Yasmin Ahmad

OECD Development Co-operation Directorate

Eleanor Carey

OECD Development Co-operation Directorate

Yasmin Ahmad

OECD Development Co-operation Directorate

Eleanor Carey

OECD Development Co-operation Directorate

Official development assistance (ODA) in 2022 is operating in a rapidly evolving environment. During 2020-21, development co-operation providers saw increased demand for support driven by the COVID-19 pandemic, in order to deal with increasing poverty, hunger, conflict and economic impacts. Now, Russia’s war of aggression against Ukraine is dampening the global recovery, driving inflation and creating cascading crises around the world, including in developing countries. This paper takes stock of how COVID-19 shaped ODA spending in 2020-21, using detailed ODA data available for the first time. It also analyses how the multifaceted crisis triggered by the war in Ukraine might impact ODA in 2022 and beyond.

This paper was prepared under the direction of Mayumi Endoh, Deputy Director, Development Co-operation Directorate, Rahul Malhotra, Head of Division, Development Co-operation Directorate, and Ida Mc Donnell, Team Lead for the Development Co-operation Report. Editing and proofreading was by Misha Pinkhasov.

Special thanks for inputs and research assistance go to Jonas Wilcks.

The authors are also grateful for contributions and feedback from: Joelle Bassoul, Elena Bernaldo de Quiros, Emily Bosch, Stephanie Coic, Ana Fernandes, Anthony Kiernan, Anita King, Frederik Matthys, Nestor Pelecha Aigues, Santhosh Persaud, Katharina Satzinger, Haje Schütte, Rolf Schwarz, Rachel Scott, Jenna Smith Kouassi, Henri-Bernard Solignac Lecomte, and Jessica Voorhees.

Note: This infographic details ways in which Russia’s war of aggression against Ukraine could put pressure on official development assistance (ODA) budgets in 2022 and beyond. There are many unknowns, including the duration of the war, the eventual scale of need of Ukraine and its people, and the magnitude of crises exacerbated in other developing countries. Not all responses to the war in Ukraine will be ODA-eligible. The image also depicts the additional budgets that were mobilised for COVID-19 spending in 2020-21. Not pictured are crises (including those that are climate-related) funding gaps and demands on ODA that pre-date, and are exacerbated by, COVID-19 and war in the Ukraine.

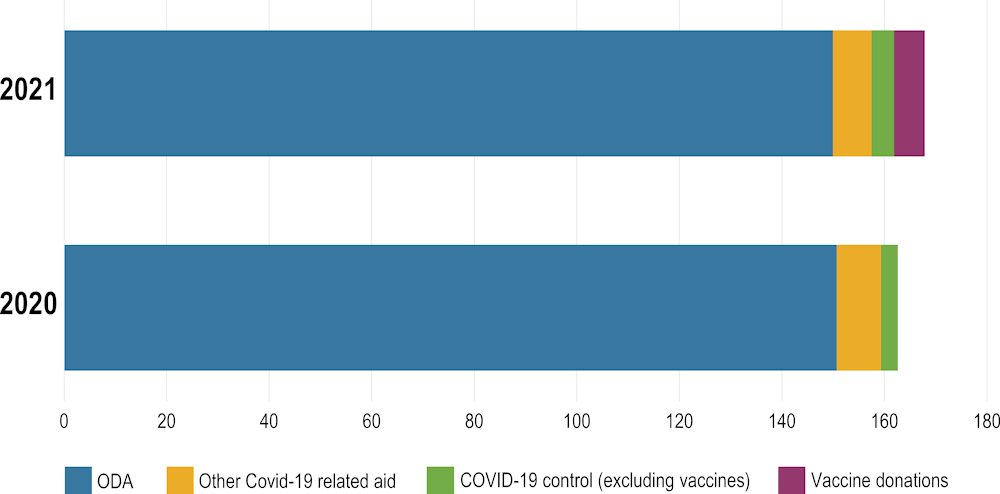

The COVID-19 crisis saw ODA levels rise by USD 35 billion in 2020 and 2021, while the ODA/GNI share remained flat. Despite official development assistance (ODA) volumes reaching record highs, the magnitude of additional need created by the COVID-19 crisis is far greater than ODA increases can meet. Moreover, behind the aggregate increase, significant differences in spending patterns emerged. Increased ODA by some providers offset decreases by others. Excluding the costs of vaccines for COVID-19 in 2021, ODA grew slightly, by 0.6% in real terms compared to 2020, although when additional COVID-19 budgets are excluded, total gross ODA fell in 2020 for all income groups except upper-middle income countries. ODA as a percentage of gross national income (GNI) has been stable in the past two years, at 0.33% for all DAC countries – far from the UN target of 0.7% to which most DAC countries committed.

As the acute phase of the pandemic subsided towards the end of 2021, global recovery advanced but became uneven, with inflationary pressures and supply constraints (OECD, 2021[1]). Developing countries faced these issues in addition to low COVID-19 vaccination rates, rising poverty and hunger, and little fiscal capacity to support populations. Many low-and-middle income countries also had to re-commence debt repayments when suspension initiatives (agreed as emergency measures during the COVID-19 crisis) came to an end. These combined pressures meant that, while the year 2021 closed with strong ODA volume in aggregate terms, it came under increasing pressure to meet rising needs.

By mid-2022, the ramifications of Russia’s war of aggression against Ukraine were felt worldwide (OECD, 2022[2]), changing also the decision-making context for ODA budgets and spending. OECD data show that GDP in most ODA-provider countries continues to grow in 2022, but at lower rates than projected before the war. While ongoing pandemic recovery stimulus packages in some ODA-provider countries and windfall profits from record energy prices in others could help these countries to meet higher domestic spending needs, national budgets, including for ODA, are under pressure in these economically uncertain times. Meanwhile, high inflation degrades the purchasing power of ODA, and governments are under pressure domestically to manage and curb the impacts of inflation and other macroeconomic trends on their own populations.

Still, demand for ODA is increasing. In addition to responding to the urgent needs of Ukraine and its citizens (both inside Ukraine and as refugees), related food and energy crises in other developing countries are driving increased poverty and needs. High debt levels in many developing countries could possibly exacerbate further demand for ODA. Indirect consequences of persistent unsustainable debt include increased humanitarian or development needs, which ODA could be called on to meet. Longer-term development goals, the 2030 Agenda for Sustainable Development – now further from reach than at any point in the last twenty years – must also not be forgotten.

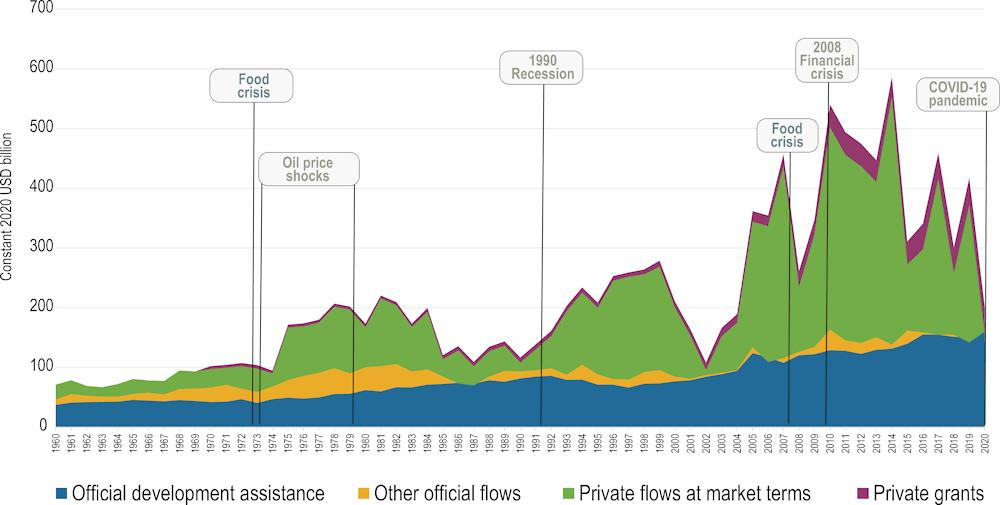

This chapter explores how ODA budgets will be shaped by these concurrent crises. In the past, ODA proved to be a reliable source of external financing during crises, usually rising to meet increased needs before experiencing a fall, often 2-3 years after the beginning of a crisis (ODA response to previous crises). The 1970’s food and oil shock first precipitated a 13% dip in ODA from 1972 to 1973, then a 16% rise in 1974 and a further 5% in 1975. ODA rose 1% during the 1979 oil shock, and again by 11% in 1980, before dropping off in 1981. During the 2007-08 food crisis, ODA dropped 8% in 2007, but rose 12% in 2008. It continued to climb in 2009 (1.5%) and 2010 (5.6%), despite the financial crisis, then fell 0.9% in 2011.

Constant 2020 USD (billions)

Source: OECD DAC Statistics (OECD, 2022[3])

Several providers are stepping up with new and additional assistance for Ukraine, the Ukrainian refugee crisis and to mitigate deepening food insecurity, hunger and extreme poverty across the globe. While the absence of a real-time system for sharing information about ODA-related funding decisions, along with the evolving nature of responses to multiple and interlinked global crises, make it impossible to predict the level of total ODA for 2022, additional budgets mobilised so far will likely drive up ODA volumes in 2022. At aggregate level, public commitments by DAC members to financial and humanitarian support in response to the war in Ukraine seem to be surpassing ODA mobilised for the COVID-19 response, at an estimated USD 46 billion (DAC members’ spending on in-donor refugee costs, number of Ukrainian refugees, anticipated costs, % 2021 ODA). At the same time, how and where current ODA budgets are spent is also likely to shift, with humanitarian spending accounting for a greater proportion. Re-allocations of funds to commitments for Ukraine could also squeeze resources for country-programmable aid in other regions.

Several providers are stepping up with new and additional assistance for Ukraine, the Ukrainian refugee crisis and to mitigate deepening food insecurity, hunger and extreme poverty across the globe.

The climate crisis also continues to demand attention, and commitments to spending in this area could affect the availability of concessional finance to meet other development goals, especially if budgets do not increase.

Data and calculations in this paper are based on the available data as of 16 June 2022.

Net ODA increased 118% in real terms since 2000 due to political commitments (Ahmad et al., 2020[4]) and rose 20% since the Sustainable Development Goals (SDGs) were adopted in 2015 (DAC member countries' net official development assistance, 2000-21). ODA has long been a stable source of development financing and cushioned the impact of previous financial crises (e.g., the 1980s Mexican debt crisis, the 1990s recession and the 2008 financial crisis). Despite DAC members’ economic losses in 2020, their ODA grew to USD 162.2 billion, up 4% in real terms from 2019. All other major external resource flows for developing countries fell that year: total external private finance to developing countries declined by 13%; trade by 8.5%; foreign direct investment by 19%; and remittances by 1% (OECD, 2020[5]). The rise of ODA again in 2021 demonstrates that it remains a stable source of finance.

