This chapter describes market developments and medium-term projections for world cotton markets for the period 2023-32. Projections cover consumption, production, trade and prices developments for cotton. The chapter concludes with a discussion of key risks and uncertainties which could have implications for world cotton markets over the next decade.

OECD-FAO Agricultural Outlook 2023-2032

OECD-FAO Agricultural Outlook

Abstract

Steady growth in the next decade

Over the next decade, world consumption of raw cotton is foreseen to grow 1.8% p.a. on account of population and income growth in middle- and low-income countries. Raw cotton consumption will continue to depend on developments of demand in the textiles and apparels sectors and on competition from substitutes. It is expected that Asian countries such as Bangladesh and Viet Nam will lead the growth in consumption of lint cotton.

The distribution of lint cotton use across the globe depends on the location of cotton mills, which are often located in proximity to clothing and apparel industries. Over the past decades, there has been a marked build-up of cotton milling capacity in Asia, and this trend is expected to persist during the next decade. Chinese consumption peaked in 2007, but has been declining since, as stricter labour and environmental regulations and rising labour costs have pushed the industry to other Asian countries, notably Viet Nam and Bangladesh. These countries have experienced strong growth of their textile industries in the past years and a further increase in their milling capacity is expected over the next decade, bolstered by large foreign investments. By contrast, Chinese mill consumption has remained constant since 2016 and the Outlook assumes stable consumption for the coming decade. In India, another major cotton consumer, the foreseen increase for textiles products is expected to result in continuous growth in cotton mill use.

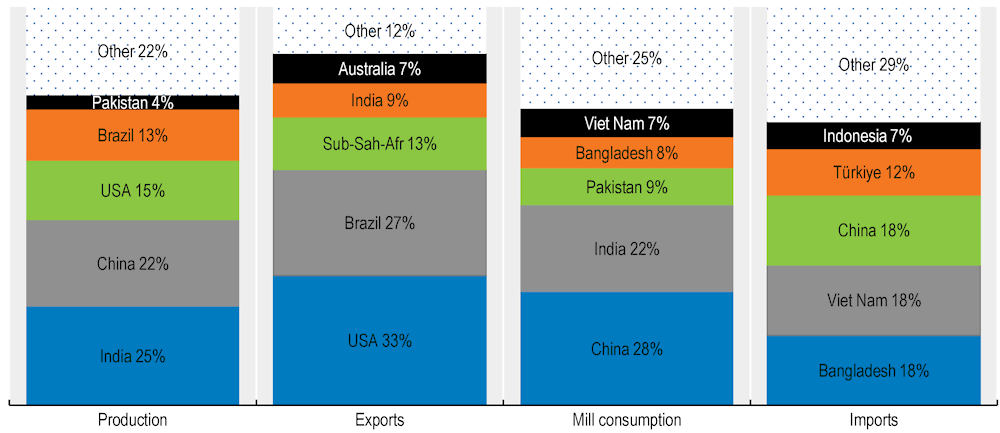

Over the next decade, global lint cotton production is projected to grow 1.81% p.a. to reach 28.1 Mt in 2032.This increase will be mostly dominated by higher yields (1.4% p.a.) and to a lesser extent on the expansion of area harvested (0.4% p.a.). Yield growth is expected to be driven by improvements in genetics, better agricultural practices, new technologies, and digitalization supporting precision agriculture. These elements will significantly contribute to enhance productivity. Additionally, marginal increases in area harvested in the United States and Brazil will also contribute to enlarge cotton production. Overall, India and the People’s Republic of China (hereafter “China”) will continue to lead world cotton production, accounting for nearly 46% of the global output in 2032.

