Residence‑based basic pensions exist in nine OECD countries and are, on average, worth 21% of the gross average wage. All OECD countries provide targeted benefits for their residents to ensure at least some income. On average in the OECD, people without a contributory record could receive 16% of gross average earnings from targeted schemes, subject to a means test, and 21% when including residence‑based basic pensions. For the nine OECD countries with contribution-based basic pensions the full benefit equals 15% of the gross average wage on average. Half of OECD countries provide a minimum pension benefit within their contributory scheme, with the full minimum contributory benefit level averaging 25% of average earnings for these countries.

Pensions at a Glance 2023

Basic, targeted and minimum contributory pensions

Key results

There are four main ways in which OECD countries might provide retirement incomes to meet a minimum standard of living in old age (Table 3.2). The left-hand columns of the table for each country show the value of benefits provided under these different types of schemes. Values are presented in relative terms – as a percentage of countries’ gross average wages – to facilitate comparisons between countries (see the “Average wage” indicator in Chapter 7). The right-hand columns show the number of total recipients as a share of the population aged 65 and over.

Benefit level

Benefit values are shown for a single person. In some cases – in particular for minimum contributory pensions – each partner in a couple can receive an individual entitlement. In other cases – especially for targeted schemes – the household is treated as the unit of assessment and generally receives less than twice the entitlement of a single person.

Most countries have multiple programmes within the first tier, which complicates the analysis of effective benefit levels. In some cases, benefits under these schemes are additive. In others, there is a degree of substitution between them. All OECD countries provide targeted benefits that are subject to means tests, but in Australia, Finland, Germany and the United States these are the only first-tier schemes in place. However, Germany recently introduced a new supplemental pension to the points scheme, which will provide additional contributory benefits to low earners with careers of at least 33 years.

