This chapter provides an overview of Germany’s green energy transition, the impact of the global energy crisis, key environmental trends and progress towards net zero. It assesses the environmental effectiveness and economic efficiency of the environmental policy mix, including regulatory and voluntary instruments; fiscal and economic instruments; and public and private investment in environment-related infrastructure. Finally, it examines the interaction between the environment and other policy areas with a view to highlighting opportunities and barriers to environmentally friendly and socially inclusive growth.

OECD Environmental Performance Reviews: Germany 2023

OECD Environmental Performance Reviews

1. Towards sustainable development

Abstract

1.1. Addressing key environmental challenges

Germany continued to improve its environmental performance over the past decade. Despite its important industry base and dense population, the country reduced several environmental pressures. Germany improved air quality and is one of the best performing countries in terms of sustainable waste management in Europe. It is working towards a more circular economy and more sustainable supply chains. It has decoupled economic growth from total energy supply and carbon dioxide (CO2) emissions generated by fuel combustion. However, the country’s energy mix still depends largely on fossil fuels, which accounted for about three-quarters of total energy supply in 2020. Germany has an ambitious climate policy and aims to reach climate neutrality by 2045 and achieve negative emissions after 2050.

Despite progress, the country faces multiple pressures on nature and water, threatening biodiversity and natural capital. Nitrate water pollution from agriculture remains a serious concern. The Baltic Sea and North Sea face acute problems with eutrophication. Many German water bodies failed to meet environmental objectives. Germany needs to strengthen efforts to improve water quality. Only about one-third of Germany’s forests have near-natural conditions and more than 90% of peatlands have been drained (BMUV, 2022[1]). The conservation status of species and habitats shows deteriorating trends. The impacts of climate change increasingly affect the country as demonstrated by the 2021 flood catastrophe. Germany is scaling up efforts to adapt and become more climate resilient (Chapter 2).

The economic downturn caused by the COVID-19 pandemic hit the economy hard, with gross domestic product (GDP) contracting by 3.7% in 2020. The economy recovered in 2021 (+2.6%) and was then again affected by the economic consequences of Russia’s unprovoked war of aggression in Ukraine, which resulted in a lower-than-expected real GDP growth of 1.9%. It is projected to recover slowly (0.3% in 2023 and 1.7% in 2024) (OECD, 2023[2]). In 2022, Germany recorded a high inflation rate of 8.8%. The crisis revealed structural weaknesses in Germany’s energy supply due to strong dependency on Russian oil and gas, obliging the federal government to rethink its energy strategy. However, the German economy has weathered the global energy crisis much better than expected (OECD, forthcoming[3]). As part of its energy crisis response, Germany has taken a series of measures, which are historic in size and scope. They are set to massively accelerate the green energy transition in the coming years.

1.1.1. Progress towards sustainable development goals

Germany ranked 6th of 163 assessed countries on the implementation of the 2030 Agenda for Sustainable Development (Sachs, J.D. et al., 2022[4]). The country has made progress in implementing the Sustainable Development Goals (SDGs) but faces many challenges, particularly related to SDG12 on responsible consumption and production, and SDG13 on climate action (Figure 1.1).

Germany has a high political commitment to support implementation of Agenda 2030 at home and abroad. In 2016, Germany incorporated the SDGs in the German Sustainable Development Strategy, including environmental indicators. The updated Sustainability Strategy of 2021 identifies six cross-cutting transformative areas, including climate action. It is one of few countries, which achieved the international target of dedicating 0.7% of gross national income to official development assistance (Section 2.4.3).

Under the co‑ordination of the Federal Chancellery, Germany applies a whole-of-government approach to support implementation of Agenda 2030. Every draft regulation or law requires the ministries to conduct an ex ante sustainability impact assessment (Federal Government, 2021[5]). Moreover, 11 Länder have adopted their own sustainable development strategies. Germany was one of the first countries to prepare Voluntary National Reviews within the broader Agenda 2030 process (2016 and 2021). Some Voluntary Local Reviews have also been elaborated. The 2022 Spending Review lays the groundwork to increase the focus on performance-based budgeting for sustainable development, which the government intends to develop in the coming years under the leadership of the Ministry of Finance (Section 1.3.5).

Figure 1.1. Germany is making progress in implementing Agenda 2030, but challenges remain

Note: The full title of each SDG is available here: https://sdgs.un.org/goals.

Source: Sachs J. D. et al. (2022), The Decade of Action for the Sustainable Development Goals, Sustainable Development Report 2021, https://dashboards.sdgindex.org.

1.1.2. Green energy transition

Initiated in the early 2010s, Germany’s green energy transition (Energiewende) aims at moving away from nuclear and fossil fuels towards renewables while promoting better energy efficiency. The transition is underway: Germany has decoupled economic growth from energy demand and CO2 emissions, and is one of the G20 and EU-27 countries with the highest levels of energy efficiency (Brüggemann, 2018[6]). The share of renewables has achieved remarkable growth over the past decade. The coal phase-out has been enshrined in the 2020 Act on the Phase-out of Coal-fired Power Plants. This contains a legally binding commitment for phasing out coal by 2038 at the latest, including targeted support to coal regions for the transition. In addition, the federal government committed to accelerating the process and completing the coal exit, ideally, by 2030. The three remaining nuclear power plants went off the grid in mid-April 2023, completing Germany’s decade-long nuclear exit (Box 1.2).

Despite progress, Germany will need to advance its energy transition at a much faster pace to secure a future that is “secure, environmentally friendly and economically successful” (BMWK, 2022[7]). More particularly, it needs to address three major challenges: i) ensuring energy security; ii) achieving national climate goals; and iii) developing the country’s economic competitiveness. Supply security has become a top priority of the government since the Russian invasion of Ukraine and the subsequent global energy crisis. Climate change is an overall leitmotif of the federal government’s coalition treaty; and rising economic competitiveness is at the heart of the country’s industry policy. However, Germany needs to find ways to advance the country’s structural transformation by addressing the triple crisis of energy, climate and biodiversity in an integrated way.

In practice, Germany faces several trade-offs. For example, emergency measures aimed at tackling energy price shocks and preventing gas supply shortage partly impede progress on climate and environmental goals (e.g. re-opening of coal energy plants; fuel price cuts; suspended 2023 increase of CO2 price for transport and buildings). While emergency measures are needed to ensure supply security and system stability, some of the government’s responses to the energy price shocks have reduced the impact of national climate policies. Given the pressing environmental and climate challenges, the country cannot afford any further delays in designing pathways towards a sustainable energy transition.

Reducing energy use

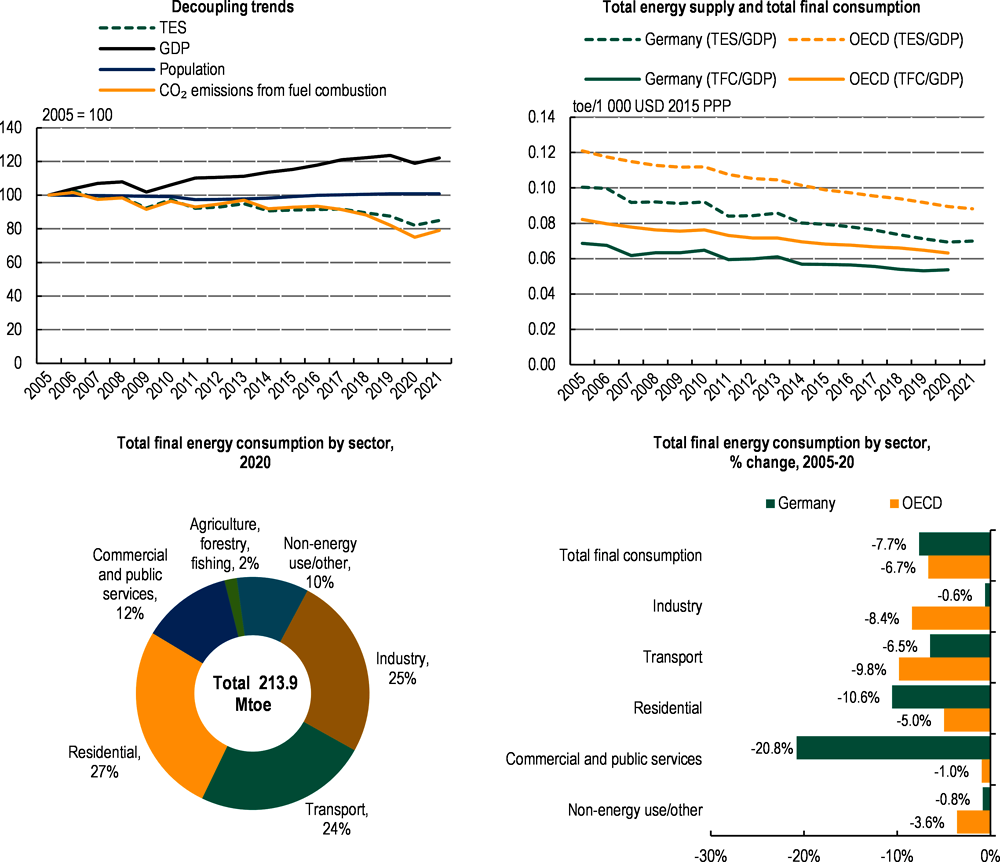

Improving energy efficiency has been a key pillar of the Energiewende. Germany has decoupled economic growth from energy demand and CO2 emissions. Total energy supply and final energy consumption are both decreasing while GDP has been growing (until COVID-19, Figure 1.2). In line with the OECD average, this resulted in a further decline in energy intensity. Energy use declined sharply in 2020 due to the pandemic and is expected to rebound in the coming years.

Figure 1.2. Germany has decoupled economic growth from energy demand and CO2 emissions

Note: TES = total energy supply. TFC = total final consumption. Gross domestic product (GDP) is expressed at 2015 prices and purchasing power parities; Toe = tonnes of oil equivalent.

Source: IEA (2022), IEA World Energy Statistics and Balances (database); IEA (2022), IEA World Greenhouse Gas Emissions from Energy (database).

The global energy crisis triggers an opportunity to advance energy efficiency. Energy savings of firms and households have been considerable: gas use in January 2023 was about 23% below the 2018-21 average (OECD, forthcoming[3]). Reducing energy consumption through technical improvements and behavioural measures is more critical than ever to help avoid mismatches between demand and supply (IEA, 2022[8]). To secure the supply of heat during the cold weather periods in 2023 and 2024, the federal government introduced additional energy saving measures on the basis of the Energy Security of Supply Act (Energiesicherungsgesetz, EnSiG) in August 2022.

Over the past decade, Germany significantly enhanced energy efficiency in the commercial, public services and residential sectors. Private households reduced their energy consumption by over 10%, mainly thanks to technological improvements (Figure 1.2). Some energy savings were also made in the transport sector. Meanwhile, energy consumption in the industry sector remained stable, which can be partially explained by increased energy consumption in the chemical industry. As a result, total final energy consumption decreased by 7.7% since 2005, above the OECD average of 6.7% (IEA, 2021[9]).

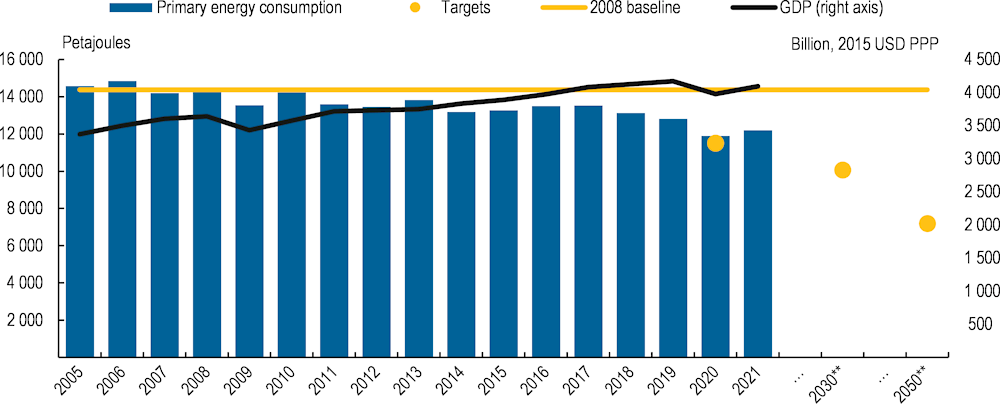

Figure 1.3. Germany has set ambitious energy saving targets

Source: IEA (2021), World Energy Balances; Eurostat (2022).