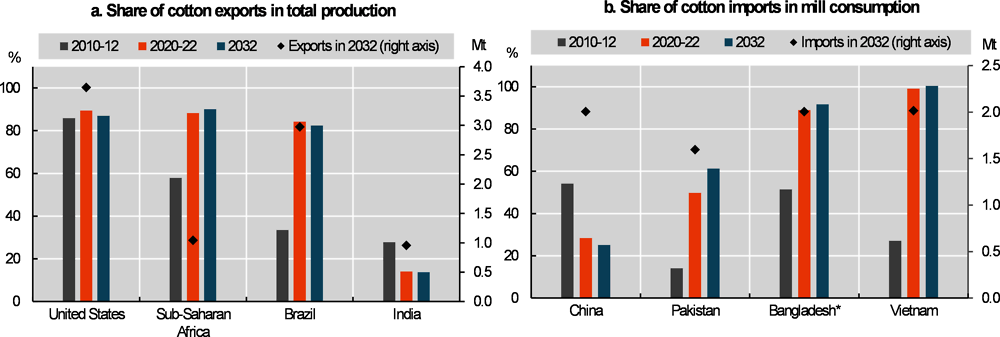

Raw cotton, or lint, is internationally shipped in the form of large bales (about 225 kg) of highly compressed fibres, easing transportation. The Outlook foresees growth in global trade of lint of 15.8% compared to the base period, surpassing 11.9 Mt by 2032. Additionally, world trade is expected to grow at a slightly higher pace than overall consumption, considering that countries with a strong textile industry such as Bangladesh and Viet Nam rely heavily on raw material imports. The growing gap will be filled mainly by top producing countries, such as Brazil and the United States, where the lint industry is primarily export oriented. Overall, it is expected that the structure of the global cotton market will not change significantly in the coming decade, with Sub-Saharan Africa as a region remaining the third largest exporter of raw cotton in 2032, after United States and Brazil (Figure 10.1).

International cotton prices, in real terms, are foreseen to trend slightly downward in the medium term. Productivity enhancement, as well as expected low prices of synthetic fibres will likewise impact cotton prices and exert downward pressure.

Key uncertainties on the demand side can potentially impact outcomes. First, developments of the global economy might influence consumption of textile and apparel products, thus affecting the demand for cotton. Second, the stronger than expected competition from man-made fibres, notably polyester, can negatively affect demand for cotton. Third, the growing concerns by governments and consumers over the environmental impacts of the textile and clothing industry can result in tighter regulations and standards affecting cotton demand.

Note: Presented numbers refer to shares in world totals of the respective variable.

Source: OECD/FAO (2023), ''OECD-FAO Agricultural Outlook'' OECD Agriculture statistics (database), http://dx.doi.org/10.1787/agr-outl-data-en.

On the supply side, the main source of uncertainty is natural risks, including climate change and pest infestations. Policy also plays an important role in cotton markets. For example, changes in stockholding measures, input subsidies and market access can alter the performance of the sector.

Increases in yields and areas are contributing to steady production growth

Global raw cotton consumption is set to decline to its lowest level in ten years in the 2022/23 season (August/July). Major declines in lint demand are anticipated to be witnessed by some of the leading cotton consumers such as India and Pakistan. The expected drop in consumption reflects the global economic uncertainty and inflation surge, which is seen to decelerate global demand for cotton-related products. Furthermore, the US dollar appreciation against Asian currencies has exacerbated the drop in lint demand, considering that main raw-cotton consumers are highly dependent on imports.

International cotton prices experienced important fluctuations in the 2022/23 season. The global economic rebound along with the upsurge of textiles demand from the previous season kept prices high until May 2022, when prices reached an eleven-year high. As a consequence of a slowing global demand for cotton from June 2022, cotton prices dropped significantly. Despite the decline, prices in 2022 averaged 38% above their year-earlier levels, prompting an increase in planted area in India and Brazil.

Global cotton production slightly decreased in 2022 as a result of extreme weather conditions. In the United States, early season drought in Texas prompted a contraction of nearly 16% of lint production, whereas in Pakistan, late season flooding plunged local production to the lowest level in nearly 40 years. However, increases of cotton production in China and India, the world's foremost producers, did not offset the global shortfall.

