Andrew Green

OECD Employment Outlook 2023

Artificial Intelligence and the Labour Market

OECD Employment Outlook

3. Artificial intelligence and jobs: No signs of slowing labour demand (yet)

Abstract

Artificial Intelligence (AI) is the latest technology to stoke fears of rapid automation and job loss. This chapter reviews the current empirical literature on the employment effects of AI to date. It begins with a discussion of the progress in AI’s capabilities and what that implies for the tasks, occupations and jobs most exposed to these advances. An overview is then given of the findings of recent studies of the effect of AI on employment including econometric studies, as well as surveys and case studies of firms and workers. The chapter concludes by discussing policies that can minimise the possible displacement effects of AI while enhancing economic growth.

In Brief

Artificial intelligence (AI) is the current technological innovation sparking hopes of rapid productivity gains and stirring fears of job loss. Using a fast-evolving suite of algorithms and statistical models – in particular, machine learning – increasingly available big data and falling costs of compute capacity, AI has made rapid advances in its ability to supply answers to problems where formal rules are impossible to codify, and where humans have until recently had a comparative advantage in inferring decisions from their training or past experiences.

AI’s improving ability to complete these non-routine tasks raises new worries of job displacement for occupations previously thought impervious to automation. Occupations in finance, medicine and legal activities which often require many years of education, and whose core functions rely on accumulated experience to reach decisions, may suddenly find themselves at risk of automation from AI.

This chapter explores whether such fears are grounded in the empirical evidence that has accumulated so far. To do this, it analyses the emerging empirical literature on the effect of AI on labour demand in general, and on the occupations most exposed to advances in AI. Caution is however required in drawing conclusions from these stylised facts since this evidence does not account for the impact of recent advances in large language models and generative AI generally, whose potential impacts are difficult to quantify. The key findings are:

Theoretically, the net impact of AI on employment is ambiguous. AI will displace some human labour (displacement effect), but it can also raise labour demand because of the greater productivity it brings (productivity effect). AI can also create new tasks, resulting in the creation of new jobs (reinstatement effect) particularly for workers with skills that are complementary to AI.

Measures of AI exposure, which are used in this chapter to evaluate the degree of overlap between tasks performed in a job and those which AI is theoretically capable of performing, show that AI has made the most progress in its ability to perform non-routine, cognitive tasks, such as information ordering, memorisation and perceptual speed. These are often key abilities demanded in occupations that usually require several years of formal training and/or tertiary education. These measures pre‑date the recent advances in generative AI applications (ChatGPT, for example), and one should therefore interpret them with caution: both the occupational range and extent of AI exposure might rapidly become larger as generative AI use is increasingly incorporated into production processes and new, more powerful AI systems are developed.

High-skilled occupations are those most likely to involve non-routine cognitive tasks, and they have therefore been the most exposed to progress in AI. Examples of such occupations include business professionals, managers, chief executives and science and engineering professionals.

So far, there is little evidence of significant negative employment effects due to AI. Empirical studies using cross-country variation in AI exposure, or studies using within-country variation by local labour markets, do not find any statistically significant decrease in employment. Similarly, recent surveys of workers and firms, or case studies of firms adopting AI, find few employment changes. However, AI is evolving rapidly, and advances in generative in AI may disprove some of the evidence accumulated so far.

Despite their higher exposure to AI, high-skilled workers have seen employment gains relative to lower-skilled workers over the past ten years. This may be because AI creates new tasks and jobs for workers who have the right skills, and this chapter does provide evidence that this reinstatement effect is prominent at this early stage of AI adoption in production activities.

Other reasons why the impact of AI on employment may so far have been limited is that adoption rates remain relatively low or that firms are reluctant to lay off workers in the short term and instead rely on natural attrition (e.g. retirement and voluntary quits) to lower employment. Firms may also need time to implement new technologies after adoption. Any negative employment effects of AI may therefore take time to materialise. However, the latest wave of generative AI may further expand the tasks and jobs that can be automated.

From a policy perspective, the evidence points to the need for education and training to ensure that workers have the skills to take advantage of this new technology (see also Chapter 5), and for social dialogue to effectively manage transitions and achieve a fair distribution of productivity gains (see also Chapter 7). Moreover, to minimise possible negative employment effects, countries could further enhance competition in both the product and the labour market and review their mix of labour and capital taxation to ensure that it does not incentivise labour-replacing technology adoption. Recent developments in large language models and generative AI additionally necessitate policies to prepare for potential economic and labour market disruptions (see Chapter 6).

Introduction

Advances in artificial intelligence (AI) may unsettle the established narrative on the risk of employment loss from automation. The most recent wave of AI started around 2011 when advances in machine learning, a branch of computational statistics used to make predictions from unstructured data, began to find applications in a variety of industries and settings (Agrawal, Gans and Goldfarb, 2019[1]; OECD, 2019[2]). Like electricity or the steam engine before it, AI can be considered a general purpose technology due to its ability to be used pervasively across many industries and to foster general productivity gains (Bresnahan and Trajtenberg, 1995[3]; Lane and Saint-Martin, 2021[4]). The consensus among economists and policy makers from previous rounds of automation technologies, however, is that labour demand should remain strong. Human labour complements new technologies, which gives rise to new jobs and productivity gains, and raises demand for labour overall (Autor, 2015[5]; OECD, 2019[6])

However, AI is different from previous automation technologies. Previous technologies automated primarily routine tasks and did not lead to reductions in labour demand overall (OECD, 2019[7]). AI is a machine‑based system that can, for a given set of human-defined objectives, make predictions, recommendations or decisions influencing real or virtual environments (OECD, 2019[8]). In other words, AI takes data and, (usually) using a statistical model, generates predictions, decisions or recommendations. Importantly, AI can learn from its actions, and improve its predictions and recommendations over time. Noteworthy applications include credit scoring and lending, legal assistance and medical diagnosis. Previously, it was widely believed that humans had a comparative advantage over machines in these sorts of complex tasks. AI, however, may render these tasks more amenable to automation (Agrawal, Gans and Goldfarb, 2019[9]). Some have gone as far as to theorise that AI will have the potential to “increase [its] productivity and breadth to the extent that human labour and intelligence will become superfluous” – see Nordhaus (2021[10]).

This chapter assesses the emerging empirical evidence for how AI may affect labour demand. During the past decade, the economics profession has revised its thinking on how technology affects labour demand. Theories of automation take much more seriously the displacement effects of automation, and the possibility that new technologies may lead to decreased labour demand (Susskind, 2022[11]). At the same time, advances in applications of machine learning have led to a greater overlap with abilities used in the workplace. Measures of AI exposure can be used to gauge the overlap between tasks performed in a job and tasks which AI is theoretically capable of performing, and therefore to make predictions for the occupations and jobs most affected by AI. The theory of how AI will automate and complement labour, combined with measures of AI exposure, form the basis for the empirical evidence of the employment effect of AI (Section 3.1).

Using these measures of AI exposure, the chapter discusses the emerging estimates on the effect of AI on employment. The automation of routine tasks was previously shown to decrease the share of jobs in middle‑skill occupations (Autor, Levy and Murnane, 2003[12]; OECD, 2017[13]). AI is now expected to affect a much broader set of occupations. The chapter therefore also assesses how certain groups may be particularly vulnerable to AI exposure. The discussion analyses empirical estimates at various levels including firms, occupations and countries, but also draws on new OECD research including surveys of workers and employers, and firm-level case studies based on interviews with those tasked with implementing or managing AI within firms (Section 3.2).

Policy should be designed to mitigate the harmful effects of displacement from AI. AI will substitute for labour in certain jobs, but it will also create new jobs for which human labour has a comparative advantage. The chapter discusses policies to encourage the ways AI and human labour can complement each other, and in cases where AI must replace labour, to ensure that the policy in place amplifies the productivity effects to the largest extent possible, creating new demand for labour in jobs not substituted by AI (Section 3.3).

3.1. Artificial intelligence expands the set of jobs at risk of automation

In the last decade, AI has made impressive progress in many domains including computer vision, playing games, as well as reading comprehension and learning. These domains can be loosely viewed as grouping many non-routine, cognitive tasks which are key demands in many highly paid occupations, which typically require a post-secondary education. Even more astonishing than the capabilities is the short time span in which this progress has been made. In November 2022, OpenAI launched ChatGPT, a large language model (LLM) trained on vast amounts of data, which has obvious applications in the workplace including the ability to write text, pass exams in law or business and assist in clinical decision making (see Chapter 2). The occupational range impacted by AI might rapidly grow as generative AI use finds applications in a wider set of production processes and new, more powerful AI systems are developed.

From a theoretical perspective, AI will automate tasks employed in production, but it will also complement labour and create new tasks. The effect of AI on the quantity of labour demanded is therefore ambiguous. AI will displace human labour (displacement effect), but it can also raise labour demand in jobs not exposed to AI because of the greater productivity it brings (productivity effect), as well as the creation of entirely new jobs (reinstatement effect). Which of these effects dominates, and whether aggregate labour demand therefore increases, or decreases is unclear a priori. However, not all workers are exposed to AI to the same degree, and the employment of certain groups may be more affected than others. Workers who perform a high share of non-routine cognitive tasks, such as white‑collar professionals, have been the most exposed to advances in AI.

3.1.1. Artificial intelligence will automate certain tasks, but the net impact on employment is ambiguous

The most basic building block for understanding the impact of AI on labour demand is tasks. The production of a final good or service requires the completion of a set of tasks, and groupings of tasks are what defines production in a firm, a job, or an occupation.1 For example, a worker in a warehouse where incoming orders are received, processed and filled will be required to complete a set of tasks including reading an order, walking to the correct set of shelves and picking items. The firm operating the warehouse will employ different sets of workers and therefore encompass a wider set of tasks for production. Continuing the example, the picker may pass the completed order to a packer who is tasked with preparing a box for shipping, securely packing the items in the box, and then sealing the box with a shipping label.