Germany did not meet its 2020 efficiency target of cutting primary energy usage by 20% relative to the 2008 level (Figure 1.3). However, it only narrowly missed the mark thanks to a sharp consumption drop in 2020 related to COVID-19. Technical efficiency gains were offset by rising energy demand (e.g. economic growth, higher traffic volume, changes in lifestyle and consumption patterns). More efforts will be needed to sustainably reduce energy consumption in absolute terms to meet Germany’s national climate and energy targets. To close the energy savings gap, new measures need to focus on current bottlenecks such as the renovation of building stock (Section 1.3.2). The electrification of the transport sector will also greatly contribute to efficiency gains.

The federal government has set itself the goal of “making Germany the most energy-efficient economy in the world” (BMWK, 2020[10]). Germany’s Energy Efficiency Strategy 2050 sets out a long-term pathway for strengthening German energy efficiency policy (BMWK, 2020[10]). Ambition was further raised with a new goal of reducing energy consumption by 30% in 2030 and by 50% in 2050, compared to 2008 levels. The national strategy includes primary and final energy targets, and is supported by a nationwide dialogue process. Targets should be compatible with national climate goals and will need to be adjusted to the revised EU Energy Efficiency Directive. The federal government advanced work on a national Energy Efficiency Law in parallel to the now concluded EU process. Many measures and instruments under the National Energy Efficiency Action Plan (NAPE 2.0) contribute to cutting CO2 emissions, including private sector networks (Box 1.1).

Box 1.1. Policies in practice: Energy efficiency and climate action networks

Building on a Swiss initiative, Germany has developed a network approach to promote systematic information-sharing and mutual learning on energy efficiency and climate action in a simple and non-bureaucratic way. A network (Effizienznetzwerk) typically brings together 8-15 businesses, which set joint energy and climate targets and work together towards achieving them.

To date, more than 350 energy efficiency networks bring together industry, trade and skilled crafts from over 3 000 companies across the country. This is fewer than the 500 networks announced for 2020 in 2014. However, these networks have been instrumental in working together towards achieving joint energy and climate targets. By 2025, some 300-350 networks shall work together towards saving 9-11 terawatt hours, as well as 5-6 million tonnes of CO2-eq emissions.

Many networks outperformed initial goals and its members benefit from experience from other companies and greater visibility, making changes more socially acceptable. The initiative compiled a series of success stories from various sectors across the country. Other countries are now developing similar initiatives.

Source: Effizienznetzwerke: www.effizienznetzwerke.org.

Mandatory measures, such as energy audits or energy management schemes, will apply to businesses. Data centres will be required to re-use 40% of their waste heat. The federal government provides EUR 1 billion for energy-efficient measures, including for digital modernisation across its public administration and within companies. Public authorities at all government levels are required to participate more strongly in saving energy according to their respective size. Households receive energy saving tips through an information campaign called “80 million together for energy change”.

The systematic approach of introducing energy-saving measures at all levels goes in the right direction and will help Germany reduce energy losses while reducing reliance on fossil fuels. However, more targeted support will be needed to promote system change such as helping vulnerable households to replace natural gas heating systems and gas boilers with climate-friendly alternatives (Section 1.3.2). Germany could also harness behaviour-related efficiency potential to a much greater extent (e.g. incentives for shared mobility, reduced heating temperatures in buildings) (ERK, 2022[11]).

Decarbonising the energy mix and the nuclear exit

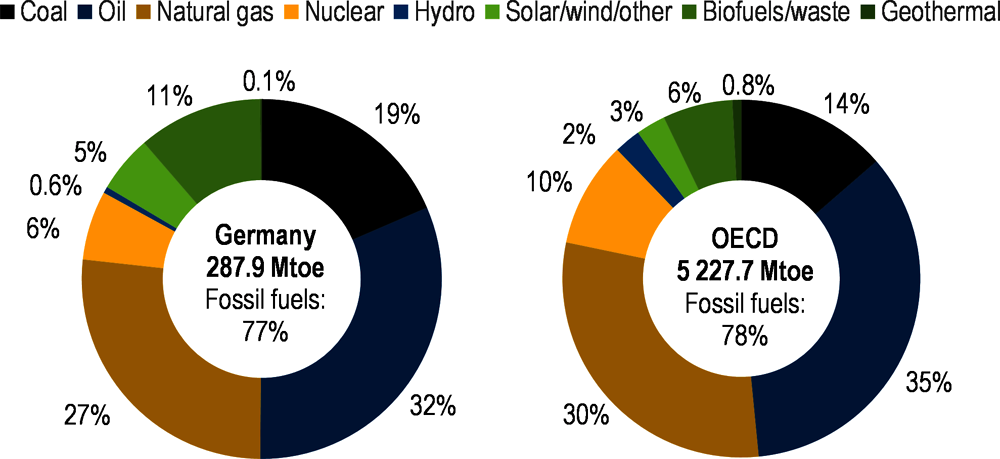

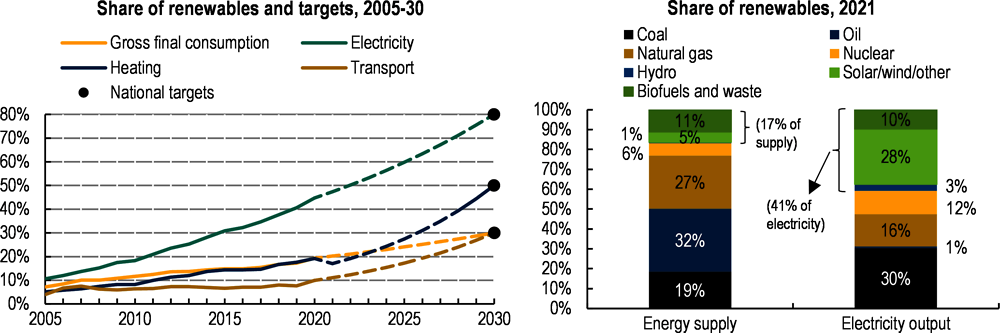

Despite massive investments in renewables, Germany’s energy mix remains dominated heavily by fossil fuels, representing about three-quarters of total energy supply (Figure 1.4). This is about the same share as a decade ago. Oil and gas remain the main sources of Germany’s total energy supply. The expansion of renewables mainly contributed to fill the gap created by advancing the nuclear power phase-out (Box 1.2). As a result, Germany will need to expand renewables at a much broader scale to further decarbonise its energy mix (Box 1.3).

Figure 1.4. Total energy supply remains carbon intensive despite increases in renewables

Note: Data refer to 2021. The breakdown of energy supply excludes heat and electricity trade, but percentages shown reflect ratios calculated on total energy supply. Biofuel and waste include negligible quantities of non-renewable waste.

Source: IEA (2022), IEA World Energy Statistics and Balances (database).

Box 1.2. Germany’s nuclear exit

Germany’s energy transition places great emphasis on phasing out nuclear power by 2022, as stipulated in an amendment to the Atomic Energy Act. The decision in 2011 following the Fukushima Daiichi nuclear power plant accident in Japan. The nuclear exit has received widespread public support and political consensus to some degree. However, Germany's nuclear phase-out has been and will continue to be debated in light of energy supply and security challenges. For instance, in response to the global energy crisis, the federal government temporarily extended operations of the three remaining nuclear power reactors (Isar 2, Neckarwestheim 2 and Emsland) to offset reduced gas supply from the Russian Federation. The three plants were shut down in mid-April 2023, effectively completing Germany's decade-long nuclear phase-out.

Germany will still need to deal with a sizeable amount of nuclear waste. The country has licensed the former Konrad mine in Salzgitter in the state of Lower Saxony as a repository for low- and intermediate-level waste from the spent nuclear fuel of its past nuclear programme. The site is scheduled to start operations in 2027. For high-level waste, Germany is seeking a final repository since the Gorleben salt dome was ruled out as a potential site.

Phasing out of nuclear energy leaves Germany the challenge of ensuring a stable and reliable, low-carbon energy supply in both the short and long term. Without more reliance on fossil fuels, the country’s shift towards renewable energy sources such as wind and solar power will pose significant challenges for the stability and security of the power grid.

Germany’s nuclear phase-out takes place in a changing context for nuclear energy worldwide. Several countries continue to invest in the expansion of nuclear power. For example, Japan recently moved to promote use of nuclear energy to achieve net zero by 2050. It intends to restart as many reactors as possible and extend the lifespan of existing reactors beyond 60 years. Similarly, in February 2023, 11 countries of the European Union (Bulgaria, Croatia, the Czech Republic, Hungary, Finland, France, the Netherlands, Poland, Romania, Slovakia and Slovenia) launched a nuclear alliance. They aim to promote nuclear energy as an important tool for achieving net-zero objectives in the European Union. In 2022, France committed to building at least six large reactors.

Source: NEA (2023), www.oecd-nea.org.

Energy security

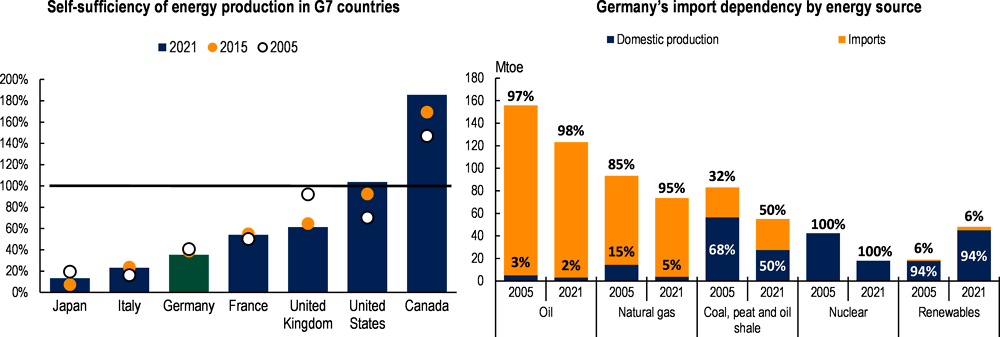

Germany relies heavily on fossil fuel imports, which represent more than 60% of its total energy supply, slightly above the European average (Figure 1.5). The country completely depends on imports for critical minerals and metals for development of renewable energy sources. This makes it vulnerable to economic fluctuations and geopolitical issues (Box 1.10). At the crossroads of European energy infrastructure, Germany advocates for common European solutions to address the European-wide energy crisis. It would greatly benefit from deeper integration of the European market.

The Russian invasion of Ukraine on 24 February 2022 and the successive global energy crisis obliged the German government to rethink its energy strategy. The energy crisis revealed structural weaknesses of Germany’s energy supply due to strong dependency on Russian oil and gas. The country’s past energy policy has been criticised for being “short-sighted” because it underestimated the supply security risks related to the geopolitical realities of its policy on the Russian Federation.

However, the federal government has quickly adjusted to new realities by diversifying its supply sources to ensure security of supply (Box 1.3). Measures include filling up gas storage tanks (with the highest storage obligations in the EU), negotiating liquefied natural gas (LNG) trade deals, temporarily re-opening coal plants and raising public awareness on energy saving. Gas storages had been fully filled in October 2022 and stood at 77% in early February 2023, thanks notably to a relatively mild winter (OECD, forthcoming[3]). Direct imports from Russia to Germany through Nord Stream 1 and 2 gas pipelines have stopped.

Figure 1.5. Germany depends heavily on imported fossil fuels

Note: Self-sufficiency is defined as energy production divided by total energy supply, e.g. how much of the energy supply is produced domestically.

