Satoshi Araki

Sandrine Cazes

Andrea Garnero

Andrea Salvatori

Artificial Intelligence and the Labour Market

Satoshi Araki

Sandrine Cazes

Andrea Garnero

Andrea Salvatori

The recovery from the COVID‑19 pandemic lost momentum in 2022, with employment and unemployment stabilising. Labour markets remain tight, despite signs of easing. In this context, the quality of jobs on offer has improved in some dimensions, but real wages are falling significantly in almost all OECD countries despite a pick-up in nominal wage growth. In most countries, profits have grown robustly, often more than nominal wages. Nominal minimum wages are keeping pace with inflation, but any real gains may fade rapidly if inflation remains high. In contrast, wages negotiated in collective agreements between employers or employers’ organisations and trade unions are reacting with some delay even in countries where the majority of workers are covered by a collective agreement, although a catch-up phase is expected in the coming quarters.

Amid a cost-of-living crisis, the robust recovery from the COVID‑19 recession lost momentum since 2022. The energy shock caused by Russia’s war of aggression against Ukraine put a drag on global growth and contributed to propelling price inflation in many countries to levels not seen in decades. However, OECD labour markets have proved resilient. Employment and unemployment have held their ground, and the labour market remains tight in most countries, despite some signs of easing. The past quarters have shown signs of improvements, with global GDP growth picking up slightly.

The latest available evidence at the time of writing suggests that:

After stabilising in the second half of 2022, employment in the OECD area picked-up slightly in the first months of 2023. In May 2023, OECD-wide employment was about 3% higher than in December 2019. Unemployment rates across the OECD mostly remained below pre‑crisis levels. A recent pick-up in growth has led to an improvement of the economic projections for the near future, but GDP growth is likely to remain subdued in 2023 and 2024. Over the same period of time, OECD-wide employment is projected to continue to expand and the unemployment rate to increase slightly.

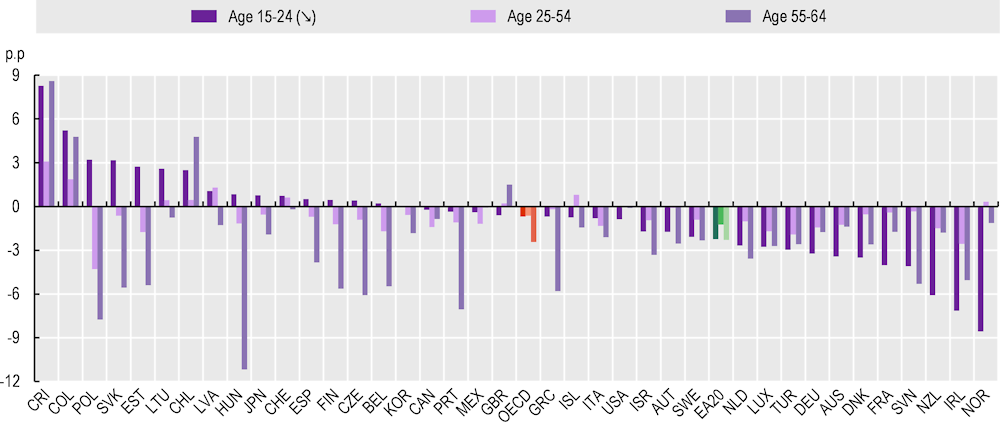

Inactivity rates have declined relative to the pre‑ COVID‑19 crisis in most countries. Early concerns that the pandemic might permanently increase inactivity rates have not come to pass, including among older adults. On average across all OECD countries, inactivity rates for 55 to 64 years old have decreased more than for the younger age groups. Inactivity rates for the whole working age population, however, are higher than before the crisis in seven OECD countries, with the largest increases found in Latin American member states.

Labour markets remain tight even as pressures are easing. Labour market tightness (i.e. the number of vacancies per unemployed person) eased in the second half of 2022 but remained well above pre‑crisis levels. Online job postings data for selected countries suggest that labour demand has continued to ease in the first half of 2023.

Amid tight labour markets, nominal wage growth has picked up and some non-monetary aspects of job quality have improved. In Q1 2023, nominal year-on-year wage growth exceeded its pre‑crisis level in nearly all OECD countries, reaching 5.6% on average across the 34 countries with available data. Among new hires, the share of temporary contracts and involuntary part-time has declined in most OECD countries. In addition, data on online job postings in Canada, the United Kingdom and the United States show an increase in the share of vacancies offering employee benefits, especially health-related benefits, retirement programs/schemes and paid time off.

As inflation reached levels not seen in decades in many countries, real hourly wages have fallen – often substantially – in virtually every industry and OECD country, contributing to the cost-of-living crisis. In Q1 2023, despite the pick-up in nominal wages, the difference between nominal annual wage growth and inflation was ‑3.8% on average across the 34 OECD countries with available data, with a negative difference observed in 30 countries. The loss of purchasing power is particularly challenging for workers in low-income households, who have less leeway to deal with increases in the cost of living through savings or borrowing and often face higher actual inflation rates because a higher proportion of their spending goes to energy and food.

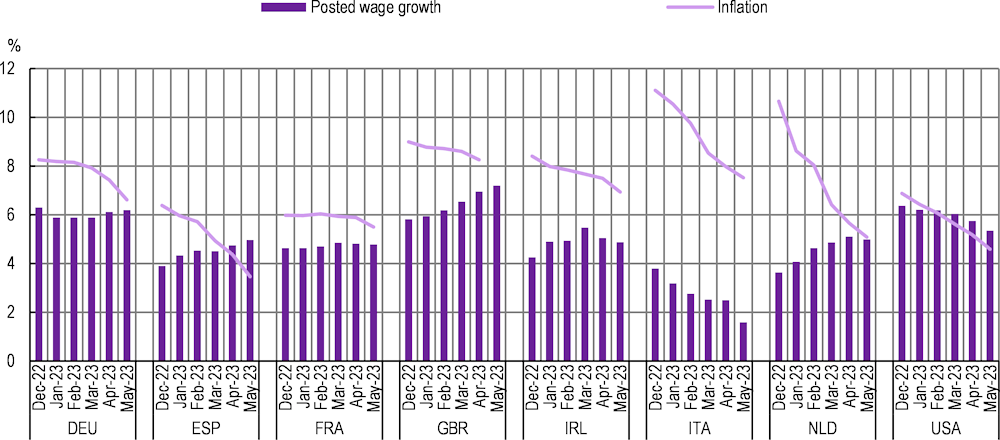

Nominal wage growth has not significantly accelerated in the first half of 2023, but the gap with declining inflation is narrowing in some countries. Recent wage data from five countries point to stable nominal wage growth in most in April and May 2023. Similarly, growth in wages posted on the online platform Indeed has been steady or declining in the first five months of 2023 in France, Germany, Ireland, Italy and the United States. In Spain, the Netherlands, and – more markedly – the United Kingdom nominal growth of posted wages has increased. In general, the gap between inflation and nominal wage growth in posted wages has become smaller. However, wages posted on Indeed have grown in real terms only in Spain and the United States in recent months.

In many countries, real wages are falling across all industries, but less so in low-pay industries. Among the 31 countries with available data, in Q1 2023, real wages in low-pay industries performed better than those in mid-pay industries in 18 countries, and better than those in high-pay industries in 22 countries. Real wages in low-pay industries had a worse performance than real wages in both mid- and high-pay industries only in six countries.

In most countries, profits have increased more than labour costs, making an unusually large contribution to domestic price pressures, and leading to a fall in the labour share. Data from Europe and Australia indicate that this has occurred not only in energy sectors, but also in other parts of the economy, including in accommodation and food and manufacturing. As economies re‑opened, pent-up demand and large recovery plans bolstered aggregate demand, helping profits grow quickly while supply bottlenecks limited the speed of adjustment of output. With strong consumer demand and rapidly evolving inflation driven by external factors, many producers were likely able to adjust prices quickly, while wage increases typically involve longer renegotiations periods.

Several policy levers can be activated to limit the impact of inflation on workers and ensure a fair sharing of the cost-of-living crisis between taxpayers (through government taxes), companies, and workers. The most direct way to help workers is via an increase in their wages. Wage setting institutions – including minimum wages and collective bargaining – can help mitigate losses in purchasing power and ensure a fair distribution of the cost of inflation between firms and workers, while avoiding a price‑wage spiral. The latest available evidence and information from a policy questionnaire addressed to Labour Ministries and social partners across OECD countries suggests that:

