps needed to identify non-store e-tailers will probably be needed anyway to identify the e-commerce business of store retailers.

Compilation of digital industries using aggregate reallocation based on indicators

As the creation of the Digital SUTs is a re-allocation rather than an initial compilation, it is possible to produce estimates for the new digital industries without identifying the specific units to which the values belong. Since all the output and value added associated with the new digital industries is already included in the output and value-added estimates of the conventional SUTs, once an estimate of the proportion belonging to the specific digital industry has been created, the amount can simply be deducted from the existing industries.

Such an approach is particularly useful for estimating the output of units that are hard to identify (such as producers dependent on DIPs) or where part of a conventional industry does not meet the definition of the new industry. For example, for estimating output related to e-commerce, the United States Bureau of Economic Analysis (BEA) uses a specific indicator, in this case online sales from the Annual Wholesale Trade Survey (United States Census Bureau, 2020[107]) and the Annual Retail Trade Survey (United States Census Bureau, 2020[41]), to determine the proportion of retail and wholesale margin that is associated with digital ordering. The BEA applies this proportion to the estimated retail and wholesale margin in the conventional SUTs (Bureau of Economic Analysis, 2022[47]). This estimate of “e-commerce retail margin” can be used as the basis for an initial estimate of gross output (and thus used to calculate GVA) for the e-tailer industry.17

Both the United States BEA and Statistics Canada include output that is not entirely consistent with the definition in the Digital SUT framework. Since the BEA’s estimate is modelled using data from an indicator, it may include output from firms that may make only a minority of sales through digital ordering, and therefore are not e-tailers as defined in this chapter. The estimate from Statistics Canada, on the other hand, likely includes some legacy units from the NAICS category, that are not receiving orders digitally, as well as missing some traditional retail units (not classified to NAICS 454110) that are now receiving a majority of orders digitally. However, both approaches have been published with transparent methods allowing users to understand their scope, and both are a starting point for the estimates of the e-tailers industry.

A digital industry that contains particularly hard to identify units is “producers dependent on DIPs”. Many of the producers are unincorporated or individuals acting as independent contractors. However, this very characteristic can be used as a potential indicator of activity. Statistics Canada made the reasonable assumption that people who were registering as independent contractors within the taxi industry were doing so solely in order to leverage the opportunities created by DIPs. After calculating the average revenue of a driver and multiplying this by the number of new registrations, they estimated the growth of output within this product and industry. This provided a timelier estimate than waiting until the new units had been added to the business register.

In many countries, producers that source demand through a DIP may not have undertaken the official registration process or been added to the business register. However, assuming that the methods used to include output from the informal sector are considered robust, the output from these units should still be included in the aggregates of the conventional SUTs.18 It is simply a question of finding an appropriate indicator, source data or model in order to estimate aggregates and then re-allocate these aggregate estimates of output or value added into the new industry. The recently released Handbook on Measuring Digital Platform Employment and Work (OECD, ILO, European Union, 2023[108]) includes several recommendations to make it easier for statistical compilers to identify workers involved with digital platforms. While these are often based around labour surveys, knowledge of the amount and characteristics of workers and producers who are dependent on platforms is an important first step in modelling estimates of output and value added.

Another example of work in this area, concerns estimating the value added of accommodation services created through accommodation-sharing platforms like Airbnb. A joint OECD/BEA project presented at the fifth meeting of the IAG on Measuring GDP in a Digitalised Economy sought to compile estimates of value added from the use of Airbnb. Although many accommodation-sharing platforms exist, Airbnb is the most widely known and used.

Using only publicly available data combined with some basic assumptions, indicators consistent with the Digital SUT framework were produced. This included value added produced by the individuals (or firms) providing the accommodation service (Figure 5.7), household consumption of the total accommodation services facilitated by the DIP, and intermediate consumption of intermediation services provided by the DIP (see Box 5.3).

The project used data from the national accounts of countries and from privately constructed (but publicly available) sources. The publicly available data included the number of booked nights per year, average length of stay (nights), revenues earned by the host per year, ratio of Airbnb houses to total housing stock, and the fee charged by Airbnb to the owners.

Only one year of results was produced, and the results for some countries are still experimental. However, the project showed what is possible using publicly available data.

Figure 5.7. GVA produced by Airbnb hosts as a proportion of accommodation and food services GVA, 2018

Note: Results for the Netherlands only refer to Amsterdam.

Source: (Tobiassen, 2021[84]).