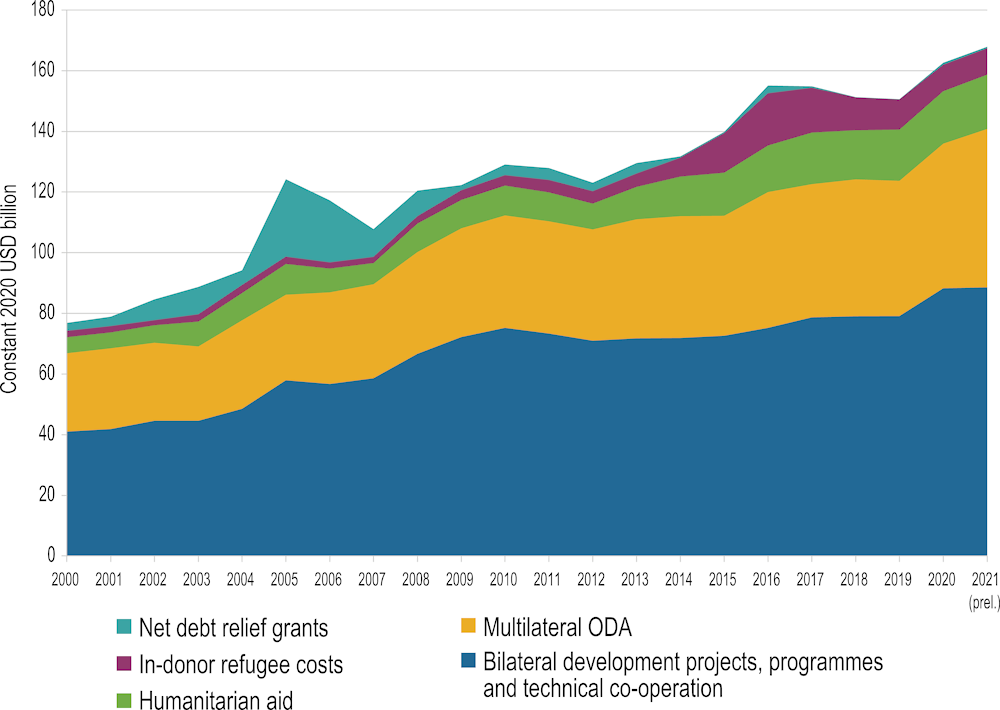

Total ODA in 2021 rose 4.4% in real terms compared to 2020, reaching its highest level ever. In 2021, ODA by DAC members amounted to USD 178.9 billion, or 0.33% of DAC members’ combined GNI (unchanged from 2020), with just five DAC members meeting the 0.7% ODA/GNI target. When the pandemic hit in 2020, most donors had already adopted their ODA budgets and maintained their commitments, with some mobilising additional funding to support developing countries facing exceptional circumstances. In 2021, the increase was mostly due to DAC members’ support for COVID-19 response, particularly donations to address global vaccine inequities.1 Excluding costs for vaccines, ODA in 2021 grew 0.6% compared to 2020, mostly due to increases in multilateral funding.

Constant 2020 USD (billions)

Source: OECD DAC Statistics (OECD, 2022[3])

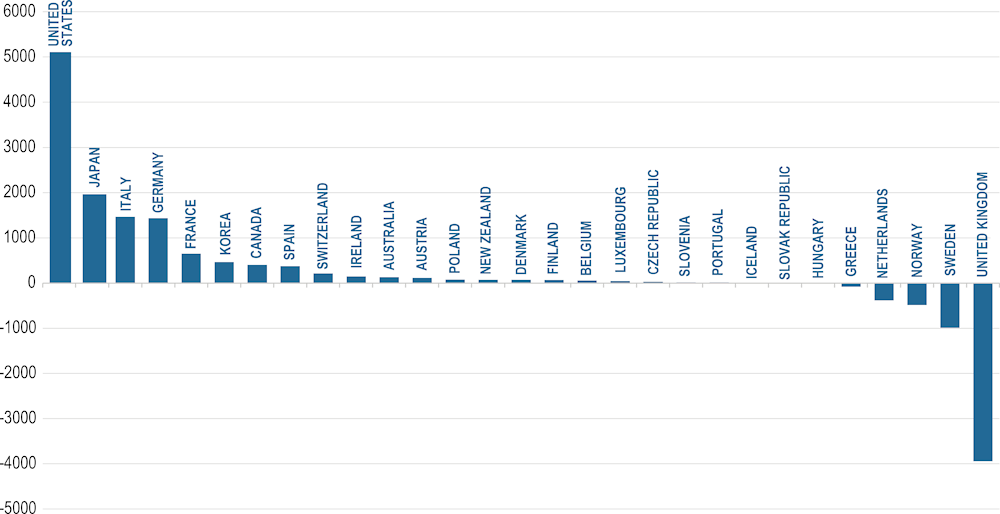

ODA volumes rose in 23 DAC members in 2021, often due to support for COVID-19 responses, and fell in six countries (Year-on-year ODA volume change, 2020-21). Had ODA remained stable in countries where it fell, it would have risen 8% in real terms, to USD 185 billion, an additional USD 6.1 billion over the actual 2021 ODA figure.

Constant 2020 USD (millions)

Source: OECD DAC Statistics (OECD, 2022[3])

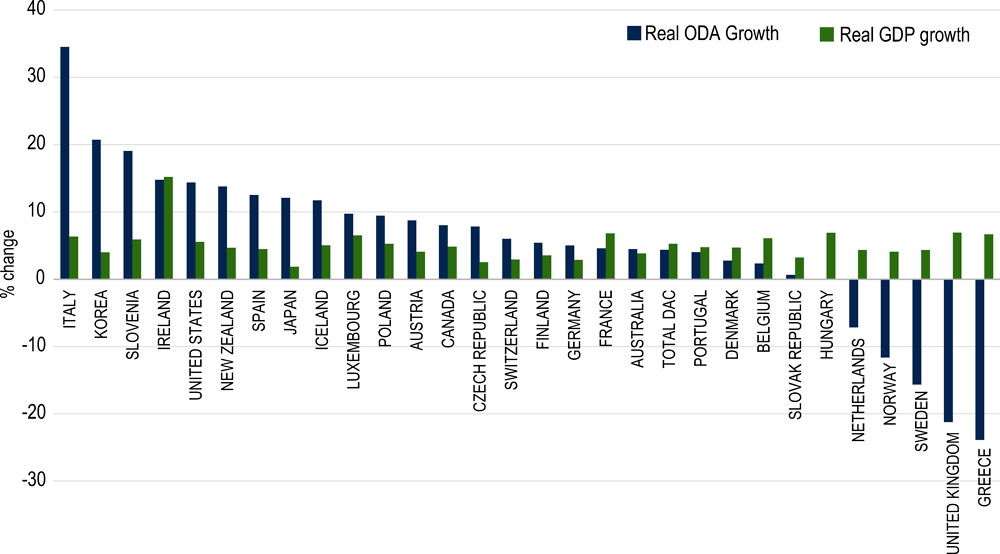

While 2021 saw uneven global economic recovery from COVID-19, GDP in all DAC members grew, albeit not to pre-COVID levels (Year-on-year ODA and GDP change, 2020-21). Greece, the Netherlands and the UK were the only countries to see ODA declines in both 2020 and 2021. In 2021 the UK allocated 0.5% of GNI to ODA instead of 0.7% for the first time since 2013 (House of Commons Library, 2021[6]). If the UK had allocated 0.7% of GNI to ODA in 2021, its ODA would have been USD 6 billion higher.

% change

Source: OECD DAC Statistics (OECD, 2022[3])

Contributions to ODA-eligible international organisations rose by 9.4% in real terms from 2020 to 2021, due to a substantial increase in contributions to vertical funds. Bilateral ODA for programmes, projects and technical assistance (excluding in-donor refugees and vaccine donations) fell by 3.3%, due in part to a drop in bilateral sovereign ODA lending. DAC countries’ lending to other countries (bilateral sovereign loans on a grant-equivalent basis) had increased by 35% in real terms between 2018 and 2020, but fell by 4.6% in 2021 and represented 10% of bilateral ODA. In contrast, EU Institutions’ sovereign lending increased by 2% and represented 15% of its bilateral ODA. Net ODA contributions for private sector instruments (recorded on a flow basis) fell by 4%.

As in previous years, net debt relief remained low, at USD 545 million.

Over 2020 and 2021, DAC countries mobilised approximately USD 35 billion in financing to respond to the COVID-19 crisis, most of which was additional to their pre-crisis ODA budgets.

In 2021, DAC countries spent USD 18.7 billion of total ODA on COVID-19 responses (preliminary data),2 representing 10.5% of their combined net ODA (DAC members’ bilateral ODA allocations for COVID-19 response, 2020-21). COVID-19 vaccine donations accounted for USD 6.3 billion of ODA (3.5% of total ODA) and amounted to 857 million doses for developing counties. Of this, USD 2.3 billion (1.3% of total ODA) were for donations of excess supply3 (amounting to nearly 357 million doses), USD 3.5 billion for donations of doses purchased for developing countries, and USD 0.5 billion for ancillary costs.

In 2020, DAC member countries provided USD 16.2 billion in bilateral aid for COVID-19 response (DAC members’ bilateral ODA allocations for COVID-19 response, 2020-21), while multilateral organisations provided USD 8.9 billion and other providers USD 0.5 billion. On average, two-thirds of COVID-19-related aid by all donors was provided in the form of grants, and one-third in the form of loans or other types of non-grant finance, with France (USD 1.4 billion), Germany (USD 1.7 billion), Japan (USD 1.9 billion) the largest providers of ODA loans. Among other providers, Saudi Arabia (USD 0.3 billion) was the largest donor.

Constant 2020 USD (billions)

Source: OECD DAC Statistics (OECD, 2022[3])

Foundations and philanthropic organisations provided USD 2 billion of COVID-19-related aid in 2020. The largest providers were BBVA Microfinance Foundation (USD 0.9 billion) and the Bill & Melinda Gates Foundation (USD 0.4 billion). The largest recipient countries of these providers were Colombia, the Dominican Republic and Peru.

Further commitments to funding for COVID-19 response were made in 2022 (Commitments show ODA spending on COVID-19 response will continue in 2022, but large funding gaps remain) and some spending in this category is likely to feature in 2022 ODA figures.

The World Health Organization (WHO) estimates that 14.9 million excess deaths were associated with the COVID-19 pandemic in 2020-21, concentrated in Southeast Asia, Europe and the Americas, and in middle-income countries (WHO, 2022[7]). At the end of 2021, the Independent Allocation of Vaccines Group (IAVG) called for 70% coverage of COVID-19 vaccines in all countries by mid-2022 (WHO, 2021[8]). By June 2022, 66.3% of the world population received at least one dose of a COVID-19 vaccine, compared to only 17.8% of people in low-income countries (Our World in Data, 2022[9]).