World trade of raw cotton is foreseen to decrease compared to the previous season. On the supply side, exports are expected to be significantly lower due to the underperforming season in the United States, the worlds’ larger exporter. On the demand side, weaker global textile consumption significantly reduced lint imports in Viet Nam, Bangladesh, and Türkiye. Furthermore, in Pakistan, a sharp depreciation of local currency against the US dollar has shrunk imports, while China’s trade remained stable compared to the 2021/22 season.

10.3.1. Consumption

Viet Nam and Bangladesh displacing China in leading growth in consumption

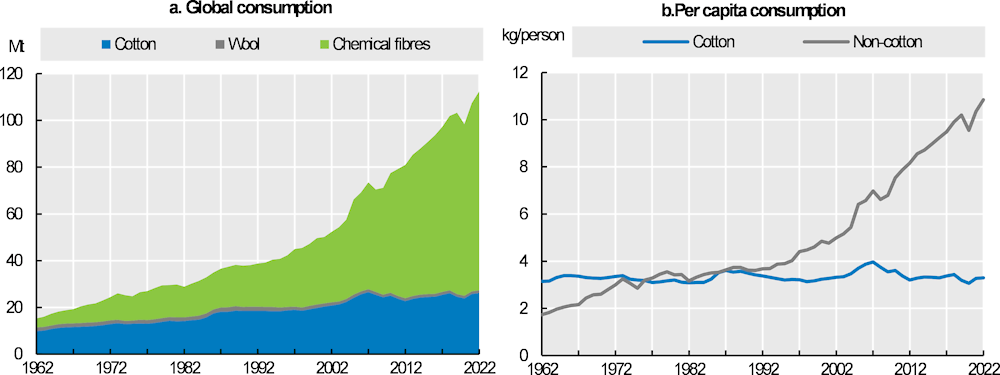

Cotton consumption refers to the use of cotton fibres by mills to transform it into yarn. Cotton mill-use depends largely on two major factors: global textile demand and competition from synthetic fibres. Over the past decades, global demand for textiles fibres has sharply increased, driven mainly by population and income growth, particularly in low- and middle-income countries. This expanding demand has been largely supplied by chemical fibres (Figure 10.2, panel a). The diverse advantages of synthetics compared to cotton including durability, wrinkle resistance, moisture-wicking, and/or competitive prices have boosted textile manufacture industry to favour synthetic over cotton fibres. As a result, global consumption of natural fibres peaked in 2007 at 26,5 Mt and shrank to around 24,4 Mt in 2020-22.

From the early 1990’s, non-cotton fibres have gained solid ground in the textile industry. In 2022, the end-use market-share reached 76.7% for chemical fibres and only 23.3% for cotton. Likewise, per capita consumption of non-cotton fibres has strongly outpaced per capita consumption of cotton fibres and continues to strongly increase. In contrast, per capita consumption of cotton has remained stagnant over time and trended downwards in recent years (Figure 10.2, panel b)

Source: ICAC World Textile Demand estimates, 2023.

The prospects for global cotton use relies mainly on its evolution in developing and emerging economies. Demand from these regions with lower absolute levels of consumption but higher income responsiveness is projected to exert upward pressure on global demand for cotton as the incomes and population of these countries are projected to increase. As a result, the Outlook expects global growth consumption of cotton products to slightly overtake growth of global population in the coming decade. Correspondingly, global mill use is projected to grow by around 1.8% p.a. over the next decade.

The geographical distribution of demand for cotton fibres depends on the location of spinning mills, where natural and synthetic fibres are transformed into yarn. Traditionally, the spun yarn industry has been established predominantly in Asian countries, where conditions such as lower labour costs are favourable for the industry. China has been the world’s leading cotton consumer since 1960. However, major changes in the geography of cotton production in China have reshaped global cotton markets in the last decade. With 90% of Chinese cotton currently produced in the region of Xianjiang and a tariff-rate quota binding mill-cotton imports, yarn production has gradually shifted to other Asian countries.

