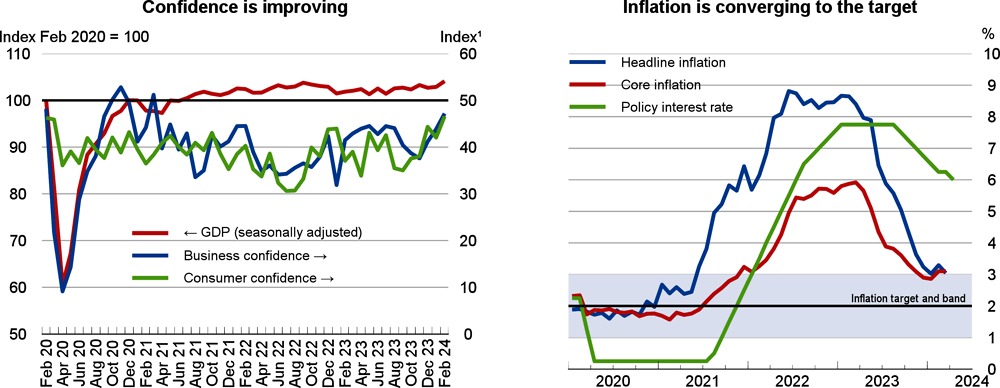

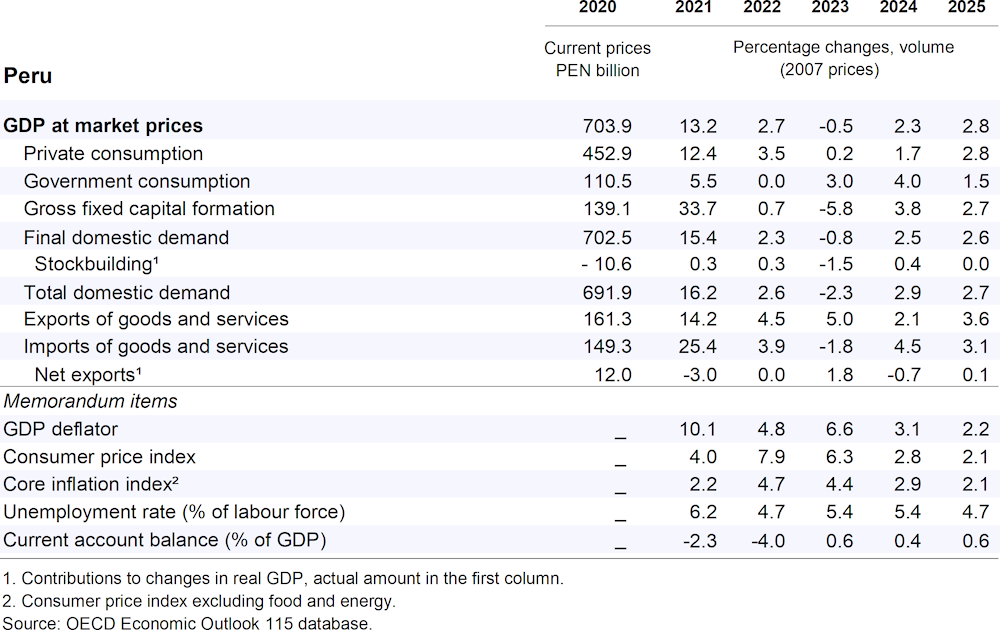

GDP will pick up to 2.3% in 2024 and 2.8% in 2025, supported by more favourable financial conditions and reduced inflation that will bolster domestic demand. Central government efforts to expand infrastructure, coupled with a faster execution of public investment projects by subnational governments, will support investment. A gradual employment recovery will stimulate private consumption. Exports are expected to be sustained by a rebound in tourism, fishing, and agricultural production as the impact of El Niño dissipates. Inflation will slow further, converging gradually to the midpoint of the target range of 2% by the end of 2024.

Monetary policy is expected to continue easing, as inflation and inflation expectations return to the target. The planned gradual reduction of the fiscal deficit over the next years, in compliance with the fiscal rules, should be implemented to maintain low public debt and safeguard the credibility of the robust fiscal framework. Enhancing spending efficiency and implementing a tax reform to boost public revenues are needed to address critical infrastructure and social needs.