At the second Global COVID-19 Summit in May 2022 (co-hosted by the US, Belize, Germany, Indonesia and Senegal), commitments of USD 3.2 billion were made in addition to previous commitments in 2022 for COVID-19 response, including commitments of USD 712 million in seed funding for a new pandemic-preparedness and global health security fund at the World Bank (The White House, 2022[10]).

Despite these commitments, the ACT-Accelerator had a funding gap of USD 13 billion for 2021-22 as of 13 June 2022 (WHO, 2022[11]). COVAX has been the most important delivery vehicle of COVID-19 vaccines in sub-Saharan Africa (UNICEF, 2022[12]). However, the number of vaccines delivered to the region by any means fell month-on-month from December 2021, apart from a small increase in May 2022 (UNICEF, 2022[12]). Furthermore, reports of falling demand for vaccines in low- and middle-income countries began to appear in the first half of 2022 (Financial Times, 2022[13]; Devex, 2022[14]).

To value 2021 donations of COVID-19 vaccine doses exceeding domestic supply (i.e., doses that had not been bought specifically for developing countries), DAC members agreed to apply a price of USD 6.72 per dose. According to COVAX, after a surge in the supply of vaccines in 2021, donations are continuing, but at a lower level. There was also a change in the product portfolio, with a larger share accounted for by more expensive vaccines than in 2021. In the second half of 2022, the DAC will discuss whether the average price per vaccine dose needs to be updated.

Note: IAVG performs regular reviews of the COVID-19 Vaccines Global Access initiative (COVAX), which is the vaccines pillar of the WHO’s Access to COVID-19 Tools (ACT) Accelerator, an international collaboration to speed development, production and equitable access to COVID-19 tests, treatments, and vaccines.

In 2020, DAC members’ gross bilateral ODA to all income groups increased as follows: least developed countries rose by 6%; other low income and low-middle income countries by 4% each; and upper-middle income countries by 18%. However, without COVID-19-related aid, gross bilateral ODA fell for all but the upper-middle income group (highlighted cells in ODA by income group with/without COVID-19-related aid, 2019-20).

Concessional outflows by multilateral organisations rose substantially across all income groups due to expenditures from the Global Fund, the African Development Bank, the Asian Development Bank, and EU Institutions. By income group, least-developed countries received the largest share of COVID-19-related funding from all providers (30%), followed by low-middle income countries (28%), upper-middle income countries (13%) and other low-income countries (1%). ODA that is unallocated by region represented 27% of the total.

Note: Highlighted cells show decreases when COVID-19-related funding is excluded.

Source: OECD DAC Statistics (OECD, 2022[3])

In least-developed countries, nearly half of ODA disbursements were spent on the immediate aspects of the pandemic, and focused on health, budget support and humanitarian aid. In low-middle and upper-middle income countries, the focus of assistance was more dispersed (Focus of ODA within each income group, 2020). Budget support was particularly prevalent in least-developed and low-middle income countries.

Note: COVID-19 control includes prevention, treatment and care.

Source: OECD DAC Statistics (OECD, 2022[3])

Excluding expenditures related to the COVID-19 response, ODA to fragile contexts4 from multilateral organisations increased 20%, but from DAC members fell by 5% and from other bilateral providers fell by 7%.

The top 10 recipient countries accounted for 26% of COVID-19-related aid from all providers (calculated from Top recipients of COVID-19-related aid, 2020). Aid not allocated to specific recipients amounted to USD 5.3 billion, of which nearly half was channelled through United Nations (UN) organisations (USD 1.6 billion) and the Coalition for Epidemic Preparedness Innovations, or CEPI, (USD 0.8 billion). In terms of regional allocations, Asia was the largest recipient of COVID-19-related expenditure (USD 8.5 billion) in 2020, followed by Africa (USD 8 billion), the Americas (USD 1.8 billion), and Europe and Oceania (USD 1 billion each).

USD (millions)

Source: OECD DAC Statistics (OECD, 2022[3])

Five countries in fragile contexts received nearly a third of COVID-19-related ODA: Bangladesh (10%), Myanmar (7%), Ethiopia (5%), Cambodia (4%) and Mozambique (4%). Nearly half of total ODA to fragile contexts went to support the health sector, and nearly one-fifth was in the form of humanitarian aid.

Overall, 2020 data show little evidence of re-allocations between sectors, and all sectors received some additional allocations from COVID-19 spending. However, as 2020 budgets were set before the pandemic, it is possible that re-allocations could become apparent in detailed 2021 data,5 where COVID-19 spending was factored in from the beginning of the budget cycle.

In 2020, a large share of COVID-19-related ODA by all providers was spent in the health sector (USD 10.2 billion), focused on COVID-19 control. For example, USD 4.4 billion went to information campaigns, education and communication; testing; prevention; and immunisation, treatment and care. COVID-19 related ODA spent on humanitarian aid was USD 3.2 billion, and programme assistance was USD 2.5 billion, including budget support.

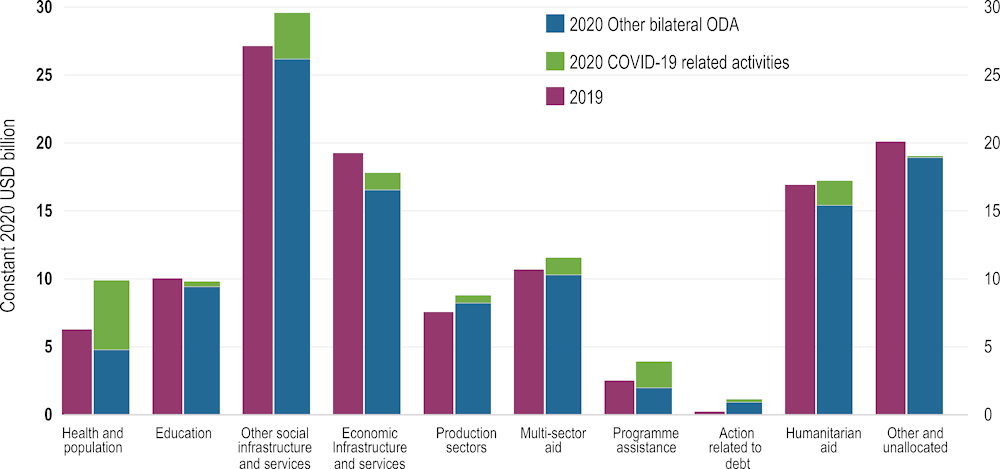

DAC member countries' bilateral ODA by sector, 2019-20 shows the impact of COVID-19 spending between 2019 and 2020 on DAC countries’ bilateral sector allocations, with spending in social sectors up 13% in 2020 – notably for health and population, which increased nearly 60% in real terms compared to 2019, with nearly three-quarters of this increase for addressing the immediate health concerns of the pandemic. Spending for social protection programmes increased by 162% from 2019, to reach nearly USD 2 billion, of which USD 1.3 billion was due to the pandemic. Bilateral ODA to production sectors rose by 16% due to COVID-19-related support for the agriculture sector. Programme assistance rose by 56% including budget support, and humanitarian aid rose by 2%. Multi-sector aid increased by 8% to address cross-dimensional aspects of the pandemic.

Spending for social protection programmes increased by 162% from 2019, to reach nearly USD 2 billion, of which USD 1.3 billion was due to the pandemic.

Constant 2020 USD (billions)

Source: OECD DAC Statistics (OECD, 2022[3])

Severe disruptions to the education system worldwide caused concern about children’s learning and well-being, long-term human capital loss, and that ODA would be allocated away from education to fund the health response. Total ODA by DAC members and multilateral organisations for education remained stable at nearly USD 14 billion per year in 2019 and 2020, and education received USD 390 million in COVID-19-related funding from DAC members (DAC member countries' bilateral ODA by sector, 2019-20). However, the share of ODA to education dropped from 8% of total disbursements in 2019 to 7% in 2020. ODA for basic and secondary education fell 2% each, whereas ODA for post-secondary education remained stable. ODA by DAC members for in-donor scholarships or training also fell 2%.

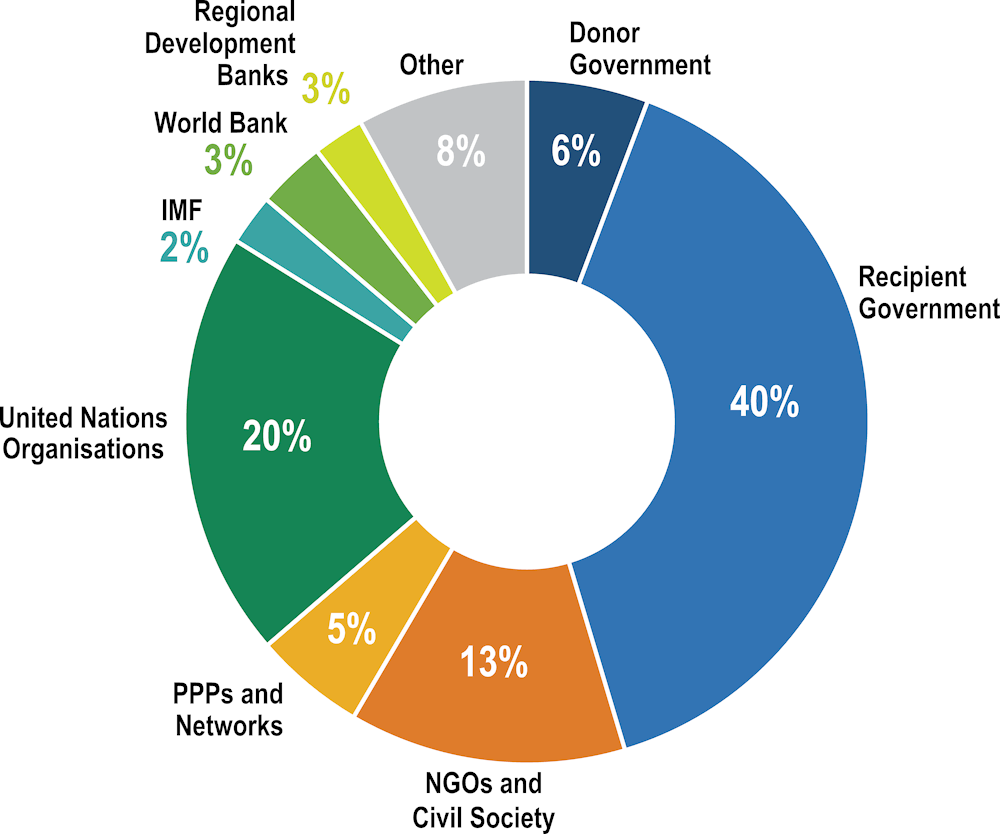

The largest share (40%) of DAC members’ bilateral ODA for the COVID-19 response was channelled directly through recipient governments (Channels of bilateral ODA for COVID-19 response, 2020). Around 30% went through multilateral organisations, of which 20% through UN organisations. Nearly two-thirds of bilateral ODA channelled through UN organisations went through the WHO, the UN Children’s Fund and the World Food Programme. The remaining bilateral ODA went through the donor governments themselves, civil society, public-private partnerships or networks, or other international organisations.