Sources: IEA (2022), World Indicators (database); IEA (2023), World Energy Balances (database); BGR (2022).

Box 1.3. Moving away from fossil fuels

Reducing oil dependency

Oil remains Germany’s most important primary energy source covering nearly a third of the country’s energy mix (IEA, 2023[12]) The country has almost no domestic oil production and depends heavily on imports. Prior to its war in Ukraine, the Russian Federation delivered most of Germany’s oil supply via the Druzhba pipeline. Overall, the oil market is more globalised than the gas market and it is thus easier to diversify supply sources. Germany will need to further enlarge the range of oil suppliers while reducing demand through transport electrification, alternative fuels and energy efficiency measures.

Alternative gas supplies – Liquefied natural gas

Gas represents about a quarter of Germany’s energy mix and is the second most-consumed energy source after oil. Over 90% of gas is used in Germany’s heating sector. About 44% of private households use gas to heat their homes (BMWK, 2023[13]). In response to the energy crisis, the federal government adopted legislation to ensure minimum levels of gas in storage. It commissioned two public LNG terminals that were built within less than a year; in total, six LNG terminals should be operational by winter 2023-24 (LNG Acceleration Act). The total import capacity of these units represents about one-third of previous gas imports from the Russian Federation. While Germany should be commended for acting swiftly, the rapid construction of terminals came at a price (EUR 6.6 billion), more than twice as much as initially scheduled. Against the backdrop of Germany’s energy transition, there is a risk of stranded assets. The federal government should therefore carefully assess import needs to avoid overcapacity. It should also lead a transparent discussion on costs, conditions and length of contracts. This would ensure that Germany implements this emergency response in a manner consistent with its climate objectives and without creating lock-in effects (G7, 2022[14]). The LNG Acceleration Act underlined that LNG infrastructure use beyond 2043 should be allowed only for facilities that produce climate-neutral hydrogen and its derivatives.

Coal phase-out

Germany has a legally binding goal for coal phase-out by 2038 at the latest. In response to the energy crisis, the federal government agreed on a temporary market return of 10.4 gigawatts of hard coal, lignite and oil-fired reserve capacity. Two lignite power plants of RWE, Germany’s biggest power producer, will remain on the market until March 2024, 15 months longer than originally scheduled. This will contribute to increasing the country’s CO2 emissions in the short term. In turn, the federal government brought forward the lignite phase-out in the western coal mining area of the state of North Rhine-Westphalia to 2030 – eight years ahead of the national commitment of 2038. This partly delivers on the coalition treaty’s promise to accelerate the phase-out of coal and achieve it “ideally” by 2030. According to government sources, the early anticipation of coal phase-out in this area would contribute to saving 280 million tonnes of CO2. Coal remains, however, a major source of electricity generation in Germany. The country is one of the world’s biggest coal users, with the largest per capita consumption. Germany’s coal phase-out also has major social impacts on employment (OECD, forthcoming[3]).

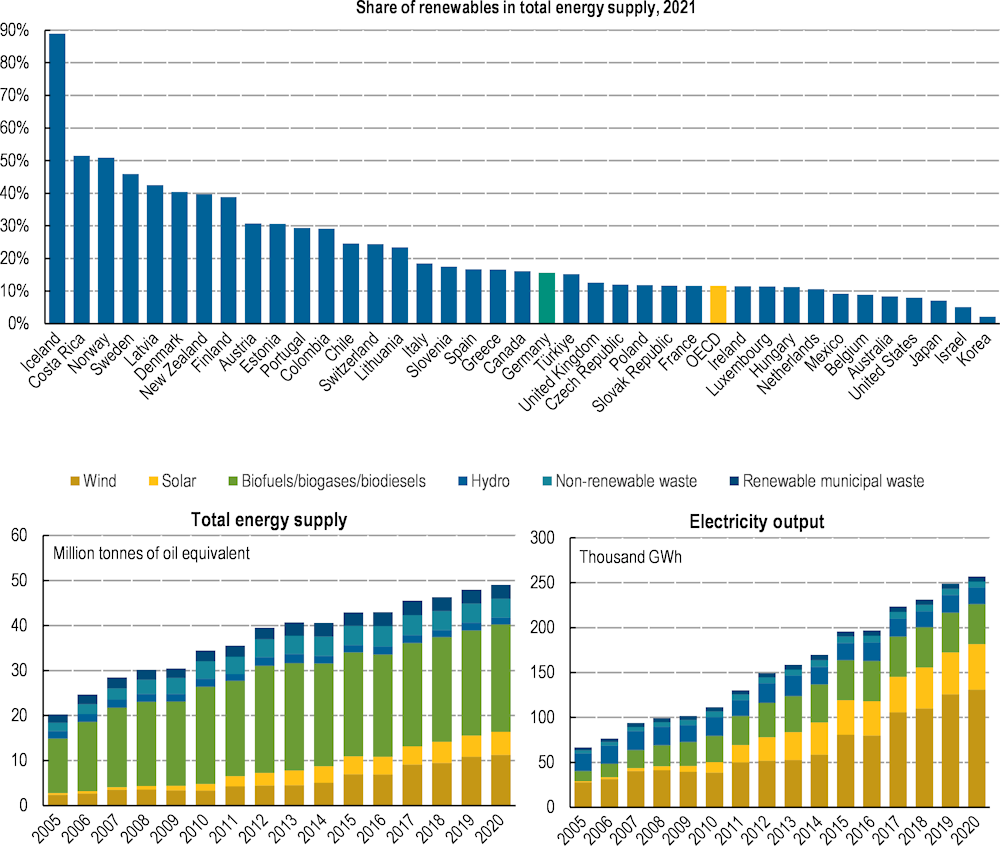

Expansion of renewables

While the share of renewables in total energy supply remains modest (17%) (Figure 1.6), Germany has achieved remarkable growth in renewable electricity over the past decade; it represented 41% of electricity outputs in 2021 (Figure 1.7). To date, bioenergy still represents the largest part of renewables in total energy supply. Solar energy has been boosted across the country since the early 2010s. Wind energy has nearly tripled since 2010. Germany has the biggest wind onshore capacity in Europe. The total installed capacity was 57 gigawatts (GW) onshore and 7.8 GW offshore in 2022. The federal government aims to double wind onshore capacity to 115 GW and reach a 30 GW offshore wind target in 2030 (Table 1.1). The renewable energy forecasts for 2022-27 are optimistic, projecting major increases in solar photovoltaic and onshore wind (IEA, 2022[15]).

Figure 1.6. Germany’s share of renewables has been growing and is above the OECD average

Note: Biofuels/biogases/biodiesels include biogasoline, biodiesels, other liquid biofuels and solid biofuel excluding charcoal, biogases and bio jet kerosene.

Source: IEA (2022), IEA Renewables Information (database).

The Easter Package 2022 lays out ambitious targets and makes significant changes to the country’s regulatory framework. This includes measures to introduce higher auction volumes and accelerate lengthy and complex permitting procedures, a major barrier for onshore wind development. The 2023 Renewable Energy Sources Act (EEG 2023) sets a new legally binding target to increase the share of renewable energy sources to 80% of electricity consumption by 2030 (previously at 65%). In addition, the share of renewables should reach 30% of gross final energy consumption, 50% of heating, and 30% of transport (Figure 1.7). The Federal Ministry for Economic Affairs and Climate Action is working on measures to accelerate the decarbonisation of heating and cooling, aiming to increase the share of carbon-neutral heating to 50% by 2030 (NAPE 2.0).

Figure 1.7. Germany has set ambitious targets for renewables

Note: Data refer to 2021. The breakdown of energy supply excludes heat and electricity trade, but percentages shown reflect ratios calculated on total energy supply. Biofuel and waste include negligible quantities of non-renewable waste.

Source: IEA (2022), IEA World Energy Statistics and Balances (database); Eurostat (2023) Energy database.

Table 1.1. New targets and measures for the expansion of solar and wind power

Source: Easter Package (2022) and draft laws.

These are ambitious goals. In addition to doubling use of green electricity, Germany must also respond to rising electricity demand due to the ongoing electrification of the transport and building sectors. The development of renewable energy becomes an “overriding matter of public interest” (BMWK, 2022[16]). This means that renewable energy will be given priority in decisions. In parallel, the federal government will need to address bottlenecks related to the electricity grid, the skills gap and supply chain risks.

Building a climate-neutral electricity grid

Reaching the renewable energy targets will require massive investment in the modernisation and expansion of electricity grids and energy infrastructure. Some EUR 32 billion and EUR 110 billion would be needed by 2030 and 2050, respectively, to expand and modernise Germany’s electricity grid (E.ON, 2020[17]). Without substantive long-term investment, Germany will face blockages related to overloaded networks that can no longer absorb electricity from renewable energy sources. Grid-stabilising costs could triple from EUR 1.4 billion in 2017 to EUR 4.2 billion per year by 2050 (E.ON, 2020[17]).

Building a climate-neutral electricity grid is complex, given the large and growing number of small, decentralised power plants and new needs related to e-mobility and climate-friendly heating systems. A spatially more equally distributed deployment of onshore wind power would help ease pressure on the power grid by favouring local usage. Digitalisation (e.g. smart meters) will also play a key role in better managing electricity flows over time and space.

The 2019 Grid Expansion Acceleration Act set targets, including connections to channel energy surpluses from wind power in the north to the major power consumption regions in the west and south. However, progress has been slow, mainly due to complex planning and approval procedures. According to the Federal Network Agency, less than 2 000 kilometres (km) of the planned 12 250 km length of priority grid expansion projects were operational at the third quarter of 2021. The large majority of expansion projects (9 700 km) were still in the planning and approval phase (BMWK, 2022[16]). Grid expansion raised concerns – among others – over soil damage and related compensation measures for farmers and citizens.

In 2022, the federal government approved new measures to simplify and accelerate planning, while ensuring more equally distributed onshore wind power (Table 1.1). Planning responsibility was transferred from state to federal level to streamline the process and avoid fragmentation of tasks. All new power network planning must contribute to building a climate-neutral grid. Getting citizens on board through increased local participation and community benefits from wind farm development, could help gain local support and reduce the number of legal appeals.

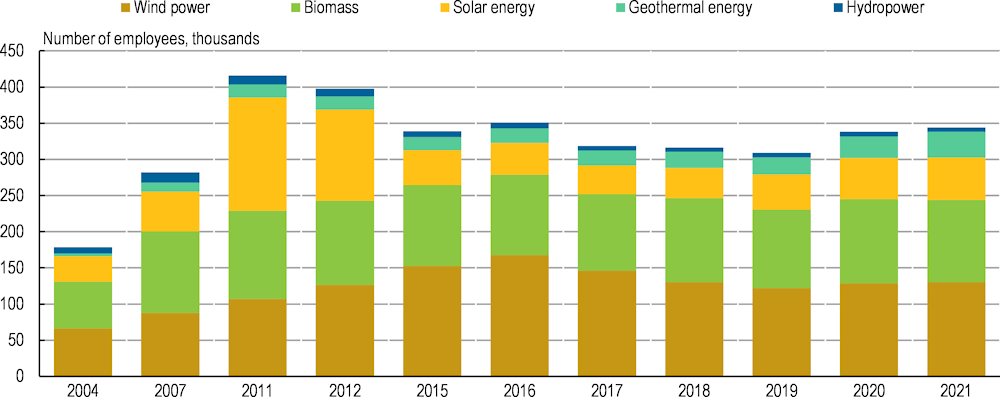

Addressing the skills gap

Germany also needs to urgently address the shortage of skilled labour across the renewable energy sector, which lacks more than 200 000 workers (electricians, heating and air-conditioning technicians, IT specialists) (Monsef and Wendland, 2022[18]). The number of employees in the renewable energy sector decreased by 17% between 2011-21 (Figure 1.8). Green jobs have mainly been lost in the solar industry due to global competition, notably with Asia. Despite massive public investment in innovation to build the German solar industry, the country has no longer any major solar panel or cell manufacturer. A similar trend occurred in the wind power industry a couple of years later. To date, skilled workers are mainly missing in the building sector to advance climate-friendly solutions.

