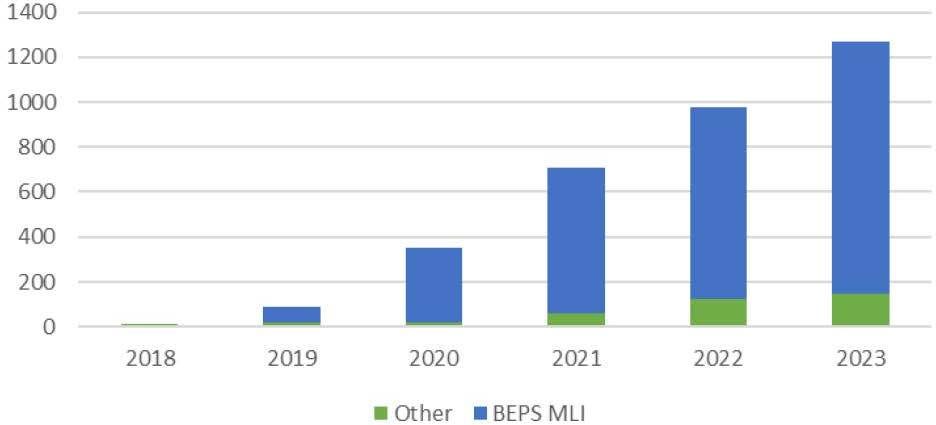

19. This section sets out the aggregate data on the implementation of the minimum standard on treaty shopping included in the Report on Action 6 (OECD, 2015[1]).

To comply with the minimum standard, jurisdictions are required to do two things in their tax agreements: include an express statement on double non-taxation (generally in the preamble) and adopt one of three measures to address treaty shopping. The minimum standard does not specify how these two things should be implemented (e.g. through the BEPS MLI or bilaterally) (OECD, 2015[1]).1

20. Aggregate data on the jurisdictions’ progress towards implementing the minimum standard is provided below. Detailed information on each jurisdiction’s progress is provided in the jurisdictional sections in Chapter 8. The information that can be found in the “Conclusion” section in some of the jurisdictional sections in Chapter 8 further highlights the following:

Members of the Inclusive Framework that have signed but not ratified the BEPS MLI are recommended to complete the steps to have the BEPS MLI take effect as soon as possible (Section 5 below);

Similarly, some of the parties to the BEPS MLI that have made a reservation under the BEPS MLI to delay its entry into effect until the completion of internal procedures are recommended to complete the steps to have the BEPS MLI take effect as soon as possible (Chapter 4 below).2

An implementation plan must be developed for agreements concluded with other members of the Inclusive Framework that are not compliant, not subject to a complying instrument or to a general statement on the detailed LOB, for which no steps have been taken to implement the minimum standard and no reasons have been given on why, for a jurisdiction, the agreement does not give rise to material treaty shopping concerns. Once a plan is in place, a jurisdiction must provide an annual update if changes occur. Where no implementation plan has been developed in respect of such agreements, jurisdictions are recommended to develop a plan for the implementation of the minimum standard (Chapters 3 and 4 below).

The OECD Secretariat stands ready to discuss with any jurisdiction that has developed, or that needs to develop, a plan for the implementation of the minimum standard to see how support could best be provided to bring the concerned agreements into compliance with the minimum standard.