Constant 2020 USD (millions)

Source: OECD DAC Statistics (OECD, 2022[3])

Between 2019 and 2020, bilateral ODA implemented through multilateral organisations rose by 15%. Core contributions (i.e., that are not earmarked) to multilateral organisations rose by 6.7% in 2020 compared to 2019. Multilateral organisations that received the largest ODA flows from DAC countries were the EU Institutions (USD 16.3 billion), the World Bank Group (USD 8.6 billion), and the UN (USD 8.0 billion).

Though ODA levels grew in 2020 and 2021, major appeals by the World Health Organization (WHO), the UN and the International Federation of the Red Cross and Red Crescent Societies (IFRC), for example, remained underfunded by approximately USD 9 billion (COVID-19 response funding appeals and gaps).

Note: WHO data is an aggregation of the 2020 and 2021 SPRPs and the 2022 COVID-19 appeal

Sources: WHO (2020[15]; 2020[16]; 2021[17]; 2022[18]; 2022[19]), UN (2020[20]; 2020[21]; 2021[22]) and IFRC (n.d.[23])

In addition to COVID-19-related appeals going underfunded, the end of 2021 and beginning of 2022 saw an increase in competing demands from other crises (next section). This meant that, while 2021 closed with strong ODA volume in aggregate terms, it was already under pressure to meet expanding needs.

Macroeconomic dynamics are shaping the wider context for ODA supply in 2022, including slowing global growth and rising inflation. At the same time, decisions to respond to escalating needs created by the direct and indirect effects of Russia’s war of aggression against Ukraine could contribute to an increase in ODA volumes in 2022 when countries are able to mobilise additional resources. Furthermore, changes in spending patterns are likely. For example, an increased share of ODA allocated to address food crises or meet other basic needs in Ukraine and other countries could reduce budgets for country-programmable aid. The surge in Ukrainian refugees will drive up in-donor refugee spending, which is ODA-eligible although the impacts across DAC members ODA levels will be uneven. Additionally, development co-operation providers are under pressure to deliver on other commitments, such as responding to climate change and sustaining support for countries most in need. Compounded, these pressures could crowd out providers’ ability to respond to other crises and invest in long-term development goals, unless significant additional financing is mobilised.

Though Ukraine is an ODA-eligible country, not all support to meet the direct and indirect needs created by the war in Ukraine will be ODA-eligible (for example military aid), and the magnitude of demand created is far higher than ODA alone could ever meet. Ultimately, the impact on ODA spending will be determined by a range of intersecting policy decisions by individual governments, regional and multilateral bodies, and other stakeholders in the development co-operation system.

Though Ukraine is an ODA-eligible country, not all support to meet the direct and indirect needs created by the war in Ukraine will be ODA-eligible (for example military aid), and the magnitude of demand created is far higher than ODA alone could ever meet.

In the past, some crises and other developments led to the review or clarification of ODA reporting rules, carried out through agreed procedures and negotiated amongst DAC members (History of ODA classification and accounting rules changes). Any revisions to ODA deemed necessary due to spending changes in response to the war in Ukraine would need to go through similar lengthy procedures, whilst preserving the integrity of ODA, and are therefore unlikely to impact ODA in 2022.

To ensure that DAC statistical collections remain relevant, the DAC has continuously reviewed the ODA methodology since its definition in 1969 to account for new forms of aid. The table below highlights major changes to the definition of ODA during the last 50 years.

Taking recent downward revisions of GDP growth into account, if ODA/GNI levels for all DAC countries remain at 2021 levels in 2022, ODA would reach USD 184 billion, or an increase of USD 5 billion from 2021.6 Prior to the war in Ukraine, global recovery from the COVID-19 pandemic was expected to continue in 2022, with growth in 2023 expected to reach pre-pandemic levels. The December 2021 OECD Economic Outlook projected global GDP growth in 2022 of 4.5% (OECD, 2021[1]). In June 2022, the OECD revised growth estimates downwards for nearly every country, predicting global GDP growth in 2022 at 3.02%, and for Euro area countries at 2.62% (OECD, 2022[27]). While this slowdown could impact decisions on ODA budgets, growth remains positive and many large, development co-operation providers continue to benefit from stimulus packages that cushion fiscal constraints and which could help protect ODA budgets from being cut (The White House, 2021[28]; European Commission, 2022[29]).

Growth is slowing further in low- and middle-income countries due to the impact of the war. The World Bank estimates that growth in Africa will be 3.6% in 2022, down from 4% in 2021 (Girma Abreha et al., 2022[30]). Though oil-exporting countries are benefitting from the elevated price of oil, the fiscal margin for manoeuvre remains small in most African countries (Girma Abreha et al., 2022[30]), potentially increasing demand for and levels of ODA reliance, at least in the short term.

ODA would need to rise by an additional USD 8-10 billion to compensate for the rising inflation. OECD countries began 2022 with high inflation. On average, OECD countries are projected to see an 8.77% year-on-year increase in inflation rates in 2022, nearly double the projection in December 2021 (OECD, 2022[27]). In April 2022, energy prices in OECD countries had risen by 32.7% over the previous year, and food prices had risen by 11.5% (OECD, 2022[31]).

In addition to eroding consumer confidence, inflation pressures national budgets with higher costs and the need to mitigate the effects of sudden increases in the price of necessities like food and fuel on vulnerable populations. These pressures come after a period when most OECD countries had already increased general government spending from 2019 to 2020 (OECD, 2022[32]) in response to the COVID-19 pandemic. Inflation can also devalue currencies relative to others, and makes goods and services procured to support low- and middle-income countries more expensive, eroding the purchasing power of ODA budgets. For example, the World Food Programme notes that food prices are up 30% compared to 2019, exacerbated by the war in Ukraine (WFP, 2022[33]).

In sub-Saharan Africa, food and non-food inflation has been increasing since 2020, expected to remain at 12.2% in 2022 then drop to 9.6% in 2023 (IMF, 2022[34]). The International Monetary Fund (IMF) warns that risks to the inflation outlook remain, including Russia waging a prolonged war against Ukraine and exchange-rate pressures (IMF, 2022[34]). As prices rise, so does poverty, compounding the pressure on ODA. Inflation impacts poor households more because they rely on wages, spend a larger portion of their income on goods such as food and energy, and have less access to financial products and services that could cushion the impacts of inflation (Gill and Nagle, 2022[35]). The World Bank predicts the combined impact of the COVID-19 crisis, inflationary pressures and the war in Ukraine will leave 75-95 million more people in poverty in 2022 than according to pre-pandemic projections (World Bank, 2022[36]).

A cost-of-living crisis for many of the poorest households could mean that development co-operation providers are called on to support greater social protection spending to help alleviate strain. Sudden increases in the cost of staple goods have been linked to rising instability, which could increase humanitarian needs. ODA from all providers for social protection increased from USD 2.61 billion in 2019 to USD 7.76 billion in 2020, in response to the COVID-19 crisis. Many social protection measures put in place in 2020 and 2021 could be used to support populations with current needs.

When food prices rose 11.3% between 2010 and 2011 (FAO, 2022[37]), it is estimated that global poverty increased by 1% (Ha, Ayhan Kose and Ohnsorge, 2019[38]). In 2022, food prices are expected to rise 17.7% on top of the substantial increase in 2021.7 The impact could be catastrophic for poverty and hunger, already at historically high levels due to COVID-19 and climate change. Before the war in Ukraine, 811 million people in the world suffered from hunger (WFP, 2022[33]). At the time of Russia’s invasion, the WFP predicted that 47 million people would be added to the 276 million already suffering acute hunger (WFP, 2022[33]). West Africa was expected to see the largest increase in acute hunger (24%), followed by East Africa and Southern Africa (WFP, 2022[39]). The WFP is calling for USD 21.5 billion in support this year (WFP, 2022[33]). In 2020, ODA providers allocated about a quarter of this amount, USD 5.87 billion, for emergency food assistance. In late June 2022, the G7 committed to provide an additional USD 4.5 billion to support global food and nutrition security (G7, 2022[40]).

In addition, higher planting costs due to a scarcity of fertiliser are predicted to affect long-term food prices around the world. Russia is a key exporter of the three major groups of fertilisers: nitrogen, phosphorus and potassium (Kennes, 2022[41]). It is also among the largest producers of urea and potash needed to make ammonia (FAO, 2019[42]). The price of urea more than doubled between September 2021 and March 2022 (IEA, 2022[43]). These higher input prices are likely to hurt domestic food production through lower yields and higher prices in developing countries long into the future (World Bank, 2022[44]). Smallholder farmers are likely to be impacted the worst.

The pace of progress towards the Sustainable Development Goal for energy access (SDG 7) had already slowed due to COVID-19 disruptions, and Africa remains the least electrified region in the world, with 568 million people without access (World Bank, 2022[45]). Energy costs had been rising in 2021 and early 2022, when the invasion of Ukraine added major disruption to fossil-fuel markets, re-drawing traditional trading relationships and cutting off supply routes. Concerns now are that developing countries could pivot towards more polluting forms of energy, especially coal, to meet their needs (World Bank, 2022[44]). In contrast, others point out that tightening in the global energy market could lead to investment in clean-energy innovations, as occurred after the energy crisis of the 1970s (IEA, 2022[46]). The falling costs of technology (Schwerhoff and Sy, 2020[47]) and the fact that renewable energies are not impacted by the volatility of fossil-fuel markets (IRENA, 2020[48]) could precipitate this change. Support is needed to keep green transitions on track and achieve the Paris Agreement.

Annual global public investment required to reach a net-zero scenario by 2050 is USD 1.2 trillion (IEA, 2021[49]), while ensuring universal energy access would cost USD 51 billion annually (SE4All, 2019[50]). At the 2021 COP26 in Glasgow, projections and commitments indicated that the goal of mobilising USD 100 billion per year (by developed countries for climate action in developing countries) would be met by 2023 and would be majority financed from public sources (UKCOP26, 2021[51]). Ahead of COP26, the DAC committed to align development co-operation with the goals of the Paris Agreement (OECD, 2021[52]). Official donors spent a combined USD 11.8 billion on energy-related ODA in 2020 (ODA allocated to energy, 2011-20), representing 9% of ODA to developing countries that year. Accelerating the clean energy transition would require a significant shift in financing trends and meeting much higher capital requirements (IEA, 2021[49]).