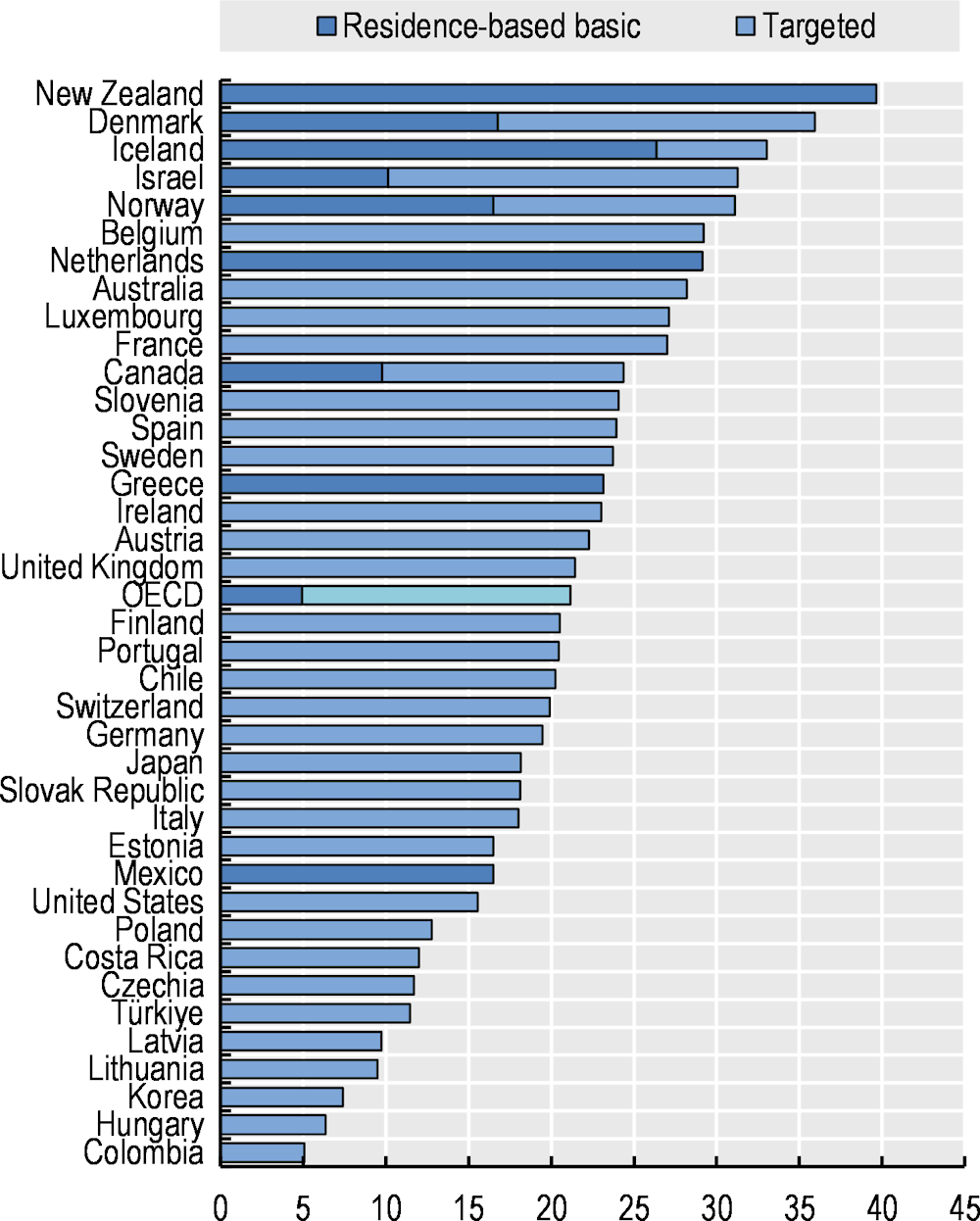

Figure 3.2 summarises the level of non-contributory residence‑based benefits. Residence‑based basic pensions are present in nine countries with an average benefit of 21% of the gross average wage and a maximum of 40% in New Zealand. Norway is phasing it out, with a full elimination in 2030. Those eligible to the residence‑based basic pensions in Greece, the Netherlands and New Zealand cannot receive targeted benefits on top. In Canada, Denmark and Iceland, residence‑based basic pensions do not reduce the targeted benefit. On average amongst all OECD countries, 16% of gross average earnings can be received from targeted schemes subject to means tests, but this increases to 21%, on average, if the residence‑based basic pensions, of the nine countries, are also included.