China’s cotton mill consumption has been decreasing since the support price system was abolished in 2014. The artificially higher prices had caused a shift in demand from cotton to synthetic fibres. Likewise, the decline in cotton demand also reflects the structural change that took place as a result of higher labour costs and more stringent labour and environmental regulations. This provoked a move to other Asian countries, notably Viet Nam and Bangladesh. In recent years, mill consumption has regained some lost ground in China, in part because domestic cotton prices have become more competitive when compared to polyester, which appears to have suffered a setback due to government measures to combat industrial pollution. Chinese spinning mill use should remain stable over the next decade if margins are remunerative at the mills.

In India, the growing textile industry coupled with competitive labour costs, and government support to the sector are expected to result in continuous growth in cotton mill use. Cotton plays an important role in the Indian economy as the country's textile industry is predominantly cotton based. The textile industry, however, faces several challenges, including technological obsolescence, high input costs, and poor access to credit. The government is promoting investments in the sector and has launched several schemes over the past few years for the promotion of the textile industry and improving the livelihood of the people involved.

The phase-out in 2005 of the Multi-Fibre Arrangement (which had fixed bilateral quotas for developing country imports into Europe and the United States) was expected to favour Chinese textile producers at the cost of smaller Asian countries. In practice, countries such as Bangladesh, Viet Nam, and Indonesia experienced strong growth of their textile industry based on an abundant labour force, low production costs, and government support measures. In addition, the escalation of the United States-China trade dispute has spurred additional mill use in Bangladesh and Viet Nam. In the case of Viet Nam, this was partly driven by its accession to the World Trade Organization in 2007 and by foreign direct investment (FDI), notably by Chinese entrepreneurs.

Structural changes in cotton production in China along with the surge of more robust textiles industries in Viet Nam, Bangladesh, and other central Asia economies, have boosted mill consumption growth in recent years and is foreseen to keep expanding over the coming decade. Viet Nam will take the lead in annual growth of mill use. The ratification of the Free Trade Agreement (FTA) with the European Union in mid-2020 is expected to contribute to this growth. In Bangladesh and Indonesia, growing demand for yarn and fabric from the domestic garment and textile industries is prompting investments in new spinning facilities or in enhancing production capacity of existing mills. Hence, cotton fibres consumption is expected to rise 3,4% p.a. and 3,2% p.a. accordingly.

10.3.2. Production

Improvements in yields drive growth, but sustainable production remains the main concern

Cotton is grown in subtropical and seasonally dry tropical areas in both the northern and southern hemispheres, although most of the world’s production takes place north of the equator. The leading producing countries are India, China, the United States, Brazil, and Pakistan. Jointly, these countries account for around 78% of global output in 2032 (Figure 10.1).