Sets of tasks currently performed by human labour are at risk of automation by AI.2 Workers complete tasks that have not already been automated,3 but firms are cost minimisers, and they will replace human labour with AI if it is technologically feasible and cheaper for AI to complete a task.4 For example, if the firm that owns the warehouse can develop or purchase AI to automatically queue and move the shelves rather than have the worker walk to each one, this will replace the task of picking by a worker and could lead to cost savings and productivity improvements.

AI can affect labour demand by automating certain tasks, complementing humans in completing existing tasks, but also creating new tasks. First, just as in the example above, developments in AI can automate tasks previously done by human labour. This results in AI replacing human labour in tasks. Second, AI may create new tasks which will require human labour. In the warehouse example, if the firm is successfully able to use AI to install moving shelves, the new technology will require monitoring, maintenance, and possibly improvements, thereby creating new tasks for workers to perform. Finally, AI may complement workers, which means that AI will uniformly improve a worker’s productivity in all tasks to which they are assigned. With this last channel, AI neither replaces workers in the completion of tasks nor creates new tasks; it allows workers to perform the same tasks more efficiently.5 The three channels are not mutually exclusive, and all may be present at the same time.

The implications for labour demand depend on which effects dominate. The creation of new tasks should lead to increases in labour demand. In particular, the creation of new tasks results in a reinstatement effect that creates new jobs and leads to increasing employment. These jobs can come from anywhere, but real-world examples usually link them to the operation of the new technologies themselves (Acemoglu and Restrepo, 2018[14]; Autor et al., 2022[15]). For AI, these new jobs are likely to be workers with the skills to develop or maintain AI systems (see Chapter 5), but they also include new jobs for the larger set of workers who will only interact with AI applications.

The automation channel, or the replacement of tasks previously performed by human labour, is ambiguous with respect to whether it increases or decreases demand for labour. The automation channel results in a displacement effect, which decreases labour demand as human labour is replaced by AI. To return to the warehouse example, if workers do not need to walk to each shelf, the warehouse will probably need fewer of these workers resulting in decreased labour demand. Finally, in addition to the displacement effect, the automation channel can give rise to a productivity effect which can result in increases in labour demand for tasks or jobs not automated by AI such as packers and forklift operators. The productivity effect neither arises (directly) from the automation of tasks, nor the ability to perform tasks more efficiently. The productivity effect is a product of the induced demand for tasks or jobs generated from the cost savings of automation.

Whether the productivity effect dominates the displacement effect, and therefore whether automation increases or decreases labour demand, is the core question facing the future of labour and AI. The automation resulting from AI can lead to increases in labour demand if the cost savings from AI increase demand for the final good or service produced by a firm, or demand for goods produced in other firms. In the warehouse example, if the decrease in labour demand for pickers decreases costs enough so the firm can reduce prices sufficiently to raise demand for their services, this may result in the firm hiring more packers and forklift operators. It may also result in the firm increasing demand for other goods and services produced outside the firm thereby contributing to greater labour demand.6 This productivity effect needs to be sufficiently large so that increases in employment for workers not exposed to AI more than offset the workers displaced by AI (Acemoglu et al., 2022[16]). Finally, the productivity effect depends on the share of the cost savings from AI that are passed along to customers in the form of lower prices and the elasticity of demand for the final product.7

To summarise, there are two key questions concerning the effect of AI on aggregate employment. Broadly, is AI increasing or decreasing labour demand in the aggregate with all channels (productivity, displacement and reinstatement) included?8 More narrowly, when tasks are automated with AI, which effect is dominant: the productivity or displacement effect?9 Although the first question is often the first order point of concern, policy makers should pay careful attention to which effect is driving the results. The effects that are dominating point to which groups’ employment prospects may be most harmed by AI and suggest specific points where policy makers may wish to intervene to ensure that the cost savings from AI do not result in lower demand for labour (see Section 3.3 for a discussion of policies).

3.1.2. AI has made the most progress performing non-routine, cognitive tasks

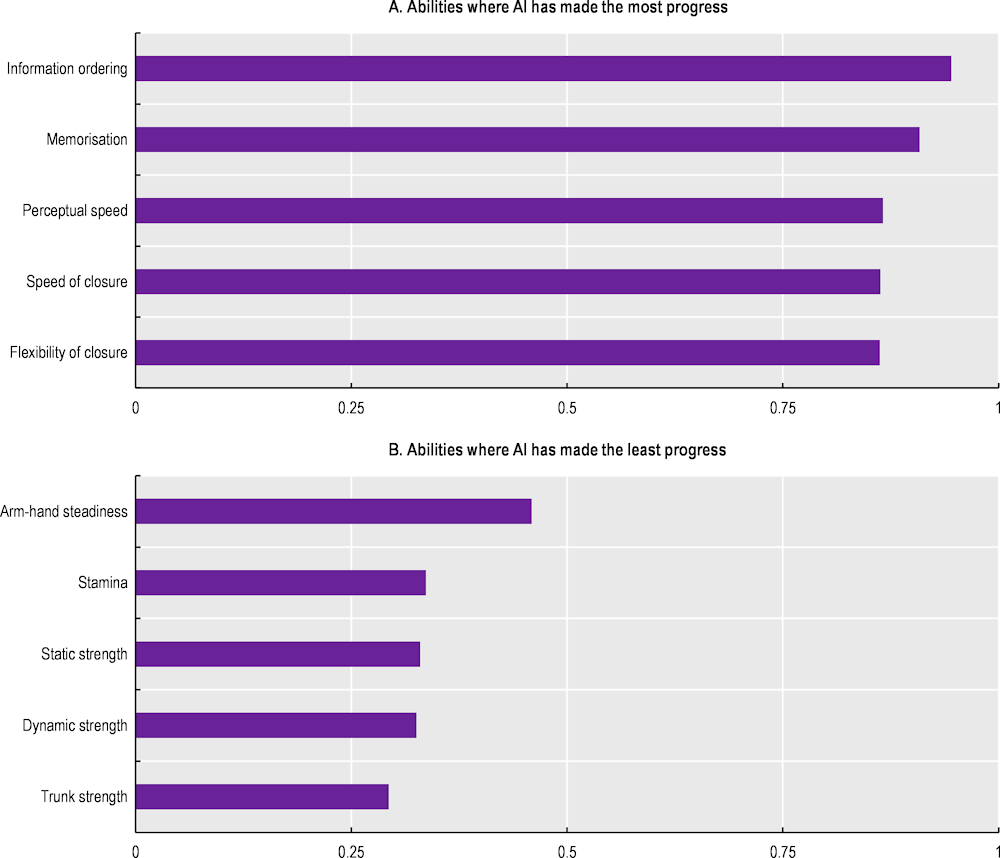

AI has made the most progress in automating non-routine, cognitive tasks. Figure 3.1 shows the abilities where AI has made the most progress in replicating human performance as of 2015. The most progress has been made in the abilities “Information ordering”, “Memorisation”, and “Perceptual Speed”. The overlap of these abilities with AI is straightforward. For example, “Speed of Closure” is the ability to quickly make sense of, combine, and organise information into meaningful patterns. Examples include making sense of messy handwriting and recognising a song after the first few notes (O*NET, 2023[17]). These cognitive abilities are often important for high-skill occupations, such air traffic controllers, engineers, and managers. In contrast, various abilities related to strength are where AI has made the least progress. These are more indicative of non-cognitive, non-routine occupations such as dancers, athletes, bricklayers and farm workers.10

This chapter uses advances in the capabilities of AI compared to the tasks performed in jobs as a proxy for AI exposure. This approach draws on matching the assessed capabilities of AI (Brynjolfsson, Mitchell and Rock, 2018[18]; Webb, 2020[19]; Tolan et al., 2021[20]; Felten, Raj and Seamans, 2021[21]; Lassébie and Quintini, 2022[22]) to the tasks currently performed by human labour as described in the Occupational Information network (O*NET, see Box 3.1). For example, the measure of AI exposure used in this chapter comes from Felten, Raj and Seamans (2021[21]) who measure progress in AI applications from the Electronic Frontier Foundation’s AI Progress Measurement project and connect it to abilities from O*NET using crowd-sourced assessments of the connection between applications and abilities.11 The measured exposure of each task to AI is then aggregated to the occupation (industry or local labour market, respectively) level to derive measures of exposure. The measure is theoretically ambiguous with respect to whether the overlap between progress in AI and the abilities required in a job means “risk of displacement”, or if AI will be complementary. Finally, these exposure measures can also be viewed as an instrument for actual AI adoption, which may be concomitant with the adoption of other technologies, and where workers are likely to be aware of its deployment.12 This allows for more credible empirical strategies for measuring employment effects than observational studies of AI adopting firms.13

Figure 3.1. AI has made the most progress in abilities that are required to perform non-routine, cognitive tasks

Relative progress made by AI in relation to each ability, 2010‑15

Notes: The x-axis measures the relative exposure to AI scaled such that the minimum is zero and the maximum is one. Exposure is defined as the link between O*NET abilities and AI applications (a correlation matrix) taken from Felten, Raj and Seamans (2019[23]). The matrix was built by an Amazon Mechanical Turk survey of 200 gig workers per AI application, who were asked whether a given AI application – e.g. image recognition – can be used for a certain ability – e.g. near vision. The correlation matrix between applications and abilities is then calculated as the share of respondents who thought that a given AI application could be used for a given ability. To obtain the score of progress made by AI in relation to a given ability, the shares corresponding to that ability are first multiplied by the Electronic Frontier Foundation (EFF) progress scores in the AI applications; these products are then summed over all nine AI applications.