Constant 2020 USD (millions)

Note: Gross disbursements in constant prices

Source: OECD DAC Statistics (OECD, 2022[3])

Actions and funding decisions by development co-operation providers beyond the DAC could also ease cost pressures and bolster financing for energy transitions. In response to rising prices since the outbreak of the war in Ukraine, members of the International Energy Agency (IEA) released 60 million barrels from emergency stocks on 1 March 2022 and 120 million barrels on 1 April 2022 (IEA, 2022[53]) – two of only five times they ever took collective action. Current spare oil capacity is concentrated in Saudi Arabia and the UAE,8 both of which are benefitting from the higher price of oil (OECD, 2022[27]). Saudi Arabia is one of the few countries where GDP growth was revised upwards between December 2021 and June 2022 (OECD, 2022[27]). The benefits from higher oil prices stand in contrast to the fall in both countries’ ODA in recent years. From 2018 to 2021, Saudi Arabia’s ODA/GNI dropped from 0.56% to 0.30%, while the UAE’s decreased from 0.93% to 0.40%. ODA volumes also decreased considerably over these years.9

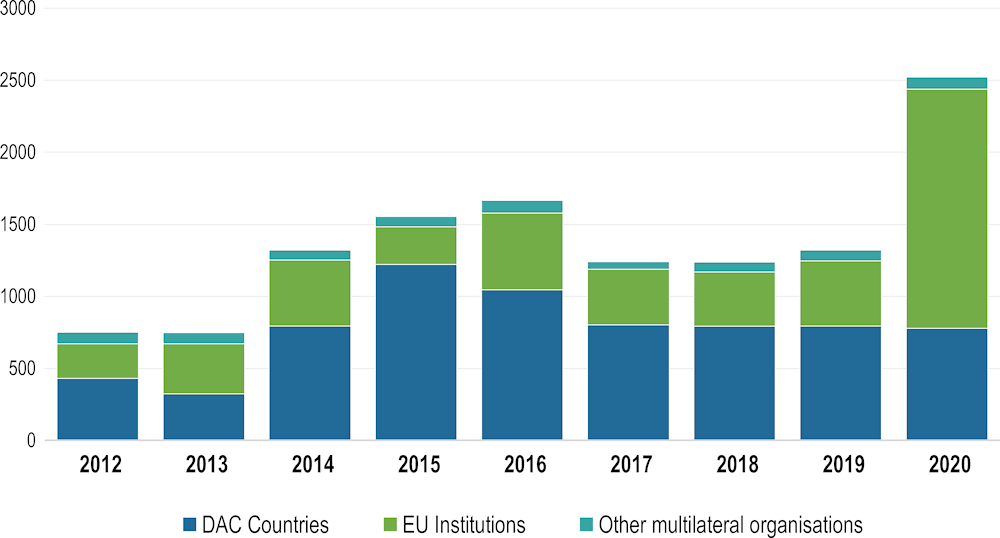

In 2020, Ukraine received USD 2.55 billion in ODA from all official donors, of which USD 1.74 billion was from multilateral organisations (DAC country and multilateral ODA to Ukraine, 2012-20). Of multilateral spending, 79% was in the form of a standard loan from EU Institutions to the Central Government, mainly for general budget support and infrastructure investments in energy, public transport and upgrading food-industry value chains. The US and Germany were the largest DAC-country ODA providers to Ukraine in 2020, while the overall ODA increase in 2020 was driven by EU spending. The volume of DAC country disbursements to Ukraine peaked in 2015 (following the 2014 annexation of Crimea, mostly from Germany and the US).

Constant 2020 USD (millions)

Note: Figures represent gross disbursements in constant prices.

Source: OECD DAC Statistics (OECD, 2022[3])

The economic loss, destruction and reconstruction costs for Ukraine are magnitudes larger than ODA support received in recent years. The Government of Ukraine recently communicated that it requires USD 7 billion per month to make up for economic losses caused by the war (Reuters, 2022[54]) and costs will remain high and unpredictable while Russia continues its aggression against Ukraine. As of 16 June 2022, DAC members had committed USD 46 billion in financial and humanitarian assistance to Ukraine (DAC members’ financial and humanitarian aid commitments for Ukraine and % equivalent of 2021 ODA). While not every activity will be ODA-eligible, given that this sum represents 25.7% of total ODA in 2021, re-allocating budgets to cover even a portion of this amount would have a devastating impact on other recipient countries and crises that require support. US support constitutes nearly half of the total, funded through the Additional Ukraine Supplemental Appropriations Act (U.S. Department of State, 2022[55]), and is therefore likely to be additional rather than re-allocated budget. Multilateral organisations are also increasing support. The World Bank mobilised a package of USD 4 billion for Ukraine (World Bank, 2022[56]) and the IMF board approved a multi-donor administered account for Ukraine (IMF, 2022[57]). Of the financial aid committed, half is loans, 36% is grants, and the remainder is guarantees and central bank swap lines (Kiel Institute for the World Economy, 2022[58]). By June 2022, loans from EU Institutions were playing the largest part in financial aid to Ukraine (EUR 12.2 billion) (Kiel Institute for the World Economy, 2022[58]). The figures presented in this section represent commitments and not disbursements. Under the DAC recommendation on good pledging practice, members commit to strive to observe the principles of clarity, comparability, realism, measurability, accountability and transparency (OECD, 2011[59]) and this instrument should guide member actions in the current context. The OECD will work with members to support them to achieve the principles of this recommendation.

As of 16 June, DAC members had committed USD 46 billion in financial and humanitarian assistance to Ukraine.

Conversations are underway about how to respond to the reconstruction needs of Ukraine. Estimates vary (Estimated costs of reconstruction and recovery in Ukraine), but most agree that compensating economic losses and financing re-building and modernisation will run to the hundreds of billions, if not trillions of dollars. Calls for a “Marshall Plan for Ukraine” indicate that innovation in mechanisms of pooled funding and disbursements will be needed like after World War II (Eichengreen, 2022[60]). The Government of Ukraine has established a National Council for the Reconstruction of Ukraine from the Effects of War, which is developing a recovery plan. Reconstruction will be a massive undertaking, requiring input and expertise from the private sector. There are also calls for seized Russian assets or reparations to contribute.

Losses and destruction incurred to date are at devastating proportions. But the trajectory and length of the war in Ukraine will be the greatest determinant of how much reconstruction and recovery will cost.

The war in Ukraine has caused large economic losses. The World Bank estimates that the Ukrainian economy will shrink 45% in 2022 because of the war (World Bank, 2022[61]). Estimates by the Kyiv School of Economics (2022[62]) suggest that total economic losses as of 3 May 2022 reached USD 564‑600 billion. Damages of USD 92 billion to infrastructure have been documented, including 33 million m2 in lost residential housing and 23 800 km of roads (Kyiv School of Economics, 2022[62]).

While it is too early to determine the cost of reconstruction, especially with unclear prospects for how Russia’s aggression against Ukraine will unfold, estimates have been made. Some, based on an aggregation of capital stock per capita, range from USD 330 billion to USD 550 billion (Becker et al., 2022[63]). Others, based on war efforts, the cost of rebuilding infrastructure, civilian losses (e.g., housing), and the loss of current and future revenue, range from USD 500 billion to USD 1 trillion (Becker et al., 2022[63]).

Central to Ukraine’s plans for reconstruction is building a foundation for growth and modernisation, as the country works towards accession to the EU. There are opportunities to modernise the productive capacity of Ukraine through technological advances, infrastructure reconstruction and training, with a focus on human capital (Becker et al., 2022[63]). Modernisation can also be pursued in the wider infrastructure, housing and energy sectors, with a view to promoting a greening of the country.

Humanitarian funding has held relatively steady around 10% of total ODA since 2014. To date the humanitarian commitments by DAC members to Ukraine alone are equivalent to 7% of total 2021 ODA. Assuming development co-operation providers earmarked a similar proportion of ODA for humanitarian reserves in 2022, the resources remaining to respond to humanitarian crises elsewhere are severely diminished. In May 2022, 303 million people in 69 countries needed humanitarian aid and protection, 29 million more than in December 2021 (UN News, 2022[64]). Humanitarian needs in the Central Sahel region increased in 2021, but only 41% of the funding requirements were met between 2020 and 2021 (OCHA, 2022[65]). The UN launched the largest single-country aid appeal ever (at that time) in early 2022 to raise USD 5 billion for Afghanistan (UN, 2022[66]), of which 31.9% is currently covered (UNOCHA, 2022[67]). The United Nations Office for the Coordination of Humanitarian Affairs (UNOCHA) estimates that Yemen and Syria will each require approximately USD 4 billion in 2022, currently one-quarter funded (UNOCHA, 2022[67]). The size of rations to families in Syria and Yemen were reduced due to funding gaps (WFP, 2022[68]). Significant funding gaps also remain for COVID-19 response.

Unless all components of ODA rise together, re-directing spending to focus 2022 ODA on the crisis in Ukraine would have significant adverse impacts elsewhere in the world, diminishing a traditionally stable source of support at the moment countries and households face severe economic issues and deprivations.

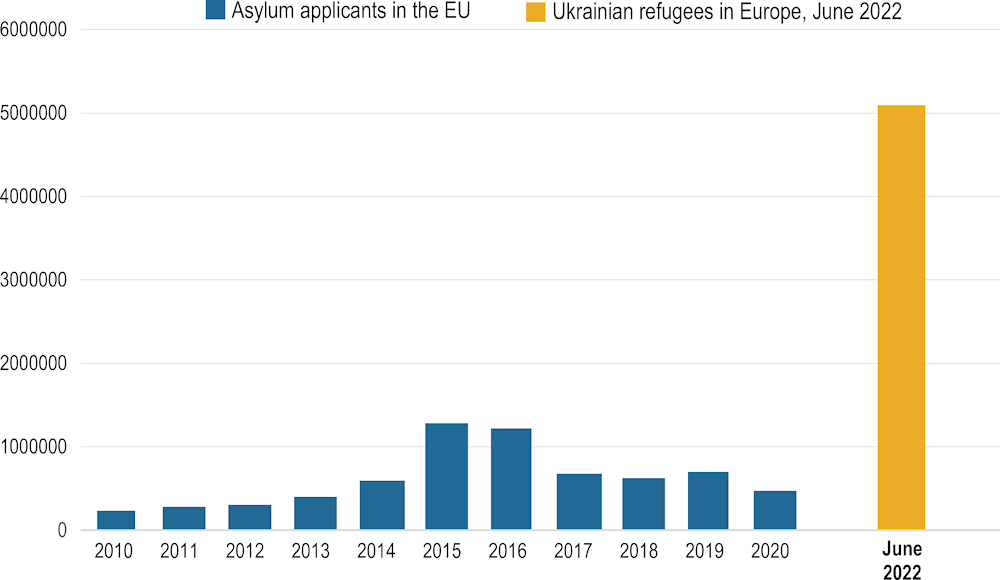

Development co-operation providers must choose how to cover the cost of meeting the needs of Ukrainian refugees. As of 16 June 2022, approximately 5 million refugees from Ukraine were recorded across Europe (UNHCR, 2022[69]), 65% of which are in DAC countries (DAC members’ spending on in-donor refugee costs, number of Ukrainian refugees, anticipated costs, % 2021 ODA). As EU asylum applicants, 2010-20, and Ukrainian refugees in Europe, June 2022 shows, this far outpaces flows in the previous decade, when European Union (EU) countries dealt with the highest numbers of asylum seekers in 2015 and 2016 (1.28 million and 1.22 million respectively) (EU, 2022[70]). In 2016, in-donor refugee costs amounted to USD 16 billion and represented 11.0% of total ODA.