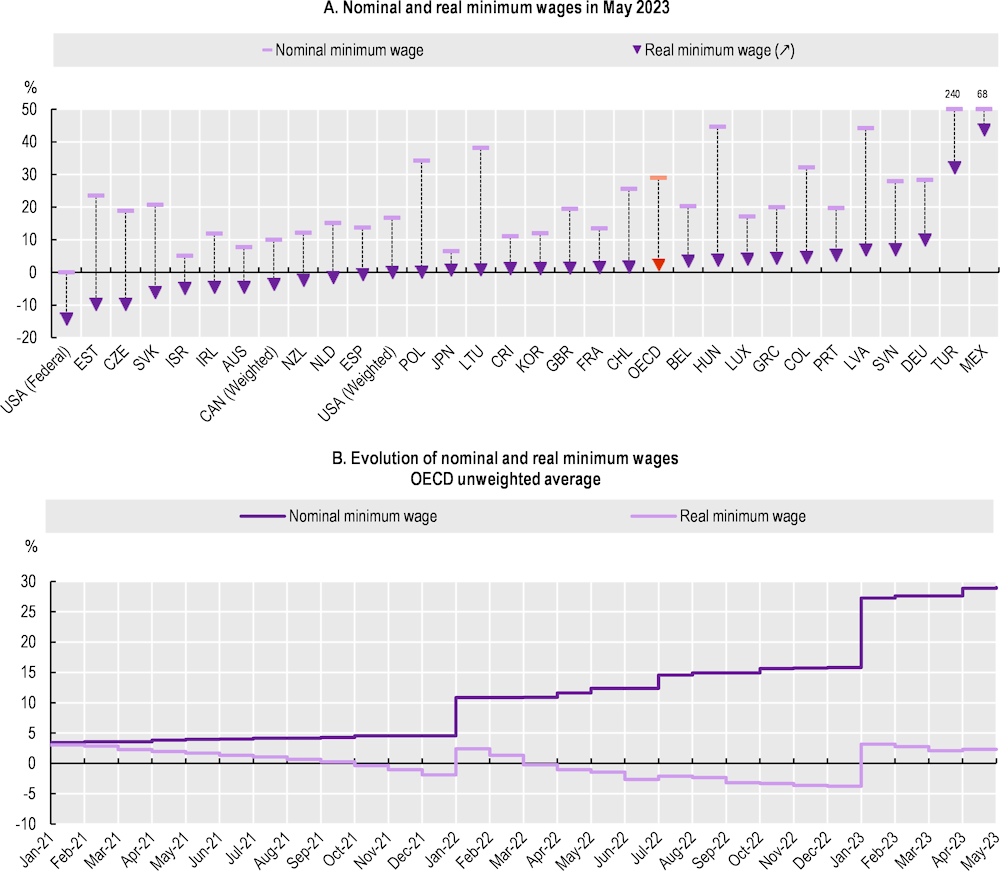

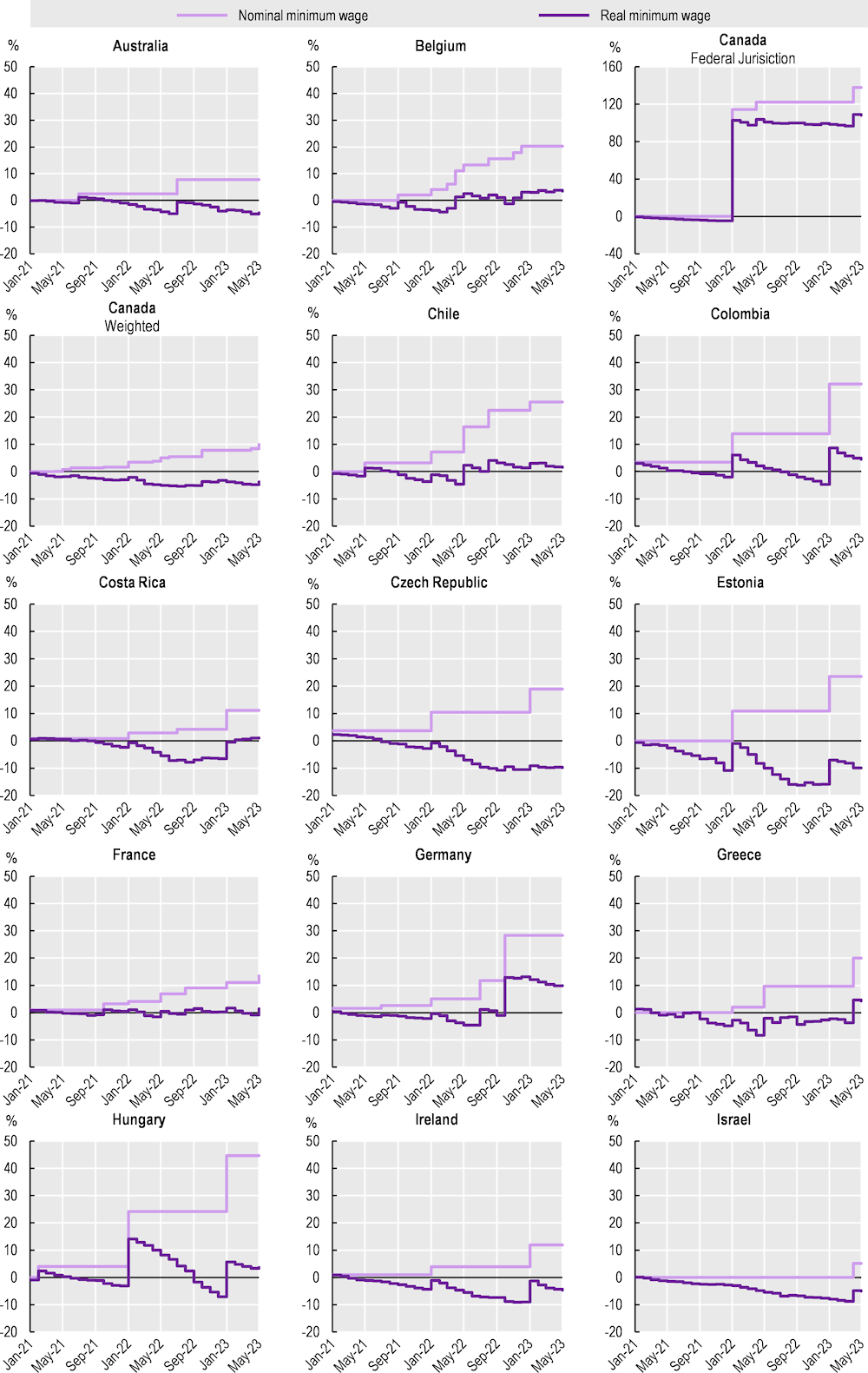

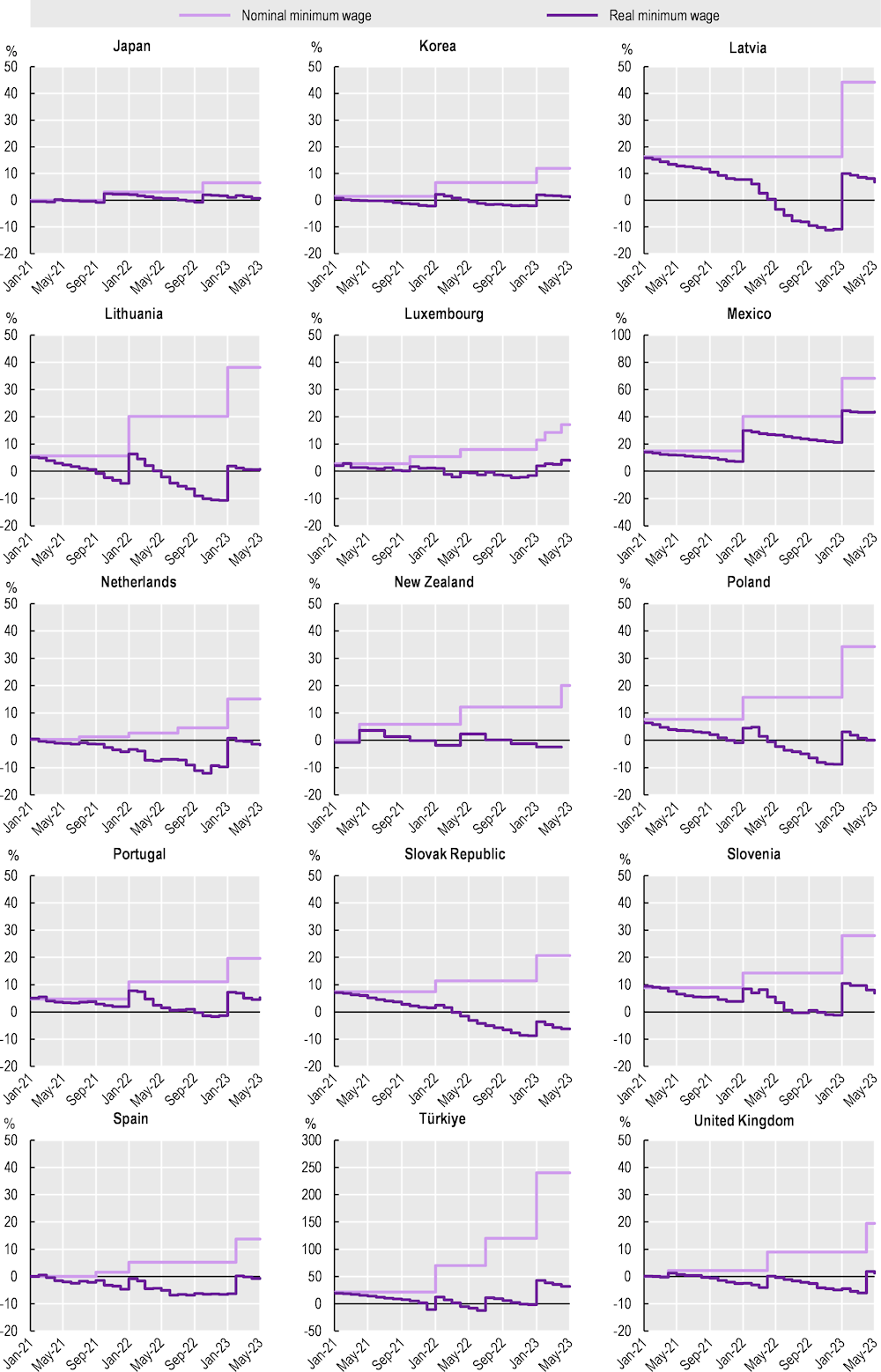

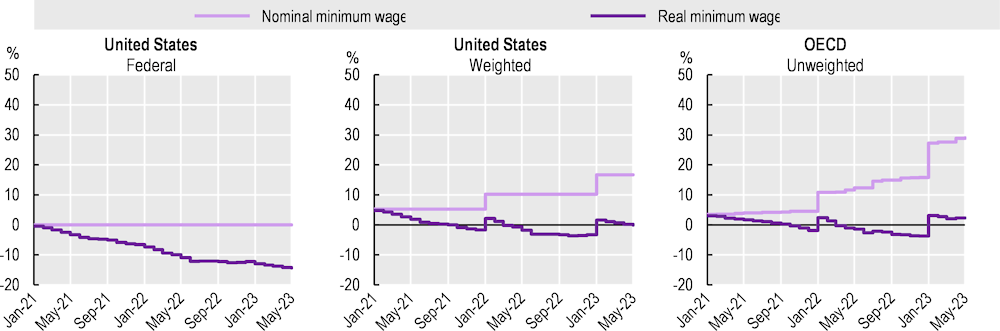

Between December 2020 and May 2023, on average across OECD countries, nominal statutory minimum wages have increased by 29%. This trend has allowed minimum wages to keep pace with inflation (prices increased by 24.6%, on average, over the same time period), even if real gains tend to be quickly eroded as inflation remains high. Going forward, it is important to ensure that statutory minimum wages continue to adjust regularly through the different national institutional settings and uprating mechanisms. There is a concern that increases in the minimum wage contribute to fuel inflation. However, the effect of minimum wage increase to the growth in aggregate wages is limited, even accounting for spillover effects on wages above the minimum.

In most OECD countries, increases in the minimum wage are the result of a discretionary policy decision that is typically taken once a year at most, while in six countries the national statutory minimum wage is automatically indexed to inflation. Automatic indexation helps to safeguard the purchasing power of minimum wage earners and improve the predictability of future increases. However, it also reduces the scope for governments, social partners or commissions to exercise judgement on future increases and could lead to an excessive compression of the wage distribution if other wages are not raised, with consequences both for individual careers, and for the design of redistribution policies.

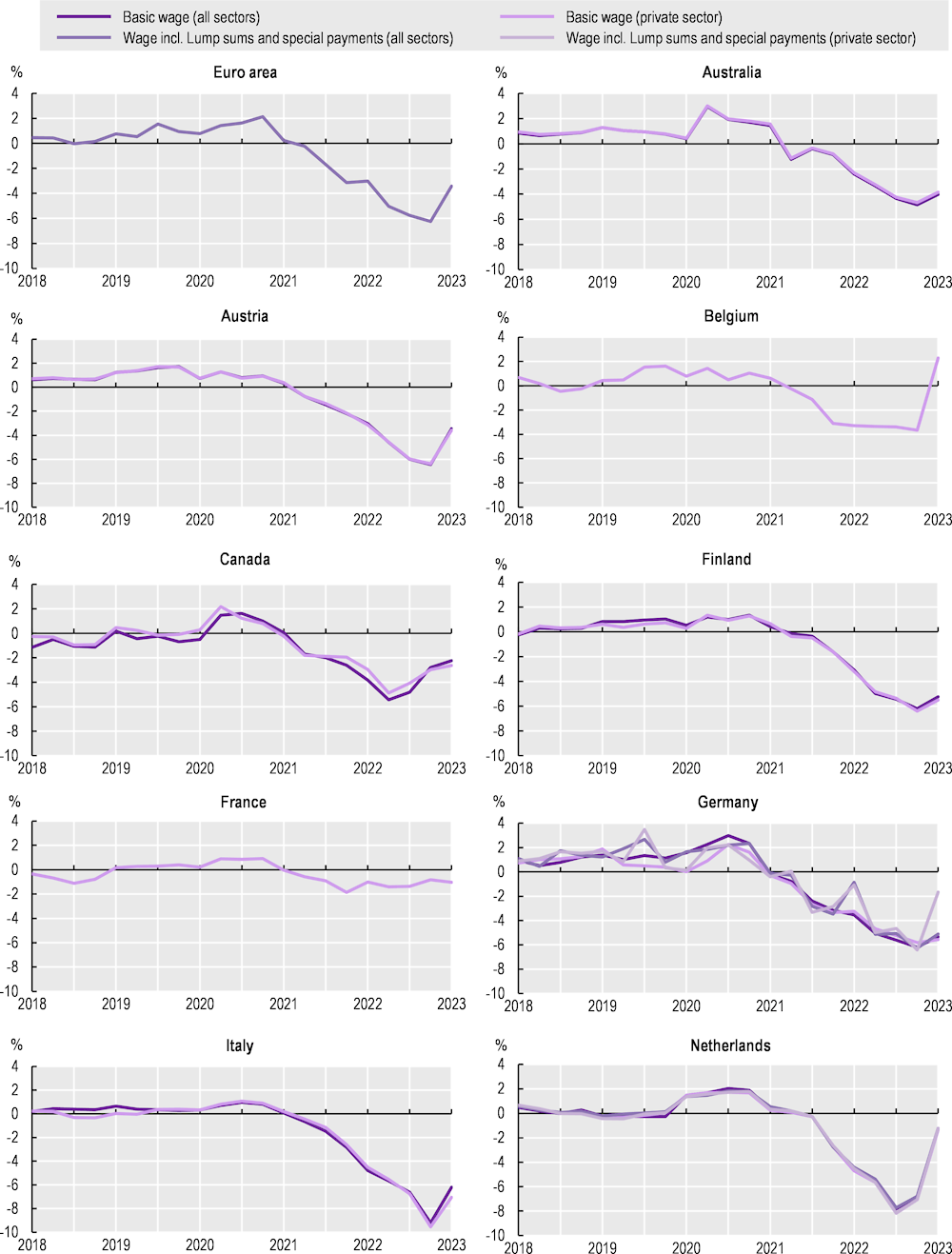

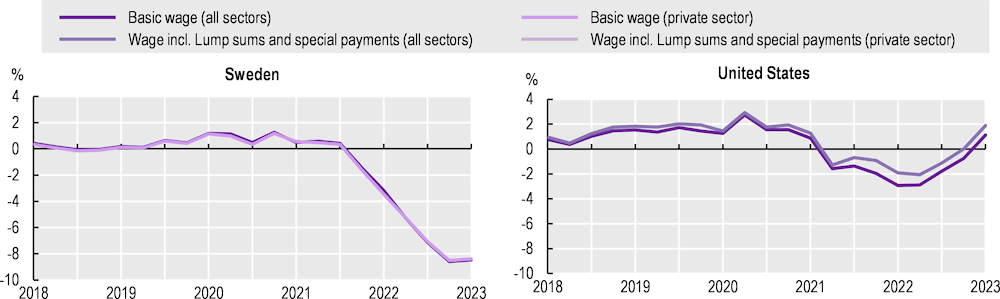

Wages negotiated in collective agreements between firms and workers have declined in real terms and are reacting with longer delays. Several factors can explain why negotiated wages, on average, have not managed to keep up with inflation. Most importantly, the staggered and rather infrequent nature of wage agreements means that negotiated wages rarely adjust immediately to unexpected price inflation. However, in some OECD countries, unions, employers’ organisations and governments have found innovative ways to cushion the effects of inflation while limiting the costs for firms by using tax-free lump-sum bonuses or non-wage benefits.

Faster growth in negotiated wages is likely in the coming quarters as the most recent bargaining rounds have tried to recoup some of the losses in purchasing power. However, the available evidence suggests that, after a catch-up phase, nominal negotiated wage growth are likely to go back to previous trends without generating a price‑wage spiral. Overall, aggregate nominal wage growth is projected to be just over 4% in the OECD area in 2023, before moderating to around 3.5% in 2024 while inflation is projected to be at 6.6% in 2023 and 4.3% in 2024.

Minimum wages and collective bargaining can help achieve a fair distribution of the cost of inflation between workers and employers, as well as across workers of different pay levels. A fair sharing of the cost of inflation can prevent further increases in inequality and support effective monetary policy by averting feedback loops between profits, wages and prices. The analysis of this chapter suggests that, in several sectors and countries, there is room for profits to absorb some further increases in wages to mitigate the loss of purchasing power at least for the low paid without generating significant additional price pressures. Given the downward rigidity of prices, the recent decline in input costs will also likely provide further room to absorb some wage increases without generating inflationary pressures. Collective bargaining can also help identify solutions tailored to firms’ varying ability to sustain increase in wages – for instance for small and medium firms that may face more significant constraints.

This chapter offers a detailed overview of recent labour market developments across the OECD countries with a particular focus on wage dynamics and discusses the policy measures that countries have at their disposal to help address the ongoing cost-of-living crisis, focusing on wage policies. This includes a discussion on the role that minimum wages and collective bargaining have played so far in cushioning the costs of inflation, drawing on a policy questionnaire that was addressed to OECD countries as well as employers’ organisations and trade unions through, respectively, the Business@OECD (BIAC) and the Trade Union Advisory Committee (TUAC) networks.

The chapter is organised as follows: Section 1.1 reviews recent labour market developments across the OECD; Section 1.2 reports on recent wage developments; and finally Section 1.3 discusses the role of statutory minimum wages and collective bargaining as a policy lever to support workers and ensure a fair burden-sharing of the cost of inflation among governments, firms and workers. Section 1.4 concludes with policy recommendations.

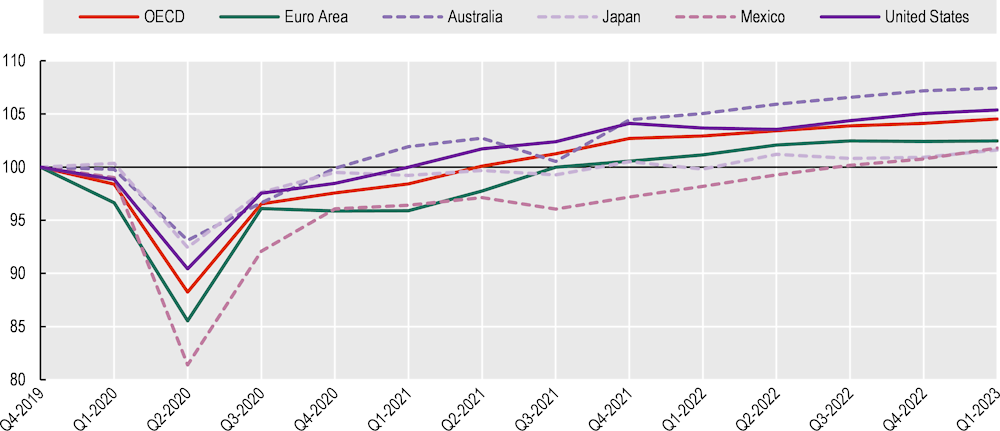

Growth across the OECD slowed substantially over the course of 2022, but there are signs of improvement in 2023 (Figure 1.1). Russia’s war of aggression against Ukraine pushed up prices substantially, especially for energy and food, adding to inflationary pressures at a time when the cost of living was already rising rapidly around the world. Inflation eroded household incomes and monetary policy tightened considerably amidst the unusually vigorous and widespread steps to raise policy interest rates by central banks in recent months (OECD, 2022[1]). By the fourth quarter of 2022, global growth had slowed to an annualised rate of just 2%, with growth over the year falling to 2.3%, just over half the pace seen through 2021. Output declined in 15 OECD economies in the fourth quarter, with most of these in Europe. The recent decline in energy prices and the improving prospects for China have contributed to an uptake in economic indicators in the first half of 2023, with global GDP growth picking up to an annualised rate of just over 3% in the first quarter, despite mixed outcomes across countries and particularly weak growth in the Euro Area (OECD, 2023[2]). In the first quarter of 2023, GDP for the OECD area stood 5% above its level at the end of 2019, after a year-on-year growth of 1.5% (Figure 1.1).