Source: Reproduced from Georgieff and Hyee (2021[24]), “Artificial intelligence and employment: New cross-country evidence”, https://doi.org/10.1787/c2c1d276-en, using data from Felten, Raj and Seamans (2019[23]), “The Variable Impact of Artificial Intelligence on Labor: The Role of Complementary Skills and Technologies”, https://doi.org/10.2139/ssrn.3368605.

Box 3.1. The O*NET database

The Occupational Information Network (O*NET) contains information on occupations including the skills and abilities they require. Created in 1998 by the U.S. Department of Labor, and updated on a regular basis, it covers almost 1 000 occupations.1 Most of this information is collected from job incumbents and experts through surveys (Tsacoumis, Willison and Wasko, 2010[25]). Skill and ability requirements of occupations are measured in terms of importance and level. The former indicates whether a skill or ability is important to perform the job. The latter indicates the level of mastery or proficiency in that skill or ability needed for the job. Both O*NET Skills and Abilities ratings on Importance and Level are also based on the responses of incumbent workers (or occupational experts) to other items on the O*NET survey questionnaire. More information on the O*NET database, and current and archive versions of the dataset can be found online.2

As O*NET is developed by the Employment and Training Administration in the United States, it is geared towards the content of jobs in the labour market in the United States. Despite this, O*NET has been regularly used for the analysis of countries other than the United States. The assumption that skill measures from one country can be generalised to other countries has been tested and largely holds (Handel, 2012[26]; Cedefop, 2013[27]). For example, Handel (2012[26]) finds that occupational titles refer to very similar activities and skill demands across different countries. Specifically, high correlations are found between O*NET scores and parallel measures from the European Social Survey, EU Labour Force Survey, Canadian skill scores, the International Social Survey Program, and the UK Skill Survey, respectively, with average correlations of 0.80. Most skill scores can thus be generalised to other countries with a reasonable degree of confidence. As a result, the O*NET information on skill and ability requirements has been used extensively in labour market research, including to study issues of automation (Deming, 2017[28]; Webb, 2020[19]).

1. See O*NET Taxonomy at: https://www.onetcenter.org/taxonomy.html#latest.

Other approaches to measuring AI exposure that have been used in the literature do not capture workers without AI skills or are less suited for cross-country comparative analysis. One popular method for identifying AI exposure uses job postings and their associated skill demands to infer AI adoption by firm, occupation or industry (Alekseeva et al., 2021[29]; Squicciarini and Nachtigall, 2021[30]; Calvino et al., 2022[31]; Manca, 2023[32]; Green and Lamby, 2023[33]).14 However, this method misses firms who adopt AI but do not develop or service it in-house, or workers whose abilities overlap with AI advances but who do not need AI skills.15 Another approach used in the literature relies on government surveys of AI adoption by firms. These surveys have the advantage of being representative of the labour market, and they are already emerging in some countries, but they are often not uniform across countries,16 and too recent to track longer term employment changes.

One downside of the AI exposure measure used in this chapter is that it is backward-looking. The exposure measures developed in Felten, Raj and Seamans (2021[21]) and used as inputs in Figure 3.1 and Figure 3.2 stem from 2010‑15. This is necessary because it takes time for scientific advances to be confirmed; developed into commercial applications; and then have firms adopt and implement them before one can reasonably expect to detect employment changes. However, it does raise the question of whether these AI exposure measures are still relevant given recent developments in large language models (LLM) as exemplified by ChatGPT, for example. However, various researchers have produced updated estimates of AI exposure considering the advances in LLM, and the results of early uses of LMM do not seem to suggest qualitative differences in exposure compared to the measures used in this chapter (see Box 3.2).

Box 3.2. The growth of large language models (LLM) and the perils of predicting the effects of rapidly progressing AI

In late November 2022, OpenAI released ChatGPT, which astounded AI researchers, policy makers and the public with its ability to generate human-like responses with knowledge of a multitude of subjects. Essentially a chatbot that responds to users’ queries, ChatGPT has a range of potential applications from everyday convenience to automating tasks in the workplace. It can write legal contracts, summarise the literature and accumulated knowledge on a particular subject, write and debug computer code, translate among languages, and even do arithmetic. Microsoft, Google, among other large technology companies, are developing their own versions of AI-trained chatbots. The widespread potential use and the phenomenal speed of improvement of LLM potentially changes what it means to be “exposed” to AI and raises questions about the relevance of existing estimates of the effect of AI on employment.

Recent estimates of how LLM may change AI exposure measures do not find large differences in AI exposure compared to previous estimates. Felten, Raj and Seamans (2023[34]) update their original AI exposure measures in light of the release of ChatGPT by reweighting their initial estimates to only include language modelling. Their results are largely in line with their previous studies with teaching professions notably becoming the most exposed. Researchers affiliated with OpenAI, the firm that created ChatGPT, released their own measures of exposure by evaluating whether the time to complete tasks on the job can be reduced by at least 50% with the aid of ChatGPT or similar applications (Eloundou et al., 2023[35]). They find that exposure rises with average earnings (based on data from the United States) as well as education and training requirements. The investment bank Goldman Sachs also released estimates of AI exposure, based on the existing literature and their own assessments of likely use cases of large language models. They find that AI exposure is most heavily concentrated in high-skill professional services industries (Briggs and Kodnani, 2023[36]).

These early estimates of occupational AI exposure that take into account the capabilities of large language models like ChatGPT reach similar conclusions as previous estimates of AI exposure. It is primarily high-pay occupations requiring higher than average education or training that are most exposed to AI. However, these estimates are based on the early assessments of the researchers, and they have not yet been validated on external data. In addition, exposure is not necessarily equivalent to automation, and the effect of AI on employment will require continuous monitoring.

3.1.3. High-skilled, white‑collar occupations have been most exposed to recent progress in AI

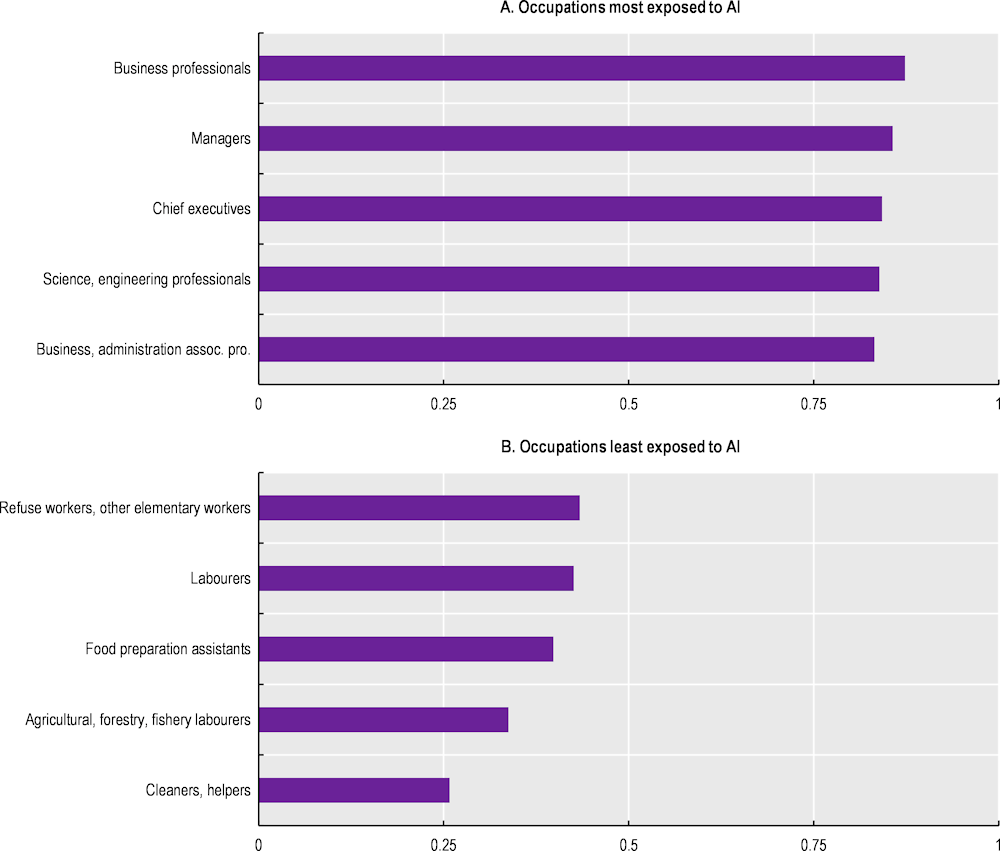

The occupations most exposed to recent progress in AI are high-skill, white collar occupations. Georgieff and Hyee (2021[24]) use the Survey of Adult Skills (PIAAC) data to allow the assessed progress of AI to vary by country.17 They find that, on average across OECD countries in their sample, “Business Professionals”, “Managers”, “Chief Executives” and “Science and Engineering Professionals” are the most exposed occupations to AI (Figure 3.2). This follows intuitively from the abilities where AI has made the most progress. In contrast, “Food preparation assistants”, “Agriculture, forestry and fishery labourers” and “Cleaners, helpers” are the least exposed to AI.