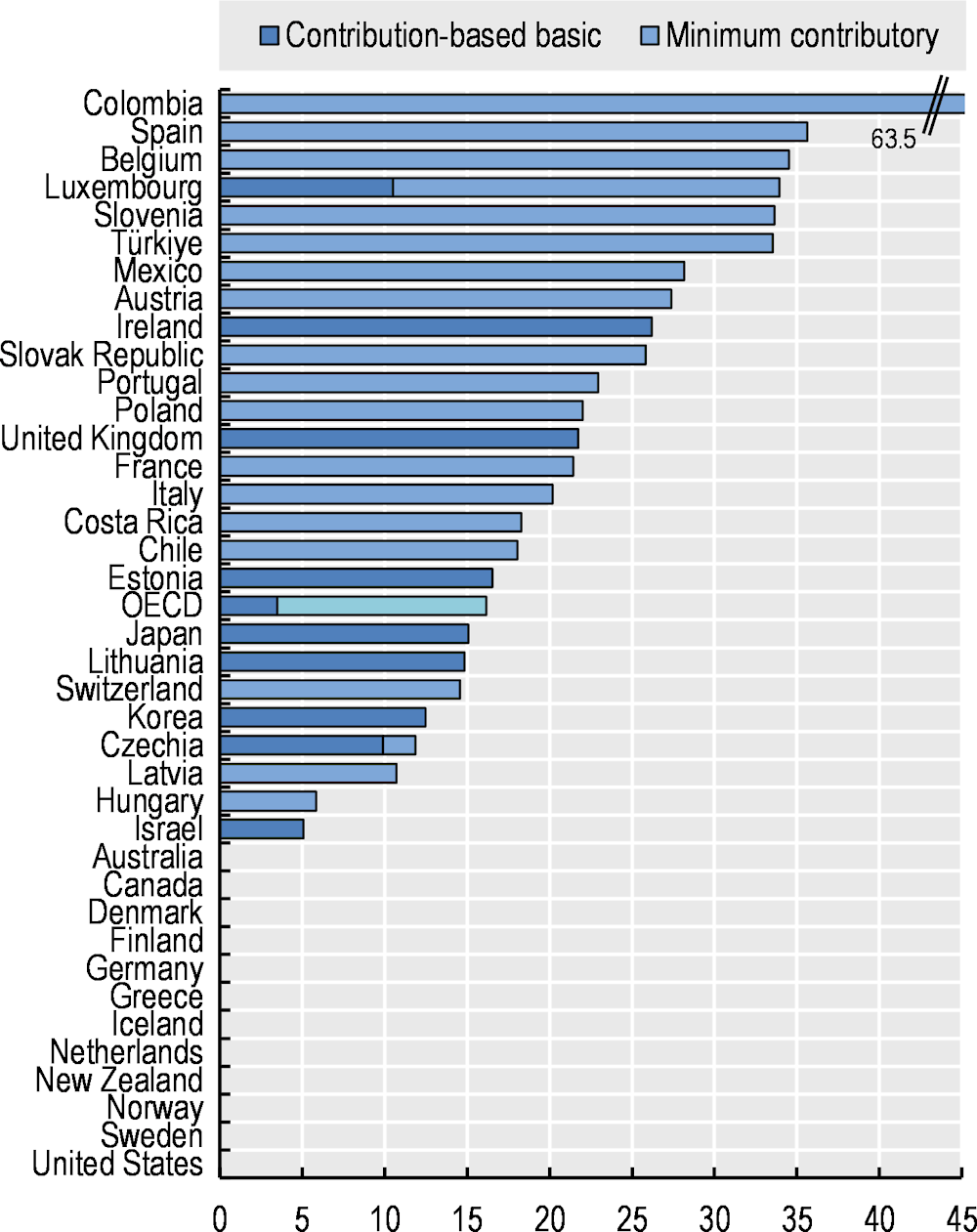

As for the contributory components of first-tier pensions, one‑third of OECD countries has neither contribution-based basic nor minimum contributory pensions (Figure 3.3). Nine OECD countries provide contribution-based basic pensions, which lie on average at 15% of average earnings for the full benefit for these nine countries, or 3% when averaged across all countries. They range from 5% of average earnings in Israel to 26% in Ireland. In half of OECD countries, low contributory pensions are topped up to a higher minimum pension level, up to 25% of average earnings, on average, among countries with minimum contributory pensions (13% across all 38 countries). These minimum pensions vary between a low of about 5% of the average wage in Hungary and 11‑12% in Czechia and Latvia to a high of about 35‑36% in Belgium and Spain and even 63% in Colombia where the minimum contributory pension is set at the minimum wage.

Coverage

The importance of first-tier benefits varies enormously across OECD countries. The percentage of over‑65s receiving such benefits is shown in the final four columns for each country in Table 3.2. Different approaches of reporting the number of recipients, for example in case of benefits paid to couples or even households, may blur the data comparability across countries to some extent.

Naturally, residence‑based basic pensions have on average the highest coverage. However, contribution-based basic pensions also have very high recipient numbers in most countries that have such a scheme. Sometimes recipient numbers exceed 100% of the population aged 65 and older hinting to recipients being younger than 65 or living abroad.

The incidence of receiving a minimum contributory pension is very diverse across countries, being received by 44% of the over‑65s in Portugal, 34% in France and 31% in Belgium while it is only around 5% in Poland and the Slovak Republic and 2% or under in Hungary and Slovenia.

The range in targeted schemes is similarly big, with in particular Australia, Chile, Denmark and Korea showing high recipient numbers of more than 50% for those aged 65 or older, but in many cases the value of benefit received may be quite small due to withdrawal rules.

Table 3.2. Current level and recipients of first-tier benefits

Note:. = Data are not available. The benefit level shown is for new pensioners in 2022. The contribution-based basic amounts refer to the benefit level for a full career. People in Greece, the Netherlands and New Zealand cannot receive a targeted benefit on top of a full residence‑based basic pension. Average wage can be found in Table 7.5, which may differ significantly from country estimates, thereby affecting the above percentages.

Source: Information provided by countries and OECD calculations.

Figure 3.2. Non-contributory first-tier benefits

Figure 3.3. Contributory first-tier benefits