Real GDP indexed to 100 in Q4 2019, seasonally adjusted, selected OECD countries

Note: Euro Area refers to the averages of 20 Eurozone countries.

Source: OECD (2023), “Quarterly National Accounts”, OECD National Accounts Statistics (database), https://doi.org/10.1787/data-00017-en (accessed on 23 June 2023).

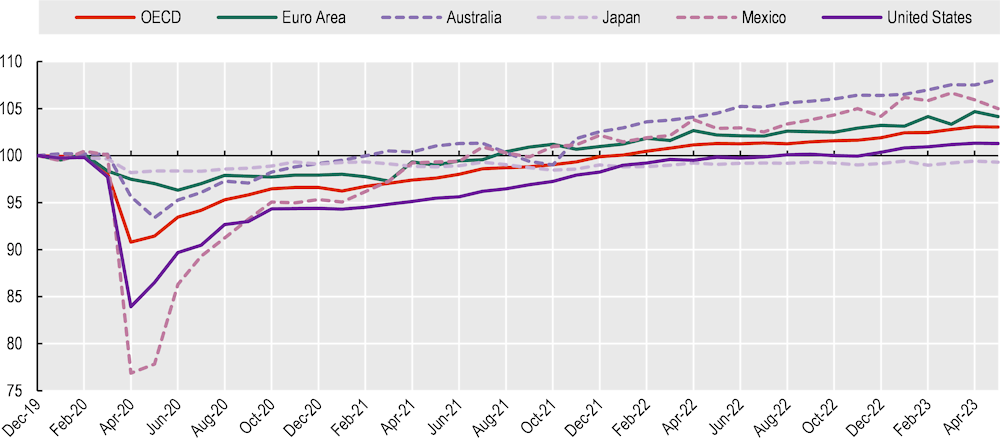

Amid the slowdown in economic growth, employment growth also lost momentum over the course of 2022 but continued to grow in the first months of 2023 (Figure 1.2). In May 2023, total employment for the OECD, was about 3% higher than in December 2019. Overall, employment growth since the start of the pandemic was slightly stronger for women than men (see Box 1.1). Employment rates across most OECD countries also stabilised above pre‑crisis levels by the first quarter of 2023 (Annex Figure 1.A.1).

Total employment indexed to 100 in December 2019, seasonally adjusted, selected OECD countries

Note: Euro Area refers to the averages of 20 Eurozone countries. The OECD average, the Euro Area and Mexico are derived from the OECD Monthly Unemployment Statistics estimated as the unemployment level times one minus the unemployment rate and rescaled on the LFS-based quarterly employment figures.

Source: OECD (2023), “Labour: Labour market statistics”, Main Economic Indicators (database), https://doi.org/10.1787/data-00046-en (accessed on 3 July 2023).

The initial labour market impact of the pandemic was stronger among women than men in most OECD countries, raising the concern that the pandemic-induced recession might be a “shecession” (OECD, 2020[3]). However, as economies reopened, in most OECD countries women benefitted more than men from the rebound in economic activity. Indeed, in early 2022 – two years after the onset of the pandemic – the employment rate gap between men and women had declined in most of the OECD countries relative to its pre‑pandemic level (Salvatori, 2022[4]).

Over the course of 2022 and the first half of 2023, employment levels for both women and men stabilised above pre‑pandemic levels (Figure 1.3). By May 2023, on average across the OECD, women’s total employment had grown about 1 percentage point more than men’s, reaching 3.5% above its pre‑crisis level.

Percentage point difference in employment growth since December 2019 between women and men, seasonally adjusted

Note: Women’s and men’s employment are indexed to 100 in December 2019. Euro Area refers to the averages of 20 Eurozone countries. The OECD average and the Euro Area are estimates derived from the OECD Unemployment statistics estimated as the unemployment level times one minus the unemployment rate and rescaled on the LFS-based quarterly employment figures.

Source: OECD (2023), “Labour: Labour market statistics”, Main Economic Indicators (database), https://doi.org/10.1787/data-00046-en (accessed on 3 July 2023).

Similarly, unemployment rates across the OECD held their ground as the year ended, mostly remaining below pre‑crisis levels (Figure 1.4). The average unemployment rate for the OECD stood at 4.8% in May 2023 – or half a percentage point below its pre‑crisis levels. In May 2023, the unemployment rate indeed exceeded its pre‑crisis levels by at least half a percentage point only in four countries – with the maximum difference of 1.6 percentage points recorded in Estonia.

Unemployment rate (percentage of labour force), seasonally adjusted

Note: The labour force population includes all those aged 15 or more. Euro Area refers to the averages of 20 Eurozone countries. For countries marked with * the latest data refer to March 2023, those marked ** to April 2023; those marked *** to Q1 2023; and those marked ‡ to June 2023.

Source: OECD (2023), “Unemployment rate” (indicator), https://doi.org/10.1787/52570002-en (accessed on 11 July 2023).

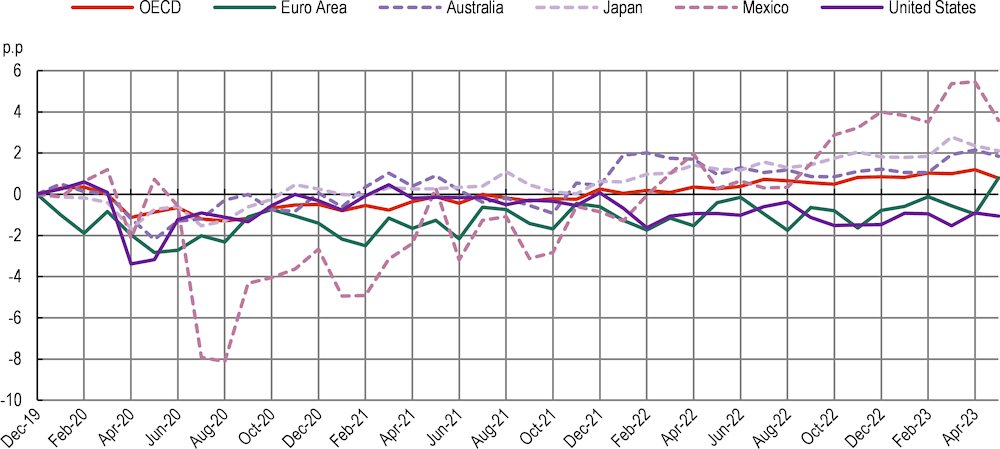

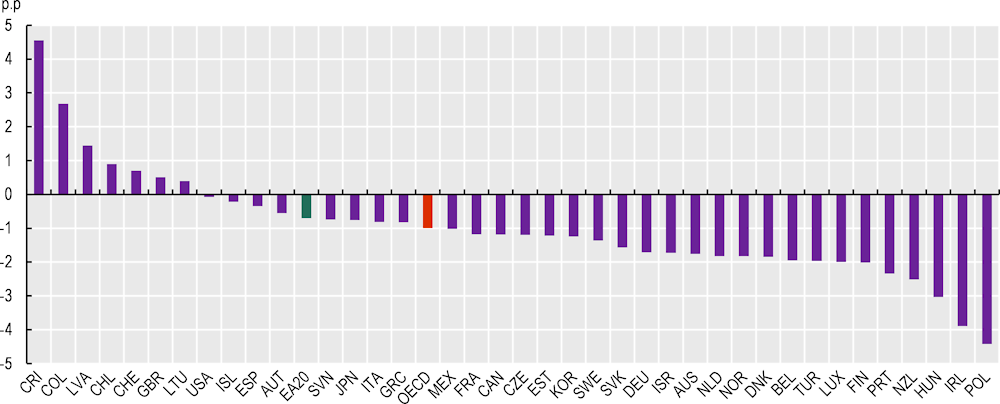

Inactivity rates among the working age population are below pre‑crisis levels in most countries, pointing to a recovery of labour supply from the initial decline at the start of the COVID‑19 crisis. As of Q1 2023, inactivity rates were at or below pre‑crisis levels in 31 countries, with an average decline across all countries of just under 1 percentage point. Inactivity rates were at least 1 percentage point above pre‑crisis levels only in Colombia, Costa Rica and Latvia.1

Percentage point change in inactivity rates among the working age population from Q4 2019 to Q1 2023, seasonally adjusted

Note: The working age population includes all those aged 15 to 64. OECD is an unweighted average of the countries shown above. Euro Area refers to 20 Eurozone countries. p.p: percentage point.

Source: OECD (2023), “Labour: Labour market statistics”, Main Economic Indicators (database), https://doi.org/10.1787/data-00046-en (accessed on 28 June 2023).

Inactivity rates have generally decreased among older adults as well, despite earlier concerns that the pandemic might induce a permanent reduction in the labour supply of this group. In fact, on average across all OECD countries, by Q1 2023, the inactivity rate for individuals aged 55 to 64 had decreased relative to pre‑crisis levels more than for those aged 25 to 54 (‑2.5 vs ‑0.6 percentage points) (Annex Figure 1.A.2). More broadly, there is little indication that the pandemic induced an increase in retirement of older workers across countries. While some earlier evidence for the United States suggested that this might have been the case (Faria-e-Castro, 2021[5]), more recent data point to a limited impact (Thompson, 2022[6]). In addition, there is no indication of significant increases in retirement in the United Kingdom (Murphy and Thwaites, 2023[7]), the Euro Area (Botelho and Weißler, 2022[8]) or Australia (Agarwal and Bishop, 2022[9]).

Hours worked per employed person are below pre‑crisis levels in most countries with recent data available (Figure 1.6). The persistence of lower hours worked in tight labour markets does raise the question as to whether the COVID‑19 crisis might have led to some structural changes, for example in workers’ preferences over work-life balance. However, the differences are generally small. In Q4 2022, hours worked per employed person were above pre‑crisis levels or below that level by less than 2% in 22 of the 30 countries with recent data available. On average, hours worked per employed person were down by just under ‑1%. In Latvia, New Zealand, Slovenia and Poland they had increased by more than 2%, while they had decreased by more than 4% in Ireland, the Slovak Republic, Portugal, Austria and Korea. The relatively large decline in hours per employed in Korea is due to the progressive lowering of the statutory limit on total weekly working hours from 68 to 52 (Carcillo, Hijzen and Thewissen, 2023[10]).

Percentage change between Q4 2019 and Q1 2023, seasonally adjusted

Notes: The figure reports total hours worked divided by total employment. OECD is an unweighted average of the countries shown above. Euro Area refers to 20 Eurozone countries. For New Zealand, it refers to total paid hours divided by filled jobs. *The latest quarter Is Q4 2022.

Source: OECD (2023), “Quarterly National Accounts”, OECD National Accounts Statistics (database), https://doi.org/10.1787/data-00017-en (accessed on 23 June 2023) for the Euro Area and the United Kingdom, Labour Force Survey (Australian Bureau of Statistics), Labour Force Survey (Statistics Bureau of Japan), Economically Active Population Survey (Statistics Korea), Household Labour Force Survey – Tables QEM034AA and QEM025AA (Statistics New Zealand), and Current Population Survey (U.S. Bureau of Labor Statistics).

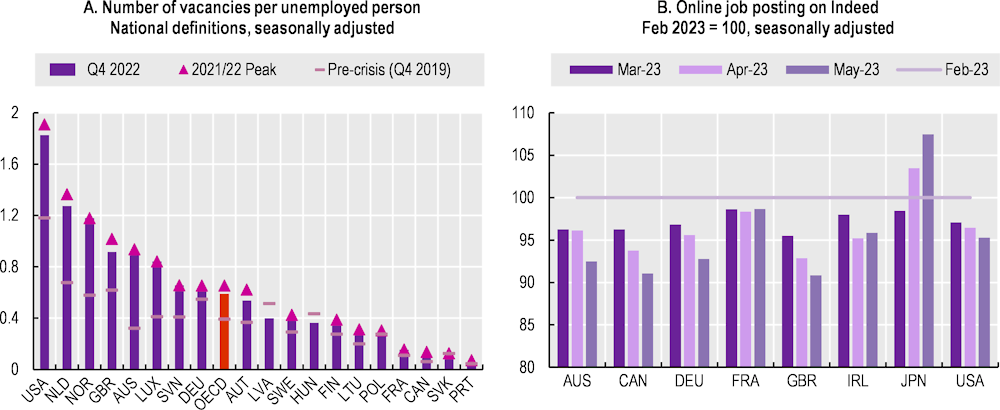

After the sharp increase in vacancies in 2021 amid the unprecedented rebound of economic activity, labour market tightness (i.e. the number of vacancies per unemployed person) peaked in the first half of 2022 in many OECD countries (Figure 1.7, Panel A). Among the 19 countries with data available, the increase in tightness in 2021 was particularly large in English speaking countries, but also in Norway and the Netherlands.2 By the end of 2022, labour market tightness was mostly below its peak levels but generally remained significantly higher than before the COVID‑19 crisis.