Figure 3.2. Highly educated white‑collar occupations are among the occupations with the highest exposure to AI

Average exposure to AI across countries by occupation

Notes: The x-axis measures the relative exposure to AI scaled such that the minimum is zero and the maximum is one. Estimates are derived from cross-country averages taken over the 23 countries included in Georgieff and Hyee, (2021[24]). The analysis uses the Survey of Adult Skills (PIAAC) to derive cross-country variation in occupational exposure to AI from Felten, Raj and Seamans (2019[23]). All estimates are unweighted and do not rely on cross-country differences in the occupation distribution. Occupations are ISCO‑08 2‑digit.

Source: Georgieff and Hyee, (2021[24]), “Artificial intelligence and employment: New cross-country evidence”, https://doi.org/10.1787/c2c1d276-en, calculations using data from the Survey of Adult Skills (PIAAC) and Felten, Raj and Seamans (2019[23]), “The Variable Impact of Artificial Intelligence on Labor: The Role of Complementary Skills and Technologies”, https://doi.org/10.2139/ssrn.3368605.

3.2. It is too early to detect meaningful employment changes due to artificial intelligence

This section examines the emerging empirical evidence for the effect of AI on employment. It draws a distinction between aggregate studies which cannot disentangle the specific effects of AI on employment (i.e. displacement, productivity and reinstatement), and more fine‑grained microeconomic studies which try to isolate the competing displacement and productivity effects. The section then discusses which groups of workers have been found to be most affected by AI and ends with an attempt to reconcile the results from different studies.

3.2.1. In the aggregate, negative employment effects due to artificial intelligence are (so far) hard to find

Studies examining the effect of AI on aggregate employment have so far found little to no effect on employment. Using their AI occupational impact exposure measure (AIOI, see above) and variation in occupational exposure within U.S. states, Felten, Raj and Seamans, (2019[23]) find no effect of AI exposure on employment growth between 2010 and 2016. Georgieff and Hyee, (2021[24]) use data from PIAAC to extend AIOI and allow for within-country variation in the AI exposure measures of Felten, Raj and Seamans, (2019[23]). They find positive but insignificant effects of AI exposure on aggregate employment using variation in occupation exposure to AI within a sample of OECD countries.

Even at lower levels of aggregation, there is currently no detectable effect of AI on aggregate employment. Acemoglu et al. (2022[16]) examine employment changes from AI using differences in AI exposure by U.S. commuting zones by industry, and separately, variation by detailed occupation. In all specifications they find no statistically significant effect of AI exposure on employment between 2010 and 2017 (industry) and 2018 (occupation). Fossen and Sorgner (2022[37]) estimate the effect of AI exposure on the probability of leaving employment using short panels of individual workers in the United States between 2011 and 2018. They find that exposure to AI decreases the probability of workers to exit employment.

Surveys of firms’ AI adoption and ensuing employment changes similarly find no detectable decreases in employment. In a survey of 759 managers of firms in the United Kingdom, Hunt, Sarkar and Warhurst (2022[38]) find that AI is leading to greater turnover, but when the researchers look at net employment changes, the results are inconclusive as firms are equally likely to report net employment gains and losses compared to firms not adopting AI. Similarly, an OECD survey of firms in manufacturing and finance across seven OECD countries finds that most firms adopting AI say that it did not change employment (Lane, Williams and Broecke, 2023[39]). Slightly more firms report employment decreases compared to increases, but these differences are not statistically significant. These results accord with national surveys of firms that adopt AI. A random sample of over 300 000 employer businesses in the United States from the U.S. Census Bureau collected information on firms’ adoption of advanced technologies from 2016 to 2018. The majority of firms reported no changes in employment levels due to advanced technologies but, of the firms adopting AI, 26% said that this caused them to increase employment compared to less than 10% which saw their employment levels decrease (Acemoglu et al., 2022[40]).

Although employment may not (yet) have declined because of AI, firms more exposed to artificial intelligence tend to hire less in jobs not requiring AI skills. Acemoglu et al. (2022[16]) use online job postings and a firm’s AI exposure in 2010 (roughly before the proliferation of AI) to show that firms more exposed to AI decreased vacancy posting for jobs not requiring AI skills. This result even holds within firms using the variation in AI exposure across local labour markets where the firms operate. Compared to aggregate studies, the empirical design attempts to isolate the competing productivity and displacement effects of AI on employment from the reinstatement effect.18 The authors interpret their results as evidence that, as of now, AI is not generating a large productivity effect to offset the decrease in hiring from the displacement effect. However, the authors also find a strong effect of AI on the growth of AI-related vacancies, which can be interpreted as evidence of a strong reinstatement effect. This may be why the authors find no evidence of aggregate effects of AI on employment (see above).19

There is some evidence of employment declines due to AI when examining specific sectors. Grennan and Michaely, (2020[41]) find that sell-side equity analysts – high-skill workers who predict stock performance for clients – are more likely to exit the profession the more they are asked to cover stocks with a lot of publicly available data, which they use as a proxy for the ease with which AI could perform the same task. In addition, analysts more exposed to equities, which are easier for AI to model, are more likely to leave research altogether suggesting that AI has a powerful displacement effect on this profession. In short, the only two studies that try to isolate the productivity effect from the displacement effect find evidence that the displacement effect dominates. Yet more research is clearly needed on this issue.

3.2.2. High-skilled workers have seen employment gains

Although high-skill workers are more exposed to AI, many studies find that high-skill workers have had better employment prospects after the introduction of AI. The effect of AI exposure on the probability of transitioning into non-employment declines the most for workers with a tertiary education (Fossen and Sorgner, 2022[37]). Using the median annual income for an occupation, and variation across U.S. states, Felten, Raj and Seamans, (2019[23]) find a positive relationship between employment growth and AI exposure for high-skill (high income) occupations but not for low- and medium-skill occupations. Using within- and cross-country variation in AI exposure, Georgieff and Hyee (2021[24]) find AI exposure is associated with higher employment growth only in occupations with the highest degree of computer use, which is a proxy for higher skills. These occupations are highly correlated with measures of skill, including education and median annual income. All these studies appear to be picking up a similar signal, but exactly what that is, and its causal interpretation, remains an open question for future research. Moreover, given the rapid increases in the capabilities of AI, in particular with generative AI models, it is likely that these associations will evolve in the future (see Box 3.2).

There is also evidence that low-skilled workers may face declining employment prospects because of AI. In their survey of AI-producing firms, Bessen et al., (2018[42]) find that, within customer firms for AI products, higher skilled occupations are the most likely to see employment growth from AI adoption, but that occupation groups including front-line service workers and manual workers are the most likely to see employment declines. OECD case studies of manufacturing and finance firms adopting AI similarly find that low-skill workers were often at the greatest disadvantage because when their tasks (and, by extension, their jobs) would be automated – unlike other workers – they were often the most difficult to retrain or move to another position within the firm (Milanez, 2023[43]).

3.2.3. Why is the employment effect of AI small (so far…)?

The results in the previous section have shown that, so far, AI has had little effect on aggregate employment. Moreover, although high-skilled workers are disproportionately exposed to recent advances in AI, they do not seem to have been adversely affected (yet). The rest of this section presents reasons for why the employment effects of AI to date are small, including: low overall AI adoption and productivity gains; firms’ preference to adjust labour demand through attrition rather than layoffs; the fact that advances in AI and AI exposure do not necessarily imply automation; and the creation of new tasks and jobs.20

Currently, AI adoption is low and the cost savings to firms are modest

Firms’ adoption of AI is just beginning, and overall penetration rates are still low. A recent module of the Annual Business Survey (ABS) from the U.S. Census Bureau which sampled 300 000 businesses finds that just 3.2% of firms used AI between 2016 and 2018. This is consistent with data from Eurostat, which finds that, among OECD European Union countries, enterprise‑level AI adoption ranges from 23% in Ireland, 12% in Finland and 11% in Denmark to 3% in Hungary and Slovenia and 2% in Latvia (Eurostat, 2021[44]). Estimates from non-official sources tend to be higher though their qualitative findings are generally in line with official estimates – see Lane, Williams and Broecke, (2023[39]) for a discussion of the different sources of measurement.21

Low adoption rates should lead to marginal employment changes, which may be too small to detect in aggregate studies. The low adoption rates combined with little evidence for substantial productivity gains (see Chapter 4) from AI suggests that neither the displacement nor the productivity effect will be large enough compared to the overall labour market. This is the preferred interpretation of Acemoglu et al., (2022[16]) who find firm-level evidence of decreases in hiring from AI exposure, but argue that such changes are too small to detect in aggregate studies of the effect of AI on employment.

Firms rely on worker attrition rather than layoffs to adjust labour demand

Displacement from tasks or jobs does not necessarily imply short-term losses in employment. The studies (Section 3.2.1) that do find evidence of a displacement effect rely on data on hiring or narrow occupation groups. While these studies show that firm or establishment hiring may decline, or that narrow occupation groups within a firm may contract, they do not show that employment within the firm goes down.

Firms may keep affected workers within the firm and allow natural attrition to decrease employment levels over time. This would dampen or mitigate any short-term impacts of AI on employment. OECD case studies of finance and manufacturing firms adopting AI find that this is overwhelmingly the case. For example, a Canadian manufacturer of auto parts adopted an AI software that performs the cutting of custom metal moulds for auto parts. According to the firm, the ensuing productivity gains were large, and the necessary employment declines were managed gradually through planned retirements rather than immediate layoffs (Milanez, 2023[43]).

Firms may also be slow to adjust employment after adopting AI as a hedge against uncertainty in the efficacy of the applications themselves. Firms adopting AI may need time to understand the capabilities of AI and how to optimise its deployment to maximum effect (see below). However, there is no guarantee that AI applications will increase productivity to the extent it is hoped at the time of adoption. Retaining workers after AI adoption, and by extension their accumulated firm-specific human capital, provides insurance in the case AI applications underperform their projected benefits (Milanez, 2023[43]).