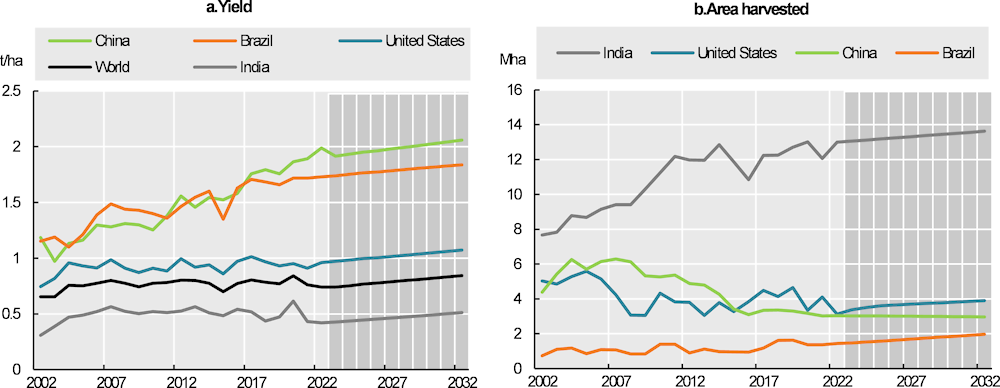

Global production of cotton is expected to grow steadily and reach 28.-15 Mt by 2032, 12% higher than in the base period (Figure 10.4). The foreseen increase will mostly come from growth in the main cotton producers: United States will account for about 29% of the global increase, followed by India (25%), and China (7%). Overall, gains in cotton production are predominantly driven by higher yields, and to a lesser extent, on expansion in area harvested.

Average global yields are projected to increase by 8% compared to the base period. Factors such as improvements in genetics, better agricultural practices, and digitalization supporting precision agriculture will significantly contribute to enhance productivity and sustainability. Over the past two decades, global average yields have been stagnant, suggesting static or decreasing yields in some of the major producers. For instance, in 2022, yields in China and Brazil were double the world average yields while India, the main cotton producer, remained well below (around 0.5 times global average yields). These differences are estimated to slightly broaden over the outlook period. (Figure 10.5, panel a). Cotton area is projected to expand by 4% compared to the base period.

Source: OECD/FAO (2023), ''OECD-FAO Agricultural Outlook'' OECD Agriculture statistics (database), http://dx.doi.org/10.1787/agr-outl-data-en.

Production in India is estimated to grow by around 2.5% p.a. over the next decade, mainly on account of yield improvements rather than area expansion, since cotton already competes for acreage with other crops, such as soybeans and pulses. Raw cotton productivity has remained stagnant in recent years and is among the lowest globally. Cotton producers struggle with several obstacles such as adverse weather, pests, and diseases. Moreover, cotton is traditionally grown on small farms, which limits the adoption of intensive farming technologies. However, growing demand from the domestic apparel industry continues to spur investments in the sector and the Outlook assumes a growth in yields that reflects increased use of smart mechanisation, varietal development, and pest management practices. Nonetheless, climate change, with most cotton grown under rain-fed conditions, may undermine the yield growth potential.

Chinese cotton is currently produced with the highest global yield (1.90 t/ha average in 2020-22), which are more than double of the world’s average. Over the past two decades, the cotton area in China has been declining, mostly due to changing government policies. Nevertheless, this trend seems to have slowed down since 2016. It is expected that the cotton area will decrease by 0.4% p.a. during the outlook period.

In Brazil, cotton is grown in part as a second crop in rotation with soybeans or maize. Recently, output has strongly grown in the main cultivation areas such as Mato Grosso, where 70% of Brazilian cotton is currently harvested. Cotton output is foreseen to increase by 3.9% p.a. Production gains are mostly coming from higher yields and the use of genetically engineered (GE) seeds and fertilisers. Recent investments in cotton-growing capacity and the acquisition of new equipment (planters, pickers, and ginning capacity) are expected to boost production in the coming years. Due to strong competition with other crops, mainly soybeans, the planted area depends widely on the profitability of cotton compared to other commodities.

