Healthcare is delivered by a wide variety of providers ranging from hospitals and medical practices to ambulatory facilities and retailers, which impact expenditure patterns for different goods and services. Analysing health spending by provider can be particularly useful when considered alongside the functional breakdown of health expenditure, giving a fuller picture of the organisation of health systems.

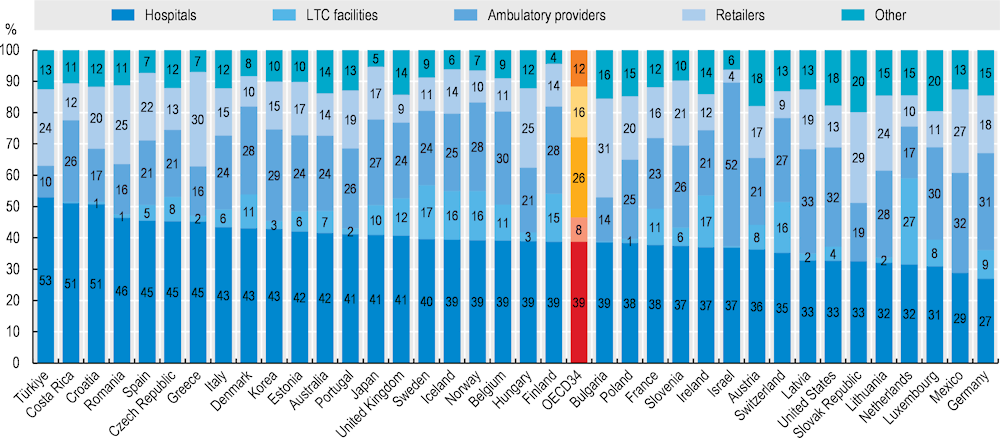

The organisational differences in healthcare delivery across OECD countries can be substantial, resulting in a wide variation in the distribution of health spending across providers. At 39%, activities delivered in hospitals accounted for the largest proportion of health system funding across the OECD. This average was largely exceeded in both Türkiye and Costa Rica where hospital activities received more than half of all financial resources (Figure 7.19). On the other hand, Germany and Mexico spent less than 30% of the total health budget on hospitals.

After hospitals, the largest provider category are ambulatory providers. This category covers a wide range of facilities with most spending related to either medical practices including GPs and specialists (e.g. Austria, France and Germany) or ambulatory healthcare centres (e.g. Finland, Ireland and Sweden). Across OECD countries, care delivered by ambulatory providers accounts for around a quarter of all health spending on average – within this, around two‑thirds of all spending relates to GP, specialist practices and ambulatory healthcare centres, and roughly one‑fifth relate to dental practices. Overall, spending on ambulatory providers exceeded half of total health spending in Israel in 2021 and reached one‑third in Latvia but remained at 10% in Türkiye and below 20% in Greece, the Netherlands and the Slovak Republic.

Other main provider categories include retailers (mainly pharmacies) which accounted for 16% of all health spending and residential long-term care facilities (mainly providing inpatient care to dependent people), to which 8% of the total health spending can be attributed.

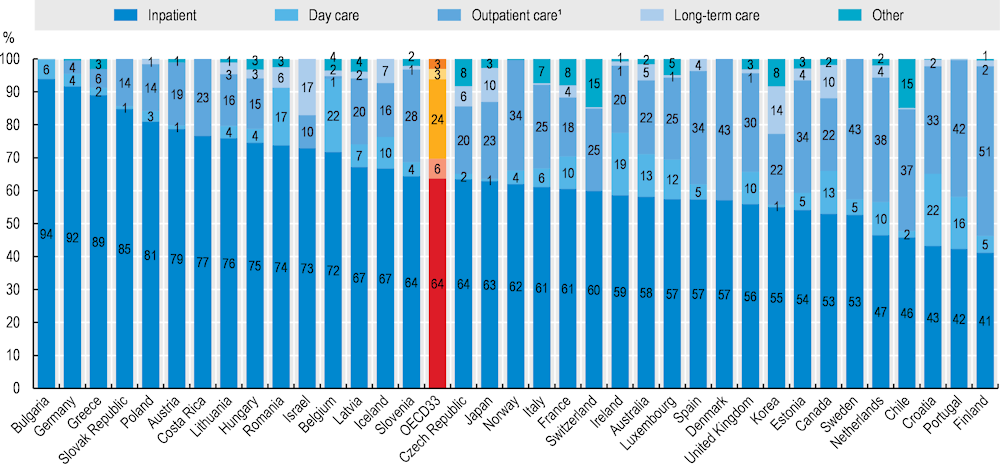

Across OECD countries, there is a wide variation in the range of activities that may be performed by the same category of provider, reflecting differences in the structure and organisation of health systems. These cross-country differences are most pronounced in the hospital sector (Figure 7.20). Although inpatient curative and rehabilitative care define the primary activity of hospitals and therefore represent the majority of their expenditure, hospitals can also be important providers of outpatient care in many countries, for example through accident and emergency departments, specialist outpatient units, or laboratory and imaging services. In Finland, Denmark, Sweden and Portugal, outpatient care accounts for over 40% of hospital expenditure since specialists are typically receiving patients in hospital outpatient departments. On the other hand, in Germany and Greece, hospitals are generally mono-functional with the vast majority (around 90%) of spending on inpatient care services, and very little outpatient and day care spending. Over the last decade, many countries have shifted some inpatient services to day care departments aiming at potential efficiency gains and a reduction in waiting times. As a result, day care services account for more than 15% of all hospital expenditures in Belgium, Ireland and Portugal.

Measures taken to address the COVID‑19 pandemic have also affected the provider distribution of health spending. In 2020, the proportion of resources allocated to hospitals increased to 40% reflecting higher input costs of inpatient service delivery and important financial support targeted at hospitals. This share dropped again in 2021 with a reduced need for hospital subsidies. Interestingly, while the outbreak of the health emergency has led to major disruptions in the service delivery in hospitals, the spending distribution by type of service remained relatively stable in most countries.