This gradual adjustment through attrition rather than immediate redundancies has previously been found to be the dominant way that firms in OECD labour markets adjust employment to accommodate the productivity gains from new technologies (OECD, 2020[45]).22 If firms are relying on attrition to adjust their labour demand, this does imply employment declines (or much slower growth), but it is preferable to mass layoffs. Workers who lose their jobs due to layoffs or other economic reasons often see long-term earnings losses (Jacobson, LaLonde and Sullivan, 1993[46]; Farber, 2017[47]; OECD, 2018[48]).

AI may be leading to greater efficiencies in labour market matching

One way the increasing use of AI may lead to higher employment is through improved labour market matching. One aspect of labour market performance is the efficiency and quality of labour market matching – i.e. the process by which workers are matched to jobs. Labour market matching involves a range of steps from writing job descriptions and opening vacancies all the way to making offers and salary negotiations. It covers private recruitment by firms, but it can also refer to the activities of public (see Box 3.3) and private employment services, as well as those of jobs boards and online platforms. It can even include internal matching within a firm.

Improved labour market matching should lead to lower unemployment. Matching jobseekers to vacancies is time‑consuming and therefore costly. The longer it takes to match workers to vacancies, the higher equilibrium unemployment will be (Blanchard et al., 1989[49]; Mortensen and Pissarides, 1999[50]). AI has vastly expanded the range of time‑ and resource‑saving possibilities when screening and shortlisting candidates. For example, AI, through “semantic expansion”, can parse CVs and take a single word such as “accountant” and expand the information linked to the candidate to include known synonyms, such as “account specialist.” This increases the efficiency of matching and ensures that candidates are not ruled out by narrow phrasing or phrasing that is slightly different from advertised text as is done in many current screening applications (Broecke, 2023[51]).

Box 3.3. The use of AI in Public Employment Services (PES) is growing in precedence across OECD countries

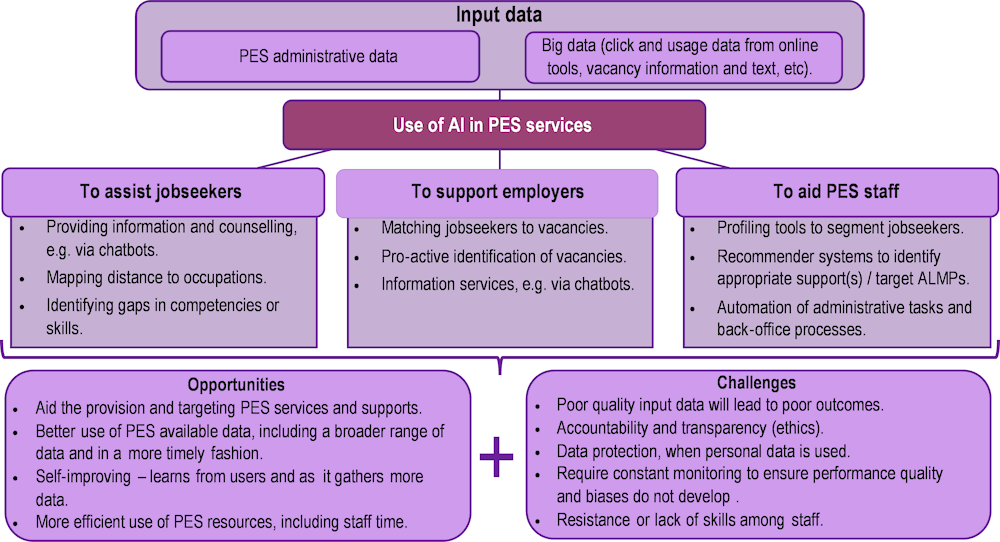

PES across the OECD have been increasingly engaging in efforts to modernise and digitalise in recent years, with the COVID‑19 pandemic undoubtedly acting as an accelerant of this trend. As part of this digitalisation trend, PES are exploring how AI and advanced analytics can be used to enhance their tools, services and processes and, ultimately, help jobseekers find work more quickly, or find better work (OECD, 2022[52]). Combining PES administrative data, along with broader data, the application of AI can assist the provision of many areas of PES activity (Figure 3.3).

Figure 3.3. AI presents various opportunities and challenges for PES

Note: AI – artificial intelligence, ALMP – active labour market policy, PES – public (and private) employment services.

While many opportunities exist for PES in adopting AI, the territory also comes with challenges. PES must therefore take additional steps to ensure that AI tools perform well and that their intended benefits are realised. First, monitoring and evaluation of AI-powered tools should be imbedded into their design and implementation. This can include experimentation, testing and piloting in the development phase, close monitoring (including user feedback) and ongoing fine‑tuning upon rollout and counterfactual impact evaluations (or process evaluations where appropriate) to understand their true impact. PES staff should also be supported through this journey, with ongoing training sessions, the provision of guidelines and informational materials, or dedicated support staff or units. Policy makers must also ensure that the development and use of AI in PES adheres to ethical standards. For example, the French PES has recently implemented a charter for the ethical use of AI. The OECD is undertaking further work in this area in order to better understand levels of AI adoption across PES and the associated development practices and governance approaches.

Source: OECD (2022[52]), Harnessing digitalisation in Public Employment Services to connect people with jobs, https://www.oecd.org/els/emp/Harnessing_digitalisation_in_Public_Employment_Services_to_connect_people_with_jobs.pdfhttps://oe.cd/digitalPES; Pôle Emploi (2022[53]), Pôle emploi se dote d’une charte pour une utilisation éthique de l’intelligence artificielle, https://www.pole-emploi.org/accueil/communiques/pole-emploi-se-dote-dune-charte-pour-une-utilisation-ethique-de-lintelligence-artificielle.html?type=article.

Advances in artificial intelligence only account for a small part of automation

The indicators of AI exposure discussed in this chapter, and used by many authors to estimate the effect of AI on employment, measure progress in the capabilities of AI as related to the abilities needed in occupations. However, progress in the capabilities of AI is not equivalent to the probability of automation. Recent progress in AI may complement human labour rather than automate it. More importantly, AI is just one of the many advanced technologies (ICT, robotics etc.) which can lead to the automation of tasks previously done by human labour. Aggregate changes in employment will ultimately depend on all sources of automation, and the predicted effect of AI on certain groups may be very different when one does not carefully consider all sources of automation.

To account for the latest progress in automation technologies, a new study by the OECD conducted in 2021 reassesses occupations’ exposure to automation exploiting novel data collected through an original survey on the degree of automatability of approximately 100 skills and abilities (Lassébie and Quintini, 2022[22]). The survey was developed with the help of, and completed by, experts from different AI research fields. The study does not only focus on AI technologies but extends to other automation technologies – e.g. robotics – now enhanced with AI.23 This allows different technologies to complement each other.