Note: Asylum applicants are considered those who applied for international protection. The solid yellow bar is the number of Ukrainian refugees registered in Europe on 14 June 2022.

Source: (OECD, 2022[2]) with number of Ukrainian refugees updated on 14 June 2022 from (UNHCR, 2022[69])

The situations in 2015-16 and today are not directly analogous. The EU’s Temporary Protection Scheme means that Ukrainians crossing into the bloc do not need to apply for asylum and automatically have the right to live and work in the EU (EU, 2022[71]). In addition, the European Investment Bank (EIB) Board approved a EUR 4 billion credit line to support the integration of refugees in Ukraine in EU countries (EU, 2022[72]). However, in terms of ODA impact, it is helpful to note that in 2015-16, DAC members took a range of approaches to dealing with in-donor refugee costs: some did not consider them ODA, others used different budgets to cover costs. Sweden implemented a cap for in-donor refugee costs of 30% of its ODA budget. Other donors set up more flexibility in multi-year budget appropriations.

In 2021, in-donor refugee costs amounted to USD 9.3 billion, practically unchanged in real terms compared to 2020, representing 5.2% of DAC countries’ total ODA. Estimates using a baseline costing method show that meeting the anticipated cost of only Ukrainian refugees in DAC countries would account for 10.9% of their total ODA if levels remain unchanged from 202110 (DAC members’ spending on in-donor refugee costs, number of Ukrainian refugees, anticipated costs, % 2021 ODA). The costs of refugees originating from other countries would be additional. The impact will not be equal across countries. Poland received the highest number of Ukrainian refugees (1.1 million), followed by Germany, the Czech Republic, Türkiye and Italy, each of which received fewer than one million (2021 in-donor refugee costs and anticipated costs (3 months) of Ukrainian refugees in selected countries). Germany mobilised additional budget to offset in-donor refugee costs, while Poland and the Czech Republic face costs far higher than their total 2021 ODA budgets. Poland and the Czech Republic are also among the top 10 countries with the largest projected rises in inflation, making the cost of refugees even harder to pay (OECD, 2022[27]). In contrast, the anticipated cost of Ukrainian refugees for three months in Germany, Türkiye and Italy represents a relatively small portion of their ODA budgets.

Germany mobilised additional budget to offset in-donor refugee costs, while Poland and the Czech Republic face costs far higher than their total 2021 ODA budgets.

Countries that announced plans to re-direct ODA to cover in-donor refugee costs (Denmark, the Netherlands, Sweden, Norway) received a comparatively smaller number of Ukrainian refugees, though more than the asylum applications they received in 2021 (2021 in-donor refugee costs and anticipated costs (3 months) of Ukrainian refugees in selected countries). Though Norway initially announced plans to re-allocate NOK 4 billion (USD 417 million) to in-donor refugee costs (Government of Norway, 2022[73]), in mid-June 2022, this re-allocation was partially reversed (Donor Tracker, 2022[74]). Concerns have been raised about the impact of re-allocations on other ODA recipients (Chadwick, 2022[75]).

Note: Anticipated cost uses the Kiel Institute’s baseline cost of EUR 500 per refugee per month for three months, using a conversion rate of EUR 1 = USD 1.0624. Only the top five Ukrainian-refugee-receiving countries and DAC members that announced changes to ODA budgets regarding in-donor refugee costs are shown. The refugee situation is dynamic and this table is accurate as of mid-June 2022. Calculations of share of 2021 ODA represented by anticipated in-donor costs for Ukrainian refugees are for comparative purposes only.

Source: In-donor refugee costs 2021 from DAC1 Table, Net Disbursement (OECD, 2022[3]). Number of asylum applications received 2021 (UNHCR, 2022[76]). Number of Ukrainian refugees received from (UNHCR, 2022[69]) and anticipated cost from (Kiel Institute for the World Economy, 2022[58]). Announced adjustment to ODA budgets: (BMZ, 2022[77]); (The Government of the Netherlands, 2022[78]); (Government Offices of Sweden, 2022[79]); (Denmark Ministry of Foreign Affairs, 2022[80]); (Government of Norway, 2022[73]); (Donor Tracker, 2022[74]).

As of April 2022, eight countries were in debt distress and a further 30 were at high risk (IMF, 2022[81]). Public debt in Africa has been rising since 2011 and accelerated in 2020 as governments borrowed to fund COVID-19 responses (Girma Abreha et al., 2022[30]). Debt in the Middle East and Central Asia increased by three percentage points of GDP in 2021, on top of an increase in 2020 (IMF, 2022[82]). Increased borrowing costs are impacting low- and middle-income countries’ ability to finance debt on international markets and complicating the management of high debt levels, for example in Latin America and the Caribbean (IMF, 2022[83]). Addressing the direct and indirect impacts of the war in Ukraine without adding to debt vulnerability is now a widespread policy challenge (IMF, 2022[34]).

Debt restructuring, suspension or forgiveness is now more complex than in the past. The composition of debt, particularly in Africa, changed substantially in recent decades, with more private creditors, bilateral creditors from non-Paris Club countries (predominantly China) and a shift towards domestic government debt (IMF, 2022[34]). The G20 Common Framework for Debt Treatments, a successor to the Debt Service Suspension Initiative agreed during the COVID-19 crisis, has come under criticism from the IMF (Georgieva and Pazarbasioglu, 2021[84]) and the World Bank (Malpass, 2021[85]), and the G20 itself called for next steps to be “more timely, orderly and predictable” (Bretton Woods Project, 2022[86]). Should debt treatment under the Common Framework become more frequent in 2022, this could increase recorded ODA for debt relief, depending on the type of debt and decisions over its treatment.

An additional instrument that could contribute to easing debt is the potential re-allocation of Special Drawing Rights (SDRs). In August 2021, the equivalent of USD 650 billion in IMF SDRs became effective in accordance with countries’ existing quotas (IMF, 2021[87]). The IMF is now exploring options to re-allocate or channel SDRs to more vulnerable economies from advanced economies that receive a larger share due to the quota system. The options include increasing the size of the Poverty Reduction and Growth Trust (PRGT), channelling through the Resilience and Sustainability Trust (RST) or channelling SDRs to other SDR-holder organisations, including the World Bank (Pazarbasioglu and Ramakrishnan, 2021[88]). Discussions regarding the ODA-eligibility of SDR re-allocation are ongoing.

In 2022 alone, low-income countries will need to make debt service payments of USD 53 billion (World Bank, 2022[89]), which could put pressure on domestic spending and drive reliance on ODA.

While it is impossible to predict the level of total ODA for 2022, OECD members are stepping up with new and additional assistance for Ukraine, the Ukrainian refugee crisis and to mitigate deepening food insecurity, hunger and extreme poverty across the globe. Fulfilling these commitments and other development commitments will drive up ODA levels in 2022. Nevertheless, the international community will need to manage carefully the risk that budgets and programmes for countries most in need and the SDGs will be crowded out by today’s emergencies and crises. Other development finance flows, including private finance, other official flows and development finance from providers beyond the DAC must also step up to meet the magnitude of need. The world’s compounding crises and others that might lie ahead raise questions about how to balance demands for emergency response with commitments to longstanding crises and long-term development goals. ODA is a precious resource for those most left behind, and must be allocated where it is needed most.

Note: Data are correct as of 16 June 2022. 2021 ODA data are preliminary. Table arranged in descending order of total commitments. Calculations of the equivalent share of 2021 ODA represented by commitments are for comparative purposes only. Commitments do not equal disbursements.

Source: Financial and humanitarian commitment from (Kiel Institute for the World Economy, 2022[58]); % ODA calculated from OECD statistics.

Note: 2021 ODA data are preliminary. Number of individual Ukrainian refugees as of 14 June 2022. Anticipated cost uses the Kiel Institute’s baseline cost of EUR 500 per refugee per month for three months, converted using a rate of EUR 1 = USD 1.0624. Calculations of share of 2021 ODA represented by anticipated in-donor costs for Ukrainian refugees are for comparative purposes only.

Source: In-donor refugee costs 2021 from DAC1 Table, Net Disbursement (OECD, 2022[3]). Number of Ukrainian refugees from (UNHCR, 2022[69]) and anticipated cost from (Kiel Institute for the World Economy, 2022[58]).

[4] Ahmad, Y. et al. (2020), “Six decades of ODA: insights and outlook in the COVID-19 crisis”, in Development Co-operation Profiles 2020, OECD Publishing, Paris, https://www.oecd-ilibrary.org/sites/5e331623-en/index.html?itemId=/content/component/5e331623-en#chapter-d1e20 (accessed on 20 November 2020).

[63] Becker, T. et al. (2022), “A blueprint for the reconstruction of Ukraine”, Rapid Response Economics, Vol. 1, https://cepr.org/sites/default/files/news/BlueprintReconstructionUkraine.pdf (accessed on 25 May 2022).

[77] BMZ (2022), Federal cabinet approves supplementary budget for Ukraine: EUR 1 billion earmarked for development cooperation | BMZ, https://www.bmz.de/de/aktuelles/aktuelle-meldungen/bundeskabinett-verabschiedet-ukraine-ergaenzungshaushalt-108294 (accessed on 21 June 2022).

[86] Bretton Woods Project (2022), G20 press briefing analysis – Spring Meetings 2022 - Bretton Woods Project, https://www.brettonwoodsproject.org/2022/04/g20-press-briefing-analysis-spring-meetings-2022/ (accessed on 20 May 2022).

[75] Chadwick, V. (2022), “UN leaders target Norway over proposed budget cuts”, Devex, https://www.devex.com/news/un-leaders-target-norway-over-proposed-budget-cuts-103245 (accessed on 1 June 2022).

[80] Denmark Ministry of Foreign Affairs (2022), Omprioritering af udviklingsmidler til ukrainske flygtninge i Danmark | Udenrigsministeriet, https://via.ritzau.dk/pressemeddelelse/omprioritering-af-udviklingsmidler-til-ukrainske-flygtninge-i-danmark?publisherId=2012662&releaseId=13646873 (accessed on 23 June 2022).

[90] Development Assistance Committee (DAC) Working Party on Development Finance Statistics (2022), Valuation of donations of excess COVID-19 vaccine doses to developing countries in ODA, https://www.who.int/initiatives/who-listed-authority-reg- (accessed on 28 June 2022).