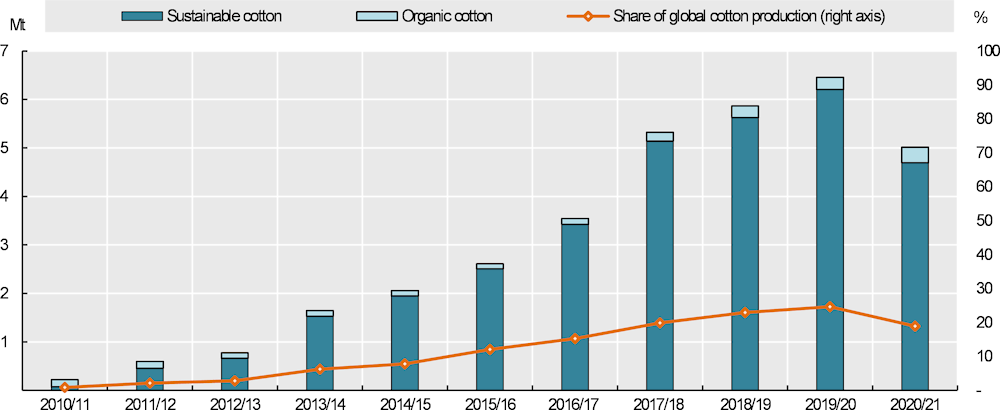

Sustainability issues play an important role and will impact cotton markets in the medium term. In a context of growing concerns over the effects of climate change and socio-environmental considerations, new initiatives have been introduced to promote sustainability along the supply chain. Among the existing standards, Better Cotton dominates globally. In 2021, the combined cotton output from worldwide partners reached 20% of sustainable cotton with respect to global cotton production (Figure 10.6). Alternative strategies1 promote better agricultural practices to mitigate climate change and provides guidance to textile brands and retailers to source their cotton inputs from recognized and certified sustainable producers. It is expected that demand for more sustainable cotton continues to rise, driven by commitments from brands and awareness among young populations. Therefore, growing trends towards consumption of more sustainable cotton products will likely boost cotton production in countries such as Brazil, where around 84% of total cotton output already complies with the sustainable standards. It is expected that Sub-Saharan Region also benefits, as programmes such as Cotton Made in Africa (CMIA) accounts for 13% of global sustainable output.

Source: Author's calculations based on Organic cotton market report 2022 and better cotton annual report 2021.

10.3.3. Trade

World cotton market relies strongly on trade, with Bangladesh and Viet Nam mill consumption depending on imports

World cotton trade is projected to expand steadily over the next decade and reach 11.2 Mt in 2032, 16% higher than in the base period. The increase mainly reflects the substantial growth in mill use in Asian countries, particularly Viet Nam and Bangladesh, which source virtually all their cotton from imports to support their growing domestic textiles sector. By 2032, imports in China are projected to decrease by 7% reaching 2.0 Mt. Shifts in the location of the planting area that took place in the last decade have reshaped the Chinese cotton market. Due to the physical distances between the spinning and the cotton fields along with imposed tariff-rate quota on imports, the Chinese textile industry has substituted raw-cotton imports by yarn imports and from 2012-21, the latter increased at 21,7% p.a. As a result, lint demand has been absorbed by other Asian economies (Figure 10.7, panel b).

The United States will remain the world’s largest exporter throughout the outlook period. Exports from the United States exports have stabilised in recent years, recovering from the lows in 2016. It is projected that its share of world trade will reach 33% in 2032 (around 3.6 Mt). Despite the major changes in the Chinese textile industry, the United States remains its main trade partner. It is foreseen that in the medium-term export volumes to China will fall, while slightly gaining ground across other Asian economies.

Brazilian exports are expected to grow strongly over the next decade, consolidating the country’s position as the second largest exporter by 2032, followed by Sub-Saharan Africa (Figure 10.7, panel a). In Sub-Saharan Africa, cotton is an essential export crop, accounting for around 13% of global exports. Overall, cotton production in the region has increased in the past several years due to area expansion and improvements in yields. The region will remain subject to pests and disease that adversely affect cotton harvests.

Note: * Includes mill consumption and imports from other countries such as Cambodia, Myanmar, Bhutan and Nepal.

Source: OECD/FAO (2023), ''OECD-FAO Agricultural Outlook'', OECD Agriculture statistics (database), http://dx.doi.org/10.1787/agr-outl-data-en.

Sub-Saharan African exports are projected to continue growing at around 1.9% p.a. in the coming decade, with South and Southeast Asia being the major export destinations. Moreover, the textile and apparel industry is expanding in countries such as Ethiopia, supported by favourable economic conditions, FDI flows, and government investments. In the long run, this could imply an increase in mill use and affect the net export status of Sub-Saharan Africa.