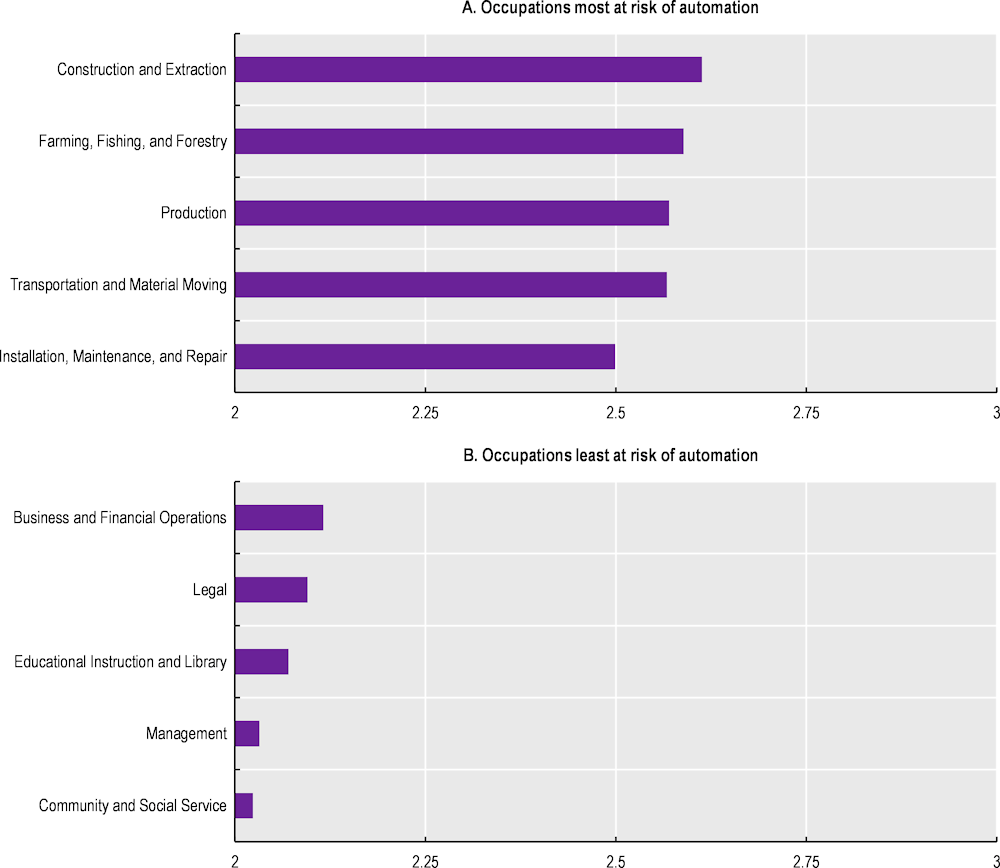

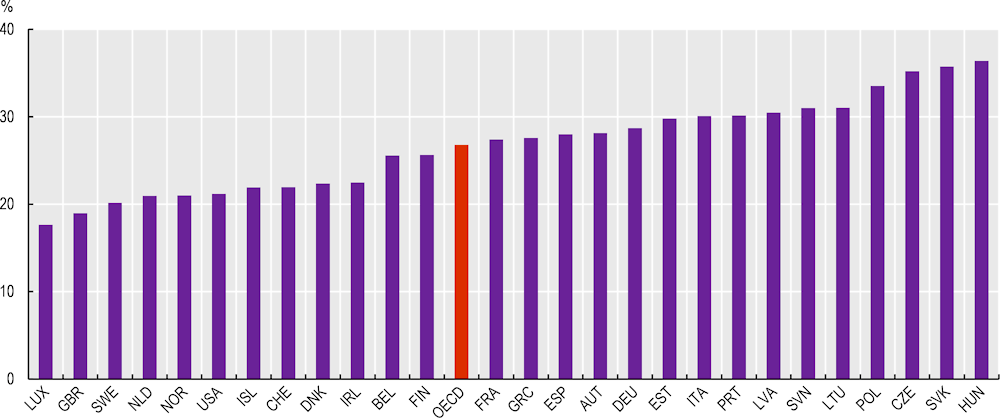

The study finds that high-skill occupations have the lowest risk of automation. Although AI has made several skills required in high-skilled jobs susceptible to automation, many other skills in those jobs remain bottlenecks to automation. The net effect is that high-skill occupations, although more exposed to recent progress in AI, are still some of the least at risk of automation. Low- and middle‑skilled jobs are the most at-risk including construction and extraction, farming, fishing, and forestry, and to a lesser extent production and transportation occupations. The least at-risk jobs include management, and community and social service occupations (Figure 3.4).

On average across OECD countries in the sample, the occupations at the highest risk of automation account for 27% of employment (Figure 3.5).24 Luxembourg, the United Kingdom and Sweden have the lowest shares of employment in the occupations at the highest risk of automation while Hungary, the Slovak Republic and the Czech Republic have highest shares

The creation of new tasks and jobs is not well captured by studies focusing only on exposure

Studies that focus on the effect of AI exposure on employment while trying to isolate the displacement and productivity effects will miss the creation of new tasks and jobs. AI exposure measures the overlap between the tasks performed in a job and the tasks which AI is theoretically capable of performing. It is much more difficult to predict what types of new tasks AI will create. New research from Autor et al. (2022[15]) find that the majority of current employment in the United States is in new job specialties introduced after 1940. The authors link these new job specialities to the introduction of new processes, products and industries.

In the case of AI, many of these new jobs will likely be created for workers with AI skills, or skills to exploit/work with AI. These are generally high-skill workers such as statisticians and software engineers who have the skills to develop, maintain and improve AI systems. Demand for workers with AI skills has grown briskly in the last decade (see Chapter 5). Strong demand for workers with complementary skills to AI, for example, high-skill workers with strong computer skills, have also seen increased demand.25 This channel will be picked up by aggregate studies but can often not be addressed by studies focused on particular industries.

Figure 3.4. The occupations most at risk of automation are quite different from occupations most exposed to artificial intelligence

Occupations most and least at risk of automation including AI and other automation technologies, 2021

Notes: Occupations are SOC‑2 digit (2018). The results are based on a survey of experts who evaluated the degree of automatability for 98 skills and abilities. The risk of automation measure is then computed by occupation as the average rating for each skill or ability used in the occupation across all expert responses weighted by the skills or abilities’ importance in the occupation as rated by O*NET. Scale is 0‑5 for all occupations.

Source: Reproduced from Lassébie and Quintini (2022[22]), “What skills and abilities can automation technologies replicate and what does it mean for workers?: New evidence”, https://doi.org/10.1787/646aad77-en, based on OECD Expert Survey on Skills and Abilities Automatability and O*NET.

Figure 3.5. Countries with higher shares of manufacturing employment and routine tasks are still more at risk of automation

Share of employment in occupations at the highest risk of automation by country, 2019

Notes: The SOC 3-digit occupations at highest risk of automation (top quartile). The results are based on a survey of experts who evaluated the degree of automatability for 98 skills and abilities. The risk of automation measure is then computed by occupation as the average rating for each skill or ability used in the occupation across all expert responses weighted by the skills or abilities’ importance in the occupation as rated by O*NET.

Source: Lassébie and Quintini (2022[22]), “What skills and abilities can automation technologies replicate and what does it mean for workers?: New evidence”, https://doi.org/10.1787/646aad77-en, based on OECD Expert Survey on Skills and Abilities Automatability and O*NET.

The strong demand for workers with AI skills, but otherwise negligible aggregate employment changes, is characteristic of the dynamics of the introduction of new automation technologies. Writing about general purpose technologies in general, and AI in particular, Brynjolfsson, Rock and Syverson (2019[54]; 2021[55]) argue that firms need time to restructure and adapt to new technologies before harnessing their full potential. Specifically, firms will spend heavily in the early adoption period on complementary investments including workers with AI skills, and other workers such as managers and computer engineers. These early intangible investments are unlikely to produce immediate productivity gains (see Chapter 4), and by extension employment changes, as firms continue to try new production processes and discover how best to deploy AI. Over time, however, these intangible investments will begin to take off, leading to a productivity “J-Curve” with initial declines in productivity as firms add complementary capital and labour followed by fast growth once they have pieced together how to use the new technology. The evidence of the employment effects of AI is consistent with this theory.

3.3. Policy can promote AI use that complements human labour and broadly shared productivity gains

There is a suite of policies that could help maximise AI’s impact on economic growth, while minimising job displacement. Policy should encourage the productivity and reinstatement effects of AI keeping in mind that the various effects depend on how the technology is used. For example, in many places the methods used by the teaching profession have not fundamentally changed over the past 200 years, so one could conceive of AI systems that could take over the tasks of some teachers. However, another approach would be to use AI to understand the different ways students learn, and then tailor teaching to their individual needs. If the latter were effective, it would not only raise student achievement, but it could also raise demand for teachers who would then specialise in different types of learning – see also Acemoglu and Restrepo (2019[56]) and Chapter 5.

Policy makers should review skills policies to ensure that workers can complement emerging AI systems. This chapter has documented a rise in demand for workers with computer, programming and data skills that are complementary to AI. Chapter 5 discusses the general increase in the demand for workers with AI skills as well as the skills that best complement AI, and it explores how adult learning systems should be adapted in response.

The tax system may also work against workers and favour excessive AI adoption. Many economies subsidise capital through the tax code while at the same time taxing labour at much higher rates. At the margin, this pushes firms to automate, but in such cases, automation would not be worthwhile without the implicit tax subsidy, and such marginal investments result only in small cost savings and a low productivity effect, which ultimately lowers labour demand. In short, employment is not reduced by large and truly innovative automation events but by the replacement of a small number of low value‑added tasks. Rebalancing capital and labour taxes away from marginal investments may halt excessive automation (Acemoglu, Manera and Restrepo, 2020[57]).

Tight labour markets can further ensure that automation produces the largest productivity effects. The cost savings from automation are greatest when unemployment is low and wages are high (Acemoglu and Restrepo, 2019[58]). Low unemployment should also increase the demand for, and speed of development of, new technologies. When unemployment is low and firms must compete for scarce workers, they have additional incentives to adopt new technologies and demand new innovations (Dechezleprêtre et al., 2021[59]). Policies to reach full employment may have the added benefit of helping automation technologies translate into higher productivity gains and stronger labour demand, although such a policy goal is not without risks (see Chapter 1).

Antitrust regulation can bolster the benefits of AI. One would like to ensure that automation from AI results in large cost savings which can then be passed through to the wider economy in the form of higher demand (Acemoglu and Restrepo, 2019[56]; Acemoglu, 2021[60]). Competition authorities can ensure that markets are competitive and cost savings from automation translate into lower prices and higher output (OECD, 2018[61]). Regulatory policy for AI is not confined to competition policy, however. A well-co‑ordinated combination of soft law and legislation is needed to effectively ensure trustworthy AI in the workplace as AI continues to evolve (see Chapter 6).

Finally, some share of the cost reductions from AI will ultimately be retained inside the firm. Policies to empower social partners and strengthen worker bargaining power can ensure that the gains from these savings are shared with incumbent workers rather than just benefiting owners. In addition, social partners can facilitate the retention of workers whose jobs are at risk of automation by ensuring that they are kept on in different roles – see Chapter 7 for a detailed discussion of the role of social partners in the deployment and use of AI.

References

[60] Acemoglu, D. (2021), Harms of AI, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w29247.

[40] Acemoglu, D. et al. (2022), Automation and the Workforce: A Firm-Level View from the 2019 Annual Business Survey, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w30659.

[62] Acemoglu, D. and D. Autor (2011), “Skills, Tasks and Technologies: Implications for Employment and Earnings”, in Handbook of Labor Economics, Elsevier, https://doi.org/10.1016/s0169-7218(11)02410-5.

[16] Acemoglu, D. et al. (2022), “Artificial Intelligence and Jobs: Evidence from Online Vacancies”, Journal of Labor Economics, Vol. 40/S1, pp. S293-S340, https://doi.org/10.1086/718327.

[57] Acemoglu, D., A. Manera and P. Restrepo (2020), “Does the US tax code favor automation?”, Brookings Papers on Economic Activity, Vol. Spring, pp. 231-300, https://www.brookings.edu/bpea-articles/does-the-u-s-tax-code-favor-automation/ (accessed on 26 January 2023).