Data on job postings on the online platform Indeed suggest a continued easing over more recent months in the majority of countries (Figure 1.7, Panel B). Online job postings declined in the first five months of 2023 in Australia, Canada, Germany, the United Kingdom and the United States. The largest decline occurred in the United Kingdom (‑10% in May 2023 relative to February 2023). In France, online job postings declined at the start of the year and stabilised in the three months leading to May 2023. Japan is the only country among those with available data where online job postings increased steadily in the first half of 2023. In New Zealand, the official index of online job vacancies fell 9.9% in the year to March 2023.3

Note: OECD is an unweighted average of the countries shown above. In Panel A, the definition of vacancies is not harmonised across countries. For European countries (except Austria, France, Germany, Hungary and Portugal – see below), a vacancy is defined as a paid post that is newly created, unoccupied, or about to become vacant for which the employer is taking active steps and is prepared to take further steps to find a suitable candidate from outside the enterprise concerned; and which the employer intends to fill either immediately or within a specific period. For Australia, a vacancy is defined as a job available for immediate filling and for which recruitment action has been taken by the employer. For Austria, a vacancy is defined as a job notified by firms to employment agencies which remain unfilled at the end of the month. For Canada, a vacancy is defined as a job meeting the following conditions: it is vacant on the reference date (first day of the month) or will become vacant during the month; there are tasks to be carried out during the month for the job in question; and the employer is actively seeking a worker outside the organisation to fill the job. The jobs could be full-time, part-time, permanent, temporary, casual, or seasonal. Jobs reserved for subcontractors, external consultants, or other workers who are not considered employees, are excluded. For France, a vacancy is defined as the monthly number of vacancies posted by companies in Pôle emploi. For Germany, a vacancy is defined as a job of seven days’ duration or more reported by employers to employment agencies to be filled within three months and remaining unfilled at the end of the month. For Hungary, a vacancy is defined as the number of vacancies notified to local labour offices and then to the Ministry of Labour. For Portugal, a vacancy is defined as the number of vacancies reported by employers to be still vacant at the end of the month. For the United Kingdom, a vacancy is defined as a position for which employers are actively seeking recruits from outside their business or organisation (excluding agriculture, forestry and fishing) based on the estimates from the Vacancy Survey. For the United States, a vacancy is defined as a job that is not filled on the last business day of the month and a job is considered open if a specific position exists and there is work available for it, the job can be started within 30 days, and there is active recruiting for the position.

Source: OECD (2020), “Labour: Registered unemployed and job vacancies (Edition 2019)”, Main Economic Indicators (database), https://doi.org/10.1787/190bb5bc-en (accessed on 23 June 2023) for Australia, Austria, Germany, Hungary, Portugal, the United Kingdom, Job vacancy statistics by NACE Rev.2 activity for Finland, Luxembourg, Latvia, Lithuania, the Netherlands, Norway, Poland, the Slovak Republic, Slovenia and Sweden (Eurostat), Job vacancies, payroll employees, and job vacancy rate (Statistics Canada), Les demandeurs d’emploi inscrits à Pôle emploi (Dares, France), Posti vacanti (Italian National Institute of Statistics), Job Openings and Labor Turnover Survey (U.S. Bureau of Labor Statistics, retrieved from FRED); Online job posting on Indeed.

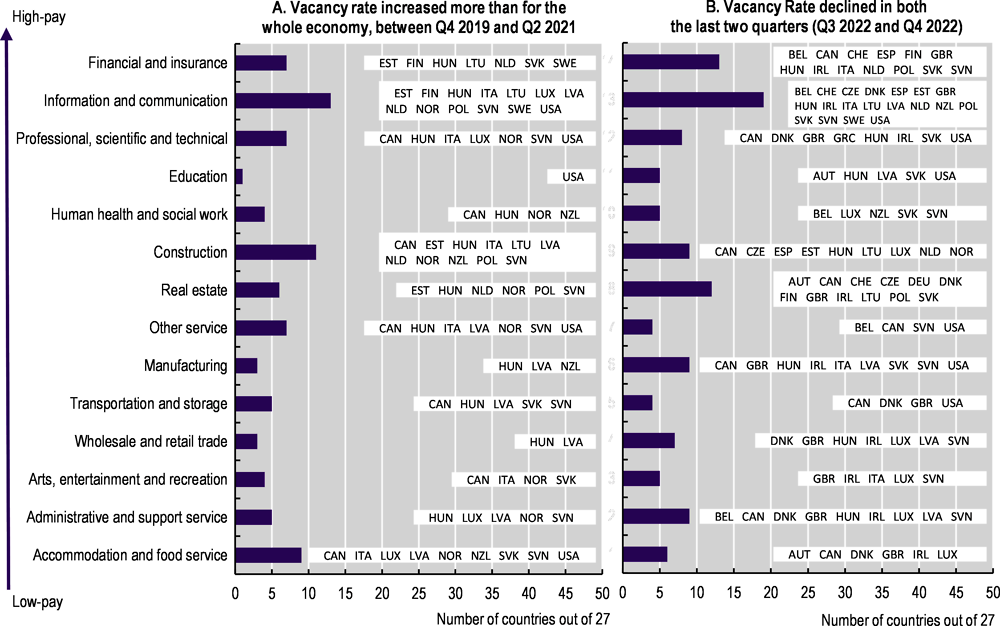

Imbalances between labour demand and supply have been widespread across industries. Vacancy rates capture the fraction of all available jobs that are unfilled and for which employers state that they are actively trying to recruit. Panel A of Figure 1.8 provides an overview of the number of countries (out of the 27 with available data) in which a specific industry experienced an increase in vacancy rates larger than the country average. The three industries most likely to have seen relatively larger increases in vacancy rates cut across the pay ranking are “Information and Communication” (13 countries), Construction (11 countries), and “Accommodation and Food Services” (9 countries).

Vacancy rates declined in the last two quarters of 2022 in many industries across countries (Panel B of Figure 1.8). Declines in vacancy rates have been particularly frequent across countries in “Finance and insurance” (13 countries) and “Information and communication” (19 countries) – two high-pay service sectors. Other industries with frequent declines in vacancy rates across countries are found across the pay rank, and include construction, manufacturing and “administrative and support services” (9 countries each).

Number of countries where the vacancy rate for a given industry increased more than that for the whole economy in 2021/22 or declined consecutively in the last two available quarters

Note: Countries where a given industry has increased more than for the whole economy (resp. has declined for the last two quarters) are indicated in white background in the chart. The countries included are Austria, Belgium, Canada, the Czech Republic, Denmark, Estonia, Finland, Germany, Greece, Hungary, Ireland, Italy, Luxembourg, Latvia, Lithuania, the Netherlands, New Zealand, Norway, Poland, Portugal, the Slovak Republic, Slovenia, Spain, Sweden, Switzerland, the United Kingdom and the United States. The definition of vacancies and vacancy rate is not harmonised across countries. For Italy, it refers to paid jobs (new or existing, if they are vacant or about to become vacant) for which the employer is looking (actively and outside the company) for a suitable candidate and is willing to make additional efforts to find one. The vacancy rate is the percentage ratio of the number of vacancies to the sum of vacancies with filled job positions. For the United States, it refers to all jobs that are not filled on the last business day of the month. A job is considered open if a specific position exists and there is work available for it, the job can be started within 30 days, and there is active recruiting for the position. For Canada, a job is considered vacant if it meets the following conditions: it is vacant on the reference date (first day of the month) or will become vacant during the month; there are tasks to be carried out during the month for the job in question; and the employer is actively seeking a worker outside the organisation to fill the job. The jobs could be full-time, part-time, permanent, temporary, casual, or seasonal. Jobs reserved for subcontractors, external consultants, or other workers who are not considered employees, are excluded. The job vacancy rate is the number of job vacancies expressed as a percentage of labour demand; that is, all occupied and vacant jobs. For the United Kingdom, vacancies are defined as positions for which employers are actively seeking recruits from outside their business or organisation. The estimates are based on the Vacancy Survey; this is a survey of employers designed to provide estimates of the stock of vacancies across the economy, excluding agriculture, forestry, and fishing. The vacancy rate is calculated as the number of vacancies per 100 jobs. For countries from Eurostat, a vacancy is defined as a paid post that is newly created, unoccupied, or about to become vacant for which the employer is taking active steps and is prepared to take further steps to find a suitable candidate from outside the enterprise concerned; and which the employer intends to fill either immediately or within a specific period. The job vacancy rate is the number of job vacancies expresses as a percentage of the sum of the number of occupied posts and the number of job vacancies. For New Zealand, Jobs Online measures changes in online job advertisements from 4 internet job boards – SEEK, Trade Me Jobs, Education Gazette and Kiwi Health Jobs (Index August 2010 = 100). For Austria, a vacancy is defined as a job notified by firms to employment agencies which remain unfilled at the end of the month.

Source: Job vacancy statistics by NACE Rev.2 activity (Eurostat), Job vacancies, payroll employees, and job vacancy rate by industry (Statistics Canada), Jobs Online (Ministry of Business, Innovation & Employment, New Zealand), Vacancies by industry (UK Office for National Statistics), Job Openings and Labor Turnover Survey (U.S. Bureau of Labor Statistics, retrieved from FRED).

Numerous factors contribute to differences in the dynamics of labour market tightness between countries. On the demand side, the initial strength of the economic rebound and the intensity of the slowdown differed depending on the composition of the economy, exposure to the energy crisis, and timing of the tightening of monetary policy. On the supply side, while labour market participation is back to pre‑crisis levels in most countries (see above), the speed of its recovery varied. Notably, labour force participation lagged behind in two of the largest OECD economies – the United States and the United Kingdom – which also experienced some of the largest increases in labour market tightness. The European Central Bank (2023[11]) attributes part of the higher labour market tightness in the United States relative to the Euro Area to the slower recovery of labour supply.

As the COVID‑19 crisis began, there was a concern that the crisis would create mismatches between labour supply and demand due to its differential impact across industries (Salvatori, 2022[4]). However, studies have found that the initial increase in mismatch was short-lived and smaller than during the Global Financial Crisis (Pizzinelli and Shibata, 2023[12]; Duval et al., 2022[13]). During the recovery, labour demand increased across sectors and countries, with no significant changes in sectoral composition. Some evidence suggests that workers redirected job searches away from affected occupations but not industries (Carrillo-Tudela et al., 2023[14]; Hensvik, Le Barbanchon and Rathelot, 2021[15]).

Workers have taken advantage of tight labour markets to improve their working conditions, leading to an uptake in quits and job mobility in several countries. In the United States, quits in non-farm employment increased to their highest levels since the start of series in 2000. After a peak in December 2021, the quit rate (i.e. quits as percentage of total employment) returned to pre‑crisis levels in April 2023.4 Initial concerns that this wave of resignations might be eroding the labour force have not come to pass as participation rates in the United States have continued to increase. Instead, the increase in quits is linked to an improvement in working conditions especially for younger and less-educated workers (Autor, Dube and McGrew, 2023[16]). In addition, historical evidence from manufacturing, indicate that the recent surge in quits was not unprecedented since waves of job quits have occurred during all fast recoveries in the post-war period in the United States (Hobijn, 2022[17]).

Similarly, evidence from France indicates that the increase in quits in 2022 was large but not unprecedented and did not erode the labour force, as over 80% of those who quit were employed within six months. Evidence from early 2022, indicates that amid the recruiting difficulties and the increase in workers’ mobility, some firms have made attempts to improve working conditions or allow more flexibility in the organisation of work (Lagouge, Ramajo and Barry, 2022[18]). Similar results also hold for Italy (Armillei, 2023[19]). In the United Kingdom, job-to-job transitions reached a record high at the end of 2021, and then declined slightly over the course of 2022, but in Q4 2022 they were still 10% higher than in the same quarter of 2019.5 By contrast, there is little indication of an increase in quits in Australia, as the proportion of businesses with open vacancies reporting the need to replace leaving employees was stable just under 80% over the course of 2021 and 2022.6

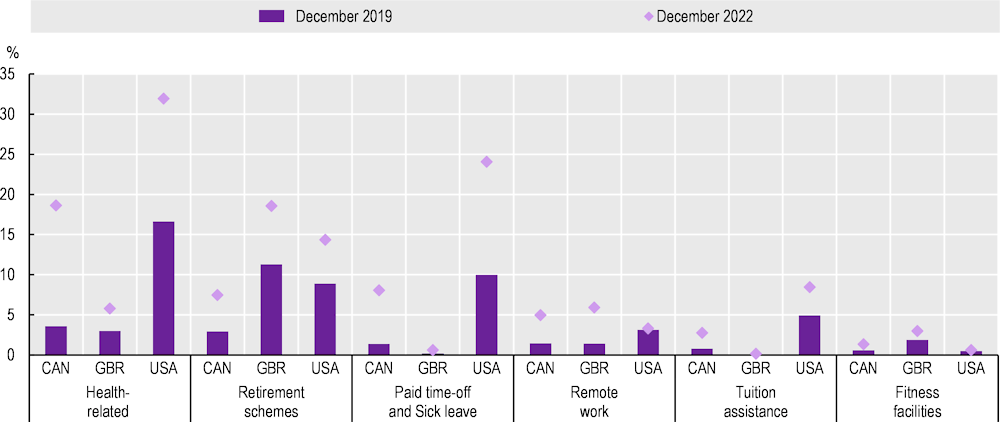

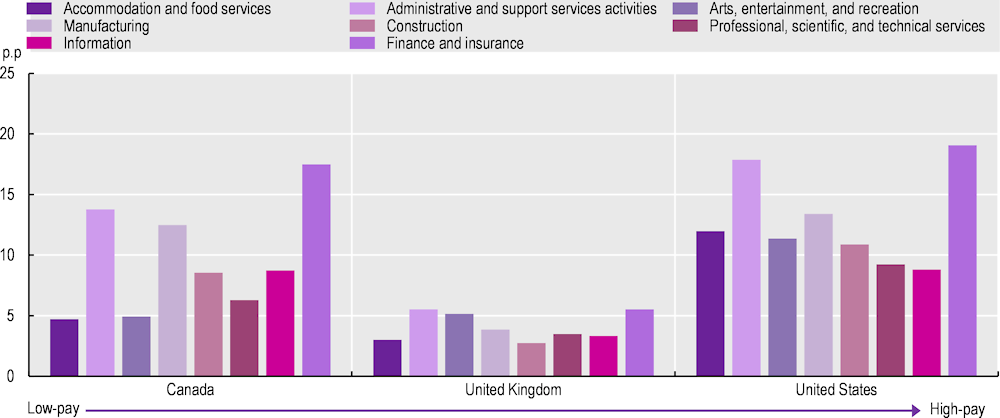

Amid tight labour markets, the share of online job postings offering job benefits has increased in several countries.7 Between December 2019 and December 2022, the United States, Canada and the United Kingdom saw an increase in the share of online job postings offering employee benefits, especially health-related benefits (including dental, vision and life insurance), retirement programs/schemes and paid time off (Figure 1.9).8 The fraction of job postings offering health-related benefits increased in particular in the United States and Canada, by 24 and 11 percentage points respectively. The mention of retirement benefits increased the most in the United Kingdom (+15 percentage points), while the share of job postings offering paid time off or sick leave increased by 17 percentage points in the United States. There were also significant increases in the mention of tuition assistance in Canada and the United States, and small increases in the mention of fitness facilities in all three countries analysed.

The increase in benefit offerings coincided with the sharp increase in labour market tightness described above. While this suggests that workers overall might have benefitted from the tight labour markets of the last year, additional analysis find no indication that benefit offerings increased more in industries where the growth in labour demand (as proxied by the growth in the number of job postings) was stronger (see Annex 1.B).9 The increase in benefit offers also appear to affect industries regardless of their pay level.

Percentage share of online job postings offering each benefit in Canada, the United Kingdom and the United States

Note: An online job posting offers a benefit if it includes in the text at least one of the keywords listed in Annex 1.B.

Source: OECD calculations based on Lightcast data.

