The future gross replacement rate represents the level of pension benefits in retirement from mandatory public and private pension schemes relative to earnings when working. For workers with average earnings and a full career from age 22, the future gross replacement rate at the normal retirement age averages 50.7% for men and 50.1% for women in OECD countries, with substantial cross-country variation. Future gross replacement rates from mandatory schemes are below 30% at the average wage in Australia, Estonia, Ireland and Lithuania while they are at 70% or more in Austria, Colombia, Denmark, Greece, Italy, Luxembourg, the Netherlands, Portugal, Spain and Türkiye.

Pensions at a Glance 2023

OECD and G20 Indicators

OECD Pensions at a Glance

Gross pension replacement rates

Key results

All of the replacement rates are calculated for full-career workers from the age of 22, which means that career lengths differ between countries. Denmark has an estimated long-term retirement age of 74 years for those starting in 2022, whilst in Colombia it will be 57 for women and 62 for men, and in both Luxembourg and Slovenia retirement will still be possible with a full pension at age 62 for both men and women (Table 4.1).

Full-career male workers will have a replacement rate of 50.7% on average across OECD countries, with a high of 80% or more in Greece and Spain and a low of under 30% in Australia, Estonia, Ireland and Lithuania. The average for women is slightly lower, at 50.1%. Gross pension replacement rates differ for women in eight countries, due to a lower future pension eligibility age than for men (Colombia, Hungary, Israel, Poland and Türkiye) and higher life expectancy when sex-specific mortality rates are used to compute annuities (Australia, Chile and Mexico). The replacement rates are expressed as percentage of earnings which are not gender specific. Women in Australia, Hungary and Israel will receive benefits around 7‑8% lower than for men with the biggest gap being found in Poland, with replacement rates for women being 22% lower than for men (i.e. 6.4 percentage points).

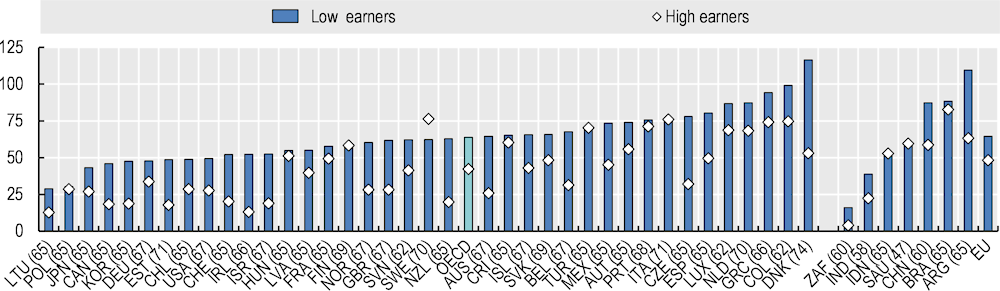

Most OECD countries aim to better protect low-income workers (here defined as workers earning half of average earnings), in particular to limit old-age poverty risks, which results in higher replacement rates for them than for average earners. Low-income workers would receive gross replacement rates averaging 63.8%. Some countries, such as Australia and Ireland, pay relatively small benefits to average earners, but are closer to or even above average across the OECD for low-income workers. Australia, Czechia and Denmark record the largest difference between gross replacement rates applying to low-wage and average‑wage workers, of at least 30 percentage points. However, projected replacement rates in six countries are basically the same for a full career at average and half-average pay: Austria, Finland, France, Italy, Spain, Sweden and Türkiye.

At the top of the range, based on current legislation, low earners in Denmark will receive a future gross replacement rate of 117% after a full career; retirement benefits are thus higher than their earnings when working. At the other end of the scale, Lithuania and Poland offer gross replacement rates of 30% or lower to low-income earners, thus implying a gross retirement income around 15% of average earnings after a full career.

On average, the gross replacement rate at twice average earnings (here called “high earnings”) is 42%. Replacement rates for these high earners equal 70% or more in Colombia, Greece, Italy, Portugal, Sweden and Türkiye, while at the other end of the spectrum, Canada, Estonia, Ireland, Israel, Korea, Lithuania and New Zealand offer a replacement rate below 20%.

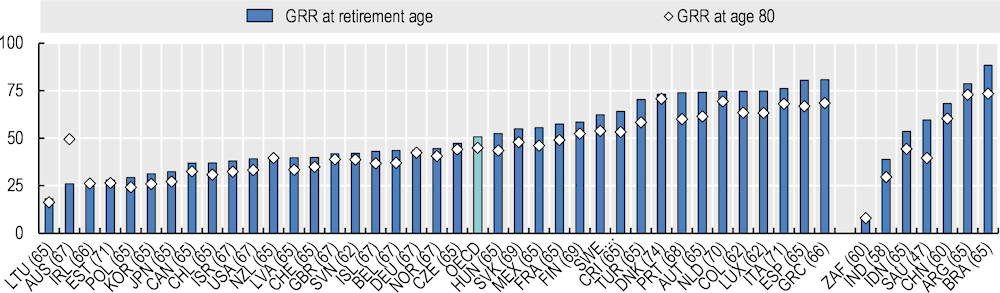

Gross pension replacement rates fall with age from 51% of the average wage at the time of retirement on average across countries to 45% of the projected average wage at age 80, a fall of 11% relative (Figure 4.1). Given projected real-wage growth, this difference is due to the indexation of pension benefits in payment, which do not follow wages in many countries. With price indexation from a normal retirement age of 65, the fall is equal to 17% based on the OECD model assumptions – as found in Austria, Costa Rica, Hungary, Korea, Mexico, Poland and Türkiye. The earlier the normal retirement age the larger the fall with price indexation. Countries where the indexation of pension benefits follows wages have the same replacement rate at age 80 than at the normal retirement age. Australia actually shows a large increase in the replacement rate at age 80 compared to normal retirement age, because the means-tested component is not available for average‑earner retirees at the retirement age as their FDC pension has a capital value over the ceiling, but as capital diminishes eligibility to the Age Pension increases.

Definition and measurement

The old-age pension replacement rate measures how effectively a pension system provides a retirement income to replace earnings, the main source of income before retirement. The gross replacement rate is shown as gross pension entitlement divided by gross pre‑retirement earnings. Under the baseline assumptions, workers earn the same percentage of average‑worker earnings throughout their career. Therefore, final earnings are equal to lifetime average earnings revalued in line with economy-wide earnings growth. Replacement rates expressed as a percentage of final earnings are thus identical to those expressed as a percentage of lifetime earnings.

Table 4.1. Gross pension replacement rates by earnings, in percentage, mandatory schemes

Note: *Low earners in Colombia, New Zealand and Slovenia are at 64%, 63% and 56% of average earnings, respectively, to account for the minimum wage level.

Source: OECD pension models.

Figure 4.1. Gross pension replacement rates in percentage: Average earners at retirement age and age 80

Source: OECD pension models.

Figure 4.2. Gross pension replacement rates in percentage: Low and high earners

Source: OECD pension models.