[58] Acemoglu, D. and P. Restrepo (2019), “Automation and New Tasks: How Technology Displaces and Reinstates Labor”, Journal of Economic Perspectives, Vol. 33/2, pp. 3-30, https://doi.org/10.1257/jep.33.2.3.

[56] Acemoglu, D. and P. Restrepo (2019), “The wrong kind of AI? Artificial intelligence and the future of labour demand”, Cambridge Journal of Regions, Economy and Society, Vol. 13/1, pp. 25-35, https://doi.org/10.1093/cjres/rsz022.

[14] Acemoglu, D. and P. Restrepo (2018), “The Race between Man and Machine: Implications of Technology for Growth, Factor Shares, and Employment”, American Economic Review, Vol. 108/6, pp. 1488-1542, https://doi.org/10.1257/aer.20160696.

[1] Agrawal, A., J. Gans and A. Goldfarb (2019), “Introduction to “The Economics of Artificial Intelligence: An Agenda””, in Agrawal, A., J. Gans and A. Goldfarb (eds.), The Economics of Artificial Intelligence: An Agenda, University of Chicago Press, http://www.nber.org/books/agra-1 (accessed on 27 September 2022).

[9] Agrawal, A., J. Gans and A. Goldfarb (2019), “Prediction, Judgment, and Complexity: A Theory of Decision-Making and Artificial Intelligence”, in Agrawal, A., J. Gans and A. Goldfarb (eds.), The Economics of Artificial Intelligence: An Agenda, University of Chicago Press, http://www.nber.org/chapters/c14010 (accessed on 27 September 2022).

[29] Alekseeva, L. et al. (2021), “The demand for AI skills in the labor market”, Labour Economics, Vol. 71, p. 102002, https://doi.org/10.1016/j.labeco.2021.102002.

[5] Autor, D. (2015), “Why Are There Still So Many Jobs? The History and Future of Workplace Automation”, Journal of Economic Perspectives, Vol. 29/3, pp. 3-30, https://doi.org/10.1257/jep.29.3.3.

[15] Autor, D. et al. (2022), New Frontiers: The Origins and Content of New Work, 1940–2018, National Bureau of Economic Research, Cambridge, MA, https://doi.org/10.3386/w30389.

[12] Autor, D., F. Levy and R. Murnane (2003), “The Skill Content of Recent Technological Change: An Empirical Exploration”, The Quarterly Journal of Economics, Vol. 118/4, pp. 1279-1334, https://economics.mit.edu/files/11574 (accessed on 8 December 2017).

[63] Bessen, J. (2019), “Automation and jobs: when technology boosts employment*”, Economic Policy, Vol. 34/100, pp. 589-626, https://doi.org/10.1093/epolic/eiaa001.

[42] Bessen, J. et al. (2018), “The Business of AI Startups”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3293275.

[49] Blanchard, O. et al. (1989), “The Beveridge Curve”, Brookings Papers on Economic Activity, Vol. 1989/1, p. 1, https://doi.org/10.2307/2534495.

[3] Bresnahan, T. and M. Trajtenberg (1995), “General purpose technologies ‘Engines of growth’?”, Journal of Econometrics, Vol. 65/1, pp. 83-108, https://doi.org/10.1016/0304-4076(94)01598-t.

[36] Briggs, J. and D. Kodnani (2023), The Potentially Large Effects of Artificial Intelligence on Economic Growth, Goldman Sachs Economics Research, https://www.gspublishing.com/content/research/en/reports/2023/03/27/d64e052b-0f6e-45d7-967b-d7be35fabd16.html.

[51] Broecke, S. (2023), “Artificial intelligence and labour market matching”, OECD Social, Employment and Migration Working Papers, No. 284, OECD Publishing, Paris, https://doi.org/10.1787/2b440821-en.

[18] Brynjolfsson, E., T. Mitchell and D. Rock (2018), “What Can Machines Learn and What Does It Mean for Occupations and the Economy?”, AEA Papers and Proceedings, Vol. 108, pp. 43-47, https://doi.org/10.1257/pandp.20181019.

[55] Brynjolfsson, E., D. Rock and C. Syverson (2021), “The Productivity J-Curve: How Intangibles Complement General Purpose Technologies”, American Economic Journal: Macroeconomics, Vol. 13/1, pp. 333-372, https://doi.org/10.1257/mac.20180386.

[54] Brynjolfsson, E., D. Rock and C. Syverson (2019), “Artificial Intelligence and the Modern Productivity Paradox: A Clash of Expectations and Statistics”, in Agrawal, A., J. Joshua Gans and A. Goldfarb (eds.), The Economics of Artificial Intelligence: An Agenda, University of Chicago Press, Chicago, http://www.nber.org/chapters/c14007.

[66] Calvino, F. and L. Fontanelli (2023), “A portrait of AI adopters across countries: Firm characteristics, assets’ complementarities and productivity”, OECD Science, Technology and Industry Working Papers, No. 2023/02, OECD Publishing, Paris, https://doi.org/10.1787/0fb79bb9-en.

[31] Calvino, F. et al. (2022), “Identifying and characterising AI adopters: A novel approach based on big data”, OECD Science, Technology and Industry Working Papers, No. 2022/06, OECD Publishing, Paris, https://doi.org/10.1787/154981d7-en.

[27] Cedefop (2013), Quantifying skill needs in Europe – Occupational skills profiles: methodology and application, Cedefop, https://data.europa.eu/doi/10.2801/13390.

[59] Dechezleprêtre, A. et al. (2021), “Induced Automation: Evidence from Firm-level Patent Data”, Working Paper Series, No. 384, University of Zurich, Department of Economics.

[28] Deming, D. (2017), “The Growing Importance of Social Skills in the Labor Market*”, The Quarterly Journal of Economics, Vol. 132/4, pp. 1593-1640, https://doi.org/10.1093/qje/qjx022.

[35] Eloundou, T. et al. (2023), “GPTs are GPTs: An Early Look at the Labor Market Impact Potential of Large Language Models”, https://arxiv.org/abs/2303.10130v4.

[44] Eurostat (2021), Community survey on ICT usage and e-commerce in enterprises, https://ec.europa.eu/eurostat/web/products-eurostat-news/-/ddn-20210413-1 (accessed on 19 January 2023).

[47] Farber, H. (2017), “Employment, Hours, and Earnings Consequences of Job Loss: US Evidence from the Displaced Workers Survey”, Journal of Labor Economics, Vol. 35/S1, pp. S235-S272, https://doi.org/10.1086/692353.

[34] Felten, E., M. Raj and R. Seamans (2023), “How will Language Modelers like ChatGPT Affect Occupations and Industries?”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.4375268.

[21] Felten, E., M. Raj and R. Seamans (2021), “Occupational, industry, and geographic exposure to artificial intelligence: A novel dataset and its potential uses”, Strategic Management Journal, Vol. 42/12, pp. 2195-2217, https://doi.org/10.1002/smj.3286.

[23] Felten, E., M. Raj and R. Seamans (2019), “The Variable Impact of Artificial Intelligence on Labor: The Role of Complementary Skills and Technologies”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3368605.

[37] Fossen, F. and A. Sorgner (2022), “New digital technologies and heterogeneous wage and employment dynamics in the United States: Evidence from individual-level data”, Technological Forecasting and Social Change, Vol. 175, p. 121381, https://doi.org/10.1016/j.techfore.2021.121381.

[24] Georgieff, A. and R. Hyee (2021), “Artificial intelligence and employment: New cross-country evidence”, OECD Social, Employment and Migration Working Papers, No. 265, OECD Publishing, Paris, https://doi.org/10.1787/c2c1d276-en.

[65] Georgieff, A. and A. Milanez (2021), “What happened to jobs at high risk of automation?”, OECD Social, Employment and Migration Working Papers, No. 255, OECD Publishing, Paris, https://doi.org/10.1787/10bc97f4-en.

[33] Green, A. and L. Lamby (2023), “The supply, demand and characteristics of the AI workforce across OECD countries”, OECD Social, Employment and Migration Working Papers, No. 287, OECD Publishing, Paris, https://doi.org/10.1787/bb17314a-en.

[41] Grennan, J. and R. Michaely (2020), “Artificial Intelligence and High-Skilled Work: Evidence from Analysts”, SSRN Electronic Journal, https://doi.org/10.2139/ssrn.3681574.

[26] Handel, M. (2012), “Trends in Job Skill Demands in OECD Countries”, OECD Social, Employment and Migration Working Papers, No. 143, OECD Publishing, Paris, https://doi.org/10.1787/5k8zk8pcq6td-en.

[38] Hunt, W., S. Sarkar and C. Warhurst (2022), “Measuring the impact of AI on jobs at the organization level: Lessons from a survey of UK business leaders”, Research Policy, Vol. 51/2, p. 104425, https://doi.org/10.1016/j.respol.2021.104425.

[46] Jacobson, L., R. LaLonde and D. Sullivan (1993), “Earnings Losses of Displaced Workers”, The American Economic Review, Vol. 83/4, pp. 685-709, http://www.jstor.org/stable/2117574.

[64] Krueger, D. (ed.) (2021), “Quasi-Experimental Shift-Share Research Designs”, The Review of Economic Studies, Vol. 89/1, pp. 181-213, https://doi.org/10.1093/restud/rdab030.

[4] Lane, M. and A. Saint-Martin (2021), “The impact of Artificial Intelligence on the labour market: What do we know so far?”, OECD Social, Employment and Migration Working Papers, No. 256, OECD Publishing, Paris, https://doi.org/10.1787/7c895724-en.