Box 5.3. Developing internationally comparable estimates of GVA produced from Airbnb

The OECD aimed to understand the GVA from accommodation-sharing platforms and its potential impact on the national accounts, with comparable estimates for countries (Tobiassen, 2021[84]). The method, which built on work previously done by Statistics Netherlands (Hiemstra, 2017[109]), estimated the production value and the intermediate consumption that takes place when a room or apartment is rented out on Airbnb (the dominant player in the industry). The difference between the two gives the GVA of Airbnb hosts for one year. An adjustment was made to account for accommodation being facilitated by other platforms.

The production value of Airbnb hosts is composed of total revenues received by Airbnb hosts (which includes a payment for cleaning that is often separately invoiced). These can be estimated using the number of listings and the average revenue per host. For ease, an assumption was made to apply an average cleaning fee for all countries in the analysis. However, if required, a per country estimate could be calculated using the average cleaning costs per booking and overnight stays per year.

Intermediate consumption of Airbnb hosts is composed of small household purchases, cleaning costs, costs of water, heating, electricity, as well as the fee charged by Airbnb to the owners. For the small household purchases and cleaning services per stay, there are no sources available, and it was assumed to be 5 EUR and 55 EUR respectively (for all countries). Based on research, the fee charged by Airbnb to owners was assigned as 3% of rent charged to the guests. Additionally, estimates were made for the fee charged by Airbnb to guests: based on research, this was estimated at 6% to 12% of rent. This amount is considered final household consumption and GVA of the DIP rather than of the hosts.

Because Airbnb is based in the United States, the service charge fee charged by Airbnb to the hosts and guests is considered an import of services in other countries. Thus, estimates of imports in respect of accommodation-sharing services can be added to the Digital SUTs.

An adjustment was made for the imputation already included in the national accounts for dwelling services (owner-occupied rent). These estimates of owner-occupied dwelling services assume that owners occupy their homes full-time, such that any unrecorded activity from short-term market lettings, such as Airbnb transactions, will in part be covered by the imputation for owner-occupied rent. Additional output created by making an apartment available through Airbnb can be considered as the difference between the short-term rental price and established rental price used to calculate the imputed owner-occupied rent.