[14] Devex (2022), COVID-19 vaccine delivery and demand ‘slowing down’ | Devex, https://www.devex.com/news/covid-19-vaccine-delivery-and-demand-slowing-down-103187 (accessed on 10 May 2022).

[74] Donor Tracker (2022), Norway reverses US$281 million in cuts to development due to Ukraine crisis after pushbacks, https://donortracker.org/policy-updates/norway-reverses-us281-million-cuts-development-due-ukraine-crisis-after-pushbacks (accessed on 28 June 2022).

[60] Eichengreen, B. (2022), Shaping a Marshall Plan for Ukraine, https://www.diplomaticourier.com/posts/shaping-a-marshall-plan-for-ukraine (accessed on 10 June 2022).

[72] EU (2022), €4 billion credit line to support Ukrainian refugees, https://ec.europa.eu/commission/presscorner/detail/en/IP_22_3202 (accessed on 24 May 2022).

[71] EU (2022), Information for people fleeing the war in Ukraine | European Commission, https://ec.europa.eu/info/strategy/priorities-2019-2024/stronger-europe-world/eu-solidarity-ukraine/eu-assistance-ukraine/information-people-fleeing-war-ukraine_en#your-rights-in-the-eu (accessed on 24 May 2022).

[70] EU (2022), Irregular arrivals to the EU (2008-2022) - Consilium, https://www.consilium.europa.eu/en/infographics/irregular-arrivals-since-2008/ (accessed on 24 May 2022).

[29] European Commission (2022), Recovery plan for Europe | European Commission, https://ec.europa.eu/info/strategy/recovery-plan-europe_en (accessed on 17 June 2022).

[37] FAO (2022), FAO Food Price Index | World Food Situation | Food and Agriculture Organization of the United Nations, https://www.fao.org/worldfoodsituation/foodpricesindex/en/ (accessed on 24 May 2022).

[42] FAO (2019), World fertilizer trends and outlook to 2022, https://www.fao.org/3/ca6746en/ca6746en.pdf (accessed on 15 June 2022).

[13] Financial Times (2022), Demand for Covid vaccines falls amid waning appetite for booster shots | Financial Times, https://www.ft.com/content/9ac9f8fc-1ab3-4cb2-81bf-259ba612f600 (accessed on 10 May 2022).

[40] G7 (2022), G7 Leaders’ Communiqué - Executive summary - Consilium, https://www.consilium.europa.eu/en/press/press-releases/2022/06/28/g7-leaders-communique/ (accessed on 29 June 2022).

[84] Georgieva, K. and C. Pazarbasioglu (2021), The G20 Common Framework for Debt Treatments Must Be Stepped Up – IMF Blog, https://blogs.imf.org/2021/12/02/the-g20-common-framework-for-debt-treatments-must-be-stepped-up/ (accessed on 20 May 2022).

[35] Gill, I. and P. Nagle (2022), Inflation could wreak vengeance on the world’s poor, Brookings, https://www.brookings.edu/blog/future-development/2022/03/18/inflation-could-wreak-vengeance-on-the-worlds-poor/ (accessed on 20 May 2022).

[30] Girma Abreha, K. et al. (2022), “Africa’s Pulse, No. 25, April 2022”, https://doi.org/10.1596/978-1-4648-1871-4.

[73] Government of Norway (2022), Government proposes record-high aid budget of NOK 44.9 billion - regjeringen.no, https://www.regjeringen.no/en/aktuelt/record-high-aid-budget/id2912567/ (accessed on 21 June 2022).

[79] Government Offices of Sweden (2022), Humanitarian assistance fully safeguarded as refugee costs increase in 2022 - Government.se, https://www.government.se/articles/2022/05/humanitarian-assistance-fully-safeguarded-as-refugee-costs-increase-in-2022/ (accessed on 21 June 2022).

[38] Ha, J., M. Ayhan Kose and F. Ohnsorge (eds.) (2019), Inflation in Emerging and Developing Economies, https://www.worldbank.org/en/research/publication/inflation-in-emerging-and-developing-economies (accessed on 20 May 2022).

[6] House of Commons Library (2021), Reducing the UK’s aid spending in 2021 - House of Commons Library, https://commonslibrary.parliament.uk/research-briefings/cbp-9224/ (accessed on 20 June 2022).

[53] IEA (2022), Frequently Asked Questions on Energy Security – Analysis - IEA, https://www.iea.org/articles/frequently-asked-questions-on-energy-security (accessed on 1 June 2022).

[43] IEA (2022), Gas Market Report, Q2-2022, https://www.iea.org/reports/gas-market-report-q2-2022.

[46] IEA (2022), Today’s energy crisis makes supporting clean energy start-ups more important than ever - News - IEA, https://www.iea.org/news/today-s-energy-crisis-makes-supporting-clean-energy-start-ups-more-important-than-ever (accessed on 1 June 2022).

[49] IEA (2021), The cost of capital in clean energy transitions – Analysis - IEA, https://www.iea.org/articles/the-cost-of-capital-in-clean-energy-transitions (accessed on 15 June 2022).

[23] IFRC (n.d.), “Global: COVID-19 pandemic - financial information”, Global, https://go.ifrc.org/emergencies/3972#financial-information (accessed on 20 May 2022).

[57] IMF (2022), IMF Executive Board Approves the Establishment of a Multi-Donor Administered Account for Ukraine, https://www.imf.org/en/News/Articles/2022/04/08/pr22111-imf-executive-board-approves-establishment-of-a-multi-donor-administered-account-for-ukraine (accessed on 29 May 2022).

[81] IMF (2022), List of LIC DSAs for PRGT-Eligible Countries, As of April 30, 2022, https://www.imf.org/external/pubs/ft/dsa/dsalist.pdf (accessed on 20 May 2022).

[82] IMF (2022), Regional Economic Outlook April 2022 Middle East Central Asia, https://www.imf.org/en/Publications/REO/MECA/Issues/2022/04/25/regional-economic-outlook-april-2022-middle-east-central-asia (accessed on 8 June 2022).

[83] IMF (2022), Regional Economic Outlook for the Western Hemisphere, April 2022, https://www.imf.org/en/Publications/REO/WH/Issues/2022/04/22/regional-economic-outlook-for-western-hemisphere-april-2022 (accessed on 8 June 2022).

[34] IMF (2022), Sub-Saharan Africa Economic Outlook - At a Glance - IMF Data, https://data.imf.org/?sk=5778f645-51fb-4f37-a775-b8fecd6bc69b (accessed on 20 May 2022).

[87] IMF (2021), 2021 General SDR Allocation, https://www.imf.org/en/Topics/special-drawing-right/2021-SDR-Allocation (accessed on 20 May 2022).

[48] IRENA (2020), Renewable Power Generation Costs in 2020, https://www.irena.org/publications/2021/Jun/Renewable-Power-Costs-in-2020 (accessed on 17 June 2022).

[41] Kennes, D. (2022), The Russia-Ukraine War’s Impact on Global Fertilizer Markets, https://research.rabobank.com/far/en/sectors/farm-inputs/the-russia-ukraine-war-impact-on-global-fertilizer-markets.html (accessed on 15 June 2022).

[58] Kiel Institute for the World Economy (2022), Ukraine Support Tracker | Kiel Institute, https://www.ifw-kiel.de/topics/war-against-ukraine/ukraine-support-tracker/ (accessed on 27 May 2022).

[62] Kyiv School of Economics (2022), “Direct damage caused to Ukraine’s infrastructure during the war has reached almost $92 billion”, Kyiv School of Economics, https://kse.ua/about-the-school/news/direct-damage-caused-to-ukraine-s-infrastructure-during-the-war-has-reached-almost-92-billion/ (accessed on 24 May 2022).

[85] Malpass, D. (2021), Remarks by World Bank Group President David Malpass to the G20 Leaders’ Summit – Session I: Global Economy and Health, https://www.worldbank.org/en/news/speech/2021/10/30/remarks-by-world-bank-group-president-david-malpass-to-the-g20-leaders-summit-session-i-global-economy-and-health (accessed on 20 May 2022).

[65] OCHA (2022), Crisis in Central Sahel is outpacing humanitarian funding - Burkina Faso | ReliefWeb, https://reliefweb.int/report/burkina-faso/crisis-central-sahel-outpacing-humanitarian-funding (accessed on 8 June 2022).

[92] OECD (2022), Development Co-operation Profiles – Saudi Arabia, https://www.oecd-ilibrary.org/sites/b2156c99-en/index.html?itemId=/content/component/5e331623-en&_csp_=b14d4f60505d057b456dd1730d8fcea3&itemIGO=oecd&itemContentType=chapter (accessed on 28 June 2022).

[93] OECD (2022), Development Co-operation Profiles – United Arab Emirates, https://www.oecd-ilibrary.org/sites/153f7558-en/index.html?itemId=/content/component/5e331623-en&_csp_=b14d4f60505d057b456dd1730d8fcea3&itemIGO=oecd&itemContentType=chapter (accessed on 28 June 2022).

[32] OECD (2022), General government - General government spending - OECD Data, https://data.oecd.org/gga/general-government-spending.htm#indicator-chart (accessed on 20 May 2022).

[31] OECD (2022), Inflation (CPI) (indicator), https://doi.org/10.1787/eee82e6e-en (accessed on 10 June 2022).

[2] OECD (2022), OECD Economic Outlook, Interim Report March 2022: Economic and Social Impacts and Policy Implications of the War in Ukraine, OECD Publishing, Paris, https://doi.org/10.1787/4181d61b-en.

[27] OECD (2022), OECD Economic Outlook, Volume 2022 Issue 1: Preliminary version, OECD Publishing, Paris, https://doi.org/10.1787/62d0ca31-en.

[3] OECD (2022), OECD Statistics, https://stats.oecd.org/ (accessed on 27 May 2022).

[52] OECD (2021), OECD DAC Declaration on a new approach to align development co-operation with the goals of the Paris Agreement on Climate Change - OECD, https://www.oecd.org/dac/development-assistance-committee/dac-declaration-climate-cop26.htm (accessed on 29 May 2022).

[1] OECD (2021), OECD Economic Outlook, Volume 2021 Issue 2, OECD Publishing, Paris, https://doi.org/10.1787/66c5ac2c-en.

[25] OECD (2021), “Official Development Assistance (ODA) | What is ODA?”, https://www.oecd.org/dac/financing-sustainable-development/development-finance-standards/What-is-ODA.pdf (accessed on 28 June 2022).

[5] OECD (2020), Global Outlook on Financing for Sustainable Development 2021: A New Way to Invest for People and Planet, OECD Publishing, Paris, https://doi.org/10.1787/e3c30a9a-en.

[59] OECD (2011), DAC recommendation on good pledging practice, https://legalinstruments.oecd.org/en/instruments/OECD-LEGAL-5018 (accessed on 28 June 2022).