10.3.4. Prices

International cotton prices to decline in real terms over the medium-term

International cotton prices in real terms are foreseen to trend slightly downward in the medium term (Figure 10.8). Prices will continue to be influenced by competition from man-made fibres along with changes in consumers preferences.

From the early 1970s, when polyester became price-competitive, cotton prices tended to follow polyester prices. For example, cotton prices were only 5% above polyester staple fibre prices between 1972 and 2009. Since 2010, however, cotton prices have been on average almost 40% above the polyester price, in nominal terms. Over the past year, cotton prices increased at a faster pace than those of polyester, resulting in a wider price differential. However, it is assumed that the relative competitiveness between these two types of fibre will not change drastically over the projection period.

Policies and the role of genetics constitute major concerns

Economic growth and urbanisation will continue to be the main factors affecting the per capita demand for textiles in developing and emerging economies. Demand trends for textiles will significantly impact demand for cotton fibres. Since the consumption of textiles and apparel is more income responsive than the consumption of food commodities, deviations from the economic conditions assumed in the Outlook could lead to important changes in the global cotton consumption, production, and trade projections.

In the short term, projections are likely to be impacted by the increase in energy prices recorded in 2022. Additionally, current macroeconomic conditions are set to play an important role in short-term investment decisions, as current high inflation and increases in interest rates affect the cost of borrowing. Moreover, for Asian countries that are highly dependent on cotton imports, the appreciation of the US dollar against Asian currencies will also impact the cotton market in the near future.

Other demand trends affecting the projections include recycling by the textile industry that is creating a competitive secondary market providing raw material to producers of lower quality textiles and non-textile products. This trend, along with stronger than expected competition from man-made fibres, could negatively affect demand for cotton. Growing concerns by governments and consumers over the environmental impacts of the textile and clothing could also affect demand for cotton, However, on the other hand, greater adoption of sustainability standards in supply chains could provide a stimulus to the demand for cotton.

Like other crops, cotton production is sensitive to pests, disease, and climate change. The latter could lead to increasing frequency of droughts, floods, and other adverse weather conditions. As noted above, yield growth has been slow in several countries over the past two decades. Faster than expected improvements in genetics and gene editing (e.g. facilitated in part by a better understanding of the cotton genome) and better pest management have the potential to lead to higher yield growth than the projections in the Outlook. Such innovations, however, take time to develop and deploy, and in the case of genetically modified cotton are sometimes controversial. In Burkina Faso, the introduction of Bt cotton in 2008 was effective in combatting bollworms but resulted in a shorter staple length (and hence lower quality premiums). This prompted the government to phase out Bt cotton in 2015.

Policies also play an important role in global cotton markets. Policies, beyond what is assumed in the Outlook, such as support for domestic textile industries or input subsidies might affect the resulting projections. Trade policies and geopolitical tensions also impact the development of lint markets. For instance, the current US-China dispute and the United States’ Uyghur forced labour prevention act2 that went into effect in June 2022 have significant consequences and caused disruptions along the supply chain in China. Finally, issues associated with social, economic, and environmental sustainability (e.g. Product Environmental Footprint (PEF) and the Strategy for Sustainable circular textiles in the European Union) are becoming increasingly important for consumers, industry, and policy makers in many countries.

Policy measures that affect consumption include, for example, the decision by several East African countries to increasingly discourage second-hand clothing imports. This could bolster cotton consumption and encourage more added value in Africa. In West Africa, efforts from the government and the private sector are being made to increase cotton processing capacities across countries.

← 1. See https://bettercotton.org/who-we-are/our-aims-strategy/2030-strategy/ and https://textileexchange.org/2025-sustainable-cotton-challenge/.

← 2. The Uyghur Forced Labour Prevention Act forbids the import of goods produced in China’s Xianjiang region. The importer must clearly prove that the merchandise coming from this region was not produced with forced labour.