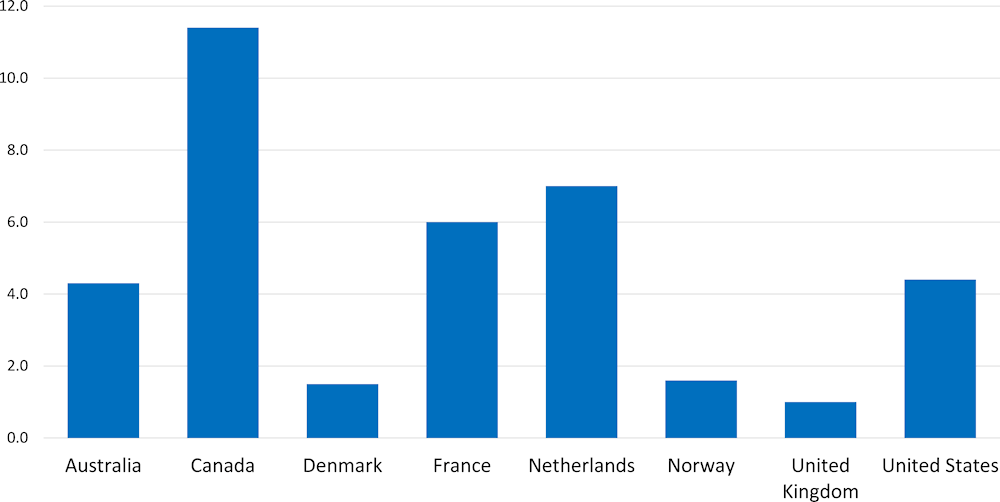

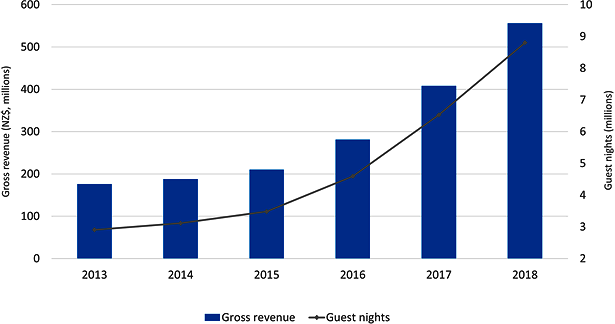

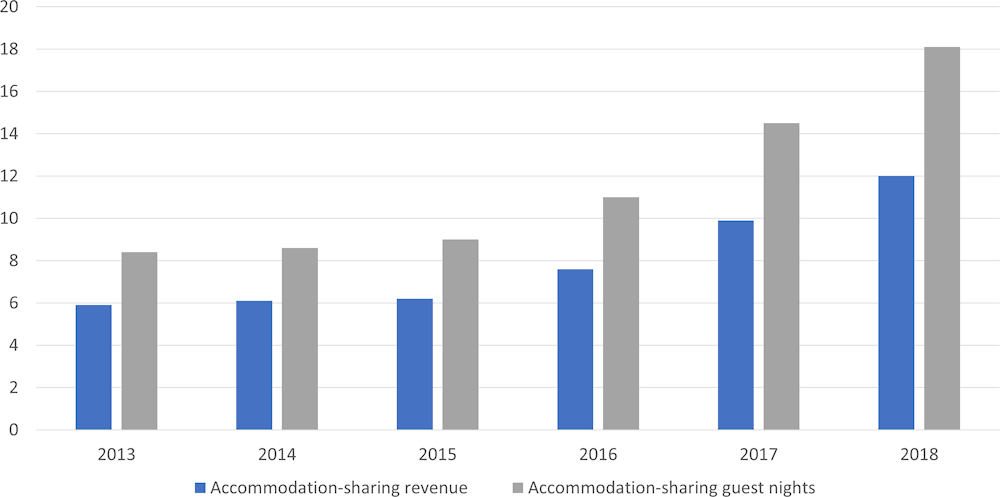

New Zealand has also produced estimates of the level and growth of output generated via accommodation-sharing platforms. Data sourced either from publicly available sites including directly from the platforms was combined with existing data sources such as a regular survey of accommodation occupancy, the national accounts and census information. To create estimates of output, different methods were used for different platforms, depending on the available source data for the platform. In some cases, the total payment received was used as a starting point, before incorporating assumptions regarding the fee charged by the intermediation platform. In others, the known number of accommodation nights was merged with estimates of average prices per night. The results show not only considerable growth of revenue in the five years to 2018 (Figure 5.8), but also that accommodation-sharing revenue accounted for over 10% of total accommodation industry revenue in 2018 (Figure 5.9) (Grant, 2019[110]).

Figure 5.8. Accommodation-sharing guest nights and revenue, New Zealand, year ending March 2013-2018

Source: (Grant, 2019[110]).

Figure 5.9. Size of accommodation-sharing relative to total accommodation industry, New Zealand, year ending March 2013-2018

Source: (Grant, 2019[110]).

At the time of the research by Grant (2019), estimates of accommodation services from accommodation-sharing platforms were mostly included in the GDP figures of Statistics New Zealand and the conventional SUTs. The excluded portion consists of the difference between the higher average rental income and the imputed rental income for those who own their own house. However due to limited impact this would have on the GDP and SUT estimates combined with the known quality concerns, a decision was made to not use the amount in the core accounts (Grant, 2019[110]). If new estimates produced by research are not included in the conventional SUTs, they cannot be re-allocated to the new digital industries. However, once the quality concerns have been addressed, these estimates could be added to the conventional SUTs and national accounts aggregates and also used for the new digital industry estimates in the Digital SUTs.

Similarly, in other countries where adjustments or additional data may be added to the national accounts aggregates to account more fully for digital transactions, the newly calculated amounts could be moved across, without specifying the units that are being reallocated. Thus, the Digital SUTs, while designed as an extension, could in fact improve the conventional SUTs and estimates of GDP.

Conclusion

This chapter has outlined the definitions and characteristics of the seven new digital industries currently identified in the Digital SUT framework. The compilation of high priority indicators for these new digital industries will depend on their usefulness for policy makers as well as on the ability of countries to produce the indicators.

Countries have so far produced estimates using two different approaches. The first attempts to identify specific units and reallocate the associated estimates to the new digital industries. The alternative approach uses indicators to derive an aggregate estimate of output, intermediate consumption and value added being produced by the new digital industry and reallocates these amounts without identifying the specific units that the estimates relate to. Both approaches have benefits and challenges, and the choice of approach also depends on the type of digital industry for which the estimates are to be compiled.

Even with these two approaches, it appears that countries may still have to make assumptions and adjustments and, at times, be flexible with the digital industry definitions in order to produce estimates. This is to be expected as countries become familiar with the source data and methods during the initial stages of compilation. Different approaches to compiling digital industry estimates are acceptable when accompanied by explanations of what is and is not included, and how the estimates may differ from those produced by other countries.