[26] OECD (2011), Measuring aid: 50 years of DAC Statistics, 1961-2011.

[91] OECD (n.d.), Conflict & Fragility - OECD, https://www.oecd.org/dac/conflict-fragility-resilience/conflict-fragility/ (accessed on 28 June 2022).

[24] OECD (n.d.), Development finance standards - OECD, https://www.oecd.org/dac/financing-sustainable-development/development-finance-standards/ (accessed on 21 June 2022).

[9] Our World in Data (2022), Coronavirus (COVID-19) Vaccinations - Our World in Data, https://ourworldindata.org/covid-vaccinations (accessed on 10 May 2022).

[88] Pazarbasioglu, C. and U. Ramakrishnan (2021), Sharing the Recovery: SDR Channeling and a New Trust – IMF Blog, https://blogs.imf.org/2021/10/08/sharing-the-recovery-sdr-channeling-and-a-new-trust/ (accessed on 20 May 2022).

[54] Reuters (2022), Zelenskiy says Ukraine needs $7 billion per month to make up for losses caused by invasion | Reuters, https://www.reuters.com/world/zelenskiy-says-ukraine-needs-7-bln-per-month-make-up-losses-caused-by-invasion-2022-04-21/ (accessed on 24 May 2022).

[47] Schwerhoff, G. and M. Sy (2020), “Where the sun shines”, https://www.imf.org/external/pubs/ft/fandd/2020/03/pdf/powering-Africa-with-solar-energy-sy.pdf (accessed on 1 June 2022).

[50] SE4All (2019), Energizing Finance: Understanding the Landscape 2019 | Sustainable Energy for All, https://www.seforall.org/publications/energizing-finance-understanding-the-landscape-2019 (accessed on 15 June 2022).

[78] The Government of the Netherlands (2022), Voorjaarsnota 2022 | Kamerstuk | Rijksoverheid.nl (tabel 74), https://www.rijksoverheid.nl/documenten/kamerstukken/2022/05/20/voorjaarsnota-2022 (accessed on 21 June 2022).

[10] The White House (2022), 2nd Global COVID-19 Summit Commitments, https://www.whitehouse.gov/briefing-room/statements-releases/2022/05/12/2nd-global-covid-19-summit-commitments/ (accessed on 20 May 2022).

[28] The White House (2021), President Biden Announces American Rescue Plan | The White House, https://www.whitehouse.gov/briefing-room/legislation/2021/01/20/president-biden-announces-american-rescue-plan/ (accessed on 17 June 2022).

[55] U.S. Department of State (2022), $700 Million Drawdown of New U.S. Military Assistance for Ukraine - United States Department of State, https://www.state.gov/700-million-drawdown-of-new-u-s-military-assistance-for-ukraine/ (accessed on 8 June 2022).

[94] U.S. Department of State (2022), Welcoming Saudi Arabia and the UAE’s Economic and Humanitarian Support for Yemen - United States Department of State, https://www.state.gov/welcoming-saudi-arabia-and-the-uaes-economic-and-humanitarian-support-for-yemen/ (accessed on 24 June 2022).

[51] UKCOP26 (2021), Climate finance delivery plan: Meeting the US$100 billion goal, https://ukcop26.org/wp-content/uploads/2021/10/Climate-Finance-Delivery-Plan-1.pdf (accessed on 17 June 2022).

[66] UN (2022), “Afghanistan: UN launches largest single country aid appeal ever | | UN News”, https://news.un.org/en/story/2022/01/1109492 (accessed on 8 June 2022).

[22] UN (2021), Global Humanitarian Response Plan COVID-19: Final Progress Report, UN OCHA, Geneva, https://reliefweb.int/report/world/global-humanitarian-response-plan-covid-19-progress-report-final-progress-report-22 (accessed on 20 May 2022).

[21] UN (2020), Global Humanitarian Response Plan COVID-19: July Update, UN OCHA, Geneva, https://reliefweb.int/report/world/global-humanitarian-response-plan-covid-19-april-december-2020-ghrp-july-update-enar (accessed on 20 May 2022).

[20] UN (2020), Global Humanitarian Response Plan COVID-19: United Nations Coordinated Appeal, UN OCHA, Geneva, https://www.humanitarianresponse.info/sites/www.humanitarianresponse.info/files/documents/files/global_humanitarian_response_plan_covid-19_.pdf (accessed on 20 May 2022).

[64] UN News (2022), Demand for lifesaving aid up 10 per cent this year: UN relief chief | | UN News, https://news.un.org/en/story/2022/05/1118632?mkt_tok=Njg1LUtCTC03NjUAAAGEgBtUmmzuyVh9HT-UNGgvno6a0Qss1BuYsbB0u4GmER4VdWM4WllCxq-DNUkMnvXiCQ3Kho4xUnmZySB2PhbqZMUj2dC38dcn-xP8f_48F8_mHw (accessed on 20 May 2022).

[69] UNHCR (2022), Situation Ukraine Refugee Situation, https://data2.unhcr.org/en/situations/ukraine (accessed on 20 May 2022).

[76] UNHCR (2022), UNHCR - Refugee Statistics, https://www.unhcr.org/refugee-statistics/download/?url=4J8Lbv (accessed on 27 May 2022).

[12] UNICEF (2022), “COVID-19 Vaccine Market Dashboard (webpage)”, https://www.unicef.org/supply/covid-19-vaccine-market-dashboard (accessed on 14 January 2021).

[67] UNOCHA (2022), Appeals and response plans 2022 | Financial Tracking Service, https://fts.unocha.org/appeals/overview/2022 (accessed on 8 June 2022).

[39] WFP (2022), Projected increase in acute food insecurity due to war in Ukraine Summary, http://www.amis-outlook.org/indicators/prices/en/ (accessed on 29 June 2022).

[33] WFP (2022), Unprecedented needs threaten a hunger catastrophe, https://docs.wfp.org/api/documents/WFP-0000138231/download/?_ga=2.13933044.259238525.1653383149-2080868853.1643364883.

[68] WFP (2022), “WFP at a glance”, World Food Programme, https://www.wfp.org/stories/wfp-glance (accessed on 2 June 2022).

[18] WHO (2022), “11 January 2022”, Weekly operational update on COVID-19, https://www.who.int/publications/m/item/weekly-operational-updates-on-covid-19---11-january-2022 (accessed on 20 May 2022).

[7] WHO (2022), 14.9 million excess deaths associated with the COVID-19 pandemic in 2020 and 2021, https://www.who.int/news/item/05-05-2022-14.9-million-excess-deaths-were-associated-with-the-covid-19-pandemic-in-2020-and-2021 (accessed on 10 May 2022).

[11] WHO (2022), Access to COVID-19 tools funding commitment tracker, https://www.who.int/publications/m/item/access-to-covid-19-tools-tracker (accessed on 10 May 2022).

[19] WHO (2022), “COVID-19 Response Fund”, Coronavirus disease (COVID-19), https://www.who.int/emergencies/diseases/novel-coronavirus-2019/donors-and-partners/funding (accessed on 20 May 2022).

[17] WHO (2021), “13 February 2021”, Weekly operational update on COVID-19, https://www.who.int/publications/m/item/weekly-operational-update-on-covid-19---13-february-2021 (accessed on 20 May 2022).

[8] WHO (2021), Achieving 70% COVID-19 Immunization Coverage by Mid-2022, https://www.who.int/news/item/23-12-2021-achieving-70-covid-19-immunization-coverage-by-mid-2022.

[15] WHO (2020), “2019 Novel Coronavirus (2019‑nCoV): Strategic Preparedness and Response Plan (Draft as of 3 February 2020)”, ReliefWeb, https://reliefweb.int/report/world/2019-novel-coronavirus-2019-ncov-strategic-preparedness-and-response-plan-draft-3 (accessed on 20 May 2022).

[16] WHO (2020), COVID-19 WHO appeal, https://www.who.int/publications/m/item/covid-19-who-appeal (accessed on 20 May 2022).

[89] World Bank (2022), Are we ready for the coming spate of debt crises?, https://blogs.worldbank.org/voices/are-we-ready-coming-spate-debt-crises (accessed on 15 June 2022).

[44] World Bank (2022), Commodity Markets Outlook: The Impact of the War in Ukraine on Commodity Markets, April 2022, https://openknowledge.worldbank.org/bitstream/handle/10986/37223/CMO-April-2022.pdf.

[36] World Bank (2022), Pandemic, prices, and poverty, https://blogs.worldbank.org/opendata/pandemic-prices-and-poverty (accessed on 24 May 2022).

[45] World Bank (2022), Report: COVID-19 Slows Progress Towards Universal Energy Access, https://www.worldbank.org/en/news/press-release/2022/06/01/report-covid-19-slows-progress-towards-universal-energy-access (accessed on 2 June 2022).

[61] World Bank (2022), Russian Invasion to Shrink Ukraine Economy by 45 Percent This Year, https://www.worldbank.org/en/news/press-release/2022/04/10/russian-invasion-to-shrink-ukraine-economy-by-45-percent-this-year (accessed on 10 June 2022).

[56] World Bank (2022), World Bank Announces Additional $1.49 Billion Financing Support for Ukraine, https://www.worldbank.org/en/news/press-release/2022/06/07/-world-bank-announces-additional-1-49-billion-financing-support-for-ukraine (accessed on 17 June 2022).

← 1. Donations of excess vaccine doses are considered in-kind aid and thus count as ODA, according to reporting rules.

← 2. Figures for 2021 COVID-19-related activities are preliminary and incomplete as donors are still collecting information, especially sector-specific data.

← 3. For more information on vaccines pricing, see (Development Assistance Committee (DAC) Working Party on Development Finance Statistics, 2022[90]). The figure is a weighted average price aligned with COVAX, the multilateral mechanism for providing developing countries with vaccines.

← 4. For further information on fragile and conflict-affected contexts, see (OECD, n.d.[91]).

← 5. This data will become available in December 2022.

← 6. In constant 2021 prices.

← 7. Food price increase in 2022 calculated from the FAO Food Price Index, https://www.fao.org/worldfoodsituation/foodpricesindex/en/

← 8. Both countries are DAC observers. Individual Development Co-operation Report profiles can be accessed for Saudi Arabia (OECD, 2022[92]) and the UAE (OECD, 2022[93]).

← 9. Recent funding announcements for Yemen by Saudi Arabia and the UAE (U.S. Department of State, 2022[94]) could contribute to ODA levels in 2022.

← 10. Calculation based on numbers of Ukrainian refugees recorded in DAC countries on 14 June 2022. Anticipated cost uses the Kiel Institute’s baseline cost of EUR 500 per refugee per month, extrapolated for 10 months (March-December 2022), using a conversion rate of EUR1 = USD 1.0624. DAC countries’ ODA excludes ODA from EU Institutions.