The trend in green employment was reversed as of 2020 thanks to the Skilled Immigration Act, which entered into force in March 2020. It provides the legal framework to facilitate immigration of skilled workers from non-EU countries, including a fast-track procedure. However, many administrative hurdles remain, such as recognition of qualifications and language requirements.

Figure 1.8. The number of employees in the renewable energy sector is slowly growing again

Notes: data for 2021 is preliminary.

Source: German Environment Agency (2023), Environmental Indicators.

A new Skilled Immigration Act is under discussion. It aims to further simplify and accelerate administration, while make working and living conditions more attractive to facilitate immigration of skilled workers at a much larger scale. A new points system may open the door to third-country nationals with “good potential” to come to Germany to seek a job. To date, foreigners need a contract offer. An online portal, “Make it in Germany”, provides information for qualified skilled workers from abroad. It is also crucial to expand adult learning opportunities and support the labour market integration of women. The gender divide in green jobs is particularly strong in Germany. Women make up 26.9% of workers in green-task jobs, compared to 28.3% across the OECD (OECD, 2023[19]).

1.1.3. Progress towards net zero

National and international climate targets

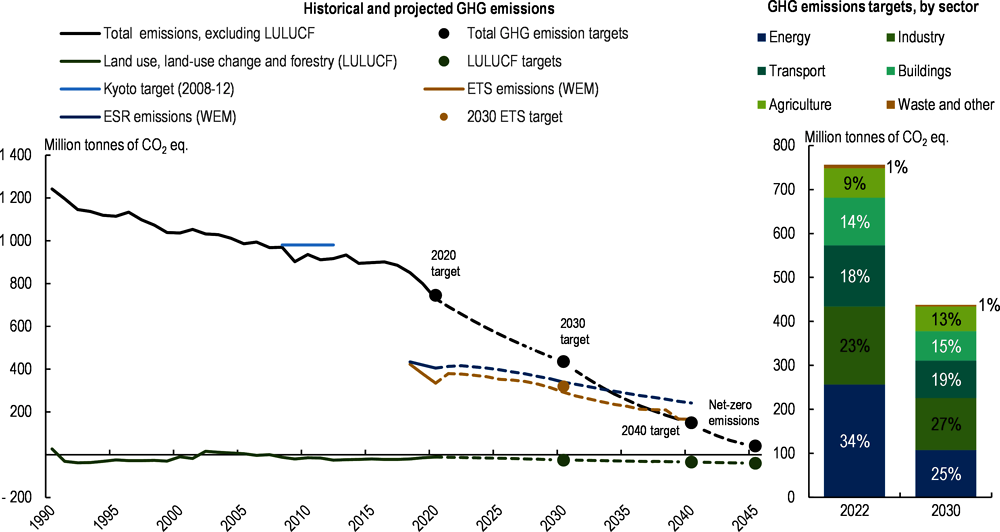

Germany has ambitious climate policies, and the federal government has recently further raised these ambitions. The federal government intends to massively expand renewable energy, increase energy efficiency and develop a climate-neutral industrial policy. Germany has set an economy-wide greenhouse gas (GHG) emission reduction target of at least 65% by 2030 and at least 88% by 2040. The country aims to be climate neutral in 2045 (five years earlier than the EU target) and achieve negative GHG emissions after 2050 (Figure 1.9). National targets are enshrined in the Federal Climate Change Act, which was approved in 2019 amended in 2021. In parallel, the federal government also aims to increase the contribution of the land use, land-use change and forestry (LULUCF) sector to reach carbon removals of at least -25 million, -35 million and -40 million tonnes of CO2-equivalent (Mt CO2-eq.) by 2030, 2040 and 2045, respectively (Section 2.3.2). Moreover, some Länder have set more ambitious subnational climate goals. For example, the state of Baden-Württemberg aims to become climate neutral in 2040. To that end, it approved a Land-level Climate Protection Act in February 2023, covering mitigation and adaptation efforts.

Germany’s climate policy is aligned with EU climate legislation, including the EU Emissions Trading System (ETS), the Effort Sharing Regulation, and transport and land-use legislation. Emissions reduction targets under the EU Effort Sharing Regulation (covering the non-ETS sector) are legally binding. Within the Europe’s Fit-for-55 package, its national emissions reduction targets in non-ETS sectors shall be raised from -14% in 2020 to -50% by 2030, compared to 2005 levels.

Figure 1.9. Germany needs to accelerate climate action to reach its 2030 and 2045 climate targets

Note: ESR = effort sharing regulation. ETS = emissions trading system. WEM = with existing measures. Dashed lines represent projections (linear to targets in the case of total emissions and LULUCF).

Sources: EEA (2022), Member States' Greenhouse Gas Emission Projections (database), www.eea.europa.eu/data-and-maps/data/greenhouse-gas-emission-projections-for-8; EEA (2022), European Union Emissions Trading System (EU ETS) data, www.eea.europa.eu/data-and-maps/data/european-union-emissions-trading-scheme-17; OECD (2022), Greenhouse gas emissions by source, OECD Environment Statistics (database); Federal Climate Change Act (2021), GHG annual emission budgets by sector.

On the international scene, Germany encourages stronger alliances for progress on climate protection. Within its G7 presidency in 2022, the country initiated an international Climate Club to help define common standards for emission measurements and carbon pricing, among other goals (Box 1.4). Moreover, Germany is a major provider of global climate finance, contributing to fulfilling the collective USD 100 billion goal (Section 2.4.3).

Box 1.4. The international Climate Club

Upon Germany’s initiative, G7 countries proposed in December 2022 the terms of reference for an open and co-operative international Climate Club. Work will be led by a Task Force, chaired by Germany and Chile, with an interim secretariat assumed in tandem by the OECD and the IEA. The Climate Club is set to be formally launched in 2023. The Climate Club will provide a “high-ambition intergovernmental forum for discussion and serve as an enabling framework for increased co-operation, improved co-ordination and potential collective action” (G7 Germany, 2022[20]). It advocates for a socially just transition of industries towards climate neutrality. Beyond G7 countries, developing and emerging countries are invited to join the initiative.

The Climate Club is built on three thematic pillars:

Advancing ambitious and transparent climate change mitigation policies

Transforming industries

Boosting international climate co-operation and partnerships.

Initial focus will be placed on the second pillar to unlock potential for the decarbonisation of hard-to-abate industrial sectors and counter the risk of carbon leakage. The Club intends to accelerate work on joint standards, methodologies and strategies for industrial sectors. For example, climate-friendly commodities, such as green steel, could enter the market more quickly and be ramped up globally.

Source: (G7 Germany, 2022[20]).

Climate governance and finance

Since end 2021, four key federal ministries have shared the main responsibilities for climate action at the federal level: the Ministry for Economic Affairs and Climate Action (BMWK), the Ministry for the Environment, Nature Conservation, Nuclear Safety and Consumer Protection (BMUV), the Foreign Office, and the Ministry for Economic Co-operation and Development (BMZ). Climate mitigation has received increased policy attention through its integration into the BMWK, while climate change adaptation remains a core responsibility of the BMUV. The Federal Foreign Office is responsible for climate change negotiations; and the BMZ manages Germany’s global climate finance for emerging and developing countries. However, climate action is mainstreamed in all government sectors and many other ministries and local governments take part in the implementation of climate action in respective work areas. A Climate Cabinet facilitates inter-ministerial co‑ordination and monitors the effectiveness, efficiency and target accuracy of new measures. Climate measures are mainly implemented at Länder level. Implementation is also supported by the German Environment Agency (Umweltbundesamt), and research institutes. An independent Council of Experts on Climate Change (Expertenrat für Klimafragen), created in 2019, assesses annual GHG emission trends and the effectiveness of measures. It also advises the federal government on implementation of the Federal Climate Change Act.

According to the Ministry of Finance, over EUR 80 billion was earmarked for climate action investment under the Climate Action Programme and the economic stimulus package for 2020 and 2021. In 2022, the Energy and Climate Fund was transformed into a new Climate and Transformation Fund (Klima- und Transformationsfonds, KTF), with a budget of about EUR 178 billion for 2023-26, including EUR 36 billion for 2023. The fund mainly focuses on the building sector, electric mobility, hydrogen development and energy efficiency. The federal government underlines the need for a specific instrument to respond more flexibly to its climate protection target and finance climate change mitigation efforts. However, this means that climate action is financed through various funding sources (e.g. federal budget, KTF, sector-specific programmes, Länder-level funds, EU funds). Spending efficiency could be raised through better use of spending reviews and policy impact evaluation (OECD, forthcoming[3]).

Box 1.5. Policy framework for Germany’s climate action, 2014-23

2014 Climate Action Programme 2020, focusing on its national goal to reduce GHG emissions by at least 40% in 2020 compared to 1990 levels.

2016 Climate Action Plan 2050 (Klimaschutzplan 2050), including sector-specific mitigation targets.

2019 Federal Climate Change Act (Bundes-Klimaschutzgesetz, KSG) with legally binding emission goals by 2030 under the EU Effort Sharing Regulation and in line with the Paris Agreement. It introduced so-called immediate action programme (Sofortprogramme) and a Council of Experts on Climate Change (Expertenrat für Klimafragen).

2019 Climate Protection Package 2030 (Klimaschutzprogramm 2030) to translate the goals of the Climate Action Plan 2050 into practice; it includes, among other climate policies, a carbon pricing system for transport and heating.

2019 Creation of a “Climate Cabinet” (Klimakabinett) by the German Chancellery bringing together ministries of the environment, economics, finance, transport, agriculture and the interior.

2021 Germany’s Federal Constitutional Court rules parts of the Federal Climate Change Act unconstitutional arguing that emission reduction targets “lack sufficient specifications for further emission reductions from 2031 onwards”.

2021 German Parliament (Bundestag) approves amendment to the Federal Climate Change Act, increasing annual reduction targets per sector from 2023-30 and enshrining annual reduction targets for 2031-40 into law (Box 1.6)

2021 Immediate Climate Action Programme for 2022, supported by an additional EUR 8 billion.

2023 Approval of EUR 4 billion Federal Action Programme on Nature-Based Solutions for Climate and Biodiversity

2023 Federal Climate Change Adaptation Act (under development) (Chapter 2).

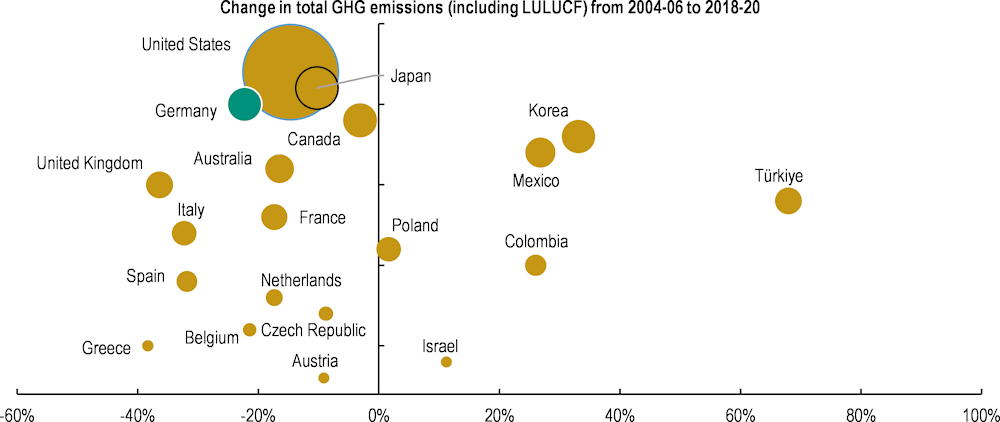

Figure 1.10. Germany has decreased emissions but remains among the top OECD emitters

Note: Total GHG emissions including Land Use, Land-Use Change and Forestry (LULUCF), top 20 OECD emitters. Data is expressed as averages of the periods 2004-06 and 2018-20.

