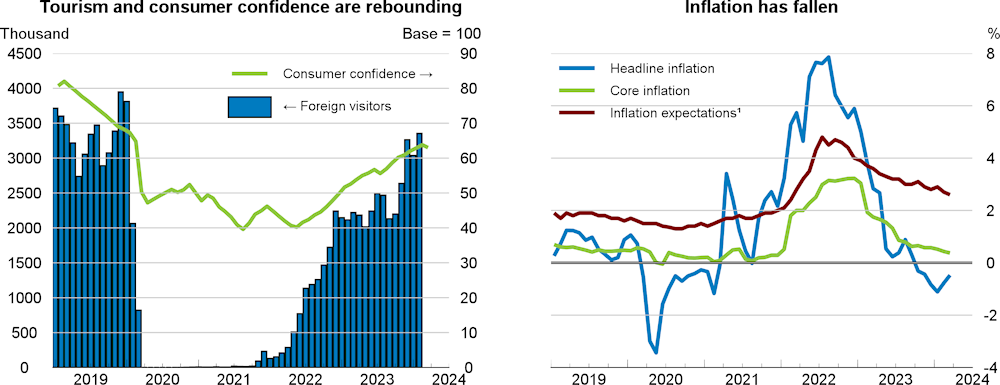

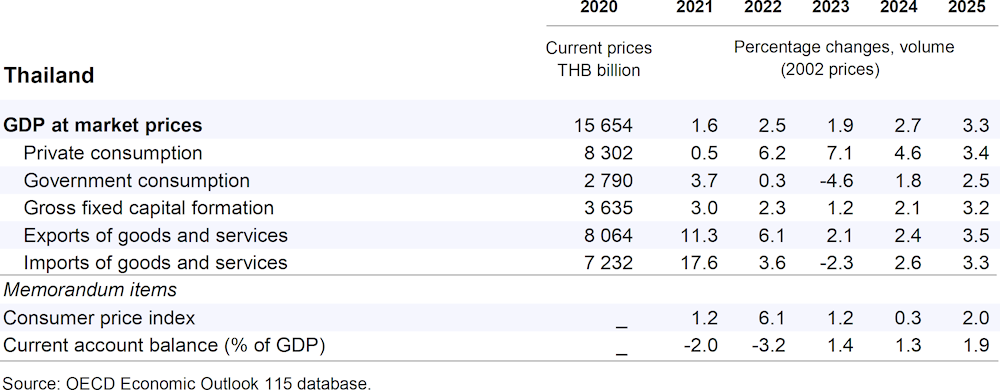

GDP is projected to grow by 2.7% in 2024 and 3.3% in 2025. Despite having lost some momentum in late 2023, private consumption, buoyed by fiscal measures, a strong labour market and declining inflation, is expected to remain robust, while investment will recover after a weak patch during 2023. A continued revival of international tourism is underpinning the steady recovery. However, weaker external demand for goods, particularly in key trading partners, could add to weakening competitiveness and reduce growth prospects.

Public debt increased rapidly during the pandemic and fiscal consolidation will be required, including by avoiding energy subsidies and broad temporary support measures while focusing on improvements in targeted, permanent support to vulnerable groups. Monetary policy should continue its neutral stance in light of solid near-term growth and upside risks to inflation. Competition remains limited across several sectors, holding back innovation and productivity. Improvements in education, training and active labour market policies would help youths and women better integrate into the labour market and boost the economy’s growth potential.