Insurers were operating in 2022 in a context of rising interest rates that affected the demand for life insurance products in different ways. These different effects relate to the different types of products that life insurance includes. Life insurance traditionally offers protection against risks affecting the policyholder directly, as well as investment or savings contracts (e.g. annuity contracts, unit-linked products).

The rising interest rates have supported premium growth in annuity markets. Rising interest rates have improved the funding of defined benefit pension schemes embedding a promise of future benefits to their members when they use market-based discount rate to value their liabilities (OECD, 2023[1]). Some schemes have sought to lock-in these funding gains by transferring the risks to insurance companies and have purchased bulk annuities, such as in the United Kingdom and the United States. These two countries recorded a rise in the number of buy-out contracts. Individual retailers have also shown increased interest in annuity products (in particular fixed annuities) in the United States, as annuities can provide guaranteed levels of payments that reassure policyholders in a context of volatile financial markets.1 Rising interest rates also spurred the sales of annuity products in Latin America (e.g. Chile), which recorded some of the largest life premium growth in 2022 in many cases.

However, life investment products have been competing with other savings products sold by other financial institutions (e.g. banks), such as in France and the Netherlands. These other saving products could provide higher guaranteed rates of return as interest rates were raising. Customers could invest their savings in these products rather than in those offered by life insurers. In the Netherlands, the sales of life insurance products have been declining for years partly because of the competition with banks and investment institutions in the market of tax-incentivised products.2

Additionally, customers may simply switch from non-guaranteed life insurance products to life insurance products guaranteeing an income stream or an investment rate of return. For example, in Belgium, the demand for investments and therefore the premiums for life products with guaranteed rates (class 23 segment) increased while they decreased for life products without guarantees (class 21 segment). Other countries also saw a decline in premiums and a shift away from unit-linked products where policyholders bear the investment risks towards non-unit-linked products (e.g. Australia, Poland). The transfers from one life insurance product to another one likely account for the relative low or absence in premium growth in the life sector in some countries (e.g. Belgium, Poland).

Unit-linked products may suffer from volatile markets when customers may become more averse to risks and uncertainty. Drops in equity markets in 2022, and volatile financial markets more generally, may account for the large drop in life premiums in Ireland in 2022 where unit-linked business is the most dominant line of business of Irish insurers in the life sector.3

The cost-of-living crisis resulting from elevated inflation may have also constrained the demand for insurance products. Salaries have increased at a lower pace than inflation and with a lag, which has put pressure on the finances of households and reduced their capacity to save – introducing a deterrent for the purchase of life insurance policies (e.g. in Finland).