[39] Lane, M., M. Williams and S. Broecke (2023), “The impact of AI on the workplace: Main findings from the OECD AI surveys of employers and workers”, OECD Social, Employment and Migration Working Papers, No. 288, OECD Publishing, Paris, https://doi.org/10.1787/ea0a0fe1-en.

[22] Lassébie, J. and G. Quintini (2022), “What skills and abilities can automation technologies replicate and what does it mean for workers?: New evidence”, OECD Social, Employment and Migration Working Papers, No. 282, OECD Publishing, Paris, https://doi.org/10.1787/646aad77-en.

[32] Manca, F. (2023), “Six questions about the demand for artificial intelligence skills in labour markets”, OECD Social, Employment and Migration Working Papers, No. 286, OECD Publishing, Paris, https://doi.org/10.1787/ac1bebf0-en.

[43] Milanez, A. (2023), “The impact of AI on the workplace: Evidence from OECD case studies of AI implementation”, OECD Social, Employment and Migration Working Papers, No. 289, OECD Publishing, Paris, https://doi.org/10.1787/2247ce58-en.

[50] Mortensen, D. and C. Pissarides (1999), “Chapter 39 New developments in models of search in the labor market”, in Handbook of Labor Economics, Elsevier, https://doi.org/10.1016/s1573-4463(99)30025-0.

[10] Nordhaus, W. (2021), “Are We Approaching an Economic Singularity? Information Technology and the Future of Economic Growth”, American Economic Journal: Macroeconomics, Vol. 13/1, pp. 299-332, https://doi.org/10.1257/mac.20170105.

[17] O*NET (2023), Speed of Closure, O*NET OnLine, https://www.onetonline.org/find/descriptor/result/1.A.1.e.1 (accessed on 21 February 2023).

[52] OECD (2022), “Harnessing digitalisation in Public Employment Services to connect people with jobs”, OECD, Paris, https://www.oecd.org/els/emp/Harnessing_digitalisation_in_Public_Employment_Services_to_connect_people_with_jobs.pdf.

[45] OECD (2020), “What is happening to middle-skill workers?”, in OECD Employment Outlook 2020: Worker Security and the COVID-19 Crisis, OECD Publishing, Paris, https://doi.org/10.1787/c9d28c24-en.

[8] OECD (2019), Artificial Intelligence in Society, OECD Publishing, Paris, https://doi.org/10.1787/eedfee77-en.

[2] OECD (2019), “Executive summary”, in Artificial Intelligence in Society, OECD Publishing, Paris, https://doi.org/10.1787/f169ea9d-en.

[7] OECD (2019), “Overview: The future of work is in our hands”, in OECD Employment Outlook 2019: The Future of Work, OECD Publishing, Paris, https://doi.org/10.1787/e4718721-en.

[6] OECD (2019), “The future of work: What do we know?”, in OECD Employment Outlook 2019: The Future of Work, OECD Publishing, Paris, https://doi.org/10.1787/ef00d169-en.

[48] OECD (2018), “Back to work: Lessons from nine country case studies of policies to assist displaced workers”, in OECD Employment Outlook 2018, OECD Publishing, Paris, https://doi.org/10.1787/empl_outlook-2018-8-en.

[61] OECD (2018), Market Concentration: Issues Paper by the Secretariat, OECD, Paris, https://www.oecd.org/daf/competition/market-concentration.htm.

[13] OECD (2017), “How technology and globalisation are transforming the labour market”, in OECD Employment Outlook 2017, OECD Publishing, Paris, https://doi.org/10.1787/empl_outlook-2017-7-en.

[53] Pôle Emploi (2022), Pôle emploi se dote d’une charte pour une utilisation éthique de l’intelligence artificielle, https://www.pole-emploi.org/accueil/communiques/pole-emploi-se-dote-dune-charte-pour-une-utilisation-ethique-de-lintelligence-artificielle.html?type=article.

[30] Squicciarini, M. and H. Nachtigall (2021), “Demand for AI skills in jobs: Evidence from online job postings”, OECD Science, Technology and Industry Working Papers, No. 2021/03, OECD Publishing, Paris, https://doi.org/10.1787/3ed32d94-en.

[11] Susskind, D. (2022), “Technological Unemployment”, in The Oxford Handbook of AI Governance, Oxford University Press, https://doi.org/10.1093/oxfordhb/9780197579329.013.42.

[20] Tolan, S. et al. (2021), “Measuring the Occupational Impact of AI: Tasks, Cognitive Abilities and AI Benchmarks”, Journal of Artificial Intelligence Research, Vol. 71, pp. 191-236, https://doi.org/10.1613/jair.1.12647.

[25] Tsacoumis, S., S. Willison and L. Wasko (2010), O*NET Analyst Occupational Skills Ratings: Cycles 1 - 10 Results, Human Resources Research Organization, Alexandria, VA, https://www.onetcenter.org/dl_files/AOSkills_10.pdf (accessed on 3 February 2023).

[19] Webb, M. (2020), “The Impact of Artificial Intelligence on the Labor Market”, Stanford University, https://www.michaelwebb.co/webb_ai.pdf.

Notes

← 1. The task-based framework discussed in this section follows Acemoglu and Restrepo (2018[14]). See Acemoglu and Autor (2011[62]) for an earlier sketch of the theory of automation and Acemoglu and Restrepo (2019[58]) for a non-technical overview.

← 2. Following Acemoglu and Restrepo (2018[14]), the discussion assumes full substitution between AI and labour (the elasticity of substitution in a CES production function is infinity, ), however everything that follows holds if one assumes partial substitution in tasks so long as AI and labour have some degree of substitution (.

← 3. Workers are assumed to have an absolute and comparative advantage in completing these tasks over automation technologies.

← 4. The explanation in this chapter follows the case of Acemoglu and Restrepo (2018[14]) where firms are “technologically constrained” such that given prices for labour and capital, firms would like to automate a set of tasks up to a threshold , but due to existing technologies they are constrained to only automate tasks.

← 5. This is the case of AI acting as a labour-augmenting productivity increase, and it is usually what one refers to as technology acting as a complement to labour. For a long time, this was the main mechanism for how economists theorised technological change affected labour demand (along with the elasticity of substitution). However, it lacks realism – the task content of labour never changes. Moreover, it implies that in almost all cases labour demand should never decline and wages should always rise with new technological improvements (Acemoglu and Restrepo, 2019[58]). For these reasons, this channel, while certainly present in some cases, is not the emphasis of this chapter.

← 6. AI is intensive in electricity and data. If the firm operating the warehouse invests heavily in AI, this may lead to higher demand for employment in electrical installation services and data storage which complement AI but are employed outside the warehousing firm.

← 7. Bessen (2019[63]) further argues that the elasticity of product demand is not constant over time and that initial price decreases due to artificial intelligence may spur a large productivity effect, but subsequent price reductions do little to increase demand and will then bring longer term employment declines.

← 8. The effects of AI on labour demand are much broader than questions of displacement, productivity and reinstatement effects, and encompass also cultural, legal, organisational and ethical considerations. For example, chief executives are one of the occupations most exposed to AI (see Section 3.1.3). However, for legal and ethical reasons it seems likely that firms will always need to have a human as the head of a firm regardless of how many of the tasks of a current CEO AI may be able to automate.

← 9. The reinstatement effect is thought to be small compared to the productivity and displacement effects, hence the emphasis on the latter two effects, but more research is needed (Acemoglu and Restrepo, 2019[56]).

← 10. The difference between routine and non-routine tasks is often not clear in practice. The work of farmworkers and bricklayers can be seen as adding up together a very large number of routine tasks, where their order is non-routine (and somewhat cognitive). AI, in fact, may be able to automate many of these tasks.

← 11. To give a sense of similar measures, Brynjolfsson, Mitchell and Rock (2018[18]) apply a rubric for evaluating task potential for machine learning to tasks in O*NET. Webb (2020[19]) measures AI progress from patents and connects this to O*NET as well.

← 12. The concern is that workers, aware of newly deployed AI, may decide to exit the firm whether they are at risk of automation or not. Any estimates of the effect of AI on employment, and especially the types of workers affected, will be contaminated with the effect of workers’ beliefs about AI, for example.

← 13. More specifically, the literature has used these exposure measures as “shift-share instruments” (Borusyak, Hull and Jaravel, 2021[64]) which posit that occupations’ or firms’ underlying task structures are uncorrelated with recent advances in AI and, therefore, provide more credible estimates of employment effects than simply regressing employment changes on AI adoption.

← 14. Calvino et al. (2022[31]) also combine job postings with other data sources that allow identifying different types of AI adopters, focusing on the United Kingdom. These include AI-related Intellectual Property Rights and information on AI-related activities mentioned on company websites.

← 15. See Georgieff and Hyee (2021[24]) for a thorough discussion of the relative merits of the various approaches to measuring AI exposure including which effects of AI on tasks each approach can recover.

← 16. Calvino and Fontanelli (2023[66]) is a recent exception. They use harmonised code to measure AI adoption on firm-level surveys from a subset of European countries.

← 17. The authors link O*NET abilities and PIAAC tasks manually by asking whether a given ability is indispensable for performing a given task. An O*NET ability can therefore be linked to several PIAAC tasks, and conversely, a given PIAAC task can be linked to several O*NET abilities. This link was made by the authors and, in case of diverging answers, agreement was reached through an iterative discussion and consensus method, similar to a Delphi method.

← 18. The researchers do this by excluding industries producing AI products (Information, and Professional and Business Services) as well as vacancies in the remaining industries demanding AI skills. Assuming the reinstatement effect can be proxied by workers with AI skills, they therefore plausibly exclude the reinstatement effect and focus only on whether increased AI exposure is dominated by the productivity or displacement effect.