Source: OECD (2022), Greenhouse gas emissions by source, OECD Environment Statistics (database).

Mitigation trends and sectoral targets

A historic emitter, Germany produces about 2% of global emissions and is still among the ten largest GHG emitters in the world (Figure 1.10). In 2020, the country managed to reduce its emissions by 41.3% compared to 1990 levels (or 729 Mt CO2-eq), meeting its 40% target for 2020. This is one of the strongest records of emission reductions in the OECD. However, emission reductions related to the COVID-19 pandemic proved to be only temporary and have quickly been reversed. Moreover, the temporary increase of coal-fired electricity generation will further increase the gap between recorded emissions and targets. The federal government aims to get back on track from 2024 and will need to accelerate new climate measures to achieve its ambitious 2030 targets. To that end, it will need to assess the short- and medium-term impact of energy emergency measures, update GHG projections and develop additional climate measures to fill the gaps on its pathway towards net zero.

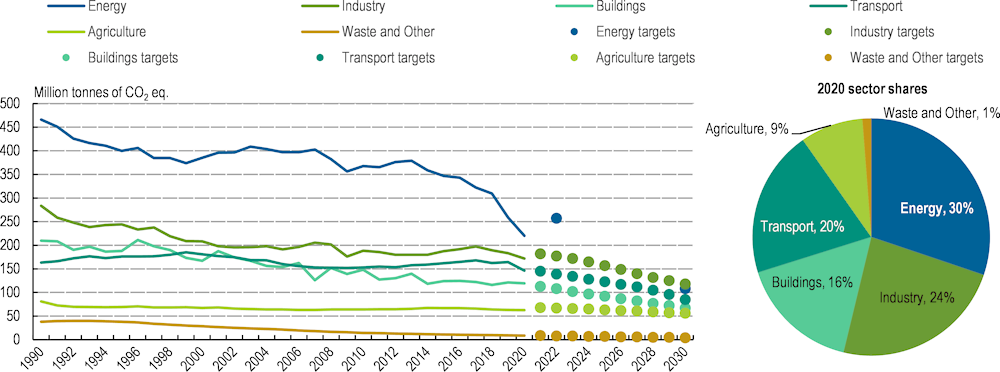

Energy industries remain the largest GHG emitter but have managed to halve emissions since 1990 (Figure 1.11). Reductions were due to a shift towards a less carbon-intensive energy mix and gains in energy efficiency. Emissions from transport, the second largest emission source, have increased by about 3% since 2005, accounting for 20% of Germany's GHG emissions in 2020. Road transport remains the primary driver of transport emissions. Emissions from agriculture (9% in 2020) have been relatively stable during the past decade, recording only a slight decrease. Methane from animal husbandry and nitrous oxide from agricultural soils are the main sources of emissions. Livestock represents about half of Germany’s agriculture emissions. The building sector has missed its sectoral target for the second time in 2021. About three-quarters of emissions come from residential buildings. Germany developed a long-term renovation strategy in 2020 to accelerate building renovation (Section 1.3.2).

Figure 1.11. Germany is on track to meet its sectoral GHG targets, except transport and buildings

Source: UNFCCC (2022), Inventory submissions.

Under the EU Effort Sharing Regulation, adopted in 2018, Germany needs to comply with binding annual targets for emissions outside EU emission trading (agriculture, buildings, small industries installation, transport and waste management). This means that if Germany misses these binding targets, it may need to purchase surplus emission rights from other countries. Between 2013 and 2020, Germany missed climate targets in key sectors, notably transport and buildings. To comply with its commitment, Germany had to purchase emission allowances under the EU Effort Sharing legislation. A lack of sector-specific progress will demand acquiring offsets, which will have significant financial consequences (OECD, 2022[21]).

In addition, the federal government has set up national annual CO2 emission budgets for six sectors until 2030, along with a monitoring and policy adjustment mechanism (OECD, 2022[21]) (Box 1.6). Four sectors (energy, industry, agriculture, waste and other) achieved sector-specific annual reduction targets in 2021; transport and buildings did not meet their respective national annual budgets. The federal government prepared immediate action programmes to correct the trajectories of these two sectors. However, additional measures will be necessary to make faster progress in these two sectors (Sections 1.1.4 and 1.3.2).

Box 1.6. Policies in practice: Germany’s annual sectoral emissions targets

The Federal Climate Change Act defines quantified, annual greenhouse gas (GHG) emissions reduction targets for six individual sectors: energy, (small) industry, buildings, transport, agriculture, and waste and others. The targets are set in line with the European GHG reduction plans, following a linear trajectory. The pace of emissions reductions varies by sector, and the amendment of 2021 tightened targets for each sector until 2030 (Table 1.2). Some federal states have also set sector-specific targets at Länder level.

The Federal Climate Change Act introduced a mandatory emissions monitoring mechanism in which sectoral emissions are assessed annually. If a sector fails to meet its annual target, the responsible ministry must prepare an immediate action programme (Sofortprogramm), which is assessed by the independent Council of Experts on Climate Change and then presented to the German Parliament. The policy adjustment mechanism aims to ensure that corrective action is taken on time and that all ministries play their part in national climate efforts. However, at a coalition meeting in March 2023, government parties agreed to soften the policy adjustment mechanism of annual sectoral targets. In future, sectoral targets may become less stringent, as long as total annual GHG emission budgets across sectors are being met. This means that lack of progress in one sector can be counterbalanced by strong emission reductions in another sector.

While climate action has been mainstreamed in nearly all policy areas, some sectors face more difficulties to reconcile sectoral objectives with climate targets. A sector-based approach is thus useful to monitor and measure progress towards achieving annual emissions reduction targets at sector level. Sector-specific climate action also contributes to much-needed transformative change with broader environmental benefits. However, harmonised carbon prices could be an even more efficient way to address significant differences in abatement costs across sectors. If Germany sets a cap in its non-ETS sectors in line with its overall target to reduce emissions, the sectoral targets may be less critical because the emission reduction will occur where abatement costs are lowest (OECD, forthcoming[3]).

Source: OECD (2022), Germany’s annual sectoral emissions targets, IPAC Policies in practice.

Table 1.2. Permissible annual emission budgets per sector

Annual emission budgets in millions of tonnes of CO2-eq

Source: Federal government (2021), Federal Climate Change Act.

1.1.4. Sustainable mobility

The decarbonisation of Germany’s transport sector is not on track. Road transport is responsible for nearly all transport-related emissions. Passenger cars represent the bulk of transport-related emissions at 60%; freight accounts for about one-third. Emission reduction efforts have been counterbalanced by the rising number of cars (Figure 1.12) and more traffic from heavy duty trucks. The sector missed its 2021 CO2 emission reduction targets by 3 Mt CO2-eq. The independent Council of Experts on Climate Change judged the proposed immediate action programme to be “insufficient” (ERK, 2022[11]).

Germany faces gaps both for ambition and implementation. Many opportunities such as broader use of speed limits, tolls for passenger and light duty vehicles, congestion charges in urban areas have not been taken; others, such as increased parking fees, are slowly materialising. A general speed limit of 120 km/h or 130 km/h on federal motorways would reduce emissions by 2.6 and 1.9 MtCO2-eq. per year, respectively (UBA, 2020[22]). While electric mobility will play a key role in decarbonising transport, Germany should not aim to replace each petrol- and diesel-fuelled car with an electric vehicle.

Germany will need to take bold action to move from individual policy measures mainly focused on “making cars cleaner” to an integrated mobility strategy for net-zero systems by design (OECD, 2021[23]). This requires a long-term vision that integrates all transport modes with a view to building synergy. An annual report on sustainable mobility could help track progress on various elements of Germany’s transport transformation. The country needs to reduce car dependency by better internalising the social costs of road transportation through road pricing and by providing sustainable alternatives (public transport, cycling infrastructure and walking).

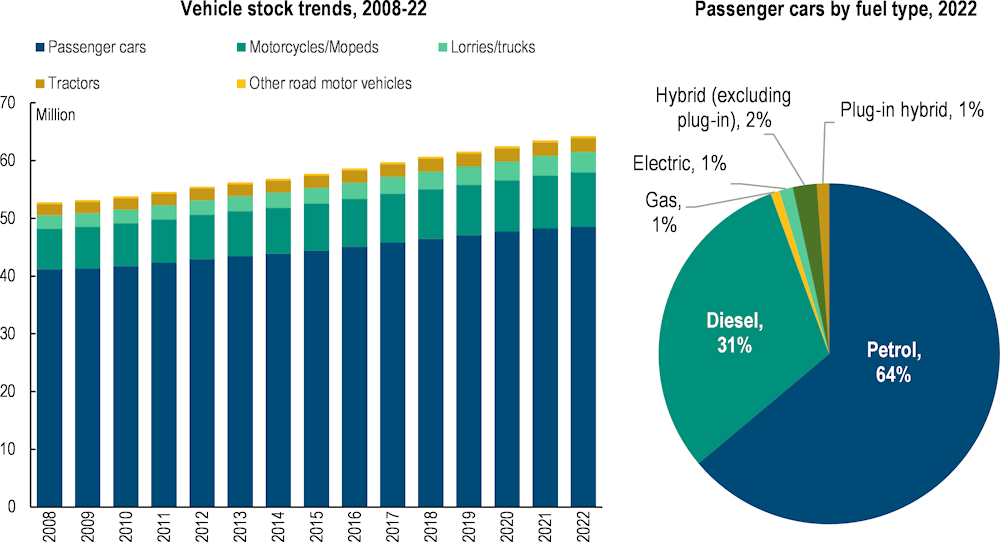

Figure 1.12. The vehicle stock keeps increasing and remains dominated by fossil fuel cars

Source: Destatis (2022), Statistics of motor vehicles and trailers; German Federal Statistical Office.

Germany has one of the densest road infrastructure networks worldwide. Plans to expand federal motorways (e.g. from six to eight lanes) need to give more attention to environmental concerns. A clear priority to investment in public transport and a shift from new roads to the maintenance and improvement of existing infrastructure would help advance the modal shift (Box 1.7).

Box 1.7. Policies in practice: Strict environmental criteria for new road building in Wales

The government of Wales developed a Sustainable Transport Hierarchy of walking and cycling; public transport; ultra-low emission vehicles; and other private motor vehicles. This guides future investment, giving priority to managing and upgrading existing transport infrastructure.

In line with this approach, the Welsh government has set strict environmental criteria for building roads. According to the Wales Transport Strategy 2021, any new road project should focus on “minimising carbon emissions, not increasing road capacity, not increasing emissions through higher vehicle speeds and not adversely affecting ecologically valuable site” (Welsh Government, 2021[24]). Consequently, major road building projects have been scrapped over environmental concerns. The Welsh approach is based on a Roads Review, undertaken by an independent panel.

The Roads Review proposes four tests to justify building roads:

To support modal shift and reduce carbon emissions (prevent increase in demand for private car travel; targeted approaches depending on location).

To improve safety through small-scale changes (to address specific safety rather than wider road improvements and increases in road capacity. Speed limits should be considered as one of the primary tools for improving safety).

To adapt to the impacts of climate change (ensure roads can continue to function and contribute meaningfully to modal shift).

To provide access and connectivity to jobs and centres of economic activity in a way that supports modal shift (new and existing access roads will be necessary to connect new developments, including Freeports, to the existing network).

Source: Welsh Government (2021). National Transport Delivery Plan 2022 to 2027.

Germany is the European country with the longest distances of daily urban travel. On an average day, urban dwellers in Germany travel 19 km, compared to less than 6 km in Greece (Eurostat, 2021[25]). Less than a third of this daily urban travel is related to work. Urban mobility remains heavily car-dominated representing about 70% of daily travel distances. Local public transport, cycling and walking represent 8%, 6% and 4%, respectively. Urban planning needs to better reflect sustainable mobility priorities by creating functional urban areas that shorten distances between home, work and leisure activities. Integrating land-use planning and promoting densification also play an important role.