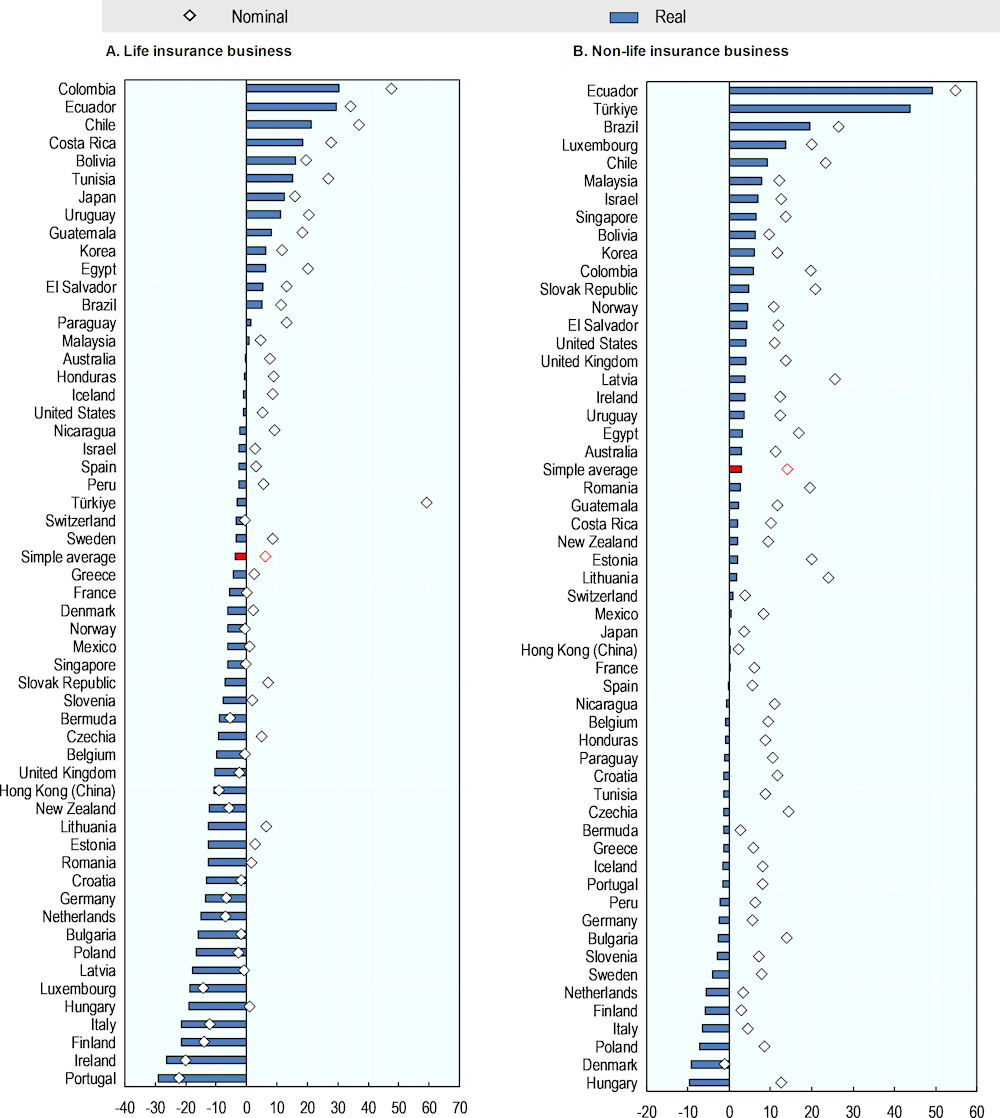

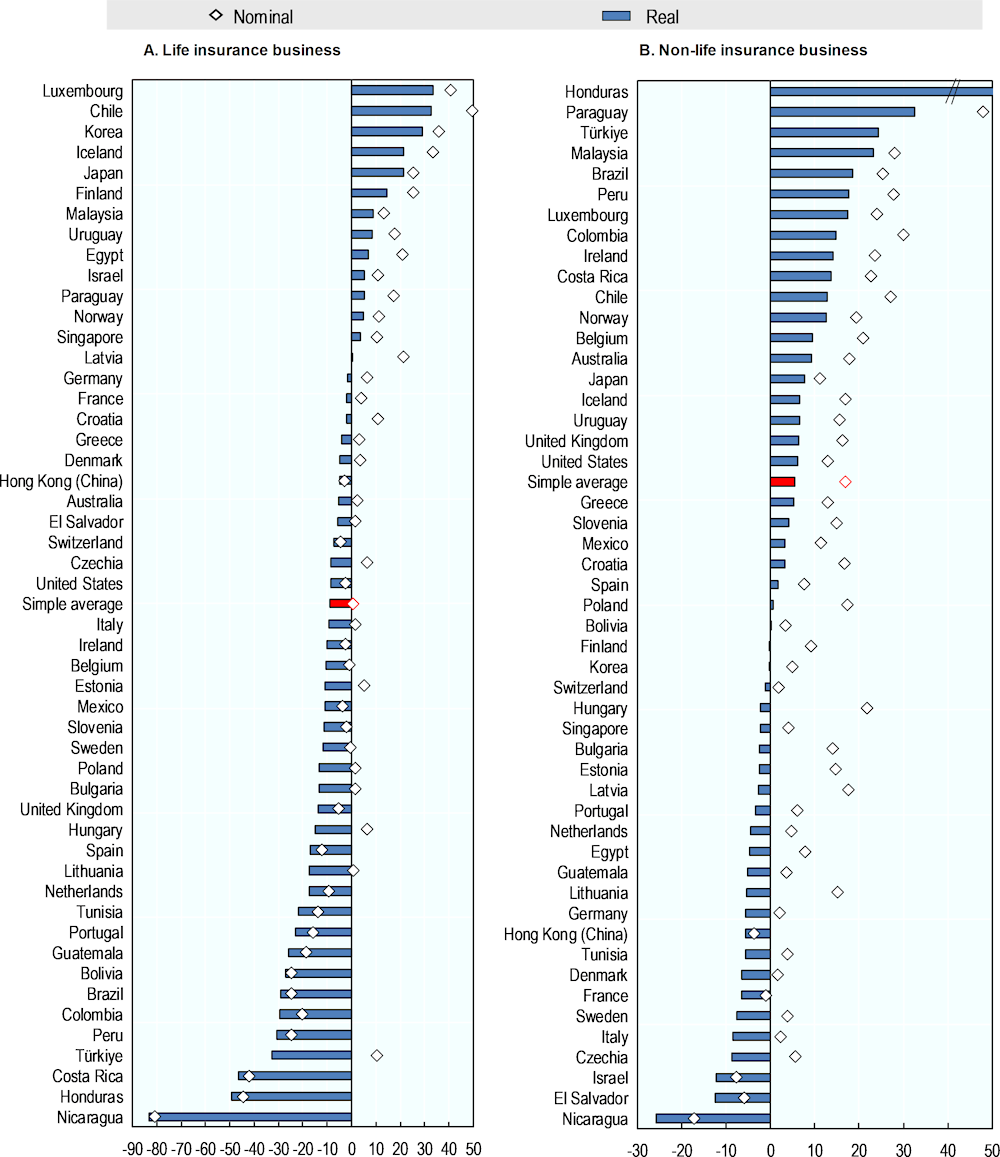

All in all, insurers still recorded higher premium volumes in nominal terms in 2022 than in 2021 on average, but lower in real terms. In many Latin American countries where life premium growth was strong in nominal terms, premium revenues remain positive in real terms. By contrast, those with low growth exhibited a decline in revenues in real terms, while inflation exacerbated the drop for those with an already declining revenue in nominal terms.