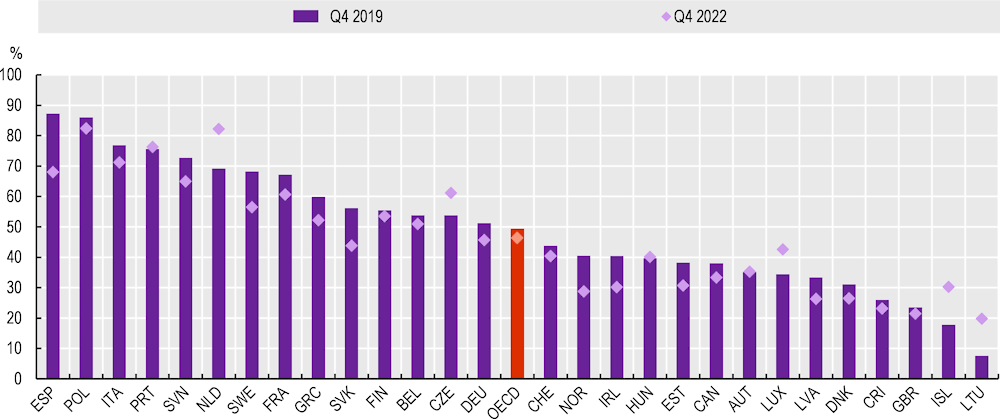

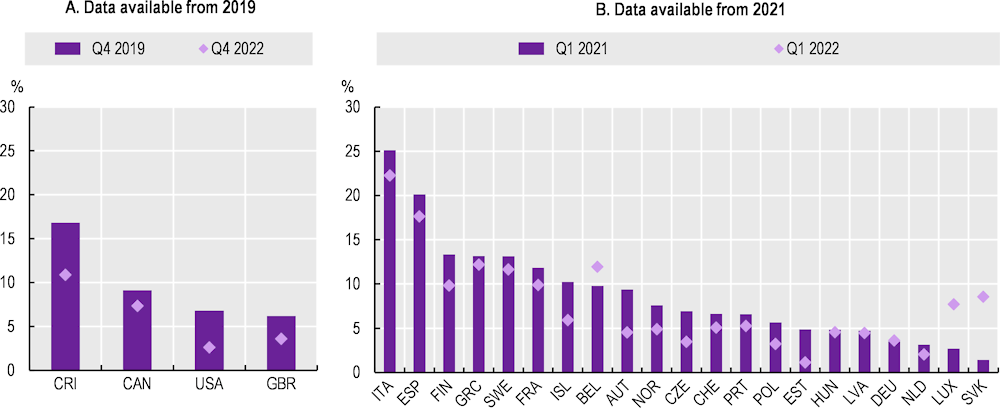

Amid the tight labour markets, the number of temporary contracts and of workers in involuntary part-time jobs have declined among new hires, suggesting an improvement in the working conditions of this group.10 In Q4 2022, the share of new hires on temporary contracts was lower than in Q4 2019 in 20 of the 28 countries with data available – despite the strong economic cycle in both periods (Figure 1.10). On average, the share of new hires on temporary contracts declined from 49% to 46%. The largest proportional declines were recorded in Norway, Spain, Sweden, the Slovak Republic and Ireland, while Lithuania and Iceland saw an increase in the share of new hires on temporary contracts although from initially low levels. Involuntary part-time among new hires declined between Q4 2019 and Q4 2022 in Canada, Costa Rica, the United Kingdom and the United States (Figure 1.11, Panel A). Similarly, in European countries, involuntary part-time among new hires declined in 18 of the 21 countries with data available between Q1 2021 and Q1 2022 (Figure 1.11, Panel B).11

Percentage share of new hires with a temporary contract

Note: OECD is the unweighted average of the countries shown. New hires are defined as employees with a tenure of at most three months.

Source: OECD calculations based on the Canadian Labour Force Survey (Statistics Canada), the Labour Force Survey (UK Office for National Statistics), Encuesta Continua de Empleo (Costa Rica) and EU labour force survey (EU-LFS) for European countries.

Percentage share of new hires in involuntary part-time

Note: Denmark, Ireland and Lithuania are not included due to anomalies in the data. Data on the share of new hires in involuntary part-time in Panel B are only available from Eurostat from Q1 2021 to Q4 2022. The figure focuses on the comparison between Q1 2021 and Q1 2022 to account for possible seasonality effects. New hires are defined as employees with tenure of at most three months.

Source: OECD calculations based on the Canadian Labour Force Survey (Statistics Canada), the Labour Force Survey (UK Office for National Statistics), Encuesta Continua de Empleo (Costa Rica), Current Population Survey (U.S. Bureau of Labor Statistics) and EU labour force survey (EU-LFS) for European countries.

Despite the signs of improvement seen in the early months of 2023, the outlook is for a period of subdued growth and persisting inflation.12 The full effects of the tightening of monetary policy since the start of 2022 are likely to appear over the course of 2023 and early 2024, particularly on private investment. Annual OECD GDP growth is projected to be below trend at 1.4% in both 2023 and 2024, although it will gradually pick up on a quarterly basis through 2024 as inflation moderates and real income growth strengthens. Helped by the decline in energy prices over the past few months, average annual headline inflation in the OECD as a whole is now projected to fall relatively quickly from 9.4% in 2022 to 6.6% in 2023 and 4.3% in 2024, with year-on-year inflation in the last quarter of 2024 down to 3.8%.

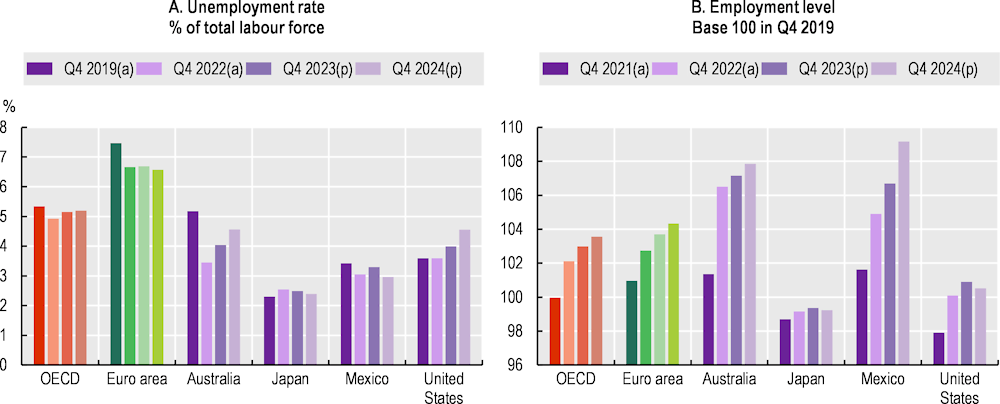

OECD-wide employment is projected to keep expanding in 2023‑24 (Figure 1.12) and the unemployment rate to rise only marginally, especially in the Euro Area. The OECD-wide unemployment rate is expected to increase from 4.9% at the end of 2022 to 5.2% in the fourth quarter of 2024 (Figure 1.12), though with relatively large rises of around 0.75 percentage point or more in Australia, New Zealand, the United Kingdom and the United States.

Note: (a) Actual value. (p) OECD projection. Euro Area refers to the 17 EU member states using the euro as their currency which are also OECD Member States.

Source: OECD (2023[2]), OECD Economic Outlook, Volume 2023 Issue 1: Preliminary version, https://doi.org/10.1787/ce188438-en.

Significant uncertainty about economic prospects remains, and the major risks to the projections are on the downside. One key concern is that inflation could continue to be more persistent than expected requiring tighter monetary policy for longer. In addition, the impact on economic growth could be stronger than expected if tighter financial conditions were to trigger stress in the financial system and undermine financial stability. Another key downside risk to the outlook relates to the uncertain course of Russia’s war of aggression against Ukraine and the associated risks of renewed disruptions in global energy and food markets. On the upside, reduced uncertainty from an early end to the war, easier-than-expected financial conditions, more robust labour force growth, and greater use of accumulated savings by households and businesses would all improve growth and investment prospects.

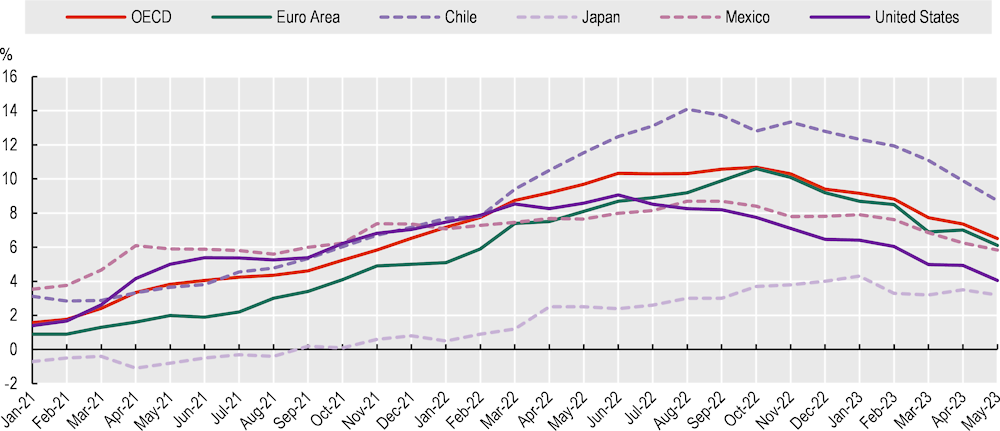

The COVID‑19 crisis was followed by a large surge in prices. Prices began to increase in 2021 due to the rapid rebound from the pandemic and related supply chain bottlenecks (Figure 1.13). Then, over the course of 2022, the impact on energy prices of Russia’s war of aggression against Ukraine pushed inflation to levels not seen for decades in most countries. Inflation was initially mostly imported and driven by input and energy prices (OECD, 2022[1]), but, over the course of 2022, it became more broad-based with higher costs increasingly being passed through into the prices of goods and services (OECD, 2022[1]).13

Inflation defined as the annual growth rate of Consumer Price Index (CPI) including all items

Note: Euro Area refers to the 20 EU member states using the euro as their currency.

Source: OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 4 July 2023).

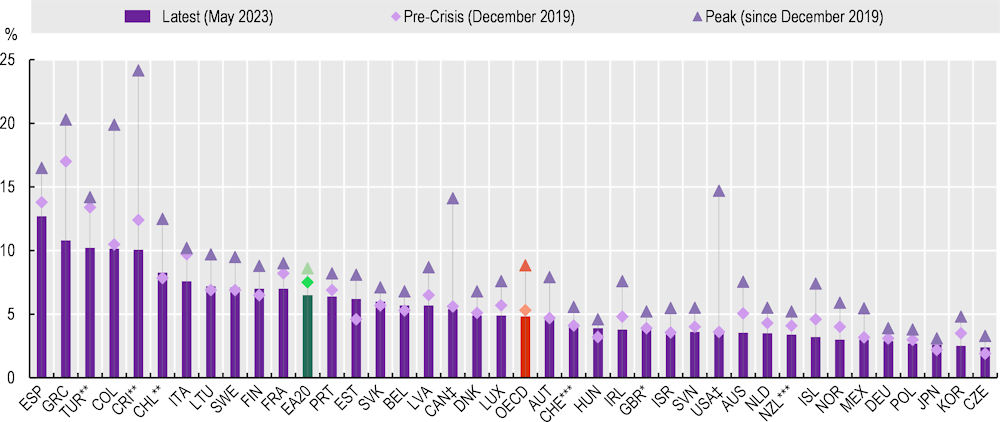

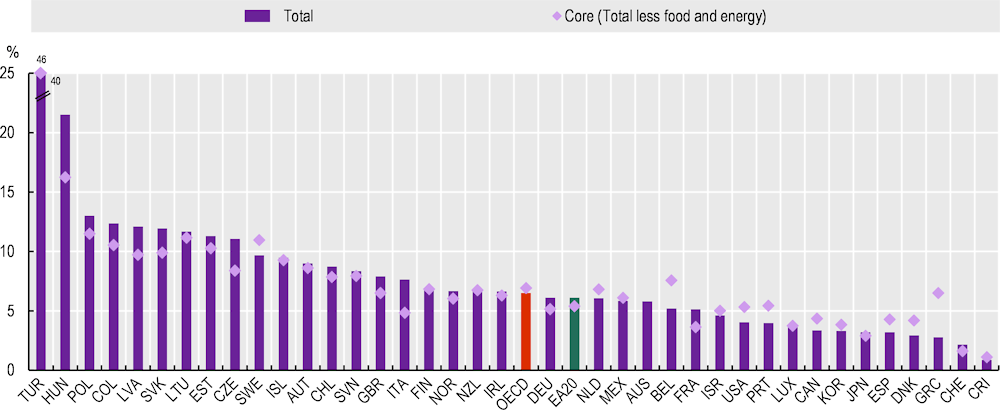

Inflation for the OECD area increased rapidly from below 2% at the start of 2021 to a peak of 10.7% in October 2022 and then fell to 6.5% in May 2023 – the last observation available at the time of writing. As of May 2023, inflation remained above 10% in nine OECD countries. Differences in total inflation across countries tended to be larger than differences in core inflation (see Figure 1.14), reflecting the differential exposure of countries to the increases in energy prices. Because of their higher vulnerability to the increase of energy prices, total inflation was particularly high in countries in Central and Eastern Europe. In general, however, amongst OECD countries, inflation was higher in Europe and South America, while it remained at relatively low levels in Korea and Japan (3.3% and 3.2% respectively).

Inflation defined as annual percentage change in the Consumer price index (CPI), May 2023 or latest observation

Note: Core inflation represents price changes excluding energy and food items, not available for Australia. Euro Area refers to 20 Eurozone countries. * For New Zealand, the data refer to year-on-year changes from Q1 2022 to Q1 2023.

Source: OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 4 July 2023), and Monthly CPI Indicator (Australian Bureau of Statistics).

In most countries, low-income households have faced a higher effective inflation rate because a higher proportion of their spending goes towards energy and food which drove most of the initial increase in inflation.14 Similarly, there is evidence that rural households have suffered more in several countries because energy and fuel account for a larger share of their total expenditures (Causa et al., 2022[20]). In general, however, as inflation becomes more broad-based, differences in effective inflation rates across different households or groups with different consumption patterns become less pronounced.