Electric mobility

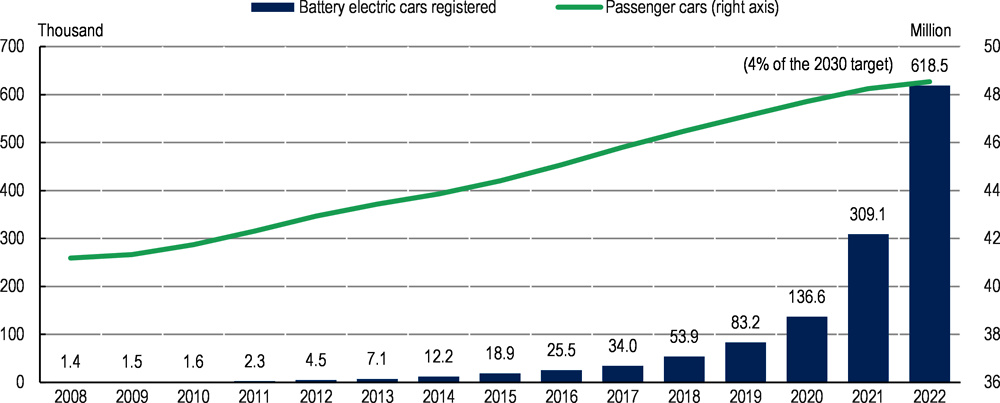

The share of electric vehicles (EVs) is rapidly growing but remains modest in the total vehicle stock. Between 2020 and 2021, EV sales doubled, reaching about 25% of newly purchased vehicles by end 2021. Germany is the largest market in terms of number of EVs sold in Europe. It also offers some of the highest subsidies (IEA, 2022[26]). The purchase premium mostly benefited companies that decided to renew and modernise their vehicle stock while also gaining tax exemptions. The federal government started scaling back support in 2023 (a maximum of EUR 4 500 instead of EUR 6 000 for the purchase premium). As of September 2023, only private consumers can benefit from the scheme. Support for hybrid vehicles has been abolished. As the electric vehicle market is maturing, it makes economic sense to gradually scale back public support.

The country surpassed the 1 million EV mark in 2022 (including hybrid vehicles), two years after its 2020 goal. However, the country has still a way to go to reach the federal government’s goal of 15 million EVs and 1 million charging points by 2030. A new master plan (Ladeinfrastruktur II) aims to boost the expansion of charging infrastructure. In May 2022, Germany had about 60 000 charging points, which means it would need to build about 300 new ones per day to reach its target (PwCNetwork, 2022[27]).

While a more dense and reliable charging infrastructure is a prerequisite for further expansion of electric mobility, the large majority of charging processes take place at home or at work. Policy makers should think more strategically about how to build a coherent, spatially balanced, user-friendly network of fast-charging points across the entire territory. More particularly, low-density areas will require public financial support to establish and maintain public charging stations in areas that lack a commercial market. This requires strong co‑ordination between the federal government and federal states.

Many other bottlenecks impede the uptake of EVs: the purchase price is still perceived as high, although EVs are already cheaper than fossil fuel vehicles from a life cycle perspective given the much lower operational costs. In addition, shorter waiting periods, a broader and more attractive product range, as well as improved battery range and charging speed would help convince a larger number of customers to make the switch. Easy access to local charging points at home, at work or in commercial centres are also important factors.

Figure 1.13. The share of electric vehicles has been growing fast in recent years

Source: Statista (2022), (database), www.statista.com; Destatis (2023), Statistics of motor vehicles and trailers (German Statistical Office).

The transition to electric mobility involves a massive transformation of the German automotive industry with heavy impacts on future employment in the car sector. The number of directly employed people working in the car industry could – in a worst-case scenario – be halved from over 800 000 in 2021 to 400 000 by 2030 (NPM, 2020[28]). Less pessimistic estimates suggest around 90 000 job losses by 2030 (VDA, 2022[29]). Moreover, a large number of small and medium-sized supply companies will no longer be needed. Large-scale job losses are inevitable. However, the impact can be softened through early anticipation and strategic workforce planning (e.g. reduced recruitment, vocational training, upskilling and early retirement schemes). In the context of new challenges related to electromobility, digitalisation and autonomous driving, the car industry needs to take an active part in the transformation of transport and proactively shape its future.

1.1.5. Sustainable farming

The environmental performance of agriculture varies largely across regions. High livestock concentration and intensive land use affect agricultural areas in the north-west and south-east. Diffuse agriculture pollution places pressure on surface water and groundwater bodies (Section 1.1.9). More particularly, nitrogen surpluses remain a major problem in some areas. In 2017 and 2020, the federal government revised the fertiliser legislation comprehensively and expects a significant reduction of nitrogen surpluses, as well as of ammonia and nitrous oxide emissions. Within the new EU Common Agricultural Policy (EU CAP) (Box 1.8), an eco-scheme encourages farmers to renounce the use of plant protection (e.g. chemical-synthetic pesticides at plot level). However, it will take several years before the impact of these measures will become visible. In turn, tighter regulations would require enhanced compliance control, which would also be challenging.

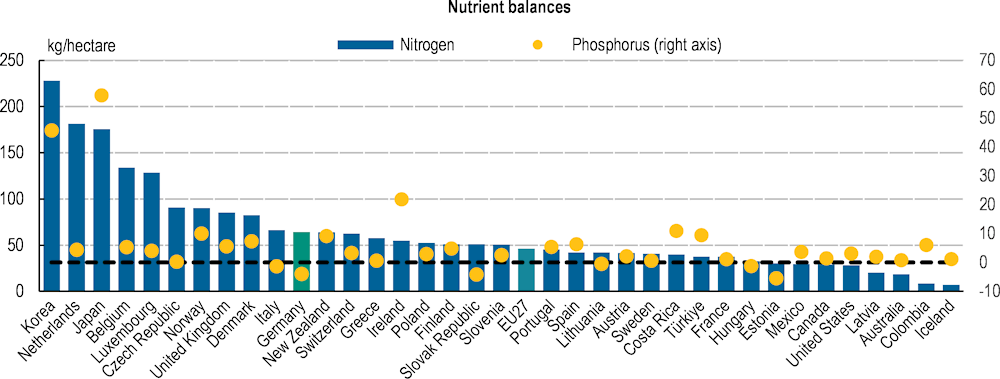

Figure 1.14. Nitrogen surpluses remain a major problem in some areas

Note: The gross nutrient balances (N and P) are calculated as the difference between the total quantity of nutrient inputs entering an agricultural system (mainly fertilisers, livestock manure), and the quantity of nutrient outputs leaving the system (uptake of nutrients by crops and grassland); the dashed line represents the zero value of the right axis (phosphorous).

Source: OECD (2023), Agri-Environmental indicators: Nutrients, Environment Statistics (database).

Agriculture represented about 9% of national GHG emissions in 2020 (Section 1.1.3). Emissions have been relatively stable during the past decade. Methane from animal husbandry and nitrous oxide from agricultural soils are the main sources of emissions. In many countries, the agriculture sector is considered to be a “difficult” sector for advancing decarbonisation, especially as agriculture pollution is diffuse and emissions are not easily attributable to individual farmers. It is therefore tricky to measure emissions. As in other countries, direct monitoring of farm-level emissions is not yet practical, but emissions can be estimated indirectly using farm-level data. Therefore, Germany should pursue efforts to improve measuring of farm-level emissions (e.g. estimates of GHG emissions based on farm practices) and consider exploring the introduction of an agricultural emissions pricing mechanism (e.g. New Zealand) (OECD, 2022[30]). A stronger focus could also be placed on promoting energy-efficient agriculture (Section 1.3.4) and activities for enhanced carbon sequestration in agriculture, including pastures (OECD, 2022[31]). The sector could thereby not only reduce GHG emissions from agriculture but also unlock its green potential as a carbon sink.

The new EU CAP 2023-27 could support Germany in making its agriculture greener and more sustainable. The federal government is also committed to promoting climate-friendly food systems worldwide by supporting COP27 targets for agriculture and policy dialogue within the Global Forum for Food and Agriculture. However, despite progress, ambition in the agricultural sector will need to be further raised to reverse the loss of species and improve the sector’s climate balance (Section 2.3.1).

Box 1.8. Germany’s CAP Strategic Plan

Towards an economically sustainable, greener and fairer CAP

Within the new Common Agricultural Policy (CAP) 2023-27, Germany’s CAP Strategic Plan aims to support the transition to a sustainable, resilient and modern agricultural sector. Overall, the new strategic plan has tightened up environmental and climate-focused requirements and increased opportunities for additional payments for farmers willing to deliver voluntary environmental services (e.g. eco-scheme measure for non-productive land; premiums for the cultivation of protein crops; support for conversion to, and/or maintenance of, organic farming).

The strategy is built around three objectives:

An economically sustainable and fairer CAP: continued income support to keep farms viable and raise the attractiveness of the sector (EUR 2.5 billion of basic income support); stronger focus on small and medium-sized farms; specific support for mountainous regions and other disadvantaged areas (EUR 1 billion); support for modernisation (EUR 933 million) and the uptake of agricultural insurance schemes (EUR 177 million).

A greener CAP: farmers’ support more strongly conditioned to mandatory climate and environmental practices; introduction of new requirements for drainage in peatlands and wetlands; additional support schemes – at federal and Länder levels – for various practices beneficial for the climate and environment moving beyond the mandatory standards.

A socially sustainable CAP: targeted support for over 800 young farmers; support for investment in line with Länder-specific needs (e.g. investment in processing and marketing capacities in rural areas); creation of more than 20 000 new jobs and support for 40 000 rural businesses.

Source: EC (2022), At a glance: Germany's CAP Strategic Plan.

The Federal Ministry of Food and Agriculture (BMEL) focuses on ten key climate action measures to advance the decarbonisation of the agricultural sector. Current programmes notably aim to reduce the use of nitrogen fertilisers, and promote organic farming and carbon sequestration. Within the Investment and Future Programme 2021-24, Germany foresees spending EUR 816 million. This will be allocated to investments in agricultural machinery for precision agriculture, storage capacity of farm manure and small-scale facilities for manure separation, as well as related planning and advisory services.

Germany aims at reducing its livestock over time by supporting farmers to develop alternative income options. This would decrease emissions and free up a considerable amount of agricultural land so far used to produce animal feed. Within the 2022 Climate Action Programme, the federal government also supports the construction of low-emission storage facilities for liquid manure, the retrofitting of storage facility covers and the construction of low-emission livestock stables. Animal welfare has gained increasing public attention (e.g. new mandatory labelling system, discussion on a meat tax and a state-funded long-term animal welfare premium).

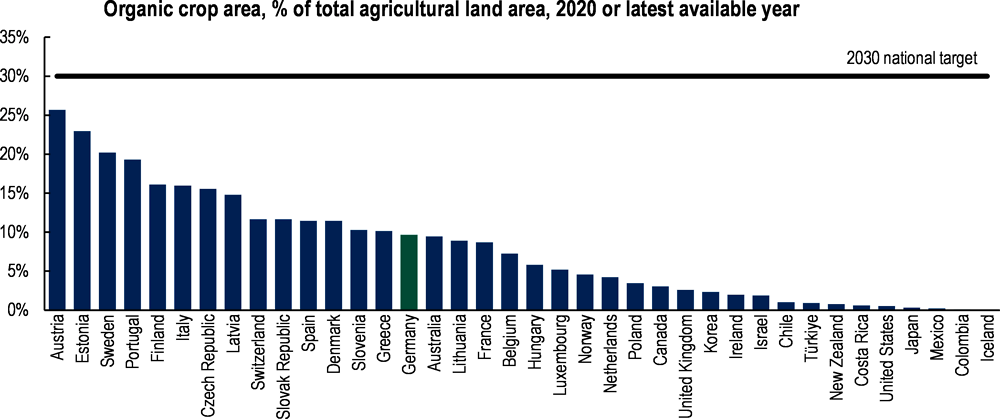

Promoting expansion of organic farming is one of the federal government’s top climate measures for the agriculture sector. It estimates an emission reduction potential between 1.9-7.5 Mt CO2-eq. annually.1 In line with a European-wide trend, organic farming has nearly doubled in the past decade, representing 11% of total agricultural area in 2021 (Figure 1.15). More than 36 000 farms were certified as operating according to organic farming standards. However, Germany would need to significantly accelerate efforts to reach its new target of 30% by 2030 and could also reduce regional disparities. There is scope to increase organic farming and related demand in all agricultural areas.

