Cash transfers and other measures to provide financial assistance to families represent a major pillar of the national family policy packages in most OECD countries. All OECD countries provide financial support to families in one form or another, though the design and means of delivery are diverse. Depending on the country, these supports are used to pursue a variety of different objectives, ranging from boosting birth rates to reducing child poverty and promoting child well-being. However, in all cases, the broad aim is to increase families’ standards of living and support families with the costs of raising children.

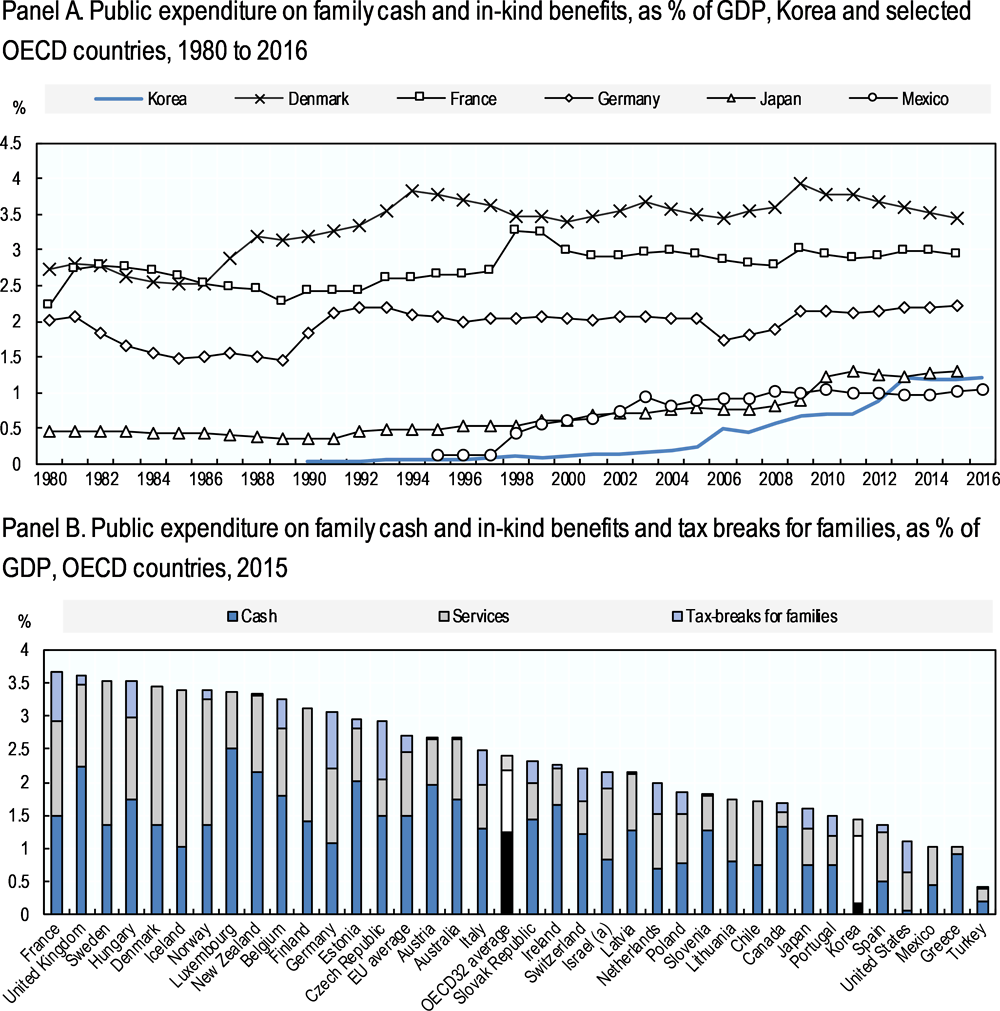

Financial supports for families can be separated into two main types. First, are family-related cash benefits, most often taking the form of child allowances (also known as child benefits or family allowances). Almost all OECD countries provide at least some kind of family or child allowance through a cash transfer targeted at children or families with children (OECD Family Database). These allowances often sit at the centre of the national family support package, and in many cases represent a major expenditure item – indeed, on average, in 2015, OECD countries spent roughly 0.7% of GDP on family or child allowances (OECD Social Expenditure Database), equivalent to more than one-third of all public expenditure on families (not including expenditure on tax breaks). Rules regarding the exact amounts provided vary widely, with payments frequently increasing or decreasing with both the age of the eligible child and the size of the family in which the child lives. In roughly half of OECD countries, child allowances are means-tested with eligibility restricted to children living in families with incomes under a certain threshold, and several benefits are reduced as household income increases (OECD Family Database).

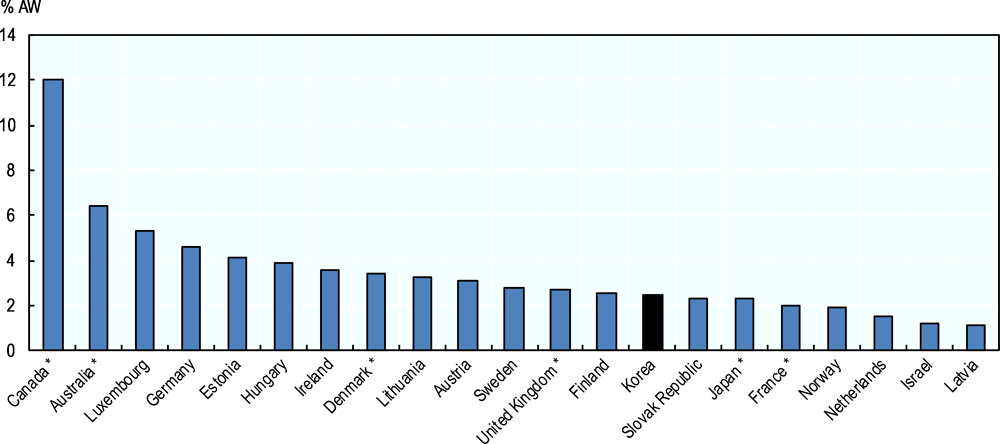

