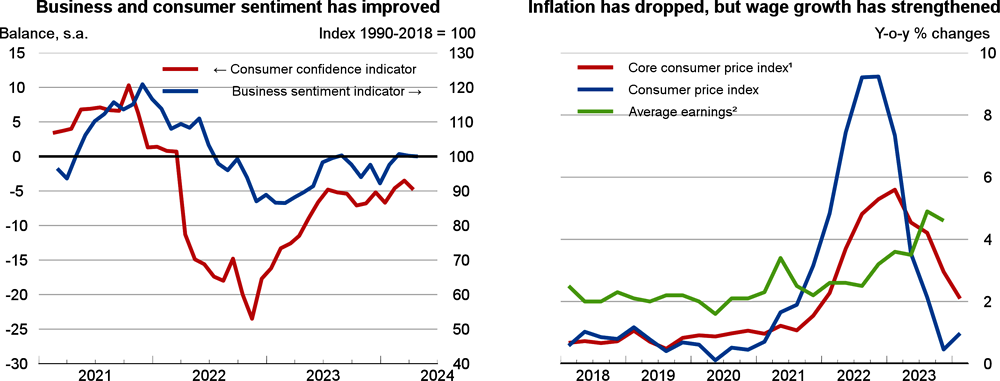

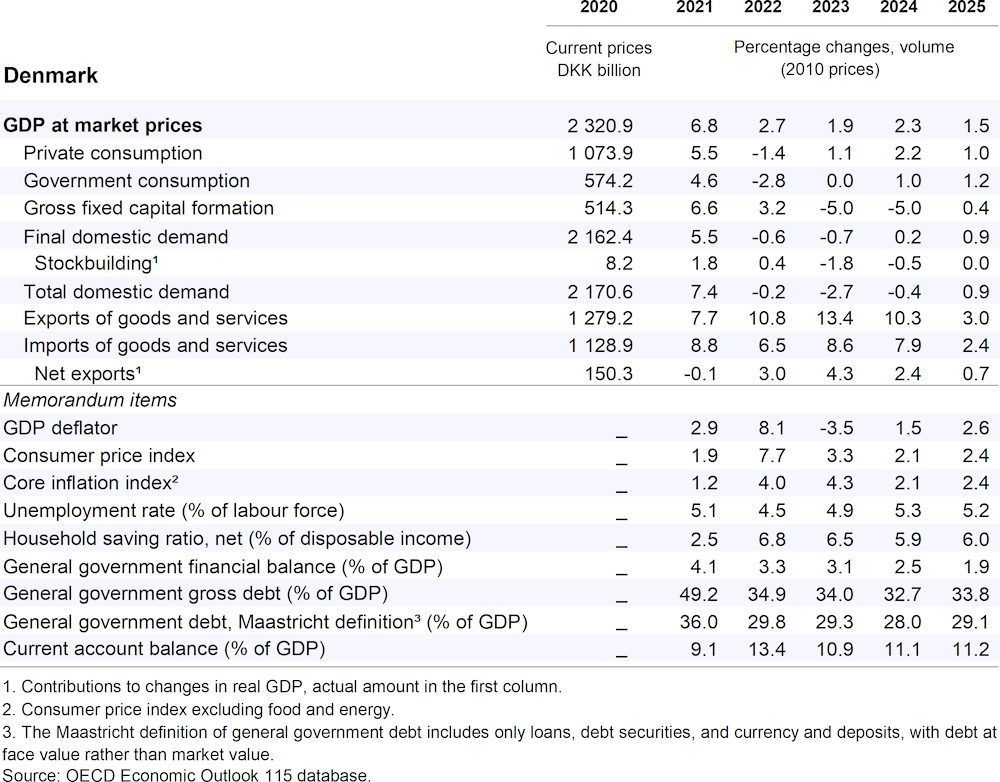

Economic growth is projected to remain robust at 2.3% in 2024 before slowing to 1.5% in 2025. Improving global trade will sustain non-pharmaceutical exports, while growth in the key pharmaceutical sector is set to moderate. Wage rises and ongoing disinflation will increase household purchasing power. Business investment will recover gradually as credit conditions improve and interest rates decrease. The main risks to the outlook relate to performance in the main exporting sectors and stronger than expected effects from rising labour costs on inflation and price competitiveness.

Policy rates are set to start easing in the latter half of 2024 in line with euro area monetary policy. The fiscal stance is mildly expansionary but appropriate given slow growth in the domestic economy. Addressing skills shortages can help mitigate labour market tightness and related inflationary pressures. Reforms are needed to remove financial barriers to work and facilitate international recruitment.