Figure 1.15. Germany’s share of organic farming is increasing but needs to triple to reach the 2030 target

Source: OECD (2023), Agri-Environmental indicators (database).

1.1.6. Atmospheric emissions and air quality

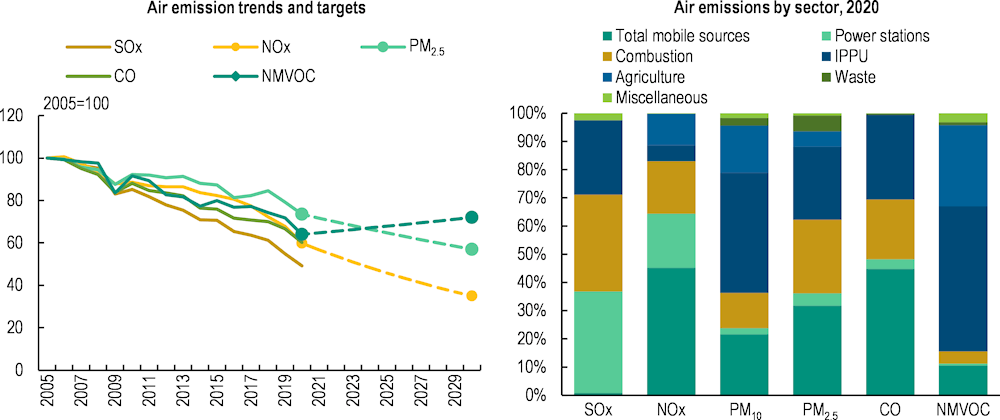

Emissions of air pollutants are trending down and are decoupled from growth of GDP (Figure 1.16). Germany complied with EU emission reduction commitments for all pollutants in 2020 (EC, 2022[32]). Germany also reached its 2020 Gothenburg Protocol objectives for sulphur dioxide and nitrogen oxides, non-methane volatile organic compounds and ammonia emissions. Emission intensities per unit of GDP and per capita are all lower than the OECD average. The country projects to meet the EU emission reduction commitments for major air pollutants without additional measures, except for ammonia between 2020 and 2029.

Figure 1.16. Air emission reductions are on track overall

Note: In the left panel, the markers in 2020 represent the 2020-29 targets and the markers in 2030 the 2030 targets, as defined in the European Union Directive 2016/2284. SOx = sulphur oxides. NOx = nitrogen oxides. PM = particulate matter. CO = carbon monoxide. NMVOC = non-methane volatile organic compounds. IPPU: Industrial processes and product use.

Source: OECD (2022), Air Emissions by Source (database).

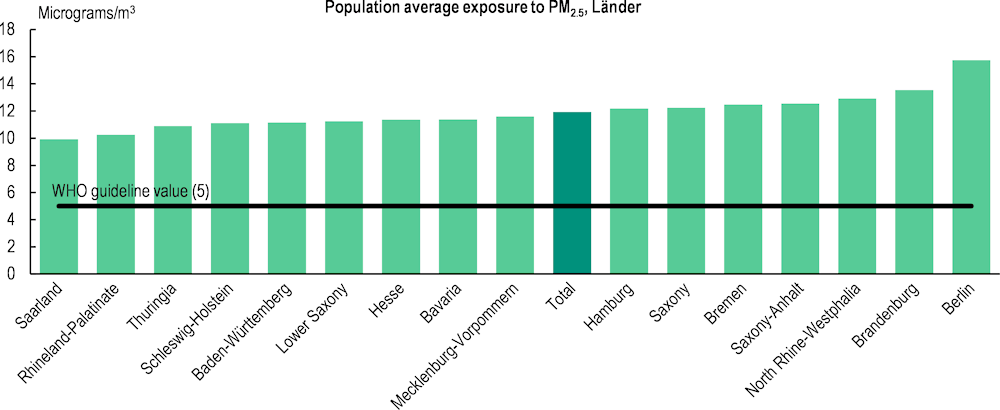

Air pollution is still a major health concern for citizens. In 2020, nearly 29 000 premature deaths were attributable to concentrations of small particulate matter (PM2.5), 10 000 to nitrogen dioxide (NO2) concentrations and 4 600 to ozone concentrations (EEA, 2022[33]). Five air quality zones still exceeded the EU limit value for NO2 in 2020 (EC, 2022[32]). People in bigger cities are much more exposed to PM2.5 than the national average. The tightening of emission values of low emission zones could help reduce air pollution. Ultra-low and zero emission zones have proven to be effective in other countries (Box 1.9). Cities and municipalities need to be empowered to play a leading role in improving air quality. Germany is still far from achieving the global air quality guideline of the World Health Organization for PM2.5.

Figure 1.17. German citizens are unevenly exposed to air pollution

Source: OECD (2022), Air quality and health: Exposure to PM2.5 fine particles – countries and regions, OECD Environment Statistics (database).

Box 1.9. Policies in practice: London’s congestion charges and low emission zones

London’s Congestion Charge zone is one of the largest in the world. It was set up nearly two decades ago to discourage road traffic in central London, improve air quality and raise additional resources for public transport. A low emission zone for heavy goods vehicles was created in 2008. In addition, the city of London introduced the world’s first 24-hour ultra-low emission zone (ULEZ) in 2019, covering 4 million people or about a third of the city’s population. While traffic congestion in central London remains a challenge, carbon emissions and other air pollutants from transport have been reduced. According to the 2022 six-month assessment report of the expanded ULEZ, a larger share of vehicles in London is cleaner, contributing to London’s commitment to becoming a zero-carbon city by 2030. Nearly 94% of vehicles driving in the ULEZ meet the emission standards on an average day. The city of London also recorded a sharp decline in the use of diesel cars driving in the ULEZ, resulting in cleaner air and important health benefits for Londoners. On average, there were 44 000 fewer diesel cars each day, representing a 20% reduction.

Source: OECD (2022), London’s congestion charge and its low emission zones, IPAC Policies in practice.

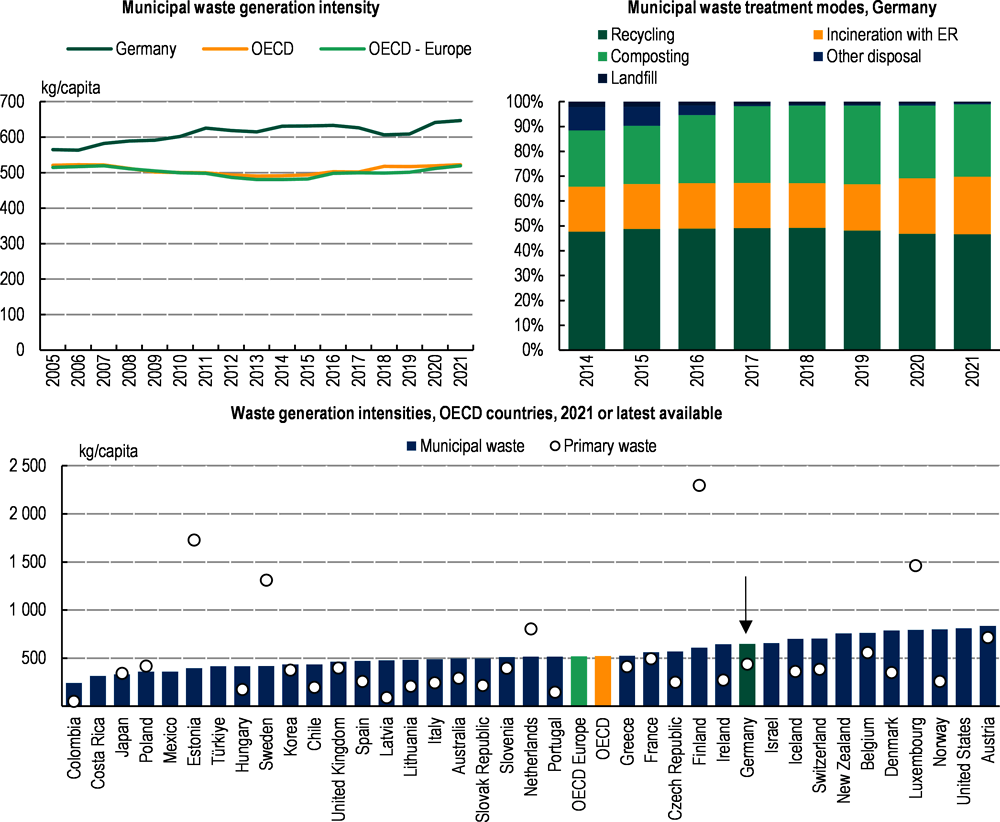

1.1.7. Waste management

Germany is one of the best performing OECD countries in terms of environmentally sound waste management. The country has one of the highest recovery rates and the second highest recycling rate in the OECD area. About two-thirds of municipal waste are recycled or composted. A ban of municipal waste landfilling has been in place since 2005.

Waste is managed at the subnational level. Regional waste management plans are conceived at Länder level and implemented by local authorities. Some Länder and municipalities have set up weight-based pay-as-you-throw pricing models. Waste separation is mandatory, using four different bins in nearly every house (light-weight packaging, paper waste, household waste and biowaste). Germany also has a nationwide deposit system for certain beverage bottles (Pfandpflicht).

As in other countries, packaging waste increased in relation to the COVID-19 pandemic. As of 2023, takeaway food and drinks suppliers such as restaurants, canteens, supermarkets or fuel stations must offer their products in reusable packaging, without any extra cost. This measure will greatly contribute to reducing the use of disposable plastic packaging. While being the largest exporter of plastic waste in the European Union, Germany has had a five-point plan since 2018 to reduce plastic waste and support international efforts to reduce marine litter. A broader waste prevention programme is under development.

Figure 1.18. Municipal waste management has greatly improved, but waste levels remain high

Note: values for OECD aggregates are estimates based on linear interpolations. The OECD aggregate excludes Canada.

Top right panel: ER = energy recovery.

Source: OECD (2023), Municipal waste - generation and treatment and Generation of waste by sector, OECD Environment Statistics (database).

Germany made little progress to reduce municipal waste and needs to strengthen waste prevention. On average, a German citizen produced 632 kg of waste in 2020, compared to 505 kg within the OECD Europe area (OECD, 2022[34]). In total, about 11 million tonnes of food along the food chain, is thrown away every year. Efforts should focus on the whole food supply chain from farm to fork, and notably target retail and household behaviour. Cutting household food waste in half, for example, could save 6 Mt CO2-eq (BMEL, 2022[35]).

Germany has had a national strategy for food waste reduction since 2019. It aims to halve per capita food waste at retail and consumer levels and reduce food losses along the supply chains by 2030. The federal government has established several dialogue platforms. Discussions on voluntary agreements with business organisations are underway. The public awareness raising campaign “Too Good for the Bin!” has been in place for a decade. Beyond dialogue platforms, binding measures with intermediate targets may be needed.

There are multiple ways of making progress towards behavioural changes. Food and nutritional education are of paramount importance (e.g. the indicative value of best-before dates) and could also help prevent the progression of obesity. More than one in ten children in Germany is obese or overweight, generating considerable health risks. Germany has introduced the Nutri-Score, which indicates the nutritional value of food products through a five-colour nutrition rating system (from A to E). However, the scheme is not yet mandatory.