The second main type is tax-based financial support for families. Over three-quarters of OECD countries provide some kind of family-related financial support through the tax system. Most often this concerns a child tax allowance (e.g. Austria, Belgium, Hungary, Slovenia, Switzerland) that is deducted from gross taxable income, or child tax credits (e.g. Finland, Germany, Italy, Poland, Portugal, the Slovak Republic, the United Kingdom, the United States) that reduce the final income tax liability (OECD Family Database). In many countries, the amounts directed through tax breaks for families are relatively small in comparison to the amount spent on family cash benefits (Figure 2.14). However, in France, Hungary, and Italy more than 0.5% of GDP is provided to working families through tax breaks and tax credits. In Germany and the Czech Republic, public spending on tax breaks for families reaches not far off 1% of GDP (Figure 2.14).

Historically, in comparison to other OECD countries, Korea has provided relatively little in the way of cash supports for families. As recently as 2015, excluding maternity, paternity and parental leave, Korea spent only 0.36% of GDP on family financial supports through cash benefits and tax breaks. This was the smallest share of GDP spent by any OECD country other than Turkey. To a greater extent than in most OECD countries, Korean families have historically relied on market earnings for their income, supported at times by a patchwork of relatively small financial supports delivered through the tax system (see below) or by local governments (see Box 2.2).

However, Korea is taking steps to expand and improve its package of family cash supports. Over the last decade or so, Korea has introduced several new child- or family-related tax breaks and supports with the aim of providing financial assistance to families with children. These range from a standard child tax allowance providing a deduction on gross taxable income, to a per-child non-refundable tax credit for all taxpayers and a per-child refundable tax credit for low-income families. More recently, in September 2018, the Korean government introduced a nationwide cash child allowance for the first time. In comparative terms, these measures are fairly modest and small in scale, with the amounts provided relatively low compared to some equivalent measures in other OECD countries (see below). Nonetheless, these are movements in the right direction.