However, low-income households have less leeway to absorb increases in cost of living even when facing effective inflation rates like those of other households. First, low-income households might have less room to substitute for lower-price alternatives if they are already buying cheaper versions of a given item.15 Second, low-income households typically can rely less on savings or borrowing to buffer the increase in cost of living (Charalampakis et al., 2022[21]; The German Council of Economic Experts, 2022[22]).16

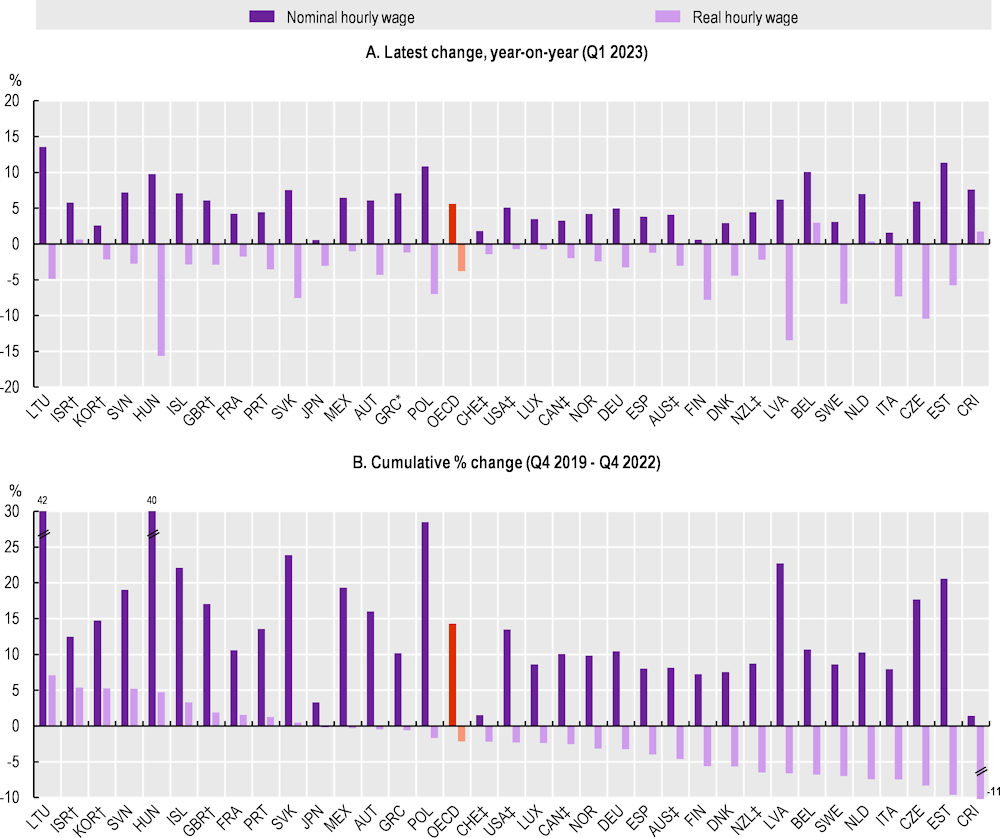

Year-on-year nominal growth in hourly wages generally picked up in 2022, but by less than the rise in inflation, leading to widespread falls in real wages. In Q1 2023, nominal year-on-year wage growth exceeded its pre‑crisis level in nearly all OECD countries, reaching 5.6% on average across the 34 countries with data available (Figure 1.15, Panel A).17 However, nominal wage growth fell short of inflation by -3.8%, on average, with negative differences observed in 30 countries.18 19

Changes in nominal and real hourly wages

Note: Real wage growth is calculated by subtracting consumer price index (CPI) inflation (all items) from nominal wage growth. OECD is an unweighted average of the countries shown above. *The latest year-on-year change refers to Q4 2022 (Greece). †The composition of industries is not fixed for Israel, Korea and the United Kingdom, and thus comparing these results with the others requires caution. ‡Additional sources of compositional shifts, such as regions (Australia, Canada, New Zealand), job characteristics and workers’ characteristics (Australia, New Zealand), gender (Switzerland) and occupations (United States) are controlled for. For Israel, the average monthly wages per employee job are used. For the United Kingdom, average weekly earnings are used. Moreover, wages in the public sector are excluded for Australia, Canada, Costa Rica, Japan, Korea, Mexico, New Zealand, the United Kingdom and the United States.

Source: The wages and salaries component of the labour cost index by NACE Rev. 2 activity (Eurostat), Wage Price Index (Australian Bureau of Statistics), Fixed weighted index of average hourly earnings for all employees (Statistics Canada), OECD calculations based on Encuesta Continua de Empleo (Instituto Nacional de Estadística y Censos, Costa Rica), Wages and Employment Monthly Statistics (Israeli Central Bureau of Statistics), OECD calculations based on Monthly Labour Survey (Japanese Ministry of Health, Labour and Welfare), Labour Force Survey at Establishments (Korean Ministry of Employment and Labour), OECD calculations based on Encuesta Nacional de Ocupación y Empleo, Encuesta Telefónica de Ocupación y Empleo, Encuesta Nacional de Ocupación y Empleo Nueva Edición (Instituto Nacional de Estadística y Geografía, Mexico), Labour Cost Index (Statistics New Zealand), Swiss Wage Index (Swiss Federal Statistical Office), Monthly Wages and Salaries Survey (UK Office for National Statistics), and Employment Cost Index (U.S. Bureau of Labor Statistics, retrieved from FRED); OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

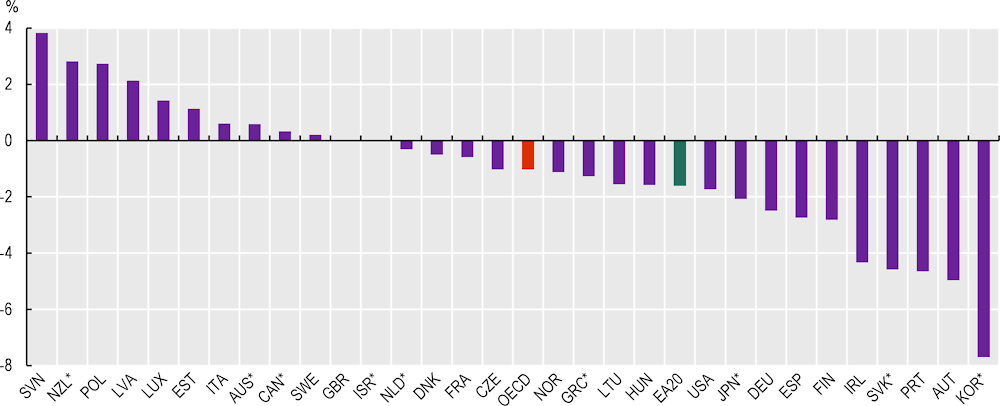

Inflation has now exceeded nominal wage growth for several quarters in most countries. As a result, at the end of 2022, real wages were below their Q4 2019 level by an average of ‑2.2% in 24 of the 34 OECD countries with available data (Figure 1.15, Panel B).20 Even in the remaining 10 countries, however, inflation had eroded most of the nominal wage growth.

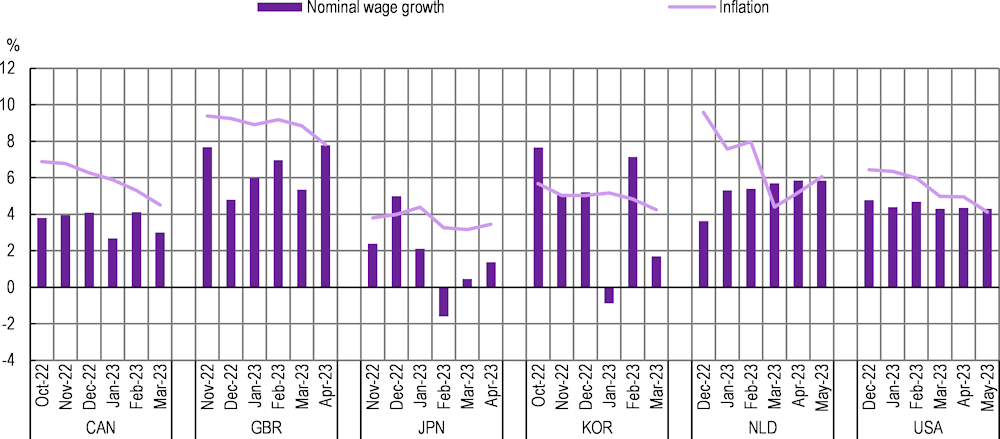

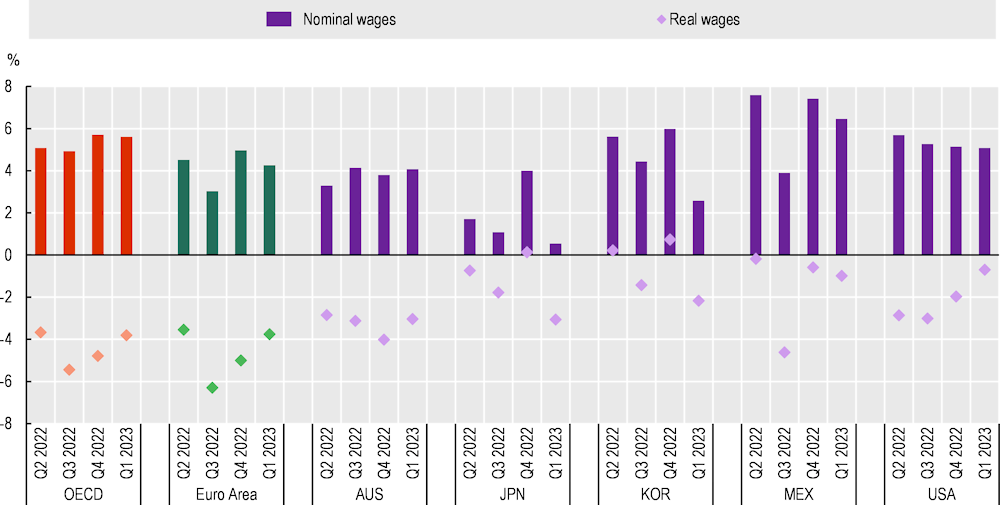

The evolution over the past year (leading up to Q1 2023) shows no clear sign of substantial acceleration of nominal wage growth across countries – with the dynamics of real wages still largely driven by inflation instead (Annex Figure 1.A.3). Data for April or May 2023 are only available for a limited number of OECD countries and, along with data from wages advertised in online job postings, point to a narrowing (or even closing in some countries) of the gap between nominal wage growth and inflation. This is mostly because of steady nominal wage growth and declining inflation (see Box 1.2).

Recent data on wages for five OECD countries mostly point to a narrowing of the gap between nominal wage growth and inflation (Figure 1.16). In fact, the latest data suggest that the fall in real wages might have come to an end in the United Kingdom, the United States and the Netherlands. This is mostly driven by a deceleration of inflation rather than an acceleration of nominal wage growth. In the United Kingdom, however, nominal wage growth was particularly robust in April 2023, reaching a high of just under 8%. In Canada and Japan, however, the latest year-on-year nominal wage growth remains below inflation, while in Korea it exhibits considerable short-term variation.

Year-on-year percentage change, over the latest six months

Note: The wage measures used above do not include the public sector and are not harmonised across countries: fixed weighted index of average hourly earnings for Canada; average weekly earnings – private sector level – seasonally adjusted total pay excluding arrears for the United Kingdom; total hourly cash earnings (seasonally adjusted) for Japan; average hourly wages (seasonally adjusted) for Korea; collective labour agreement wages per hour including special remunerations for the Netherlands; and average hourly earnings of all employees (Total Private, seasonally adjusted) for the United States.

Source: Fixed weighted index of average hourly earnings for all employees (Statistics Canada), Monthly Wages and Salaries Survey (UK Office for National Statistics), Monthly Labour Survey (Japanese Ministry of Health, Labour and Welfare), Labour Force Survey at Establishments (Korean Ministry of Employment and Labour), and Current Employment Statistics (U.S. Bureau of Labor Statistics, retrieved from FRED); OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

Evidence from wages advertised in job posting on the online platform Indeed suggests a steady or declining nominal wage growth over the first five months of 2023 in Germany, France, Ireland, Italy and the United States (Figure 1.17). In Spain, the Netherlands, and – more markedly – the United Kingdom, nominal growth of posted wages has increased slightly. In general, the gap between inflation and nominal wage growth in posted wages (both measured here as 3-month moving averages) has becomes smaller. However, real growth in posted wages has turned positive only in Spain and the United States in recent months. In Italy, the gap between inflation and growth in posted wages increased again in May 2023, after declining for the first four months of the year.

Year-on-year percentage change, 3‑month moving averages, from December 2022 to May 2023

Note: The posted wages are the average year-on-year percentage changes in wages and salaries advertised by job postings on Indeed.

Source: Indeed Wage Tracker (https://github.com/hiring-lab/indeed-wage-tracker); OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

Wage dynamics could vary across the wage distribution due to factors such as labour demand, minimum wage laws, collective bargaining, and employer monopsony power. Since data on individual wages become available only with a significant lag for most countries, this section relies on wages by industry to provide some initial insights on how workers of different pay levels have fared in many OECD countries.

To offer an overview of wage developments by industry across countries, Figure 1.18 reports changes in real wages by industries aggregated in three broad groups: low-pay industries (accommodation and food services, administrative & support services, arts, entertainment and recreation, wholesale & retail trade); mid-pay industries (transportation and storage, manufacturing, other services, real estate activities, and construction); and high-pay industries (human health and social work, education, professional activities, information and communication, and finance and insurance). Industries are weighted by employment shares within each group.

Percentage change in real hourly wages

Note: Real wage growth is calculated by subtracting consumer price index (CPI) inflation (all items) from nominal wage growth. OECD is an unweighted average of the countries shown. Low-pay industries include Accommodation & food service, Administrative & support service, Arts, entertainment & recreation and Wholesale & retail trade. Middle‑pay industries include Transportation & storage, Manufacturing, Other service, Real estate activities and Construction. High-pay industries include Human health & social work, Education, Professional activities, Information & communication and Finance & insurance. Average employment shares by industry over the four quarters of 2019 are used for aggregation and thus small inconsistencies between changes in wages by industry and changes in average wages are possible. *The latest year-on-year change refers to Q4 2022 (Greece and the Netherlands). †There are missing industries: Arts, entertainment & recreation is not included for the United States; Human health & social work and Education are not included for France. ‡Average weekly earnings are used for the United Kingdom. Moreover, wages in the public sector are excluded for Australia, Japan, Korea, New Zealand, the United Kingdom and the United States.