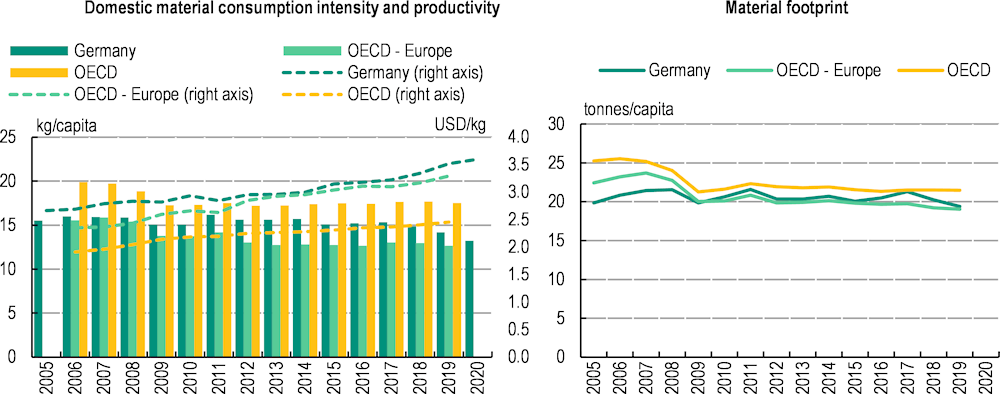

1.1.8. Towards a more circular economy and sustainable supply chains

The federal government is working on its first comprehensive circular economy strategy, drawing on many existing strategies and programmes that already deal with these issues. Circular use of materials in Germany increased from 11.4% in 2017 to 13.4% in 2020. This is below the EU average of 12.8%; and far behind the Netherlands (30.9%) (EC, 2022[32]). However, Germany has reduced the resource intensity of its economy and has decoupled domestic material consumption from economic growth. Its material consumption per capita is below the OECD average.

Figure 1.19. Material consumption productivity is growing, but material footprint remains high

Note: In the left panel, domestic material consumption (DMC) refers to the amount of materials directly used in an economy, which refers to the apparent consumption of materials. DMC is computed as domestic extraction used minus exports plus imports; gross domestic product is expressed in 2015 PPP prices; productivity (the lines) are on the secondary axis. In the right panel, material footprint refers to the global allocation of used raw material extracted to meet the final demand of an economy.

Source: OECD (2022), Material Resources, OECD Environment Statistics (database).

Box 1.10. Policies in practice: A handbook for businesses operating in mineral supply chains

Business activities amplify global threats related to environmental degradation, which occurs often in the upstream segment of the supply chain. In mineral and metal supply chains, for example, sediments and process chemicals such as mercury may leak from mine workings into surface water or groundwater. Risk-based supply chain due diligence can help enterprises identify, anticipate and react to environmental threats and thus address harms to air, land, water and biodiversity. This is particularly relevant in the context of rising demand for structural minerals and metals in a physically growing world economy as well as for functional materials critical to the energy and digital transition, such as cobalt, copper and lithium. Therefore, companies need to meet relevant requirements in relation to environmental, local labour, corporate governance, criminal or anti-bribery laws, in line with OECD recommendations.

Many stakeholders highlighted the need for hands-on support on how the environment-related recommendations can be implemented in practice. Within the context of 2020 Raw Materials Strategy, BMUV initiated a process to develop a “Handbook on Environmental Due Diligence in Mineral Supply Chains” by the OECD’s Centre for Responsible Business Conduct, in collaboration with the German Environment Agency and the Federal Institute for Geosciences and Natural Resources.1 It offers a six-step approach for suppliers:

1. Embed responsible business conduct into policies and management systems.

2. Identify and assess actual and potential adverse impacts associated with the enterprise’s operations, products or services.

3. Cease, prevent and mitigate adverse impacts.

4. Track implementation and results.

5. Communicate how impacts are addressed.

6. Provide for or co-operate in remediation when appropriate.

The handbook also explores opportunities to strengthen circular economy principles in the design, production, distribution, consumption and collection of products. It can be used by all types of businesses along the value chain, from mining to retail, to conduct due diligence on upstream impacts. The handbook will be launched at the 2023 OECD Forum on Responsible Mineral Supply Chains.

1. The handbook builds on the leading international, government-backed standards on supply chain due diligence and responsible business conduct: the OECD Guidelines for Multinational Enterprises and the associated due diligence framework set out in the OECD Due Diligence Guidance for Responsible Supply Chains of Minerals from Conflict-Affected and High-Risk Areas and the OECD Due Diligence Guidance for Responsible Business Conduct.

Source: (OECD, forthcoming[36])

As typical for many other developed economies, material footprint originates in part from outside of Germany. Germany depends heavily on imports of raw materials. Therefore, the new Supply Chain Act is a welcome development away from purely voluntary corporate social responsibility towards binding human rights and environmental obligations for companies (Initiative Lieferkettengesetz, 2021[37]). As of 2023, companies registered in Germany with more than 3 000 employees must comply with certain obligations for their entire supply chain, including human rights. Child labour, slavery and forced labour are explicitly banned. The law will be expanded to companies with more than 1 000 employees as of 2024. However, it applies only to the company's own business operations and not to indirect suppliers, which remains a loophole. The law also regulates a few environmental obligations in relation to three international conventions (Persistent Organic Pollutants, Minamata and Basel Conventions), mainly aimed at protecting human health. It could have placed a stronger focus on environmental degradation that impact other countries abroad.

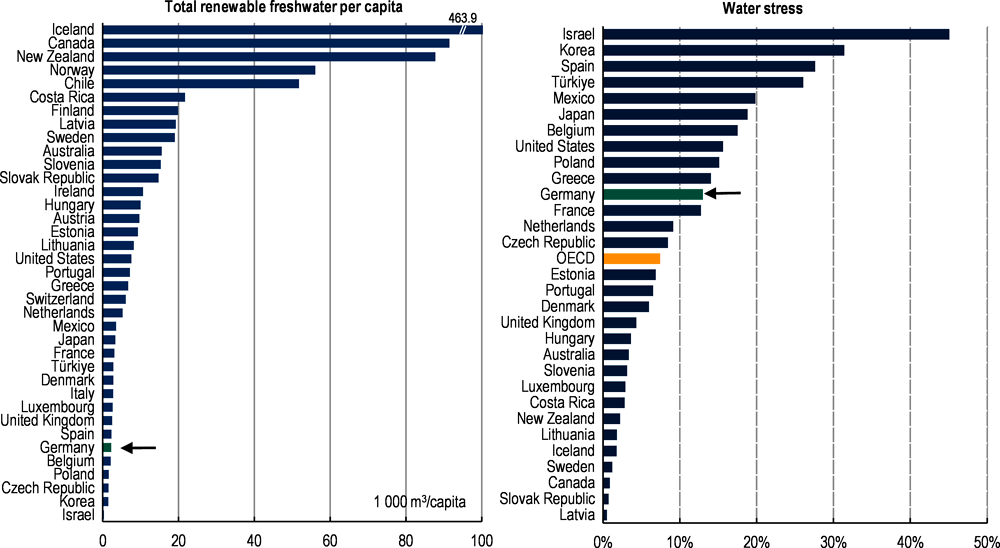

1.1.9. Management of water resources

Water resources

Germany is rich in water resources, counting over 11 000 water bodies (about 8 900 rivers, 700 lakes, 80 coastal waters, 1 300 groundwater basins) (UBA, 2021[38]). About 2.2% of Germany’s surface area is covered by water. Total annual water abstractions as a share of total available renewable water resources decreased from 20.1% in 2001 to 13% in 2016. Water abstraction per capita is well below the OECD Europe average. Nevertheless, Germany is still above the 10% threshold, making it a moderate water-stressed country (Figure 1.20). With the ongoing energy transition, Germany should be able to make additional water savings. Cooling related to electricity generation represented about half of total water abstractions. Public water supply accounted for nearly 20% in 2021. Irrigated agriculture is negligible, representing less than 1% (EC, 2022[39]).

Figure 1.20. Despite water savings, Germany still faces moderate water stress

Note: Water stress is defined as gross freshwater abstraction as percentage of total renewable freshwater resources; 2020 or latest available year (no earlier than 2014). In the right panel data refer to 2020 or to the latest available year. They include provisional figures and estimates. Freshwater abstraction: for some countries, data refer to water permits and not to actual abstractions.

Source: OECD (2022), Freshwater resources and Freshwater abstractions, OECD Environment Statistics (database).

Similarly, drinking water use declined over the past decades. A German citizen uses an average of 128 litres (L) of drinking water per day in 2022, compared to 147 L in 1990 (Statistisches Bundesamt, 2022[40]). This is well below the European average of 150 litres (EurEau, 2021[41]). Germany has generally good water infrastructure with a reliable water supply; water leakage levels are traditionally among the lowest in Europe (DVGW et al., 2020[42]).

Over two-thirds of drinking water demand is covered by groundwater. However, groundwater abstractions vary considerably between federal states. While public water supply in Bremen, Hamburg, Saarland and Schleswig-Holstein relies exclusively on groundwater and spring water, the states of Saxony and Thuringia benefit from larger surface water sources (BGR, 2023[43]). Germany uses water registers to control water abstractions with a view to ensuring sufficient groundwater recharge. Water abstractions are also controlled through a permitting system, which is regularly reviewed, except for small abstractions that are not systematically registered. To date, the impacts of climate change on groundwater levels are small but they are projected to increase by the end of the century, notably in the North and the East (ClimateChangePost, 2023[44]) (Section 2.1.1).

However, Germany’s water sector will be increasingly impacted by climate change. Prolonged dry periods and heatwaves may amplify and trigger seasonal, localised water shortages. They will also lead to dried-up rivers impeding inland waterway transport, receding groundwater levels and soil moisture loss, with major economic impacts. For example, due to the record dry summer in 2019, water levels in the Rhine River sank to their lowest since 1881 (Gustafsson, 2019[45]). Disruptions in inland waterways heavily impacted the industry and contributed to increased energy prices. Many companies such as BASF, a chemical giant, invest heavily in low-water vessels to ensure adequate supply of raw materials during times of drought.

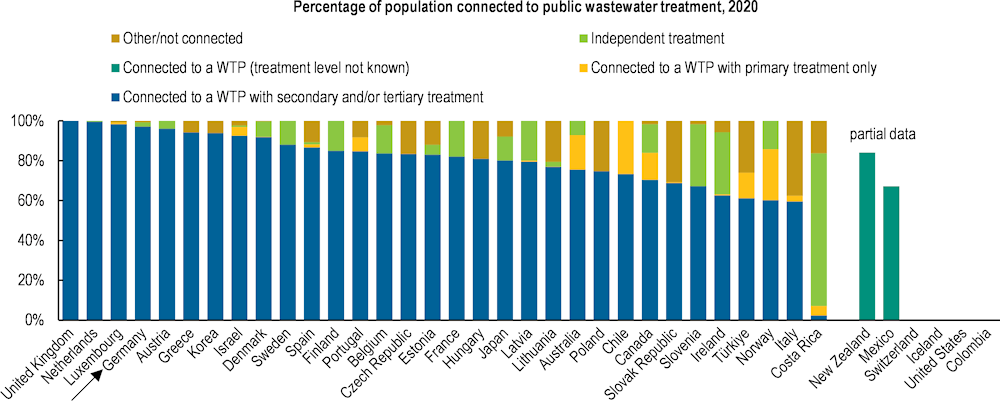

Box 1.11. Germany’s National Water Strategy

Germany’s National Water Strategy provides a comprehensive long-term vision for 2050. It aims to raise awareness of the value and sustainable use of water as a resource. The strategy emphasises the need to develop the country’s forecast capacity to better understand water needs and water availability to prevent localised water shortages and overuse in the future. As water is mostly managed at the Länder level, the strategy provides guidance and good practice examples with a view to developing uniform decision-making criteria and standards. Within the broader European context, the strategy sets goals for action and measures around four priorities:

Prevent water scarcity and conflicts of use

Adapt water infrastructure to climate change

Make water cleaner and healthier

Create a broader base to finance restructuring of the water sector.