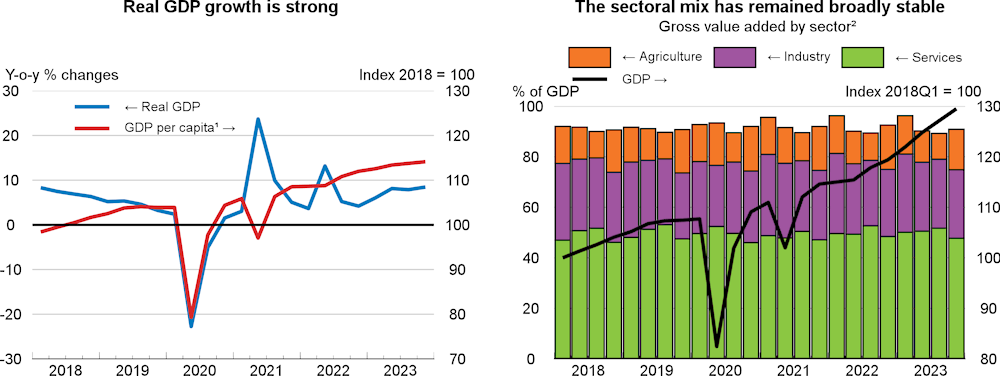

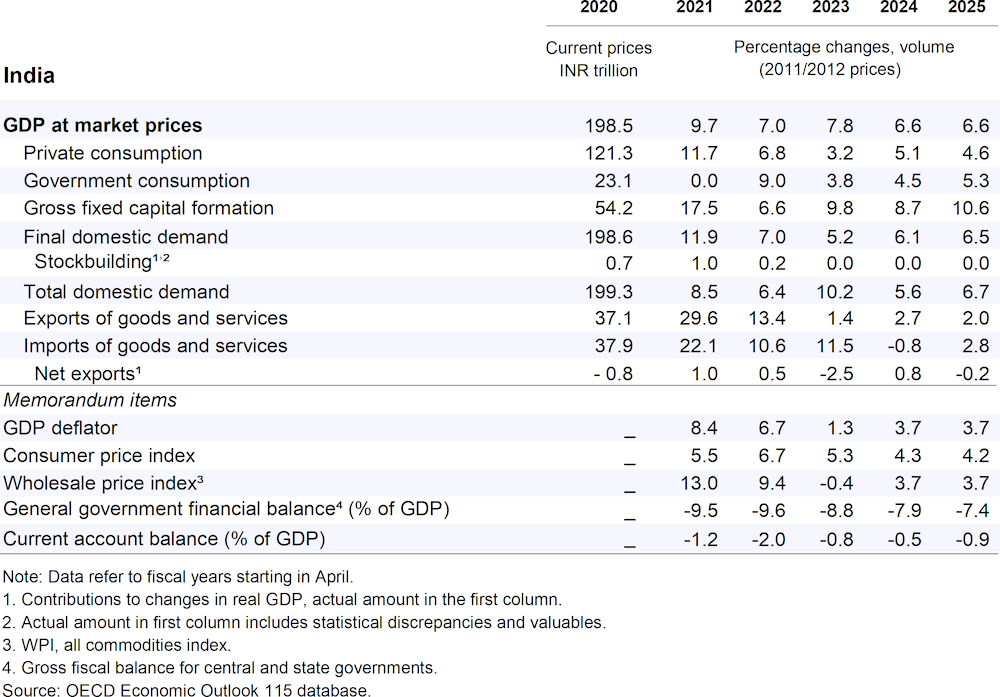

GDP growth is projected at 7.8% in FY 2023-24 and around 6½ per cent in each of the following two fiscal years. Domestic demand will be driven by gross capital formation, particularly in the public sector, with private consumption growth remaining sluggish. Exports will continue to grow, especially of services such as information technology and consulting where India will continue to increase its global market share, supported by foreign investment. Headline inflation will decline gradually, although uncertainty about food inflation remains elevated.

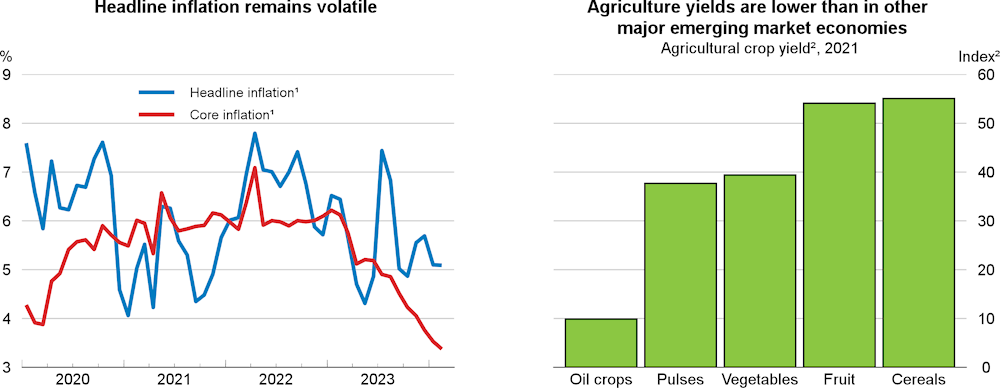

Monetary policy easing is projected to start in the second half of the year once lower inflation is maintained. The 2024 Interim Union Budget aims for consolidation, setting a fiscal deficit target at 5.1% of GDP for FY 2024‑25. Fiscal support should remain targeted towards vulnerable households. Rising debt limits fiscal space and increases the need to tackle structural problems in order to make growth fairer and more sustainable. Returns from reforms could be significant in agriculture, which accounts for the largest share of employment and, due to low productivity and still widespread poverty, absorbs considerable public subsidies.