Source: The wages and salaries component of labour cost index by NACE Rev. 2 activity (Eurostat), Wage Price Index (Australian Bureau of Statistics), Fixed weighted index of average hourly earnings for all employees (Statistics Canada), OECD calculations based on Encuesta Continua de Empleo (Instituto Nacional de Estadística y Censos, Costa Rica), Wages and Employment Monthly Statistics (Israeli Central Bureau of Statistics), OECD calculations based on Monthly Labour Survey (Japanese Ministry of Health, Labour and Welfare), Labour Force Survey at Establishments (Korean Ministry of Employment and Labour), OECD calculations based on Encuesta Nacional de Ocupación y Empleo, Encuesta Telefónica de Ocupación y Empleo, Encuesta Nacional de Ocupación y Empleo Nueva Edición (Instituto Nacional de Estadística y Geografía, Mexico), Labour Cost Index (Statistics New Zealand), Swiss Wage Index (Swiss Federal Statistical Office), Monthly Wages and Salaries Survey (UK Office for National Statistics), and Employment Cost Index (U.S. Bureau of Labor Statistics, retrieved from FRED); OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

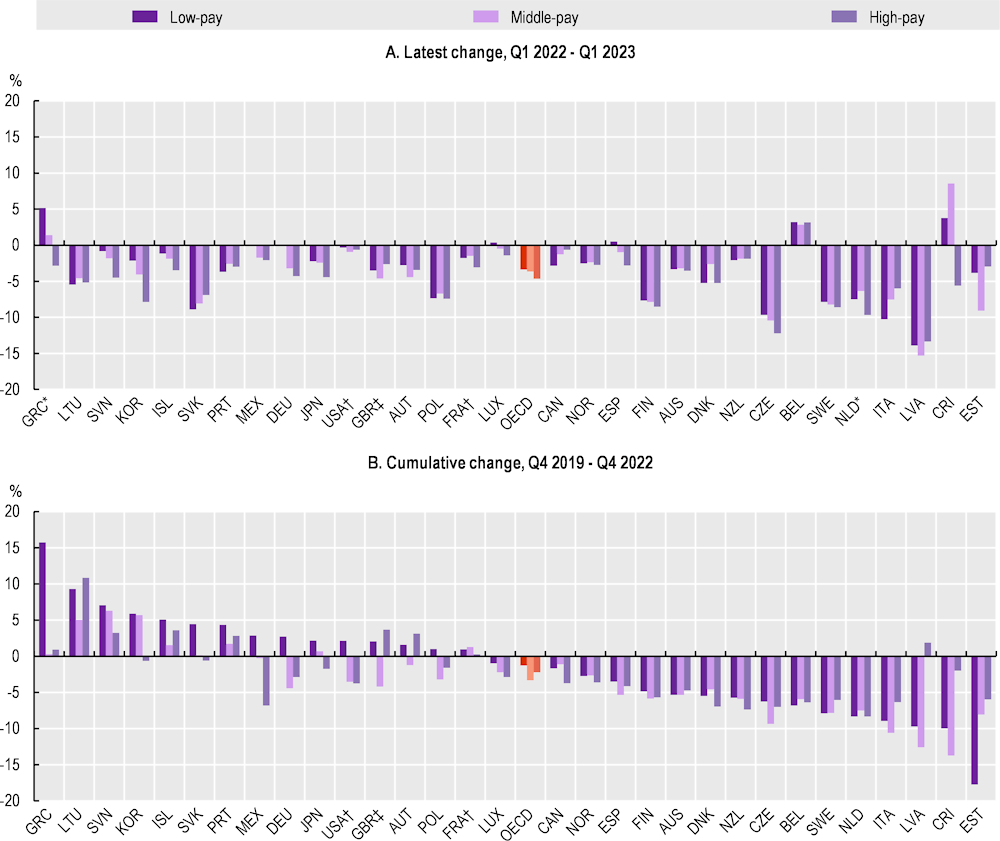

Real wages have declined across industries in almost all OECD countries, but workers in low-pay industries have often fared relatively better (Figure 1.18, Panel A).21 The latest year-on-year changes for Q1 2023 show that real wages performed better in low-pay industries than in both mid- and high-pay industries in 15 of the 31 countries with data available. Conversely, wages in low-pay industries had the worst performance only in six countries, losing more than 1 percentage point relative to both mid- and high-pay industries only in Canada and Italy. In the pair-wise comparison, real wages performed better in low-pay industries than in mid-pay ones in 18 countries, and better than in high-pay industries in 22 countries.

The pattern of relatively better wage performance in low-pay industries also holds when considering changes relative to pre‑crisis levels – even if over this longer time horizon real wages declined in fewer countries and industries (Figure 1.18, Panel B). Between Q4 2019 and Q4 2022, real wages performed better in low-pay industries than in both high- and mid-pay ones in 16 of the 31 OECD countries with available data. Conversely, wages in low-pay industries fared worse than both the other two groups of industries only in four countries (Belgium, Estonia, the Netherlands and Sweden). In the pair-wise comparison, real wages performed better in low pay industries than in mid-pay ones in 23 countries, and better than in high-pay industries in 20 countries.

Tentative evidence suggests that labour markets tightening has been associated with stronger wage growth at the industry level. A simple analysis correlating changes in real wages with changes in vacancy rates for 14 industries in 15 OECD countries suggests that – on a year-on-year basis – a 1% increase in the vacancy rates was associated with a 0.03% increase in real wages. The analysis provides some indication that the correlation between tightness and real wage growth might have been slightly stronger in low-pay industries, but the differences are not statistically significant. In addition, a simple extension of the exercise does not support the conclusion that differences in either the level of tightness or in its impact across (broad) industries can explain the relatively better performance of real wages in low-pay industries. Similarly, another extension of the analysis finds that increases in statutory minimum wages are associated with larger increases in average wages particularly in low-pay industries, but this difference does not explain the differentials in wage growth across industries (see Section 1.3. for a detailed discussion of minimum wage policies and adjustments across OECD countries in recent times).22

These findings might be at least in part the result of averaging across countries with very different institutional settings. Using more granular data from before the pandemic, Duval et al. (2022[13]) find that in the United Kingdom and the United States, the impact of a given increase in tightness on wage growth is at least twice as large in low-pay sectors as in the average industry. However, they acknowledge that the gap might be smaller in continental Europe because of binding and stickier statutory or collectively bargained minimum wages. Consistent with this observation, Hentzgen et al. (2023[23]) find no correlation across industries between recent changes in tightness and nominal wage growth in France, a country where both collective bargaining and the minimum wage play a significant role in wage setting (see Section 1.3). As for the effect of the minimum wage, Hentzgen et al. (2023[23]) find a clear correlation between recent increases in wages in an industry and the proportion of workers affected by increases in minimum wages in France, but Autor et al. (2023[16]) find no indication in the United States that wages at the bottom of the distribution increased more in states that increased their minimum wages recently.

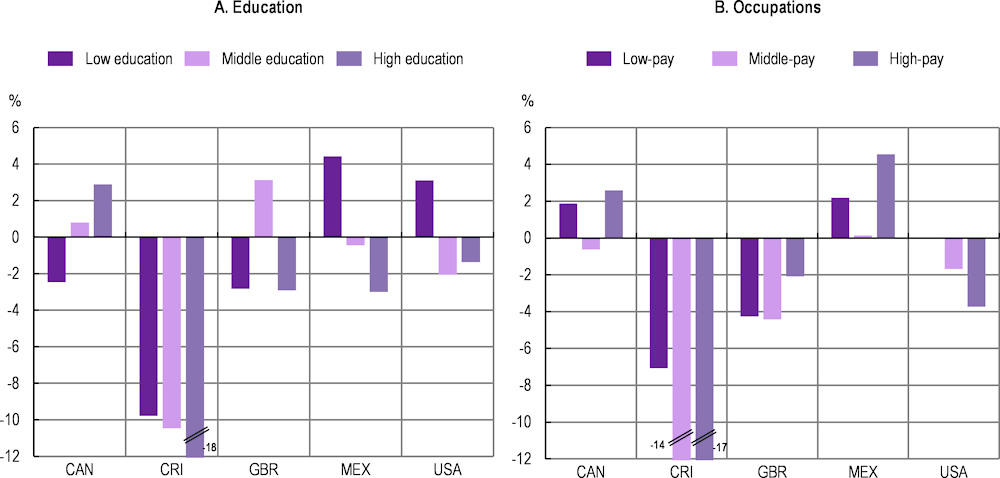

The results presented in this section indicate a trend of compression of wages across workers of different pay levels, as proxied by industry wages. For the few countries for which data on wages by education and occupations are already available, the picture is mixed, with an indication of compression of wages across both education and occupation groups in Costa Rica, Mexico and the United States, but not in Canada and in the United Kingdom (see Box 1.3).

The main analysis in the chapter looks at wages by industry to provide evidence on wage dynamics across workers of different pay levels. For five countries, the analysis can be extended to look at changes in wages by education and occupation thanks to the timely availability of Labour Force Survey data. Figure 1.19 reports changes in real wages (calculated as the difference between nominal wage growth and inflation) for various groups between the end of 2019 and that of 2022. The results suggest a compression of wages across workers of different pay levels (as proxied by education and occupation) in Costa Rica, Mexico and the United States, but not in Canada and in the United Kingdom.

In Costa Rica and the United States, wages performed better among the low educated and workers in low-pay occupations (Figure 1.19). In Costa Rica, real wages fell across the board but much less among workers of low education and workers in low-pay jobs. In the United States, workers with low education and those in low-pay occupations were the only ones that avoided a real wage contraction between Q4 2019 and Q4 2022.

Cumulative percentage change in real hourly wages between Q4 2019 and Q4 2022

Note: The classification of pay levels by occupation is determined by identifying the top/middle/bottom tercile of employed population based on the ranking of average hourly wages according to a national classification of occupations in each country. The level of education is classified as follows: low (ISCED 0‑2), middle (ISCED 3‑4) and high (ISCED 5‑8). Real wage growth is calculated by subtracting consumer price index (CPI) inflation (all items) from nominal wage growth.

Source: OECD calculations based on the Labour Force Survey (Statistics Canada), Encuesta Continua de Empleo (Instituto Nacional de Estadística y Censos, Costa Rica), Labour Force Survey (UK Office for National Statistics), Encuesta Nacional de Ocupación y Empleo, Encuesta Telefónica de Ocupación y Empleo, Encuesta Nacional de Ocupación y Empleo Nueva Edición (Instituto Nacional de Estadística y Geografía, Mexico) and Current Population Survey (U.S. Bureau of Labor Statistics). OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

In Canada, Mexico and the United Kingdom, however, there is no clear sign of a compression of wages across groups of different pay levels, with results varying depending on whether education or occupations are considered. In Canada, workers with low education are the only ones to have experienced a fall in real wages since the start of the crisis (by ‑2.5%), but workers in low-pay occupations have seen better wage performance than those in middle‑pay occupations (Figure 1.19). In Mexico, wage differentials by education have compressed, as the low-educated are the only group that experienced real wage growth. However, at the same time, wages have grown more for workers in high-pay occupations than in low-pay occupations. In the United Kingdom, the low-educated saw a decline in real wages of ‑3%, similar to that of high-educated workers, while real wages of mid-educated workers increased by 3%. Workers in low-pay occupations experienced a decline in real wages like those in mid-pay ones, while workers in high-pay occupations saw a smaller fall in real wages.

While informative of a widespread trend across OECD countries, these results do not allow strong conclusions on how the current wage crisis is affecting wage inequality more broadly. More granular data on wages are necessary to assess changes across the wage distribution and conduct a more reliable analysis of their determinants. Because of the paucity and the delay of this type of data, however, there is currently very limited evidence even on individual countries, with data pointing to a compression of the wage distribution in the United States but not in the United Kingdom.

For the United States, Autor et al. (2023[16]) document a remarkable compression of the wage distribution in 2021‑22 which counteracted one‑quarter of the four‑decade increase in aggregate inequality between the 10th and 90th percentile. They find that the pandemic increased the elasticity of labour supply to firms in the low-wage labour market, reducing employer market power and spurring rapid wage growth at the bottom. Among the factors they discuss that might have contributed to this change is a decrease in work-firm attachment spurred by the large number of separations that occurred during the pandemic. By contrast, in the United Kingdom, gross hourly earnings of employees at the bottom and at the top of the distribution have grown in similar ways between the last quarter of 2019 and the last quarter of 2022, with slightly larger growth in the top decile than in the bottom one over the last year.23

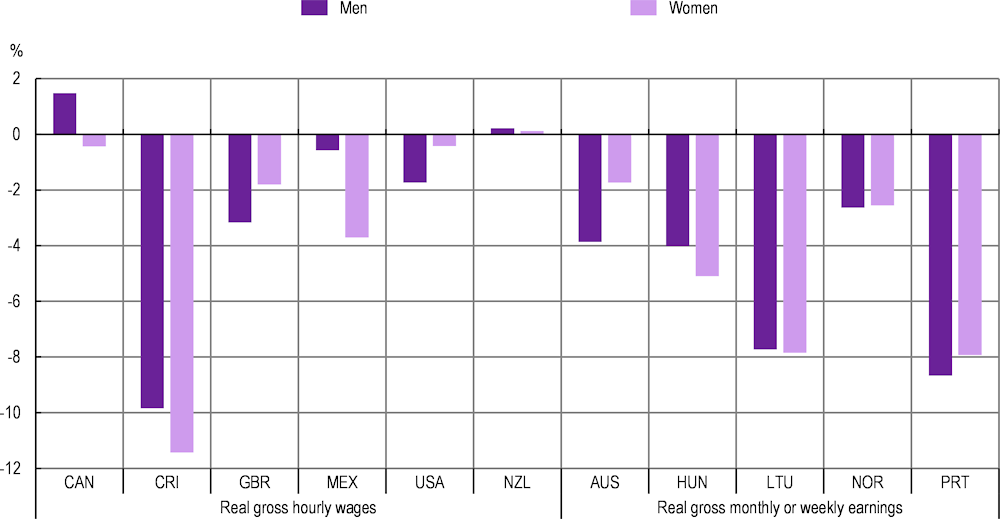

The cost-of-living crisis could affect men and women in different ways if wage dynamics differ substantially across industries and occupations with different gender composition. However, the limited data currently available show no systematic gender differences in the evolution in real wages across countries (Figure 1.20). In four of the 11 countries with data available for Q4 2022, men experienced larger year-on-year declines in real wages than women, with the largest differential in Australia and the United Kingdom where real wages for men fell by at least 3%. In four other countries, men fared better than women on average – with the largest difference in Mexico, where real wages for women fell by more than 3% against less than 1% for men. In the remaining three countries (Lithuania, Norway and New Zealand), year-on-year changes in real wages were similar between the two genders.

Percentage change between Q4 2019 and Q4 2022

Note: Gross monthly earnings for Lithuania and Norway. Gross weekly earnings for New Zealand. Net monthly wages for Portugal. Quarterly cumulative gross earnings for Hungary. Real wage growth is calculated by subtracting consumer price index (CPI) inflation (all items) from nominal wage growth.

Source: OECD calculations based on the Labour Force Survey (Statistics Canada), Encuesta Continua de Empleo (Instituto Nacional de Estadística y Censos, Costa Rica), Labour Force Survey (UK Office for National Statistics), Encuesta Nacional de Ocupación y Empleo, Encuesta Telefónica de Ocupación y Empleo, Encuesta Nacional de Ocupación y Empleo Nueva Edición (Instituto Nacional de Estadística y Geografía, Mexico) and Current Population Survey (U.S. Bureau of Labor Statistics). Average gross earnings of full-time employees (Hungarian Central Statistical Office), Average Weekly Earnings (Australian Bureau of Statistics), Average monthly earnings (Statistic Lithuania, Official Statistics Portal), Average monthly earnings (Statistics Norway), Average Weekly Earnings (Statistics New Zealand), Net monthly mean wages (Statistics Portugal). OECD (2023), “Prices: Consumer prices”, Main Economic Indicators (database), https://doi.org/10.1787/0f2e8000-en (accessed on 23 June 2023).