Notes

← 1. While this chapter will reference ISIC, this can be interpreted as the corresponding industry classification used in respective regions (NACE in Europe, NAICS in North America etc.).

← 2. For instance, while it was included as a “core measure” of the digital economy in the G20 Roadmap, the Roadmap also included two additional tiers: producers who rely on digitalisation and producers who are enhanced by digitalisation. (OECD, 2020[6]).

← 3. While digital labour platforms are a large subset of the broader DIP industry, other DIPs also exist such as those that facilitate transactions in goods (such as clothing, electrical items etc.) as well as accommodation services or tickets to an event, where the consumer must be at a specific location to receive the service.

← 4. See “An Introduction to Online Platforms and Their Role in the Digital Transformation”, OECD Publishing, Paris, https://doi.org/10.1787/53e5f593-en). Additionally, this definition makes a split between platforms and e-tailers and producers supplying services digitally by adding that the definition “excludes businesses such as direct business-to-consumer (B2C) e-commerce and ad-free content streaming, as those serve only one set of customers. It does, however, include businesses such as third-party B2C e-commerce and ad-supported content streaming, because those services involve two separate sets of users”.

← 5. The SNA defines transactions as “an economic flow between institutional units by mutual agreement” with an economic flow representing “the creation, transformation, exchange, transfer or extinction of economic value” (UNSD, Eurostat, IMF, OECD, World Bank, 2009[18]). Many interactions via platforms do not include the economic flow components as no economic value is created, transferred or exchanged.

← 6. The recording of transactions associated with DIPs is discussed further in Chapter 4.

← 7. The support for this was near unanimous, with 49 of the 52 responders agreeing that the charging of an explicit fee for digitally facilitating an economic transaction between two independent parties and not taking economic ownership of the goods and services ultimately sold to the consumer were fundamental characteristics of a DIP.

← 8. Eyeballs are views of the advertising content by visitors to the platform. It is also possible to listen to an advertisement, rather than viewing it, as would be the case with free podcasts.

← 9. Conventional businesses may also provide “free services”. Often this takes the form of sponsorship or other expenditure paid for as part of marketing; but the main source of revenue in such business models remains charging for goods and services.

← 10. These units may go against the primary classification guideline outlined in ISIC, which is that the “principal activity of the unit should be determined with reference to the value added to the goods and services produced.” The value added that these platforms are providing are services such as advertising or data analytics; however, they are unlikely to be classified as such. ISIC provides the option to classify based on other criteria such as the activity that the majority of workers is undertaking (UNSD, 2008[24]).

← 11. This “majority” is from the perspective of value of sales. That is, a unit is an e-tailer if the value of their sales via digital ordering makes up most of their total sales.

← 12. Fintech is of considerable interest to policy makers, although there is no internationally agreed definition. Work to agree on definitions and classification approaches is ongoing, for instance as part of the third phase of the G20 Data Gaps Initiative, https://www.imf.org/en/News/Seminars/Conferences/DGI/g20-dgi-recommendations#dgi3

← 13. Since goods are not able to be digitally delivered, a firm may still be considered as exclusively operating digitally if they are receiving all orders digitally but physically delivering goods.

← 14. Including a large amount of non-market producers. Interactions with the government on issues such as taxation, visa applications and social welfare are now often (although not exclusively) conducted through digital channels.

← 15. Units should be placed in this industry if they are exclusively digital and do not meet the definition of one of the previous six digital industries.

← 16. The ONS sharing economy definition is broader that then DIP definition in the Digital SUT framework. While DIPs in the framework charge a fee for facilitating the transaction, there is no such requirement for the sharing economy approach. A business may answer “yes” to each of the questions in the decision tree (Figure 5.6), but then derive their revenue from an alternative source, thus failing the definition of a DIP in the Digital SUT framework. It would, however, be straightforward to adapt the decision tree to include an additional stage ensuring that outcomes are aligned with the DIP definition for the Digital SUT framework.

← 17. It should be noted that this is a step not yet done by the BEA. In their existing publication on the digital economy, the BEA has so far focused on the product perspective.

← 18. This assumption is an important one. Digitalisation has lowered the barrier of entry for many industries and, as such, many services that traditionally experienced very little to no output from the informal sector may now have such output. For example, couriers previously faced significant set-up costs, so it was in the business interest to register in order to claim tax deductions. Now any person with access to a bike share can earn money-delivering products, and there is less incentive to register officially.