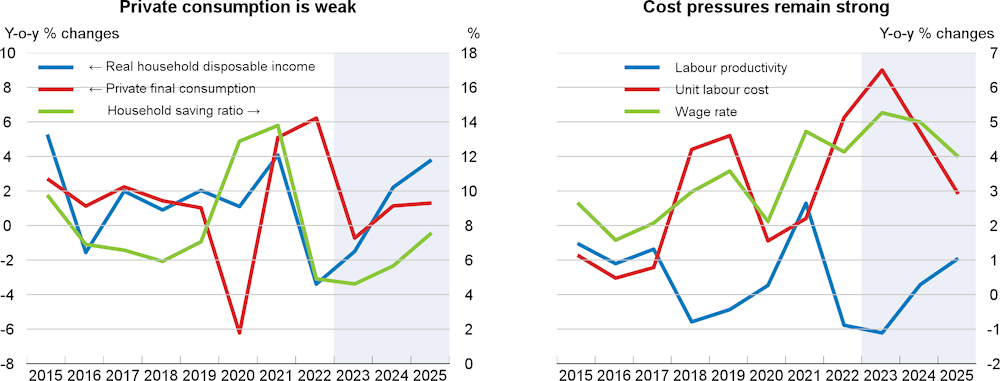

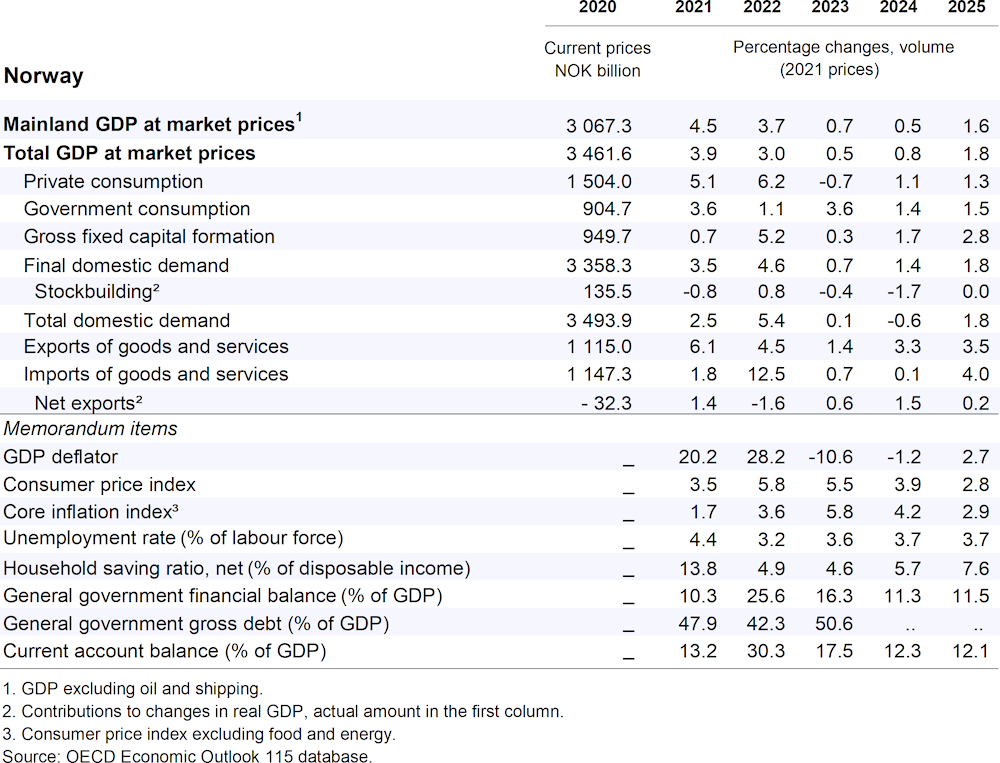

Mainland GDP is projected to increase by 0.5% in 2024, with an acceleration to 1.6% in 2025 as domestic demand strengthens. High inflation and monetary policy tightening have dampened activity, with stagnation in most non-oil sectors and a sharp decline in construction, whereas oil and gas extraction has remained buoyant. Inflation is set to decline only slowly, held up by exchange rate depreciation and cost pressures, given the still tight labour market and weak productivity growth.

Monetary policy needs to remain restrictive for some time to ensure that inflation approaches the target. The fiscal stance should not add inflationary pressures. It should turn increasingly restrictive in the medium term, making space to cope with spending pressures from population ageing. Structural reforms that limit early retirement, as well as sickness and disability benefits, are key for inclusive growth and fiscal sustainability.