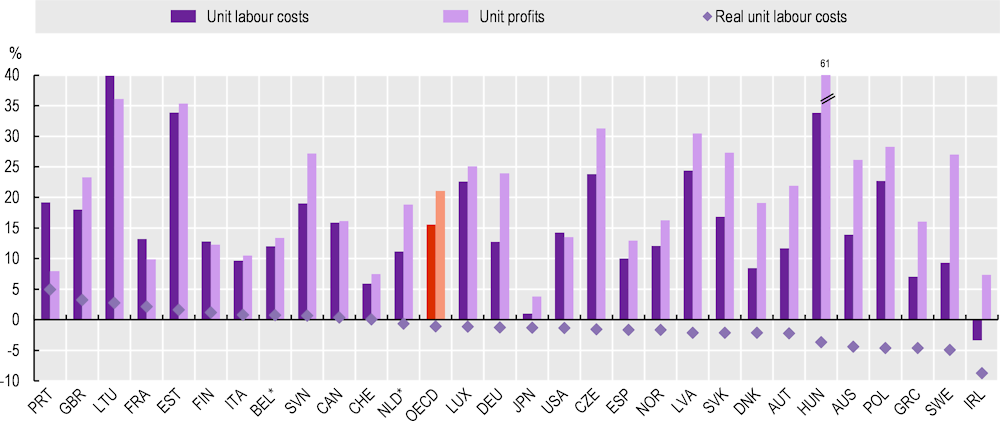

Over the last three years, labour costs per unit of real output (or unit labour costs) have increased in most OECD countries as growth in nominal wages has exceeded productivity growth (Figure 1.21).24 Profit margins, as measured by profits per unit of real output (or unit profits), also grew in most countries, indicating that – on aggregate – firms were able to increase prices beyond the increase in the cost of labour and other inputs.

In fact, in most countries, unit profits rose more than unit labour costs in 2021 and 2022. As a result, over the last two years, profits have made an unusually large contribution to domestic price pressures (Box 1.5) and the labour share (i.e. the part of national income allocated to wages and other labour-related compensation) has fallen in many OECD countries.25 Changes in real unit labour costs, i.e. the difference between changes in unit labour costs and changes in producers prices (i.e. GDP deflator) – offers a visualisation of the labour share changes. Real unit labour costs declined in 18 out of 29 countries with available data. Among the remaining countries, the largest increases in real unit labour costs took place in Portugal, the United Kingdom and Lithuania (Figure 1.21).26

The combination of rising unit labour costs and unit profits is relatively unusual as increases in one are often absorbed by a fall in the other (OECD, 2023[2]). Looking at historic evidence, one could have expected that the worsening of the terms of trade would have reduced profits (Arce and Koester, 2023[24]). The specific nature of the recovery from the COVID‑19 crisis likely provided conditions particularly favourable to the expansion of profits margins.27 At the height of the COVID‑19 crisis, in many countries, the fall in profit margins was mitigated by various forms of public support, including job retention schemes which subsidised labour hoarding to an unprecedented extent (European Central Bank, 2021[25]; OECD, 2021[26]). Unlike in previous recessions, production capacity was largely preserved during the pandemic-induced freezing of the economy. As economies re‑opened, pent-up demand and large recovery plans bolstered aggregate demand and helped profits pick up quickly as supply-chain bottlenecks slowed down the expansion of supply. In a context with strong consumer demand and rapidly evolving inflation driven by external factors, firms might have had more room to increase prices simultaneously as they expected competitors to behave in the same way, while consumers might have been more prone to accept price increases given the inflationary context (Weber and Wasner, 2023[27]). In addition, some of the increases in prices might have also been in anticipation of future increases in input and labour costs (Glover, Mustre-del-Río and von Ende-Becker, 2023[28]). However, the recent decline in the cost of energy and other inputs along with downward price rigidity is likely to sustain profit margins at least in the near future (INSEE, 2023[29]; European Commission, 2023[30]).

Percentage changes, seasonally adjusted, from Q4 2019 to Q1 2023

Note: OECD is an unweighted average of the countries shown above. *For Belgium and the Netherlands, changes refer to the period from Q4 2019 to Q4 2022. For Norway, the data are based on mainland Norway. Unit labour costs and unit profits are calculated by dividing compensation of employees, gross operating surplus, respectively, by real GDP. Real unit labour costs are calculated by dividing compensation of employees by nominal GDP, indicating the share of national income going to labour. For Japan and Norway, gross operating surplus is approximated by deducting nominal GDP from compensation of employees. Compensation of employees, gross operating surplus, gross domestic products and GDP deflators are denominated in local currencies.

Source: OECD Quarterly National Accounts: Volume and price indices – GDP Expenditure Approach, http://dotstat.oecd.org/Index.aspx?QueryId=120521; Quarterly National Accounts – Income Approach , http://dotstat.oecd.org/Index.aspx?QueryId=120186; National Accounts – Quarterly Estimates (The Cabinet Office of Japan); National Accounts – Tables 09190 and 09175 (Statistics Norway).

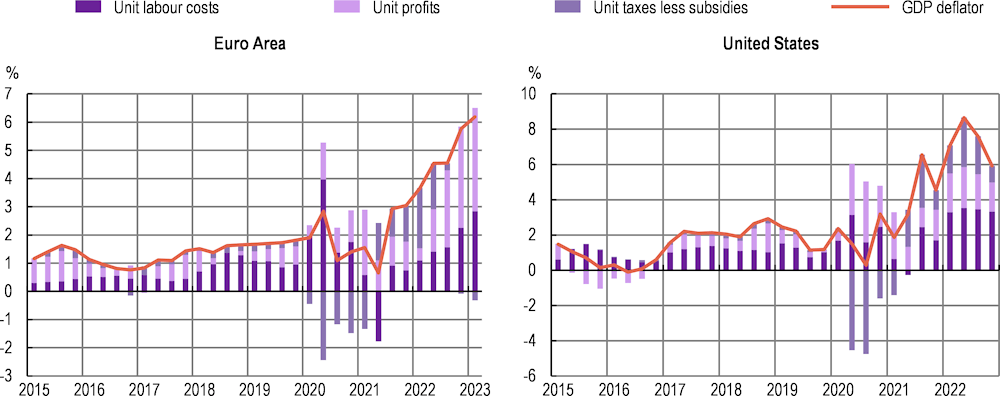

The initial surge in inflation was largely imported in many OECD countries and driven by commodity and energy prices. However, over the course of 2022, inflation became more broad-based with higher costs increasingly being passed through into the prices of domestic goods and services (OECD, 2022[1]). In addition to the increase in the costs of intermediate inputs, price dynamics are also influenced by changes in wages, profits, and taxes and subsidies. The analysis of this section shows that in recent quarters, both profits and labour costs have increased, with growth in profits exceeding growth in labour costs in many countries and sectors.

Figure 1.22 presents a decomposition of changes in the GDP deflator to gauge the contribution of wages, profits, and taxes to domestic price changes. Changes in the GDP deflator differ from consumer price inflation discussed in this section because the composition of household consumption underlying CPI-based measures of inflation is different from the composition of domestic output measured by GDP. Nevertheless, domestic price pressures are one of the main drivers of core inflation, i.e. inflation excluding energy and food (Arce and Koester, 2023[24]).

Contribution to the GDP deflator, year-on-year percentage changes, seasonally adjusted data

Note: Euro Area represents the average of 20 Eurozone countries. Unit labour costs, unit profits and unit taxes less subsidies are calculated by dividing compensation of employees, gross operating surplus and taxes less subsidies on productions and imports, respectively, by real GDP. For the United States, changes in the GDP deflator are reported net of statistical discrepancies. Data for Q1 2023 are not shown due to unusually large statistical discrepancies in the data available at the time of writing. Compensation of employees, gross operating surplus, taxes less subsidies on productions and imports, gross domestic products and deflators are denominated in local currencies.

Source: OECD Quarterly National Accounts: Volume and price indices – GDP Expenditure Approach, http://dotstat.oecd.org/Index.aspx?QueryId=120521; Quarterly National Accounts – Income Approach, http://dotstat.oecd.org/Index.aspx?QueryId=120186.

In the Euro Area and in the United States, both wages and profits have contributed to recent increases in domestic prices. In the Euro Area, the contribution of profits has been particularly large, accounting for most of the increase in domestic prices in the second half of 2022 and first quarter of 2023. This is in contrast with previous energy shocks, when increases in GDP deflator were mostly accounted for by changes in labour costs (Hansen, Toscani and Zhou, 2023[31]). In the United States, amid particularly tight labour markets, wages have generally contributed to increases in domestic prices more than profits in recent quarters. The recent contribution of profit margins was much larger than in the years before the crisis but has decreased in the most recent quarters. The differences between the Euro Area and the United States might in part reflect the fact that price dynamics have been more demand-driven in the latter (Hansen, Toscani and Zhou, 2023[31]). The contribution of unit taxes and subsidies has been particularly volatile over the period considered due to the introduction and withdrawal of pandemic-related subsidies as well as changes in the composition of household consumption (OECD, 2023[2]).

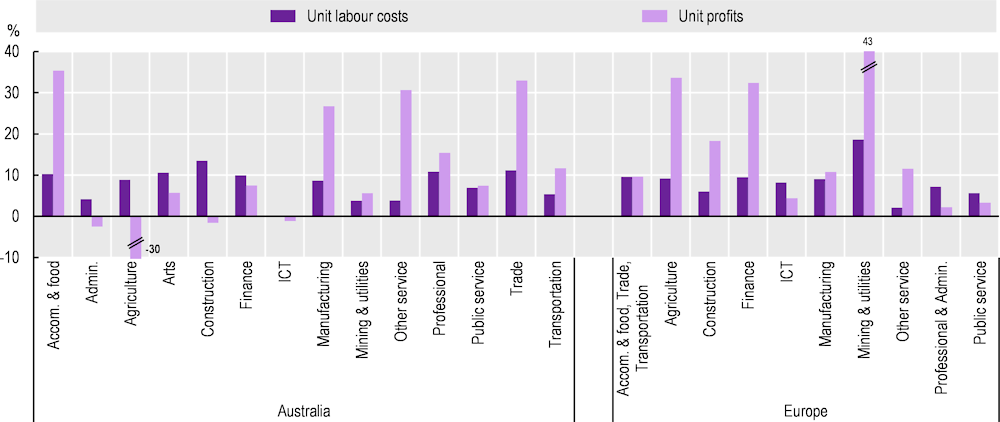

Data from Europe and Australia show that the strong performance of profits in 2022 was not limited to the energy sector. In the year to Q1 2023, in Europe, unit profits increased more than unit labour costs in manufacturing, construction and finance, and grew at the same rate as unit labour cost in “accommodation food and transportation” (Figure 1.23). Similarly, unit profits increased more than unit labour costs in several sectors in Australia, including “accommodation and food”, manufacturing, trade, and transportation.

Going forward, this evidence suggests some room for profits to absorb further partial adjustments in wages without generating significant price pressures or resulting in a fall in labour demand. However, the implications of further increases in labour costs for prices, profits and labour demand can vary across firms depending on the competitiveness of the output market, the cost structure of the firm and the evolution of the business cycle. These factors can vary significantly even within the broad sectors referenced in Figure 1.23. Firms that have more market power or operate in non-tradable sectors are more likely to be able to increase prices.28 In contrast, firms operating in more competitive markets may have to absorb wage increases by reducing profits.

Rising costs of other inputs, such as energy, can also eat into profits and limit the ability to absorb some wage increases. Indeed, some of the increases in prices might have been in anticipation of further increases in input costs, as the energy shock works its way through the supply chain. Energy-intensive manufacturing may be particularly vulnerable to these cost pressures, but some service sectors – such as accommodation and food – are also relatively energy-intensive (European Commission, 2022[32]). The impact of the increase in input prices is likely to be more significant on small and medium firms in these sectors. However, given the downward rigidity of prices, the recent decline in input costs will also likely provide further room to absorb some wage increases without generating inflationary pressures. More broadly, firm profitability may be undermined in the short term by a fall in the demand due to the tightening of monetary policy and the erosion of purchasing power. In this context, rising labour costs might be more likely to translate into a reduction in labour demand and potential employment losses. All in all, while the evidence suggests room for profits to absorb some adjustments in wages in several sectors and countries, the exact room of manoeuvre will likely vary across sectors and type of firms.

Percentage changes, seasonally adjusted, from Q1 2022 to Q1 2023

Note: Europe represents the unweighted averages of 19 European OECD countries: Austria, Belgium, the Czech Republic, Denmark, Spain, Estonia, Finland, Greece, Hungary, Ireland, Italy, Lithuania, Luxembourg, Latvia, the Netherlands, Portugal, the Slovak Republic, Slovenia and Sweden. Unit labour costs are calculated as the share of compensation of employees in gross value added (chain volume measures). For Australia, unit profits are calculated as the share of gross operating surplus and gross mixed income in gross value added (chain volume measures). For Europe, unit profits are calculated from the sum of gross operating surplus and taxes less subsidies on production and imports, which are the deduction of compensation of employees from gross value added (current prices). Compensation of employees, gross operating surplus, taxes less subsidies on production and imports, gross value added are based on local currencies.

Source: Australian National Accounts: National Income, Expenditure and Product – Table 6 & Table 45 (Australian Bureau of Statistics); Gross value added and income – A*10 industry breakdowns (Eurostat).

The quick rise of inflation over the past two years – that largely originated outside the labour market – raised the concern that it might set-off a price‑wage spiral which could further undermine the purchasing power of those employed and even lead to significant employment losses. The evidence presented in this section, however, offers no indication of signs of a price‑wage spiral so far. Nominal growth has picked up but it exhibits no clear signs of significant further acceleration across countries. The gap with inflation appears to be narrowing in recent months mostly because of a slow decline in inflation, but the erosion of real wages has not halted yet in the vast majority of OECD countries.

On balance therefore, the main problem going forward is a deepening of the cost-of-living crisis across the OECD. A gradual recovery of at least some of the recent losses in purchasing power is essential to prevent widespread increases in economic hardship especially among workers with low earnings. The analysis of this chapter suggests that, in several sectors and countries, there is room for profits to absorb some further increases in wages to mitigate the loss of purchasing power at least for the low paid without generating significant additional price pressures. Given the downward rigidity of prices, the recent decline in input costs will also likely provide further room to absorb some wage increases without generating inflationary pressures. A fair sharing of the cost of inflation can prevent further increases in inequality and support effective monetary policy by averting feedback loops between profits, wages and prices. The next section discusses policy options to tackle the cost-of living crisis while avoiding a price‑wage spiral, focusing on wage setting institutions.